TROW - Dividends: All Your Beliefs May Be Wrong

2023-09-27 13:00:00 ET

Summary

- Dividends are often overemphasized by investors, leading to unrealistic expectations of getting rich from them.

- The average investor faces barriers such as starting capital, foresight, and patience when trying to live off dividends.

- The focus should be on the growth and sustainability of the underlying business, rather than solely on the dividend yield.

I have been studying and observing the financial markets for years, and right from the start I have noticed that the average investor is extremely attached to dividends; perhaps even too much so. My impressions are confirmed on Seeking Alpha, where the most followed articles are about dividend companies. Everyone is focused on Medical Properties Trust ( MPW ), a few care about terrific companies like Visa ( V ). The lust for a monthly dividend is almost stronger than any capital gains.

Certainly, there are exceptions, but my perception is that the role of dividends in investment choices often takes on too much of a role, but then again, I am not surprised. It is human nature to constantly need confirmation, and seeing every quarter that the bank account shows a small income can convince us that our investment has been a success.

In this article, I will question what I think are the most common beliefs of dividend investors, trying when possible to provide concrete examples. Before I begin, I would like to emphasize that what I will say is from my opinion: that it does not represent absolute truth.

1st belief: getting rich from dividends is possible for anyone

I often come across financial articles where an early retirement is promised through the dividend of a particular company. Frankly, I don't know if the author really believes his words, but the positive comments make me think that someone has taken the bait unfortunately.

The harsh reality is that few people can really retire early thanks to dividends, and if they can, they are probably already rich. In my opinion, there are three main obstacles:

- Starting capital.

- Foresight.

- Patience.

Let's look at all three in detail.

Starting Capital

This is an important barrier for the average investor because in order to receive a large dividend income stream you need a huge amount of capital to invest. If you have little funds available, dividends will not change your life. The harsh reality is that those who could live on dividends alone are probably already rich: we are talking about a very small percentage of the world's population. What's more, those who have enough funds at their disposal may not necessarily favor investing in dividend companies, but might buy houses to rent for example. Considering this factor as well, the people who live and get rich every day from dividends are even fewer. Let me show you some figures to give you an idea:

- The average cost for a family of four in the U.S. is $7,095 per month or $85,139 per year. Given a portfolio with a dividend yield of 3 percent, for the average family to meet its annual expenses, that portfolio must be worth $2,837,966.

- In the case where the dividend yield is 5%, which is quite high, $1,702,780 would still be needed. Moreover, considering that this is the gross yield, the net yield is lower, especially if there are securities in the portfolio subject to double taxation.

- Wanting to be optimistic, in case the dividend yield was 10%, $851,390 would be needed, definitely less than almost $3 million, but still an out-of-reach figure for most families.

In sum, living off a dividend yield is for few, however, this does not mean that it is never worthwhile to invest in dividend companies. In my opinion, the average investor is wrong in his or her approach to investing because expectations are too high. For those with small capital, dividends can be a way to round out the salary, but not to replace it. Otherwise, there is a risk that the lust to live off the dividend can take over and cloud rationality. In front of a company with a dividend yield of 20-30%, the first thing to think about is where the catch is instead of starting to count the days before getting rich.

Realistically speaking, getting $500 a month in dividends requires a $150,000 portfolio with a dividend yield of 4%. After years of saving, this goal may be feasible even for the average family, but it requires a major commitment from all members. Finally, do not forget that we are always talking about gross returns.

Foresight

The best dividend yields are earned over time, and it is essential to rely on the right companies. Even if you had $200,000 available to invest in dividend companies, nothing guarantees that you will choose the right ones. After all, we are talking about predicting a company's performance in the distant future. Having the right investment skills is probably even more difficult than having a large amount of money on hand. History is full of successful companies that have been forced to cut or suspend the dividend. Let me show you some examples .

- General Motors had a centuries-old history behind it and was-and is-the largest automaker in the United States. In its golden years, it was able to pay steady dividends for decades, but in the early 2000s, its growth prospects deteriorated, and in 2006 it was forced to cut its dividend in half. Loyal investors decided not to sell and were still hopeful that the company would return to its former glory: big mistake, it declared bankruptcy in 2009.

