VNQ - Dividend Investing Like The Legendary Sam Zell

2023-05-26 08:45:00 ET

Summary

- Sam Zell was known as the "Grave Dancer" for buying distressed but quality assets for pennies on the dollar and selling them later at the tippy top of the market.

- Zell was a master value investor, applying standard value investing principles to the world of commercial real estate.

- We discuss three core lessons that investors (especially dividend and REIT investors) can learn from Zell's investment style and strategy.

- What would Zell buy today? I give my pitch for one particular company in an absolutely hated sector of commercial real estate.

The legendary investor Sam Zell recently passed away at the age of 81.

Although Zell called himself an "asset agnostic" investor, he is best known for his wildly successful investments in commercial real estate ("CRE"). Zell founded Equity Group Investments in 1968 as a real estate investment vehicle, and over the decades he accomplished in the CRE space what many stock investors aim to achieve in the stock market:

- He built a great fortune by buying low and selling high.

Zell became known as the "Grave Dancer" by buying dirt cheap, distressed assets that no one wanted to own and sold the same assets when they were red hot and everyone wanted to own them.

Sounds so easy, doesn't it?

Like so many investing principles, it's simple but not easy. It requires a depth of industry proficiency that takes most people a long time (and a lot of mistakes) to obtain.

Another area where Zell saw potential that others didn't was in the struggling (at the time) asset class of real estate investment trusts ("REITs") ( VNQ ). For decades after President Eisenhower enacted the law creating these publicly traded CRE investment vehicles, REITs performed poorly, attracting subpar and misaligned management teams that operated the companies for their own benefit rather than that of shareholders.

This completely defeated the Eisenhower-era idea of allowing the average, small-dollar investor to partially own and profit from high-quality CRE properties.

Zell pushed the industry to manage their businesses to create shareholder value, and he became a practitioner of this idea himself by founding multiple REITs -- first Equity Commonwealth ( EQC ) for office buildings in the mid-1980s, then Equity Residential ( EQR ) for apartments and Equity LifeStyle Properties ( ELS ) for manufactured housing in the early 1990s.

Of interest to dividend growth investors like me, Zell's shareholder-friendly real estate vehicles have also made fantastic dividend growth investments over the years.

In what follows, I want to discuss three lessons that dividend growth investors ("DGIers") can and should learn from Sam Zell's example and finish up by thinking out loud about what CRE sector Zell would be most interested in today.

But first, let's review a few examples of Zell's shrewd, audacious, and wildly successful investments.

Dancing On Skeletons

Zell once described his investment strategy as "dancing on the skeletons of other people's mistakes" in reference to the phenomenal deals available to him from others' greed, fear, and/or stupidity. This earned him the famous nickname of the "Grave Dancer."

The low interest rates of the late 1960s and early 1970s fueled a surge in CRE construction, leading multiple sectors to become overbuilt. The supply of properties outpaced demand for those properties, perhaps most notably in the multifamily space, leading to a spree of mortgage defaults and abandoned development projects. Property valuations plunged as reality set in.

Within the span of a handful of years, the market's greed and aplomb turned into fear and despondence.

Those who had ignored the fundamentals on the way up now ignored them once more on the way down as they wanted (or needed) to exit their failed investments at any price.

Zell and his business partner swooped in and bought high-quality properties for pennies on the dollar.

This is the first lesson the Grave Dancer can teach us: No matter how high-quality the asset, price always matters.

So does supply and demand. In fact, the very word "quality" in reference to an investment asset implies a favorable balance between supply and demand. Something "high-quality" can quickly be rendered mediocre or low-quality given a large enough supply of it. This is as true in the world of CRE as it is anywhere else.

In the late 1980s and early 1990s, Zell turned to buying shunned office properties at around half of their replacement value. Earlier in the 1980s, another speculative real estate boom eventually turned into a bust, contributing to weakness in the banking sector. (Sound familiar?)

Everyone became afraid of office real estate, because it was well-known to all that the sector had been overbuilt. Zell saw value in the feared and reviled, and he bought.

Almost two decades later, during another speculative frenzy in real estate in 2007, Zell sold the office portfolio he had spent a lifetime amassing to alternative asset manager Blackstone ( BX ). The price was $39 billion for 573 office buildings, the largest leveraged buyout in history.

What was significant about the year 2007? It was the year before the Great Financial Crisis, during and after which real estate once again swung from speculative euphoria to distress and despair.

Zell bought at the bottom, waited patiently for the market's mood to change (while collecting a very attractive cash yield on investment), and sold at the tippy top of the market cycle.

Zell demonstrated that there's nothing too fearsome to buy, and there's nothing too beloved to sell -- at the right price.

Once, when asked where Zell made his best CRE investments, Zell replied: "Toledo, Ohio" -- a mid-sized city with a stagnant population and few (if any) growth catalysts. Why? Price .

