HQH - Dividend Cut On The Horizon? Not So Fast Ol' Sport

Summary

- So many react without thinking, don't make their mistake.

- To be a skilled income investor, you must digest the news and understand it.

- We look at yields up to 8% as we dig deeper.

Co-produced with Treading Softly

Have you ever met someone with a terrible habit of jumping the gun? They hear half of a rumor, they fill in the blanks in their mind and spread it to everyone they know. Spreading misinformation, not through intentional dishonesty, but because they didn't take the time to verify it.

I had one such friend assure me with absolute confidence that Elon Musk was buying Google - ( GOOG , GOOGL ). I tried to tell them it was Twitter ( TWTR ) and that the deal wasn't closed yet, but they assured me I was wrong. They saw a headline on TV and misinterpreted it.

Investors are often like that friend. They hear news and react immediately, without absorbing or digesting the information. This can be called a "buy the rumor, sell the news" event. The market initially reacts in one direction, but then when the news is analyzed the price starts going the other way. We see a lot of this during earnings season.

For various reasons, distribution-paying companies and funds can be bid higher into exuberance or sell off wildly in fear. Today, I want us to take a step back, and instead of being that hair-triggered, half-cocked, overly reactive friend, let's be like the seasoned captain sailing through a storm. He knows where he is going and what he is doing and charts his course accordingly. Knowing that even if the ship is knocked off-course by the occasional wave, only small adjustments are needed.

Variable dividends and tenant fears are driving these excellent opportunities to appear while being overblown and nothing major for the long-term investor.

Let's dive in.

Pick #1: HQH - Yield 9%

Tekla Healthcare Investors ( HQH ) is a closed-end fund ("CEF") that focuses on healthcare, with a high allocation to pharmaceuticals and biotech. During the COVID years, traders bid up prices on anything vaccine-related and then cut and ran as traders are prone to do.

Fundamentally, pharmaceuticals and biotech are in a great position. The U.S. population is aging, and along with age comes more use of medications. HQH is invested in companies that were very successful long before COVID existed. ( Source: HQH Website )

HQH Website

HQH has exposure to big names like Amgen ( AMGN ), Vertex ( VRTX ), Gilead ( GILD ), and more. Companies that will play a large role in providing products to the aging U.S. population.

HQH has been investing in the sector since the late 1980s. You know, the last time inflation was this high. Since its inception, HQH has outperformed the S&P 500.

However, that is not the full story, where did these returns come from? When we look at HQH's price gains, compared to total return, we can see something common for long-term CEFs. Virtually all of the total return came from dividends.

Over 40+ years, HQH's price has been up, it has been down, and all over the place. This can matter greatly in the short term when looking at a chart covering the last 5 years. Over longer periods, HQH's dividends account for over 95% of total returns.

HQH has a variable dividend policy, paying out 2% of net assets each quarter. This means that the dividend will follow NAV, going up and down as NAV changes. Healthcare joined the general market selling off over the summer and is now very attractively valued to buy for the recovery.

Pick #2: EPR - Yield 7.7%

EPR Properties ( EPR ) saw a significant sell-off recently. This was in conjunction with news from Cineworld, the parent company of Regal, EPR's second-largest tenant. The sell-off is clearly an overreaction and we remain very confident with EPR. However, the market is likely to remain bearish in the near term until there is more certainty. Let's look at the SEC filings that sparked this sell-off.

First, the news from Cineworld (emphasis ours):

In connection with these initiatives, the Group remains in active discussions with various stakeholders and is evaluating various strategic options to both obtain additional liquidity and potentially restructure its balance sheet through a comprehensive deleveraging transaction. Any deleveraging transaction will likely result in very significant dilution of existing equity interests in Cineworld.

The Group's business operations are expected to remain unaffected by these efforts and Cineworld expects to continue to meet its ongoing business counterparty obligations. Cineworld continues to welcome guests to its cinemas across its global markets as normal, without disruption.

