DHC - Diversified Healthcare Trust Bonds: Too Risky Even At 17% Yields

Summary

- Diversified Healthcare Trust is a REIT specializing in senior living.

- The company has underperformed for at least the last two years.

- Diversified is becoming more dependent on asset sales to repay debt maturities.

Diversified Healthcare Trust ( DHC ) is a REIT that specializes in the ownership of senior living properties. The company's debt, rated on the higher end of the junk spectrum, recently saw yields top 17% to maturity for its bonds due in 2028. While this BB rated bond may be more than 1,000 basis points higher than the BB corporate index , there are significant risk factors that warrant discouraging an investment.

{kind=link}

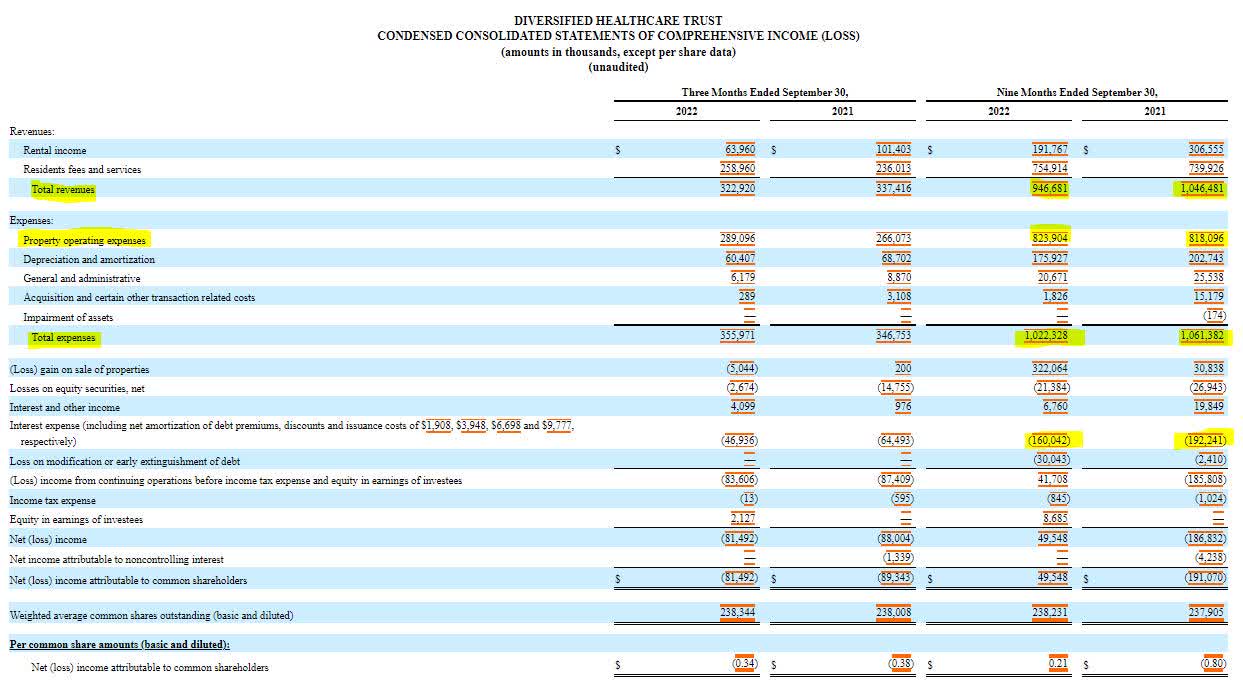

Diversified Healthcare has been operating at a loss for at least the last two fiscal years. In fact, its 2022 year-to-date performance is far worse than the same period a year ago, driven by a $100 million decline in revenue. The company's expenses were $75 million greater than revenue, and that did not include the $160 million interest expense on its debt. The only saving grace here was a $322 million gain on the sale of properties, but as I often write, a highly leveraged company can only dodge trouble for a limited amount of time by selling assets.