- Kodak was even older than General Motors and in the 1970s presented a dominant market share. For several decades it was able to issue a high and growing dividend, but in the mid-1990s it began a slow decline in sales resulting in a dividend cut. After a history of success, Kodak declared bankruptcy in 2012.

Both Kodak and General Motors ( GM ) were dominant and well-respected companies, yet they failed to avoid bankruptcy. In such cases, the dividend cut is probably the least of the problems since investors saw all their invested money evaporate. In any case, we are talking about two extreme cases, but useful for understanding how little control we have over the future. Are you so sure that the company you have invested in will continue to issue dividends in 10 to 15 years?

Patience

Assuming you have the necessary capital at your disposal and believe you have found the right company in which to invest some of it, are you sure you will be patient enough? In other words, it is very easy to say "I invest for the long term," in deeds almost no one does. Let me explain further.

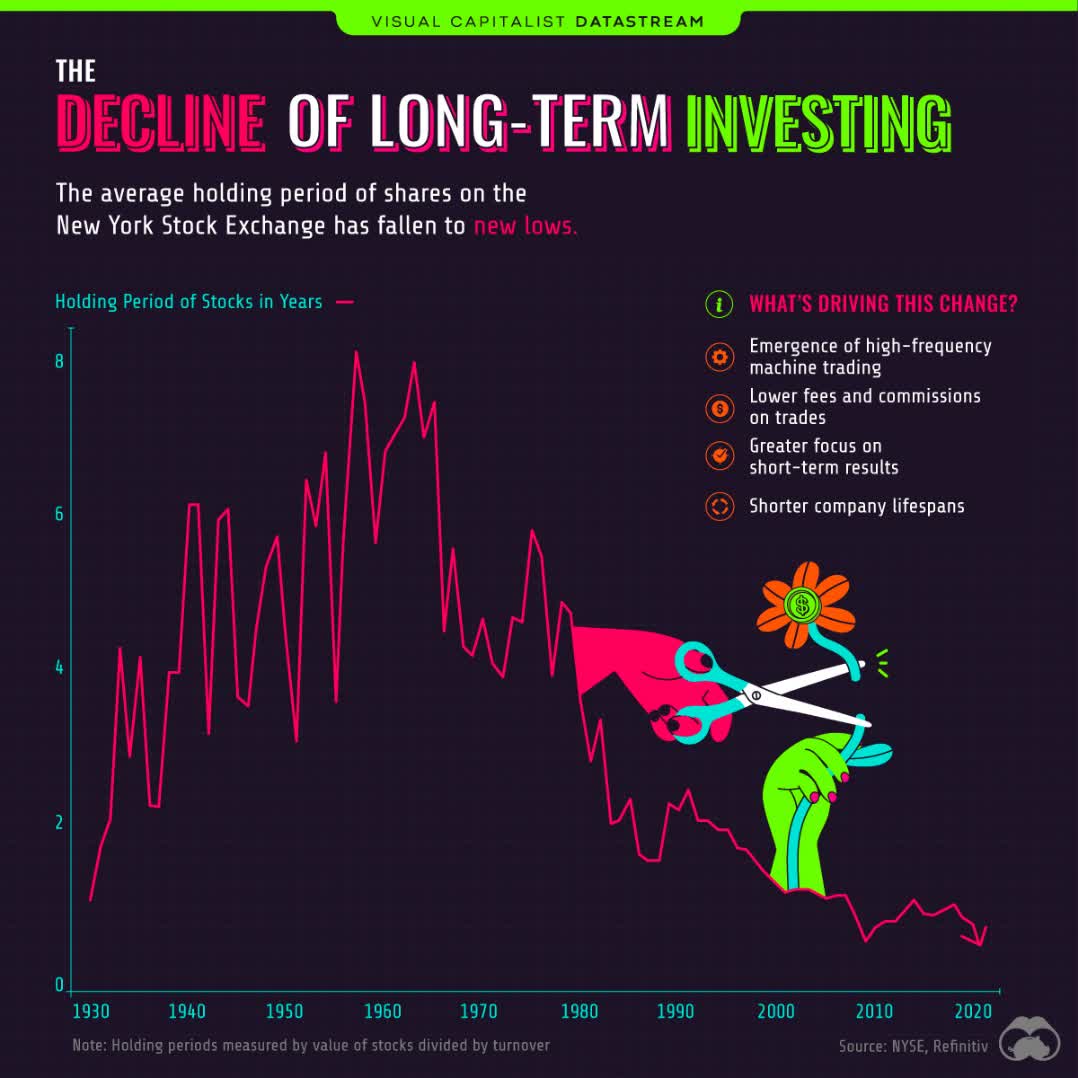

In general, my impression is that today's society is increasingly directed toward the immediate enjoyment of pleasure; short-term returns are taking over from long-term ones because there is no longer the patience to wait. In fact, supporting my thesis is this graph showing the average holding period of equities throughout history.

{kind=link}

As we can see, while in the past it was common to hold a stock in a portfolio for 8 years, today it is difficult to hold it for only one year. The ease with which in 2023 the average investor can demobilize his or her investment is disarming. Just turn on your smartphone and sell stocks worth thousands of dollars at an often relatively low spread. On the one hand this is great because it makes the financial markets accessible to anyone and anywhere, but on the other hand it should be pointed out that the average investor is more prone to making mistakes. Every day we are constantly bombarded with negative news and may be tempted to sell our portfolio stocks. After all, it only takes a few seconds to make a wrong choice and panic.

Overall, the best dividend yields are those obtained over the long term, but the average investor can hardly remain rational for such periods. Unlike decades ago, today we are constantly stimulated to make a decision and it is easier to make hasty choices.

Patience is in my opinion the most underrated characteristic when it comes to investing in dividend companies, yet it is often the main reason why an investment has not met our expectations. Investing in companies with a very high dividend yield is often synonymous with impatience, and I will discuss this extensively in the next section.