This is value investing 101, and Zell was a master at it.

Lesson #1: Develop An Industry Expertise

We all know that stock market prices aren't random. They are set based on investor sentiment. Generally speaking, when the outlook for a stock is strong, investors will bid the price up, and when the outlook is weak, sellers will accept lower and lower prices.

And investors aren't dumb. They are generally some of the smartest people in the world.

So how does one know when the market is right about a stock/asset/CRE sector versus when the price has fallen lower than the fundamental value?

Develop an expertise in that industry.

Zell didn't build a fortune by just guessing that the prices of CRE would rebound. Most of the time, CRE property prices are determined by the net operating income ("NOI") they produce, which means that you can't just get lucky in CRE investing by buying something cheap and then waiting for investor sentiment to come around. Almost always, if there's no demand from tenants, there won't be any demand from investors either.

Zell was able to buy low and sell high in his CRE investments because he had a deep expertise in the industry and asset type. He understood practically how to make money in CRE, and through this knowledge, he recognized when asset prices were too low and when they were too high.

Financial metrics are useful, but if you rely solely on metrics without knowledge of industry fundamentals, you're no better off than any other investor.

Everyone nowadays has instant access to financial metrics. Not everyone has industry expertise.

The former isn't an edge. The latter is .

Lesson #2: Learn To (Selectively) Love The Hated

If you have developed an expertise in a certain industry, it is much easier to spot false narratives and overblown investor sentiment within that industry.

This is the difference between buying Bed Bath & Beyond (BBBYQ) because it looks dirt cheap (then crossing your fingers and hoping for the best) and making long-term investments in bruised but fundamentally sound assets or companies.

Although it is in parentheses, the word "selectively" above is the most important.

When CRE bubbles popped and left everything for dead, Zell didn't go bottom fishing for the cheapest properties he could find. When apartments were cheap, he didn't buy old, rundown buildings in slums. He bought pristine, Class A apartment buildings in unbeatable locations. Equity Residential, for example, owns trophy multifamily properties like 71 Broadway Apartments in the Financial District of Manhattan.

{kind=link}

When office CRE was overbuilt and distressed, he didn't buy money pit offices in poor locations. He bought trophy office towers in busy central business districts that would be the first to recover when demand returned.

Even when it comes to manufactured housing (mobile homes), Equity LifeStyle Properties doesn't touch the lower-quality "trailer park"-type properties. They seek out the most high-quality mobile home communities in the best locations with the most amenities like clubhouses, pools, and tennis courts.

{kind=link}

Rather than trailer park slums, ELS's typical property is age-restricted, making them more akin to retirement communities. And most are near some body of water or scenic area of nature.

In an interview, Zell once said ,

In the late 1980s and early 1990s, I was the only buyer of real estate in America. People asked me, 'How could you buy it?' How could I project yields? Rents? For me, it came down to these issues: Is the building well built? Is it in a good location? How much less than the cost of replacement is its price? I bought stuff for 30 cents on the dollar and 40 cents on the dollar.

Zell was a textbook contrarian, but he was also discriminating. When opportunities arose, he didn't buy the lowest quality asset for 10 cents on the dollar. He bought the highest quality asset for 40 cents on the dollar.

To be a value investor, there has to be some enduring value that you're buying. Otherwise, you're just a hoarder.

Learn to love the hated. But for heaven's sake, buy the best of the hated, not the cheapest.

Lesson #3: Cash Truly Is King

Having the audacity to love the hated and buy what others are despondently selling is great. But in order to do that, you have to have cash . Lots of it.

Benjamin Roth, a lawyer who lived through the Great Depression, wrote in his diary in the early 1930s, "Everyone knows that stocks are cheap, but nobody has any cash to buy them."

Is there any greater tragedy in investing than knowing something is an incredible bargain and being unable to buy it for lack of cash?

This one is particularly difficult for me, because since shortly after COVID-19 began, I have been fully invested. Over the past several years, I've always seen some marginal value in the market, so I've kept seeing something to buy with any available cash.

But I think Zell would distinguish between the kind of value that earns you 15% a year when you'd normally earn 10% and the kind of value that turns a small sum of money into a fortune -- a fivebagger or tenbagger or twentybagger.

Zell didn't become a billionaire by buying marginal value. He did it by waiting patiently for those once-in-a-decade deals to come around and having plenty of liquidity to pounce on them when they did.

What Would Sam Zell Buy Today?

I can't speak for Sam Zell. No one can. But can you think of a more feared and reviled sector of CRE today than office?

In April of this year, Zell ridiculed remote work as "a bunch of bull****" and explained why he doesn't believe it will become a new, permanent norm. Sure, COVID-19 was a uniquely bad situation for office properties, but sooner or later, employers will have their way and get their workers back into the office for in-person collaboration.