{kind=link}

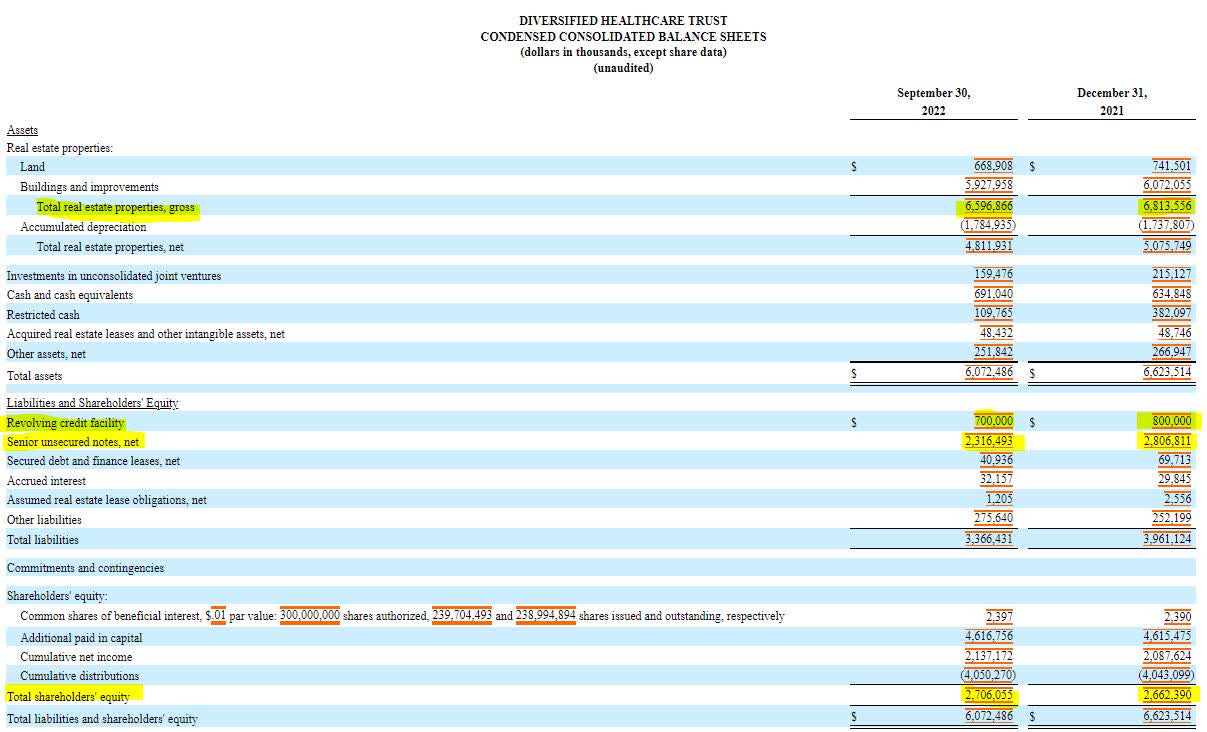

Diversified Healthcare's balance sheet does show modest improvement in 2022. Presumably, through the sale of assets and the reduction of restricted cash, the company has been able to pay down its debt by approximately $600 million. In fact, the company's equity position improved in 2022, but the assets are only as valuable as their ability to perform.