Finally, I want to tell you briefly about the quintessential dividend investment, namely Warren Buffett's purchase of Coca-Cola ( KO ) in 1988. At that time $1.30 billion was invested in the world's most famous soft drink company, and the dividend yield on cost in 2023 will be 56.70%, an absurd figure. Since dividend income in 2023 will be $736 million, every two years Warren Buffet makes back his initial investment. Huge starting capital, foresight and patience have given light to one of the most profitable dividend investments ever.

2nd belief: the higher the yield the better

We all agree that getting more is better, yet the risks involved in getting a higher yield are often underestimated. If a company issues a dividend yield of 15 percent, the first thing to do is to ask what kind of problem it has. Often, if something is too good to be true it probably is. Beyond the dividend yield, it is critical to first understand the sustainability and growth rate of the dividend.

Would you ever invest in a company with a dividend yield of 15 percent, highly indebted in an economic environment with high rates and a dividend per share almost unchanged over the past 15 years? Your answer is probably no, yet I am sure many of you have invested in Medical Properties Trust, one of the most popular stocks here on Seeking Alpha. To date, these investors have experienced significant unrealized losses and a dividend cut. This is, in my opinion, the perfect example of a wrong investment, since little is left of the growing, high and sustainable dividend.

I already talked about this company in depth months ago, so I will not go into too much detail. In any case, I think it is important to highlight what went wrong with this investment in order not to make the same mistake in the future. Why were investors convinced they were getting a bargain based on its high dividend yield?

The first factor that I think was very influential is the herd effect. Often in financial markets, the choice of a single trader is influenced by the choice of all the other traders within the market. It is very difficult to have a contrarian view, yet it is the main characteristic that differentiates an average investor from a capable one. In the case of Medical Properties Trust, many analysts sided with it because they believed that its business model could sustain a dividend yield of 15 percent. At the time of the publication of my bearish thesis there were virtually only strong buy articles. For a novice investor, it is a common mistake to side with the herd since they are unable to formulate an investment thesis on their own. Always do your own research and do not invest just because someone else said so, including me of course.