The market read this and naturally, Cineworld's stock tanked to virtually worthless, as it absolutely should. After all, Cineworld just informed shareholders they expect a "very significant" dilution of the existing shares.

The market also started selling off EPR under the logic "the tenant is in trouble! sell !" Let's be clear: if Cineworld stops paying rent, that would be a material disruption for EPR. Given its current conservative payout ratio and strong balance sheet position, the dividend would likely be maintained, but funds from operations ("FFO") would come down and the future dividend raises we expect would be delayed. It wouldn't be great for the stock price.

However, when there is a filing, we have to read the filing. What does it say? It says:

- They expect a "comprehensive deleveraging transaction" that will result in "substantial dilution of existing equity interests".

- "Cineworld expects to continue to meet its ongoing business counterparty obligation" - The rent they pay to EPR is an "ongoing business counterparty obligation".

In other words, Cineworld does not expect to default on its operating obligations, such as rent . The Wall Street Journal is reporting that Cineworld is likely to file bankruptcy.

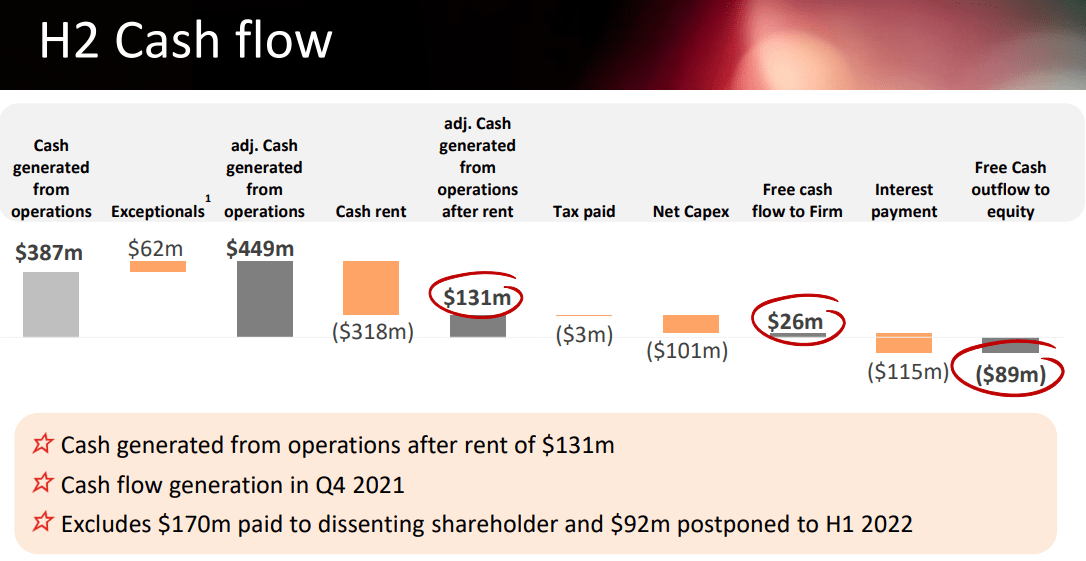

The main concern for EPR investors needs to be whether Cineworld can cover its rent. Here is a look at the second half of 2021. ( Source: Cineworld Group Presentation )

{kind=link}

Cineworld covered its rent with cash from operations by 1.4x. Not spectacular, but they are earning enough to cover rent. The problem comes in with the $115 million/half in interest payments. Cineworld's debt went from $3.5 billion pre-COVID to over $5 billion. Interest expense went from $167 million/year to $230 million/year and climbing.

Looking at it from the lender's standpoint, you either pay rent or there is no building. A tenant can't "force" a landlord to reduce rent. A tenant has no right to a building without paying rent in full as agreed. For a business like the movies, without the building, there is no cash flow. Before interest payments, that cash flow is positive. At the property level, the company is profitable.

