CARR - Divestitures Innovation And Climate Trends - Carrier Is An Impressive Wealth Compounder

2023-12-08 14:44:29 ET

Summary

- Carrier Global is reshaping itself into a "climate" powerhouse by focusing on its core businesses and divesting non-core assets.

- The company has announced the sale of its security business to Honeywell for $5 billion, allowing it to reduce debt and focus on its core operations.

- Carrier's acquisition of Viessmann positions it to capitalize on the growing demand for heat pumps in Europe's decarbonization movement.

Introduction

Carrier Global ( CARR ) is one of the most fascinating stocks on my radar.

As most of its investors know, it used to be a part of United Technologies, which spun off both Carrier Global and Otis Worldwide ( OTIS ) in 2020 when United Technologies merged with Raytheon, forming one of the world's largest aerospace & defense companies, RTX Corp. ( RTX ).

In the realm of spin-offs, I believe every single one of the aforementioned deals was fantastic for shareholder value.

I started covering Carrier in 1Q22. Since then, I have written a number of articles with very bullish titles.

{kind=link}

Seeking Alpha

I find Carrier's business strategy fascinating. It not only benefits from strong market trends like heat pumps, building automation, high demand for aftermarket products, and related services but also focuses on its core businesses by spinning off non-core holdings to emphasize margins and increase shareholder value.

In this article, I'll update my bull case, using its latest earnings, its comments during the Bair Global Industrial Conference, and above all, the just-announced multi-billion dollar sale of its Security business to Honeywell ( HON ).

So, let's get to it!

Carrier Is Reshaping Itself Into A "Climate" Powerhouse

Earlier this year, Carrier's segment overview looked like this:

Carrier Global

The company makes most of its money in the HVAC business, followed by $4 billion in annual sales in both the Fire & Security and Refrigeration segments.

In my prior article , I wrote that the company had made the decision to combine the commercial and residential fire businesses into a single capital markets transaction, set to be listed in late spring or early summer of 2024.

More recently, in its third-quarter earnings call, the company said it is actively advancing its business divestitures.

The company had stated that they engaged renowned advisors such as Goldman Sachs, JPMorgan for Fire & Security, and Bank of America for commercial refrigeration to handle the process of divesting.

It noted that there is significant interest in the divestiture assets, particularly in security, commercial refrigeration, and industrial fire.

The company didn't lie, as it just revealed a major deal with Honeywell.

{kind=link}

Bloomberg

Honeywell is buying Carrier's security business for $5 billion, including debt. This is the biggest deal for Honeywell since 2015.

As I have covered both Carrier and Honeywell, I believe this is a match made in heaven.

Honeywell's new CEO is tasked with finding new sources of growth and re-positioning Honeywell for a future based on a number of megatrends, as I discussed in this article .

Meanwhile, Carrier wants to get rid of non-core assets to focus on its bread and butter.

According to Carrier (emphasis added):

Carrier Global Corporation, global leader in intelligent climate and energy solutions, entered into a definitive agreement today to sell its security business, Global Access Solutions, which includes the industry-leading brands of LenelS2, Supra and Onity, to Honeywell for an enterprise value of $4.95 billion, which represents approximately 17x 2023 expected EBITDA . The sale agreement is a successful first step in Carrier's portfolio transformation.

Not only does Honeywell get fantastic assets with strong growth (this segment saw 5% order growth in 3Q23), but it also allows Carrier to reduce debt after its major Viessmann deal for $13 billion in cash and stock.

Carrier expects the net proceeds of the deal to be roughly $4 billion, which will be used to reduce debt to a 2x (EBITDA) leverage target. Once it has achieved this target, it will restart share buybacks.

What's interesting is that even before the deal, analysts expected the company to reduce net debt to $2.3 billion by the end of 2024, meaning that repurchases will likely resume somewhere in the middle of 2024, as that would imply a sub-1x net leverage ratio.

Additionally, the company can now fully focus on incorporating Viessmann into its business.

As I have discussed in prior articles, Viessmann Climate Solutions is well-aligned with the forced trend toward heat pumps in Europe, a trend expected to persist for years.

The European decarbonization movement is supported by government regulations and funding commitments, providing a multiyear growth opportunity, which is why I like to call these trends "forced trends."

On December 8, PV Magazine reported that the EU is likely to phase out fossil fuel-powered boilers by 2040!