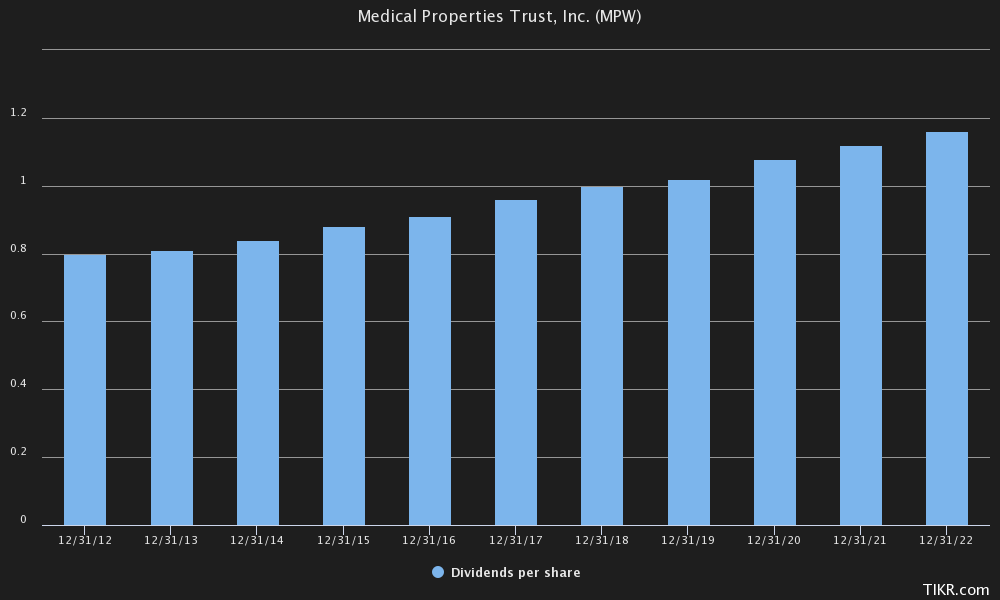

The second factor that misled investors was the macroeconomic environment.

{kind=link}

If we look at the last 10 years, we can see that the dividend per share has increased every year, and this gave the impression that the dividend could follow the same increasing trend in the future. The average investor may have thought that 15% would become 20-25% over the following years.

In fact, 10 years is a pretty good time horizon to understand whether a company tends to increase its dividend, however, the mistake lies in not considering the underlying macroeconomic environment. From 2012 to 2022, the world's major economies had interest rates close to 0% in order to trigger economic recovery after the great financial crisis of 2008. COVID-19 has further exacerbated monetary policies of an unconventional expansionary nature.

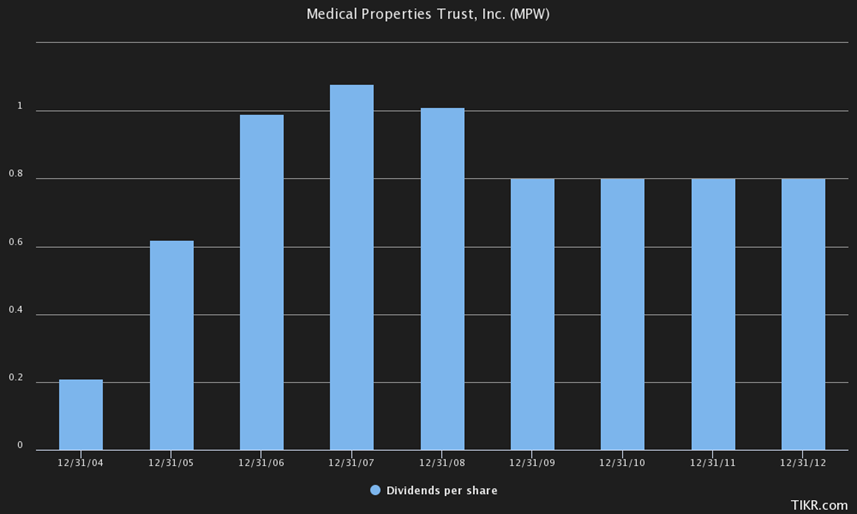

So, given the low interest rates, the 2012-2022 decade was particularly favorable for all businesses with significant debt, including REITs and therefore Medical Properties Trusts. The average investor has not considered that the coming decade will be characterized by a new macroeconomic environment that will not necessarily favor REITs. In fact, the moment the Fed started raising rates the Medical Properties Trust bubble burst.