For the most part, I've taken the other side of this view by completely avoiding office REITs. It is my opinion that, while workers will gradually return to the office over time, utilization will not settle anywhere near where it was pre-COVID. That, in my view, will leave the US with a huge oversupply of office space.

But if Sam Zell was alive and reading this, I think he would (very unsubtly ) remind me that he made the vast majority of his fortune by investing in shunned yet quality properties during periods of oversupply . Wait for supply and demand to balance itself out and the best deals will be gone.

This week, inspired by Zell, I decided to love the hated and buy an office REIT. Which would Zell buy today? I don't know. But I chose to buy the single office REIT with (in my view):

- the best demographic profile in terms of job and population growth

- the highest quality and best located buildings

- the strongest balance sheet

In my opinion, the only REIT this could be is Cousins Properties (CUZ) .

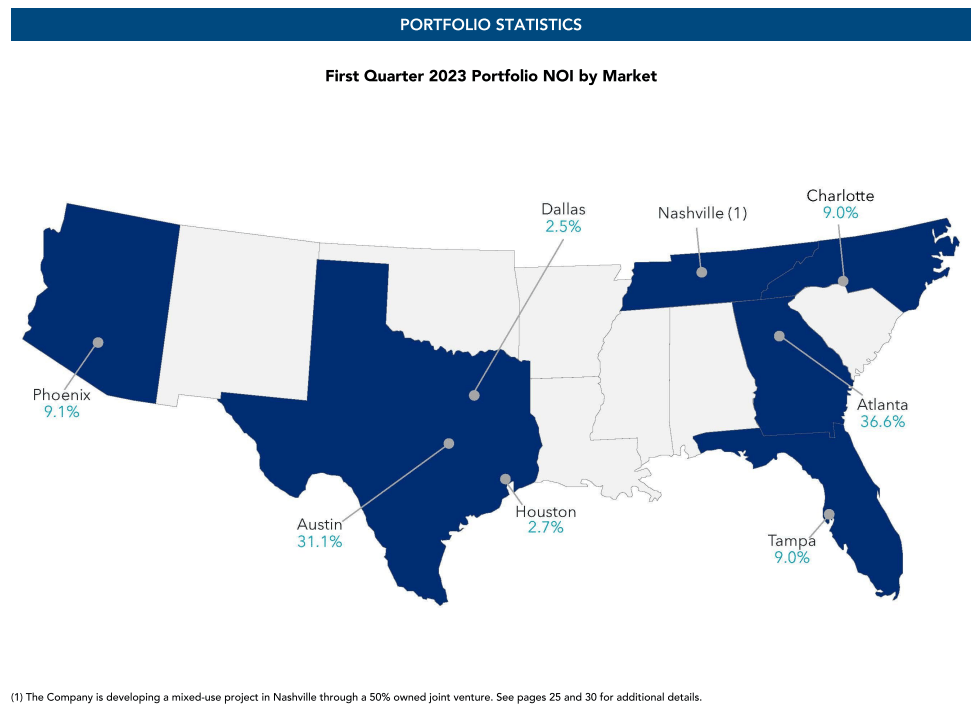

The REIT owns exclusively Class A office properties in fast-growing Sunbelt markets where corporations, jobs, and people are moving. Over 2/3rds of NOI is generated from properties in the red-hot markets of Atlanta and Austin.