{kind=link}

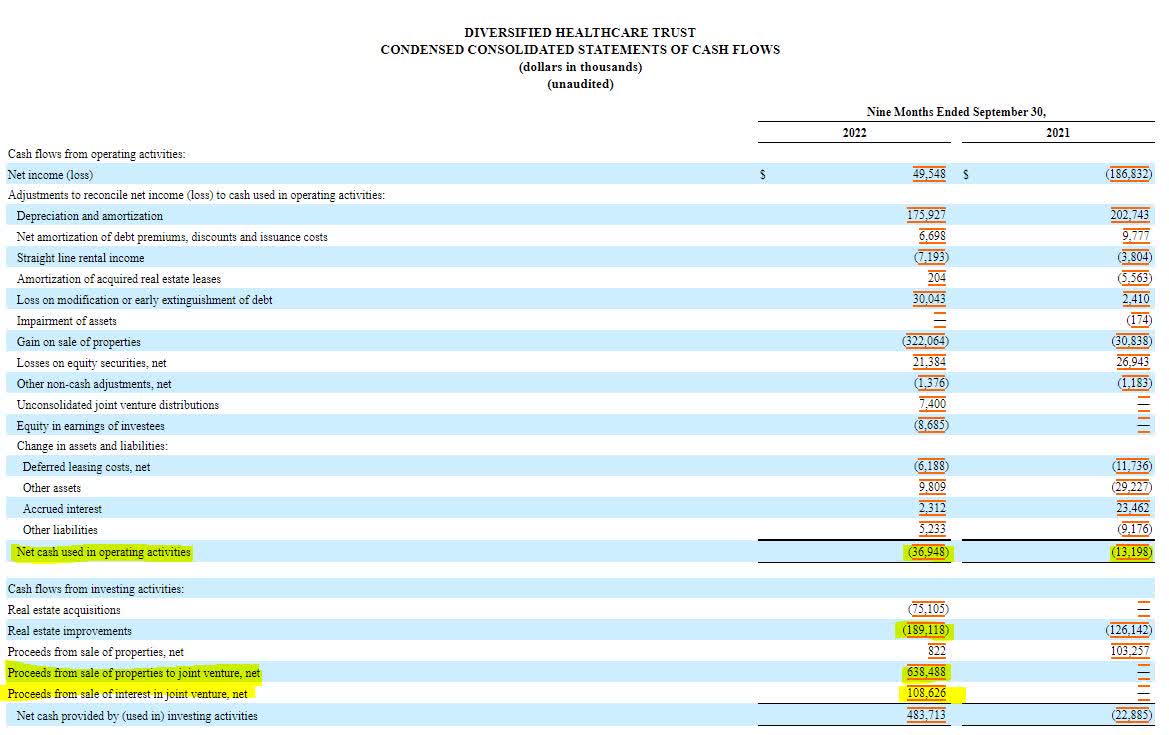

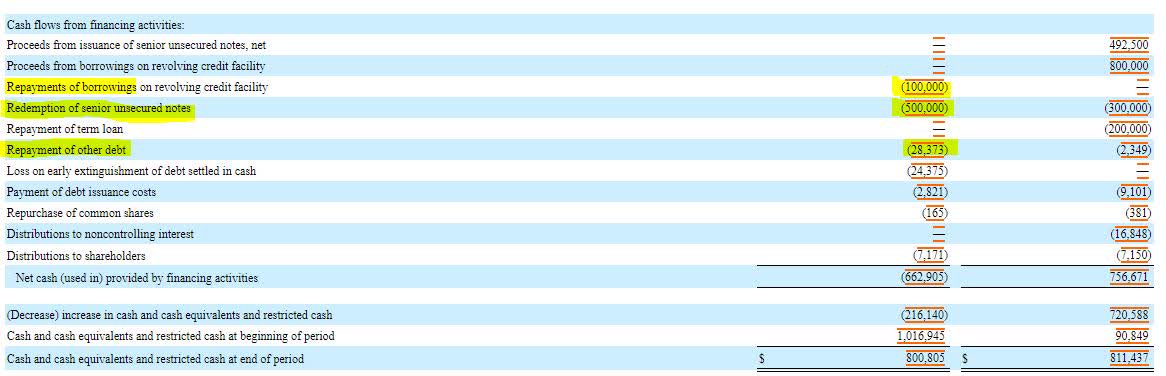

From a cash flow generation standpoint, Diversified Healthcare saw a regression in performance in 2022 as well. The company used $37 million in cash to operate year to date and dedicated $189 million to real estate improvements. To pay down debt, the company sold properties to a joint venture and sold off ownership in a joint venture. Had these transactions not occurred, the company would have burned its cash position from $1 billion at the beginning of the year to around $60 million at year-end. The cash burn is a considerable problem that the company needs to improve before its debt should be considered investable.

{kind=link}

{kind=link}

Diversified does have some things going for it. The company's current cash position is enough to cover debt maturities coming due in 2024 and 2025, but that only helps if they don't need to burn cash to finance operating losses. Their maturity wall becomes manageable, and their interest expenses would be greatly reduced if they were able to pay off the 2024 and 2025 maturing bonds without refinancing.

{kind=link}

Management of Diversified Healthcare Trust has been optimistic as well. In the third quarter financial filing, they stated that they believed they would have access to various types of financings to cover debts and obligations as they come due. The company also provided an exhibit demonstrating it had collateral available by comparing indebtedness against the net value of real estate properties.

{kind=link}

{kind=link}

But in the same report, management points out that the company's line of credit is being reduced in size once the maturity is extended for a year. As part of that refinancing and subsequent downsizing, the company will likely be forced to come up with $113 million to pay down its line to the new borrowing capacity. A "margin call" on revolving lines of credit has always been a red flag when it comes to gauging a company's ability to attract outside capital or loans.

{kind=link}

Diversified Healthcare's saving grace is to improve or divest from its largest revenue segment, senior housing. While senior housing accounts for 80% of the company's revenue, the space is underperforming on occupancy at 75%. Occupancy improvements would obviously help the company, but selling underperforming properties might speed up the turnaround process. The progress in senior living is not helped by the fact that the company has had a setback in office occupancy, as the entire sector has taken a hit.

{kind=link}

{kind=link}

Investing in Diversified Healthcare's debt does bring the risk of loss outside of bankruptcy. Should the company be unable to find outside investment and want to avoid bankruptcy, they may go to their bondholders and offer a distressed debt exchange. The offer would have to be low enough to tolerate the high interest rate on the new issue of bonds. Due to these factors, I am avoiding investing in Diversified Healthcare's debt until I see material improvement in its performance.

For further details see:

Diversified Healthcare Trust Bonds: Too Risky, Even At 17% Yields