{kind=link}

Yet, one only had to look at the previous decade to see that dividends from this stock are anything but safe when rates are not at 0%. Finally, to the refinancing problem must be added the issues with the main tenants that we all know about. The red flags were there, but the double-digit dividend yield put everything on the back burner.

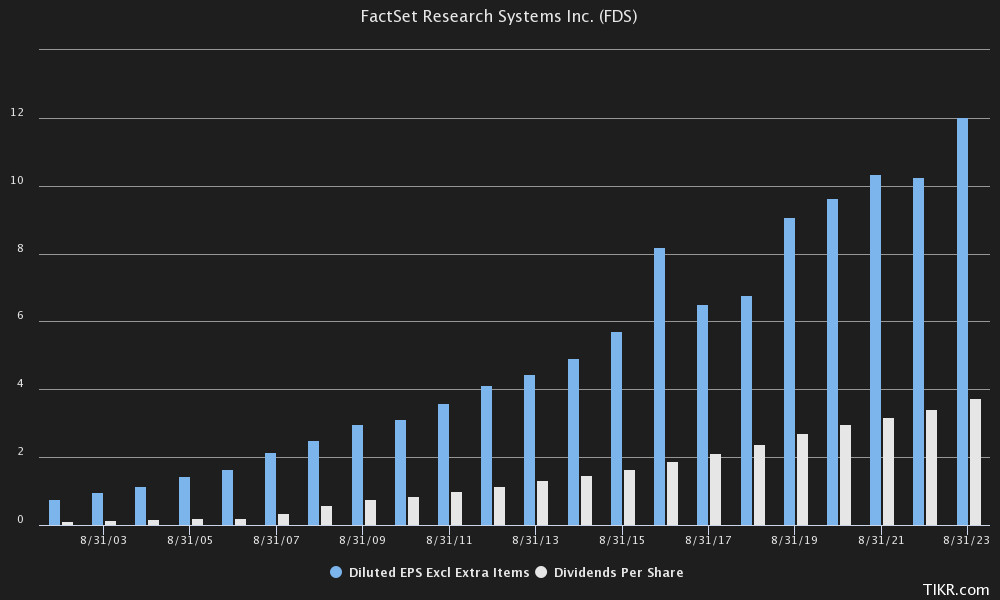

To sum it all up, it is crucial to know that investing in companies with a high dividend yield is highly risky and there are not only benefits; Medical Properties Trust is proof of this. In my opinion, to get the most benefit from dividends, one must paradoxically put aside the dividend yield and focus on the growth of the underlying business. Often, companies with a dividend yield of 1-2% are not even considered, yet their growth rate may surprise you. In my opinion FactSet ( FDS ) falls into this category. I have already written a detailed article on this company as well, so now I will simply show you some financial results.

{kind=link}

FactSet has been steadily increasing EPS and issuing an increasing dividend every single year for two decades. The soundness of this company's business is beyond question and these achievements are proof of that. Yet despite the fine premise, few people care about FactSet as we can see from the few followers on Seeking Alpha as well.

Its dividend yield is almost 1 percent, too little to attract the attention of dividend investors, but its yield on cost is 3.56 percent for those who bought it 10 years ago. So, by purchasing FactSet, one cannot expect a high dividend yield in the immediate term, but for those who are patient, they could get excellent results in the long run.

The 10-year dividend CAGR was 10.98%; assuming the next 10 is the same, buying at the current price in 2033 the yield on cost will be 2.40%. Certainly not that high (aided by a perhaps excessive price per share at the moment), but one must consider the strength of this dividend yield and its growth prospects. Also, I am not even considering the potential capital gain from investing in a company of this caliber. The 10-year CAGR of the investment was 14.80%.