{kind=link}

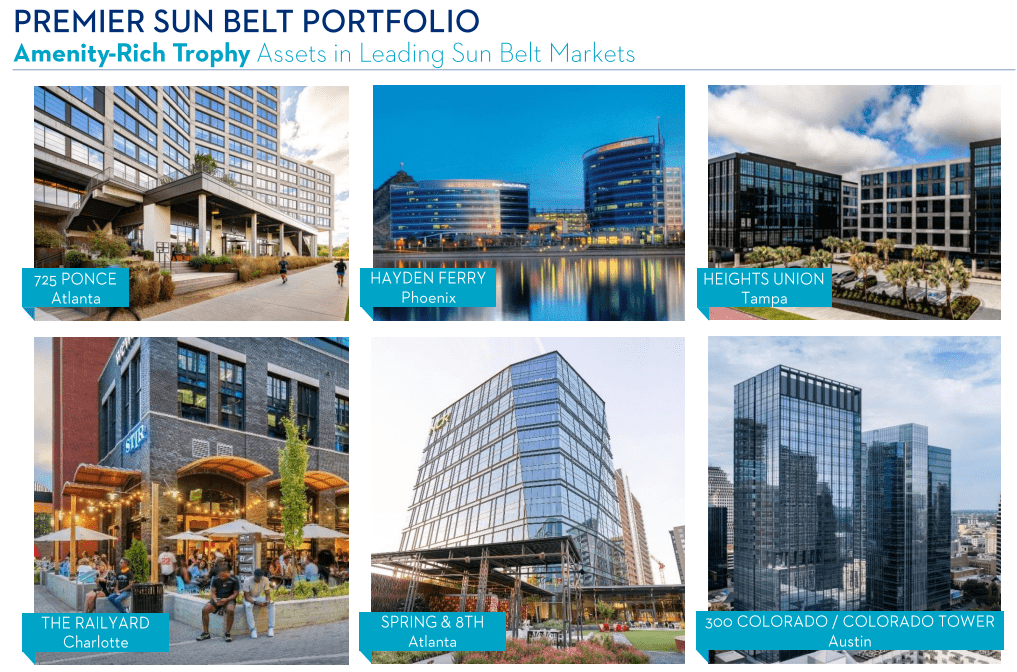

These office buildings are "amenity-rich," trophy properties that are fun, attractive places to work. Many of them, like CUZ's multiple buildings in the Domain in Austin, are also adjacent to live-work-play centers with retail, restaurants, and hotels nearby. (The retail portion of The Domain is owned by high-end mall REIT Simon Property Group ( SPG ).)

{kind=link}

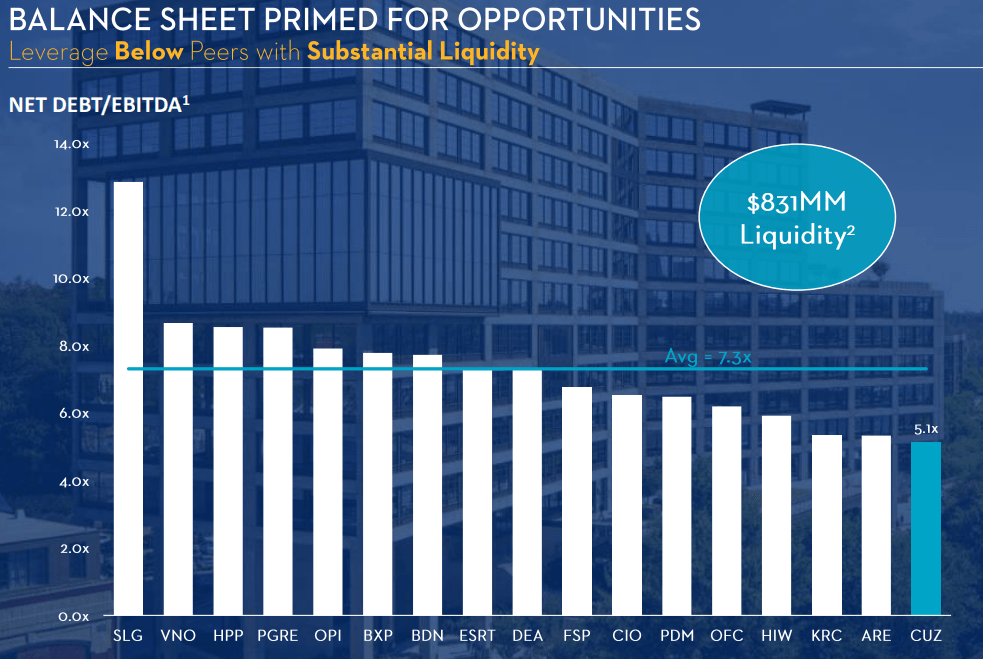

Lastly and perhaps most importantly, CUZ has arguably the strongest balance sheet in the office REIT space, illustrated by its peer-leading net debt to EBITDA ratio of 5.1x. Also, inclusive of optional loan extensions, only 4% of CUZ's debt matures through the end of 2024.

{kind=link}

Of course, CUZ faces the headwinds of rising interest expenses, tech layoffs, corporate office space downsizing, and a potential recession.

But is this not already priced in? CUZ is currently valued at 7.6x estimated 2023 FFO. By price to operating cash flow, CUZ is cheaper than it has been since the Great Recession.

And the ~6.5% dividend yield looks safe even in this difficult environment. In Q1, the dividend had a 64% payout ratio based on funds available for distribution, and management expects it to remain in its target range of 70-75% for the full year.

CUZ exists right at the intersection of high-quality assets, strong fundamentals, and an absolutely hated industry/sector. I can't help but think Zell would like it.

Takeaway

Sam Zell, the Grave Dancer of commercial real estate, was a phenomenal value investor and contrarian.

He amassed great wealth by developing an expertise in the industries in which he invested (especially CRE), taking advantage of that expertise by selectively buying solid assets in hated industries/sectors, and never getting caught in great buying opportunities without plenty of liquidity.

On top of that, Zell was an eager, outspoken, and unsubtle teacher and market commentator, a REIT industry visionary, a generous philanthropist, and (according to those who knew him) a fun-loving person.

His wit and wisdom will be missed, but he left us investors a lot of insights and examples to learn from.

For further details see:

Dividend Investing Like The Legendary Sam Zell