Fossil fuel-powered boilers will be phased out in a “gradual manner” by 2040 if a European Parliament and European Council provisional agreement reached yesterday is formally adopted.

The European Commission said if the agreement is formally supported, fossil fuel boiler installation subsidies will also cease by 2025 and publicly owned buildings will need to produce zero on-site emissions by 2028, with every other type of building expected to reach zero on-site emissions by 2030.

Brussels-based heat pump association EHPA – which calls for heat pumps to be the “ number one ” heating and cooling choice by 2030 – supports the announcement.

Buying Viessmann was a no-brainer deal that would allow Carrier to get a big chunk of this market, with support from governments pushing for this new technology.

{kind=link}

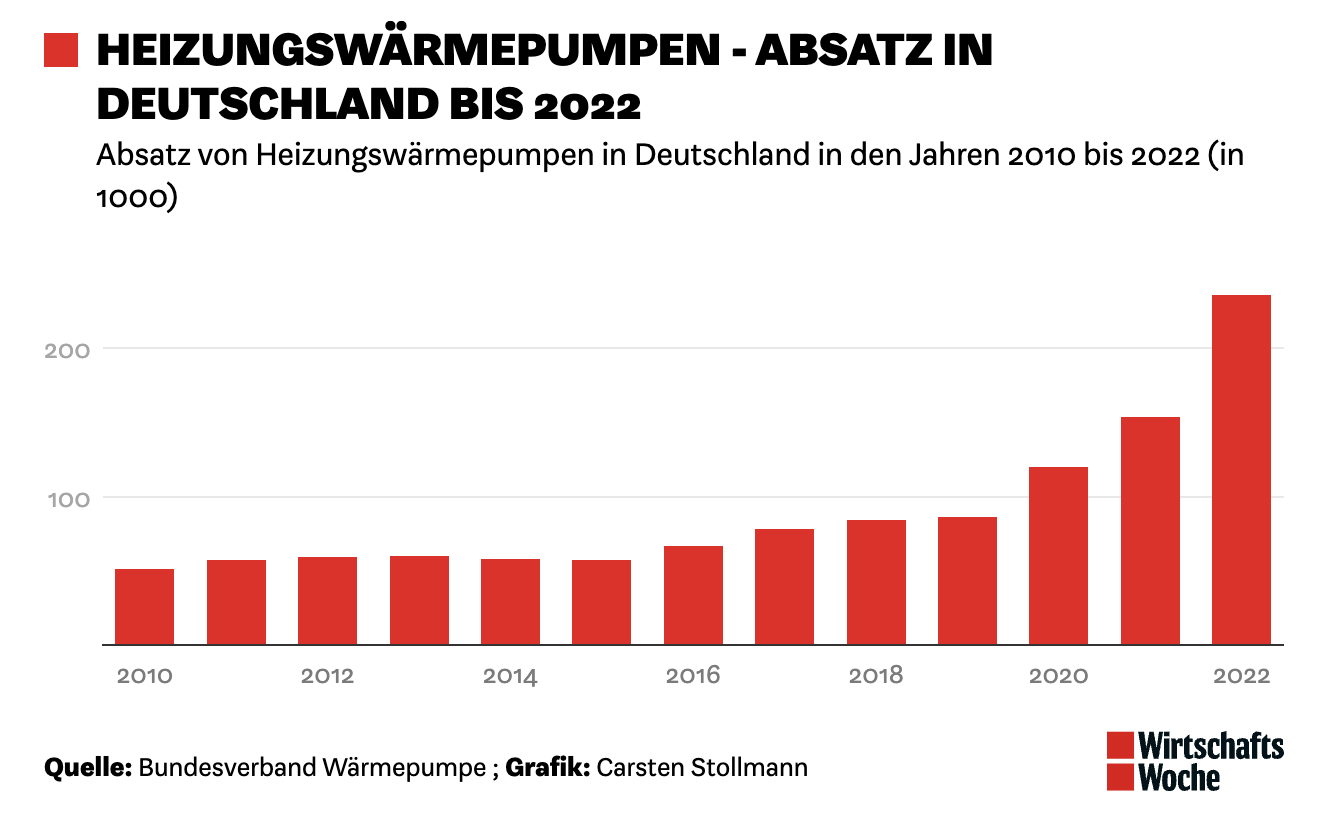

WirtschaftsWoche

In Germany alone, sales of heat pumps more than doubled between 2019 and 2022, promoting the question of why Viessmann agreed to be bought in the first place.