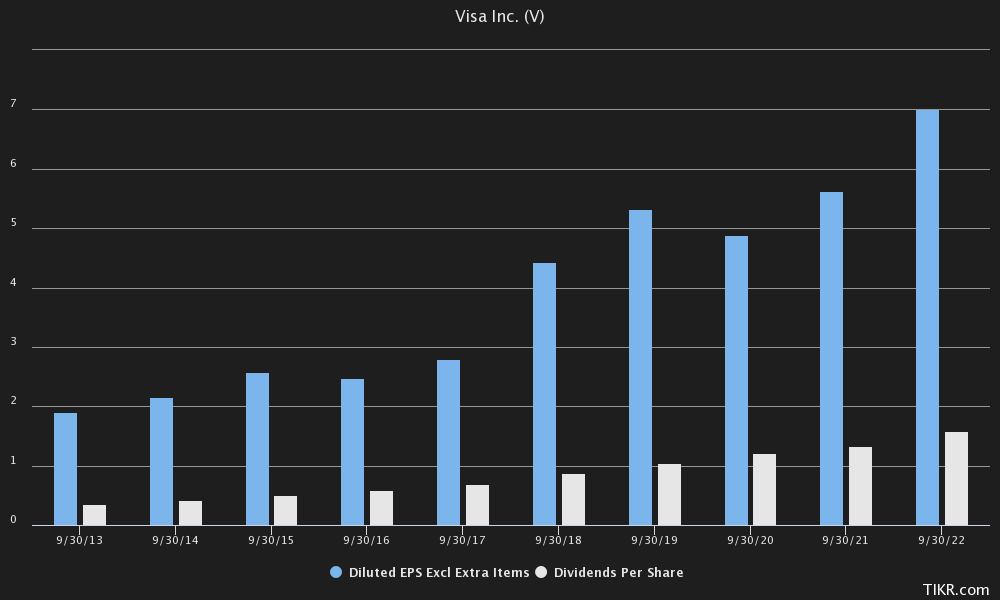

In the case of Medical Properties Trust, the CAGR was -6.70% despite the fact that the last decade has been characterized by one of the biggest bull markets in history. What is the point of a high dividend yield if this is the overall result? Sure, we are talking about different companies, but the money invested has the same value in both cases. I hope I have made my point clear through these two companies, which, I reiterate, are simply examples and not investment advice. Instead of FactSet, I could also have placed Visa, another dominant company with profits and dividends growing over the long term. But even here the interest of the average investor is minimal because the dividend yield is only 0.80 percent.

{kind=link}

Yet, for those who bought it 10 years ago the yield on cost would be around 4 percent.

The point is, if you are looking for a dividend yield, it is critical to first evaluate the company's underlying business, because it is through it that you will get sustainable and growing dividends over the long term. If profits are not growing, forget about your dividends. Investing just because you are attracted by a high dividend yield of dubious sustainability is a losing strategy in the long run. If you want to create wealth, it takes time, and shortcuts only take you further and further away from the goal.

3rd belief: dividends are always welcome

My perception is that in the collective imagination the dividend is often associated with something positive and necessary for shareholders to be satisfied with their investment. When a company decides to cut the dividend it is sure that the market will not take it well, whereas when it increases it everyone is pleased. Shareholders mainly care about their portfolio and do not care about what are the negative aspects of the dividend. Let me explain further.

Everyone is glad to have an income in their bank account, but it is good to evaluate the other side of the coin as well: the company that issued the dividend gave away millions/billions of dollars to the outside. These huge sums of money could have been used to support new projects, new acquisitions, and new research and development plans; instead, it was preferred to remunerate shareholders. In some cases, there are even companies that take on debt in order not to disappoint expectations, and this results in a vicious cycle that will inevitably lead to the decline of the company.

By this I am not saying that the dividend should be abolished, but that the other side of the coin should also be highlighted. For example, for companies with a high ROIC, issuing a dividend means giving up on allocating new capital productively within the company. Hypothetically, if Kodak had used the dividend money to invest in new technologies it might have had a different future, but it did not.

