DHC - Diversified Healthcare Trust: A Long Way To Justifying The 13% Yielding Debt

Summary

- Diversified Healthcare Trust is a senior housing/medical office REIT that has experienced significant operational challenges through the pandemic.

- The company's fourth quarter earnings report showed progress on its largest division, senior housing.

- Despite the progress, the company's cash burn combined with its ambitions leave me on the sidelines as an investor.

Diversified Healthcare Trust (DHC) reported full-year 2022 earnings earlier this week. The company saw shares spike in response to the earnings report and their debt prices rallied as well. The company's debt is currently trading between 9% and 13.5% yield to maturity. Despite the optimism surrounding the earnings report, I'm still avoiding investing in shares or debt and have serious concerns about the future of the business.

{kind=link}

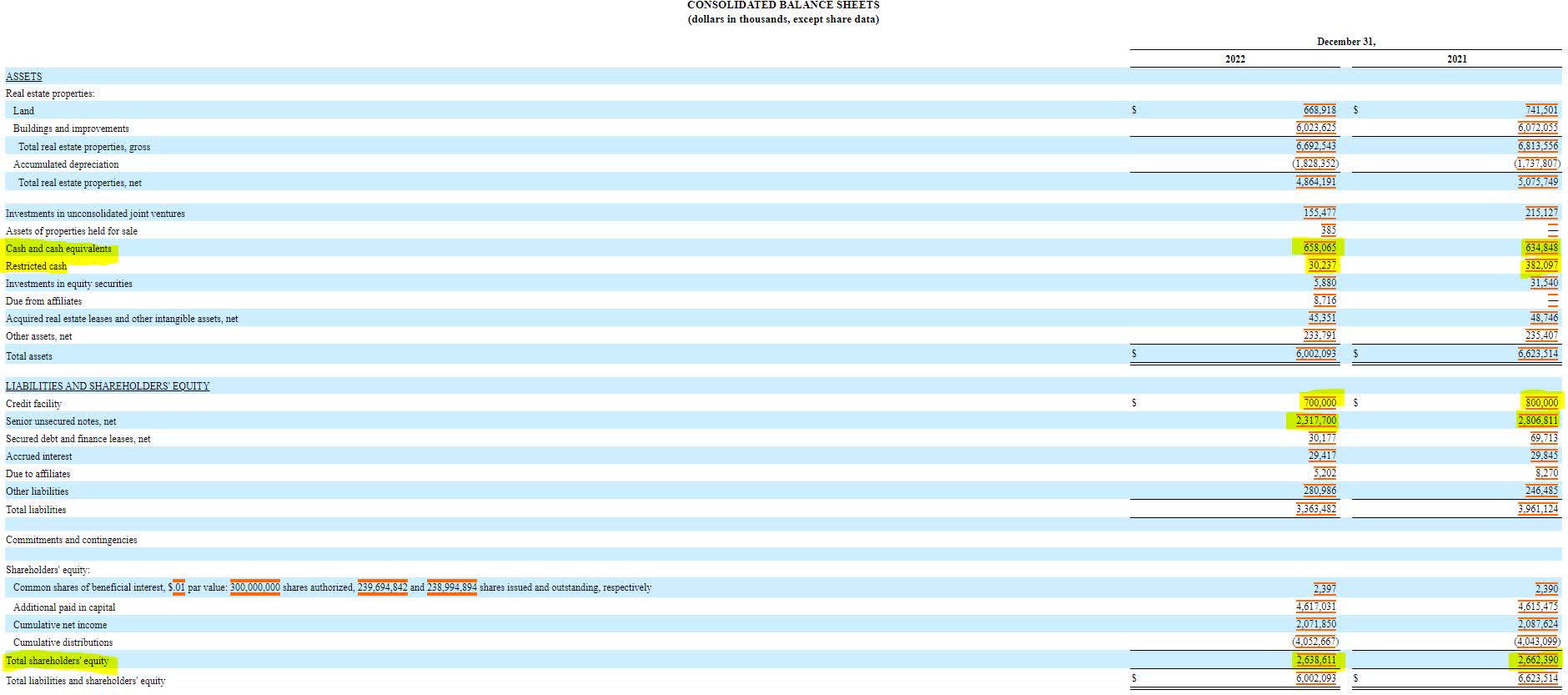

Diversified Healthcare's income statement shows continued headwinds for the company in 2022. Revenue dropped by $100 million, and expenses only declined by $37 million. Even more concerning is that the company's operating expenses, which represents a supermajority of total expenses, increased in 2022 as DHC fought against wage and inflationary pressures. Overall, the company was in the red before an interest expense of $209 million. While showing improvement in the fourth quarter, the company's senior housing division ((SHOP)) continued dragging earnings down by generating only 5% of the company's NOI while constituting 62% of the assets.