After all, if you know you're operating in a strong market with the right product, why sell?

Viessmann obviously knew about its strengths. However, it always believed that partnering (or being bought by) a large global corporation would unlock massive economies of scale, thereby protecting jobs in Germany as well.

Furthermore, Viessmann Climate Solutions distinguishes itself by providing solutions across all energy classes, including heat pumps, gas boilers, and hydrogen boilers.

This diversified approach positions it favorably compared to competitors that specialize in a single energy class. It also reduces risks.

Meanwhile, the connected ecosystem offers a range of solutions for electric homes, such as solar PV, batteries, and a differentiated digital platform.

Recent product introductions, including the OptimaLINE refrigerated container unit and high-temperature heat pumps, showcase Viessmann's commitment to innovation.

Awards, such as the Vitocal 250-A natural refrigerant air-to-water heat pump, reinforce its position as an industry leader.

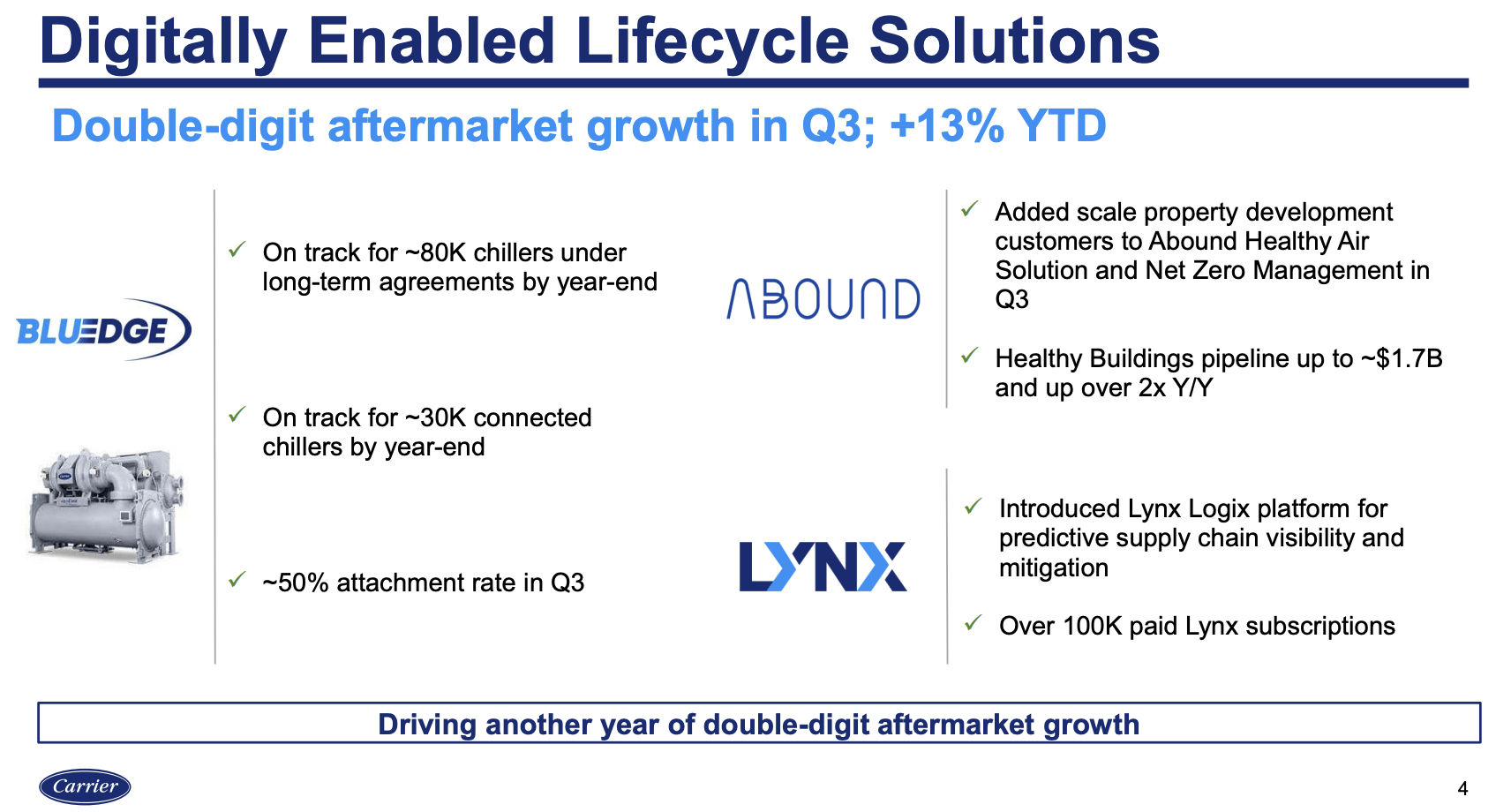

In general, Carrier is making tremendous progress in growing digitally-enabled products.

{kind=link}

Carrier Global

Its current platform will allow the company to become a provider of complete energy management solutions in the Americas, Europe, and Asia Pacific, using its core brand, Carrier, and subsidiaries like Viessmann and Toshiba Carrier.

Carrier Global

But wait, there's more!

During the aforementioned industrial conference, the company talked about its acquisition of Giwee.

This strategic step positions Carrier to tap into the Chinese market, benefitting from Giwee's growth prospects and technological advancements.

Meanwhile, the acquisition of Toshiba Carrier in Japan further bolsters Carrier's position in the global HVAC market.

This move not only brings growth prospects but also contributes valuable technological advancements.

Earlier this year, the company's products in Japan were awarded for their efficiency enhancements.

Toshiba Carrier has been recognized at the 2023 National Invention Awards of Japan for its innovative discharge port structure in multi-cylinder rotary piston compressors for heat pumps. The technology tackles the problem of overheating, resulting in improved heating capacity and efficiency.

So, what does this mean for shareholders?

Tremendous Shareholder Value

Taking a step back, the company did well in its third quarter. Total sales increased by 5% year-over-year.

Unfortunately, the global economy is witnessing a manufacturing slowdown.

This is also impacting Carrier.