However, some exceptions should be pointed out to this reasoning regarding companies with high ROICs whose dividend is a strength. For example, a company such as Coca-Cola does not need to innovate every year since its product has been the same for decades and continues to do well; the same goes for British American Tobacco ( BTI ) and Philip Morris ( PM ). Certainly, the companies that sell tobacco are now committed to investing billions to offer new products that are less harmful to health, but the low expenses of their operating business allow them to issue huge and sustainable dividends. Different discussion for companies like IBM ( IBM ).

{kind=link}

The dividend yield is quite high, 4.50%, and the dividend has been growing for 23 years in a row. If this money had been invested within the company maybe the price per share would not be the same as in 2010. Same for Intel ( INTC ), which if it had invested the cash from the dividend maybe would not have suffered so much from AMD's ( AMD ) competition.

In general, my opinion is not that dividends are useless, but that from a financial point of view their negative impact should not be underestimated. Moreover, reinvesting these sums of money over time can generate a capital gain that far exceeds the dividend yield.

Finally, I want to conclude this paragraph by highlighting a peculiarity of Berkshire Hathaway ( BRK.B ). Since its IPO it has far outperformed the S&P500 ( SP500 ), yet it has never issued a dividend.

At first glance this may seem contradictory given that there are many dividend companies within its portfolio, but it makes perfect sense. Warren Buffet has never wanted to issue dividends since he has always preferred to allocate capital in more efficient ways, such as making acquisitions or buying his own shares when the timing is right. The latter in particular has always been the preferred method of remunerating shareholders and has granted them a huge capital gain not subject to continuous taxation as in the case of dividends.

Rather than focusing only on the rising bank account in the short term, the average investor should ask himself whether the choice to issue a dividend represents the best one in terms of capital allocation for the company in which he has invested. The answer is not always yes.

When dividends are a positive factor

So far I have pointed out some flaws of dividends, but that does not mean that I believe they are pointless. If sustainable and growing, dividends are an excellent way to reward shareholders in the short term, but certain criteria must be met so that they are not harmful to the company itself.

To give concreteness to my thinking, I will show you some examples where I believe the dividend is optimally managed.

Chart based on Seeking Alpha data

{kind=link}

Hershey ( HSY ) is a leader in its market and has a distinctly high profit margin for being a consumer staple. In its case I evaluate the dividend positively since the company has a solid financial situation and its business model does not involve continuous investment to keep its leadership strong. Moreover, EPS has increased much more than dividends in recent years, and this could lead to an acceleration of dividend per share growth in the coming years. Let us now look at British American Tobacco.

Chart based on Seeking Alpha data

{kind=link}

I have already discussed on Seeking Alpha several times about this company, and I believe it currently offers one of the best dividend yields around. The dividend yield is 8.20%, there is no double taxation, it is growing over the long term and well supported by EPS. All this is possible because of its competitive advantage: barriers to entry are high, its consumers have a physical addiction to its products, and the net income margin can reach 30%. In addition, management's wise choices regarding dividend growth should be highlighted.

Since the acquisition of Reynolds Tobacco (2017), net debt has increased significantly and management has decided to slow dividend growth to accommodate a deleveraging process. This choice proved to be far-sighted since with current interest rates refinancing a huge debt would have been a problem. Any shareholder would have been excited about a large dividend increase, but the company preferred to improve its soundness first. These are the kind of choices I appreciate most since they are aimed at long-term prosperity. Opposite argument for Medical Properties Trust.