{kind=link}

{kind=link}

From a balance sheet perspective, shareholder equity remained relatively stable in 2022 at $2.6 billion. The company achieved this by utilizing some asset sales and restricted cash to pay down debt. Total debt levels fell from $3.6 billion to $3 billion. Many proponents of the company will point to the level of shareholder equity or unencumbered assets as a strength for the company going forward, which I will address later on.

{kind=link}

Diversified Healthcare's cash flow statement represents the most important report for potential fixed income investors. The report provides the company's ability to use cash generated from operations to fund capital expenditures and to reduce debt. Unfortunately, Diversified Healthcare burned $40 million in cash from operations alone in 2022 and after capital expenditures, burned nearly $340 million. Even worse, by comparing the Q4 report to the Q3 report, Diversified Healthcare has burned operating cash flow in the fourth quarter, showing that the turnaround is far from complete.

{kind=link}

{kind=link}

{kind=link}

While the company had $688 million of cash on hand at the end of the year, investors should look at another factor hurting liquidity (beyond $300 million in negative free cash flow). The company has a credit facility that's fully tapped out. During 2022, Diversified Healthcare negotiated a paydown of that line in exchange for waivers from a covenant violation. After the financial report, the company had to negotiate the revolving line again with a $136 million reduction and paydown of the revolving credit facility. This means that the business currently is down to $550 million in cash with no additional sources of liquidity. The revolving line of credit also bears an interest rate of 7.2%.

{kind=link}

{kind=link}

{kind=link}

Looking ahead, Diversified Healthcare Trust has two mountains to face. First, 21% of the company's leases are set to expire before the end of next year. These leases represent 19% of total income. While some investors may look at this as a bullish signal, it will be much harder to negotiate inflationary lease renewals if we fall into a recession. Next, the company also has $750 million in debt coming due by 2025. While cash on hand may be able to cover the $250 million coming due in 2024, the company is going to need external financing the cover the 2025 maturity.

{kind=link}

{kind=link}

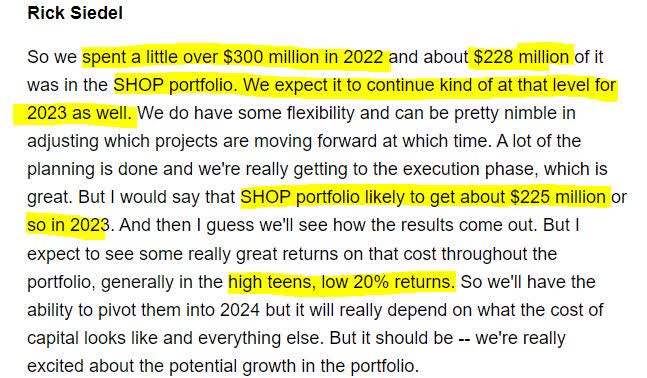

Where I get concerned further is how much capex the company is planning to spend in 2023 and 2024. On the earnings call , management discussed capex being around in the $220 million range per year in 2023 and 2024 for the SHOP segment alone. In another part of the call, they mentioned many properties getting capex renovations next year. Through these commitments, the company is pledging almost all its remaining cash to capital in the next two years and renovations are notorious for creating short-term disruptions to occupancy in senior living.

Earnings Transcript

{kind=link}

Beyond the wild cash burn and ambitious capital plans, the company fails the reverse stress test. By looking at office occupancy and SHOP occupancy, I've determined that in the best-case scenario, the company would generate $250 million in new cash flow by becoming fully occupied. This rosy scenario would bring it close to free cash flow breakeven, but still leave the company incapable of paying down debt.

Earnings Transcript Earnings Transcript

This leads us to the final problem, which is the inevitable raising of capital funds. As has been mentioned in the comments of my previous article and in the latest earnings call itself, Diversified Health Care Trust has billions of dollars of unencumbered assets. It's important to realize that having unencumbered assets and a financier lined up to lend against those unencumbered assets are two totally distinct things, especially in this rate environment. The fact that the revolving line of credit lender had to reduce its exposure to waive a covenant violation speaks loudly enough about access to future capital.

While the fourth quarter report showed progress, and the distress in the company's shares began to alleviate, investors need to keep in mind that Diversified Healthcare Trust has substantial financial problems and lofty capital expenditure ambitions. I'm expecting, at a minimum, for the company to attempt a distressed debt exchange in lieu of restructuring, and I'm not willing to take on that risk.

For further details see:

Diversified Healthcare Trust: A Long Way To Justifying The 13% Yielding Debt