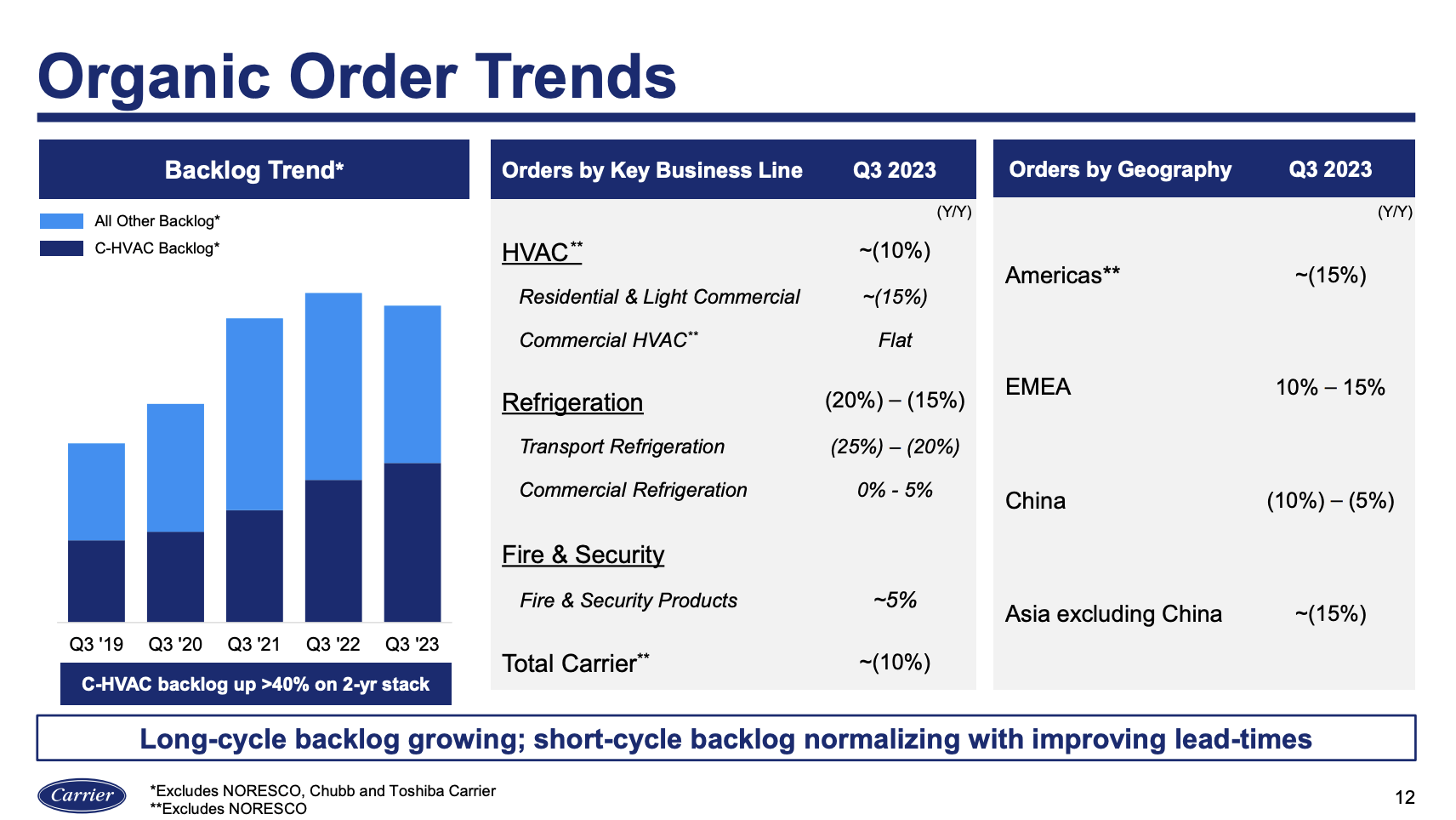

Total company orders decreased by roughly 10% in the third quarter, primarily due to declines in shorter-cycle businesses.

HVAC orders were down about 10%, while Refrigeration orders declined by approximately 15% to 20%.

{kind=link}

Carrier Global

Nonetheless, the backlog remained robust, up over 40% on a 2-year stack, extending well into next year.