The lenders don't want the properties to close down, they want that revenue. Hence why they are talking about restructuring and giving what would likely be substantially all of the equity to lenders.

There is positive cash flow, and the company is profitable at the property level, so there is little reason (and little leverage) for Cineworld to play hardball with landlords.

This was quickly confirmed when EPR issued an 8-K stating:

•Regal is current on all payments due to EPR Properties as of the filing hereof.

•EPR Properties is not in current negotiations with Regal or Cineworld regarding their obligations to EPR Properties.

Cineworld hasn't even attempted to negotiate rent with EPR, which suggests that it is not something they intend to fight in court. In bankruptcy court, there are three options for tenants:

- Pay rent as agreed.

- Reject the entire lease, which means that the landlord can evict the tenant.

- Negotiate a rent reduction before court proceedings begin.

Option #2 is off the table since, without theaters, there is no company at all. It would be incredibly risky for Regal to reject the lease, which would allow EPR to tenant the best locations to the highest bidder. Option #3 is quite common, but it is notable that Cineworld could be filing for bankruptcy within weeks but hasn't even opened negotiations with EPR.

Our conclusion: This is an issue that impacts the equity holders for Cineworld, it is not expected to impact EPR's rent payments. For the past two years, there has been a risk of rent being reduced. That risk is one reason why EPR is $50, not $70/share. Cinemark's press release is ironically very good news for EPR, as it clearly indicates that rent is not up for negotiation and that the company expects to restructure which will greatly improve its cash flow and make it a more secure tenant. The worst-case scenario is further off the table than it was last week.

Yet because this risk was brought to the forefront of investors' brains, we can expect that sentiment towards EPR will be generally bearish until there is some clarity from Cineworld. If/when Cineworld actually files for bankruptcy, we could see another impact on EPR's price. In the coming weeks, we could see a fantastic buying opportunity for EPR.

The last bankruptcy EPR dealt with was Children's Learning Adventures in 2018. EPR management provided clear and upfront guidance throughout the process, resulting in a price decline for a brief period, but the dividend kept climbing. It was mostly a psychological distraction. EPR's management is top-notch, and they will be able to deal with whatever issues Regal presents. The bottom line is that the properties are essential to the business and are cash-flow positive at the property level.

We do not anticipate risk to the dividend, and we expect to hold EPR through Cineworld's reorganization

Shutterstock

Conclusion

With HQH and EPR, we have two oversold opportunities that are driven more by short-term investor sentiment than long-term fundamental issues.

HQH, with its variable distribution policy, will see its payouts rise and fall with its NAV, which in turn rises and falls on the value of its various holdings. With a long history of outperforming the market in general, and Healthcare continues to be a sector due for further recovery, we can lock in an excellent income source while it's cheap.

EPR faces the risk of a tenant going through bankruptcy, but unlike bond or debt holders, EPR's buildings are essential to whatever surviving entity emerges from this bankruptcy process. Furthermore, rent is fully covered by the recurring cash flow of this tenant at the property level. The excess is in debt at the corporate level.

Has EPR been planning and working on reducing its exposure to theaters? 100%. Will this likely continue to light the fire under management to keep that trend alive? 100%. Is the dividend at risk? Not so much. We feel the sell-off is unjustified in the long run, but as the bankruptcy process occurs or proceeds, it will continue to be a headwind to EPR's share price, giving more opportunities to add or DRIP effectively.

In retirement, when playing defense with your portfolio, one cannot afford to act blindly and reactively. You must know your positions and the reason you own them, and like that seasoned captain, steer your portfolio through the rough seas and storms life will bring about. All along, your income will be generated strongly, and the joys of life will enjoy the warm safety of your wise decisions.

Don't break apart the boat because a gust of wind brings the smell of rain about to come.

Income investing can help you and your retirement enjoy the calm seas and storms all the same. You'll be standing in a place of confidence and experience.

For further details see:

Dividend Cut On The Horizon? Not So Fast Ol' Sport