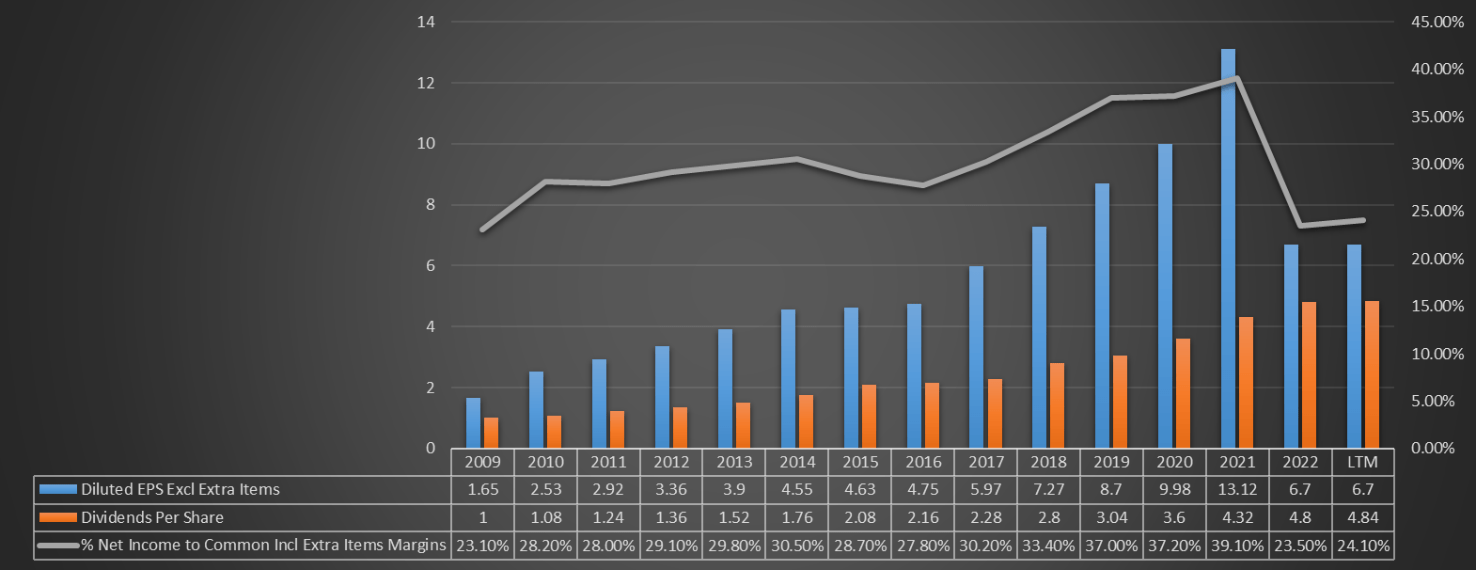

Finally, the last example of proper dividend management concerns a dividend aristocrat, namely T. Rowe Price ( TROW ).

This company has been issuing a growing dividend for 36 years and yet it is little regarded here on Seeking Alpha. Frankly, I do not understand why this disinterest since the dividend yield is also high, 4.61%.

Chart based on Seeking Alpha data

{kind=link}

EPS has always covered the dividend per share, even after the great financial crisis, while the net income margin is often above 30%. Recently, earnings have plummeted as AUM is struggling to grow given the current macroeconomic environment, but this is a problem the company has faced many times before: T. Rowe Price cannot control the business cycle. In the long run it has proven to be an excellent dividend company and among other things has negative net debt. The ROIC is high and its business model can support the issuance of a large dividend. The yield on cost is 7 percent for those who bought it 10 years ago.

Overall, I consider these three companies to be positive examples because they have the two main characteristics I look for in a dividend: growth and sustainability. Under these conditions I favor an investment; if, on the other hand, dividends do nothing but please shareholders and weaken the company's financial situation, better to opt for something else.

Conclusion

I hope with this article I have best expressed my point of view, which is that dividends are a plus only if the company issuing them has an excellent financial situation. Investing in companies with a double-digit dividend yield I believe only moves the average investor away from his or her goal. Of course, there are exceptions, but we are talking about rare opportunities that do not come along every day.

Even before looking at the dividend yield, the business model of the underlying company must be observed and understood, and an investment thesis must be made, otherwise, the risk of regretting investing in it is high. Even if you have chosen the right company, if you do not know it thoroughly, at first difficulty you will panic and sell it. Be wary of those who promise you so much and in a short time, a good dividend portfolio is not built overnight, but over the years: it took Warren Buffet 36 years to achieve a 57% yield on cost of his investment.

Getting rich is a process, not an event.

For further details see:

Dividends: All Your Beliefs May Be Wrong