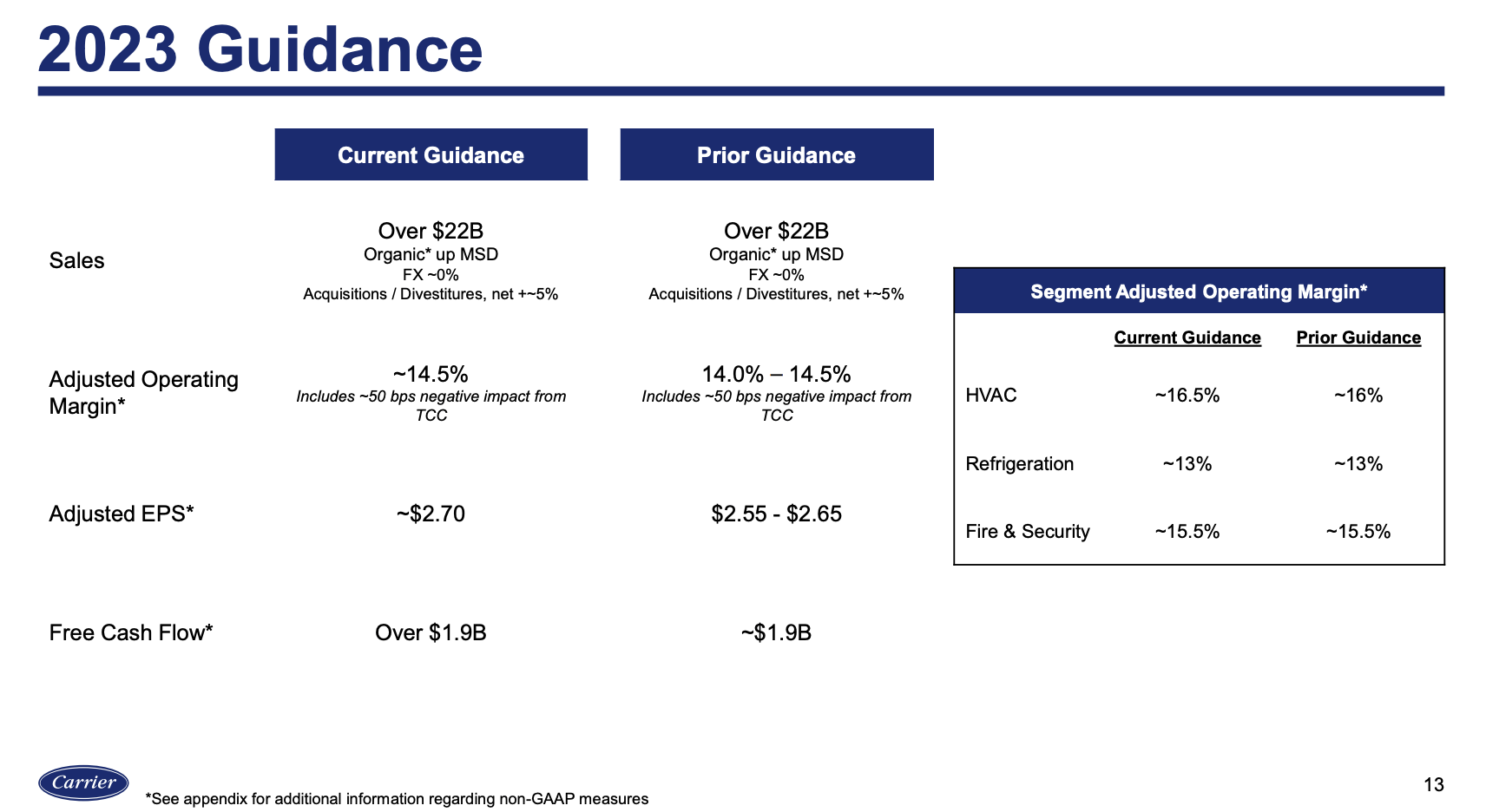

Despite these headwinds, the company reported good guidance. Please bear in mind that this is before the deal with Honeywell. Nonetheless, both the Viessmann and Honeywell deals are not closing in 2023.

As of the third quarter, the company expected full-year sales to be around $22 billion to $22.2 billion, including mid-single-digits organic sales growth.

- Adjusted operating margin guidance was raised to about 14.5%, with specific increases in HVAC adjusted operating margin to about 16.5%.

- Adjusted EPS guidance was raised by $0.10 to about $2.70.

- Free cash flow for 2023 is now expected to be slightly more than $1.9 billion.

{kind=link}

Carrier Global

In February of 2024, the company will provide new guidance, focusing on Viessmann and other deals.

With this in mind, Carrier brings a lot of value to the table.

On December 6, the company hiked its dividend to $0.19 per share. This translates to an annualized yield of 1.4%.

Last year, the company hiked its dividend by 23%.

The company is clearly playing it safe, as it is about to generate $1.9 billion in free cash flow this year. This translates to a free cash flow yield of 4.3%.

In other words, the company could have easily hiked again by 23%.

However, debt reduction is more important.

Hence, what matters here is how much cash the company can distribute once it is satisfied with its debt levels.

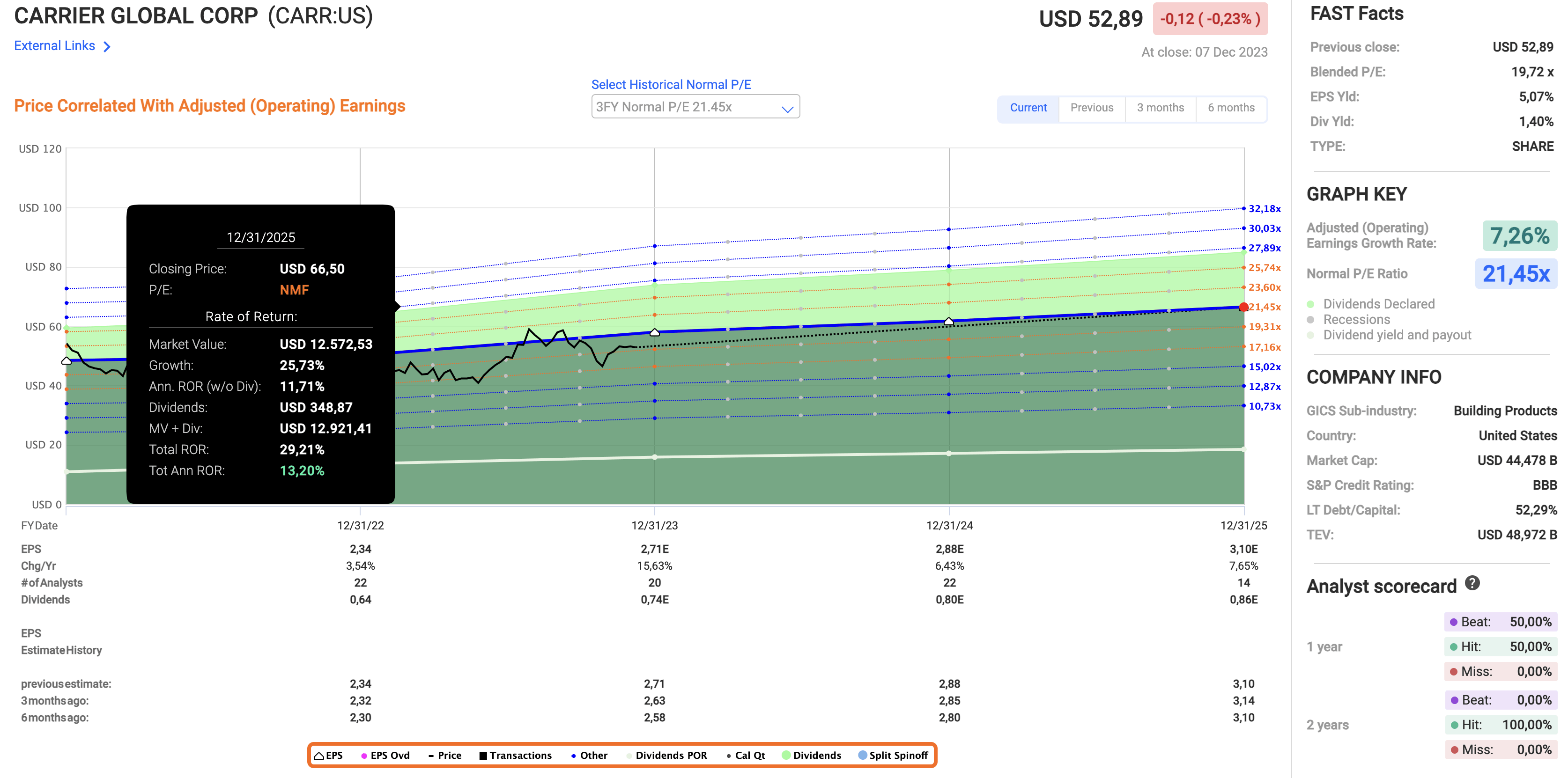

The valuation isn't bad, either.

Using the data in the chart below:

- Carrier is currently trading at a blended P/E ratio of 19.7x.

- The historic normalized valuation is 21.5x earnings. Although the company's history is very limited, I believe that's a fair long-term valuation.

- In the next two years, annual EPS growth is expected to average roughly 7%. I expect that to last on a longer-term basis.

- Despite slower economic growth, estimates for 2023 and 2024 have been hiked over the past six months, while 2025 estimates have remained unchanged.

{kind=link}

FAST Graphs

Based on the numbers above, CARR should be able to return between 10% and 13% per year, including dividends.

Although these numbers are subject to change, I really like the long-term risk/reward and believe that Carrier is in a fantastic spot to benefit from long-term secular growth in its core markets and its ability to capitalize on this through innovation, higher margins, and smart M&A projects.

On top of that, I expect dividend growth and buybacks to play an increasingly meaningful part in the long-term total return.

Takeaway

In the dynamic world of climate and energy solutions, Carrier emerges as a compelling investment opportunity.

The recent $5 billion sale of its security business to Honeywell underscores Carrier's strategic focus on shedding non-core assets, reducing debt, and driving shareholder value.

Meanwhile, the acquisition of Viessmann positions Carrier at the forefront of Europe's decarbonization movement, capitalizing on the rising demand for heat pumps.

Moreover, strategic moves like the acquisition of Giwee in China and Toshiba Carrier in Japan demonstrate Carrier's global expansion and technological advantage.

Despite short-term challenges, the company's robust backlog, increased guidance, and shareholder-friendly initiatives, such as dividend hikes and future share buybacks, reinforce confidence in Carrier's long-term potential.

As it navigates market trends with innovation and efficiency, Carrier stands poised for sustained growth and shareholder returns.

For further details see:

Divestitures, Innovation And Climate Trends - Carrier Is An Impressive Wealth Compounder