JEPI - DIVO: Designed To Outperform JEPI

2024-01-11 15:21:50 ET

Summary

- Research suggests that high-yield covered call strategies underperform low-yield strategies, leading to lower total returns.

- Covered call ETFs with higher yields have a greater negative equity exposure, resulting in lower expected returns.

- There is a positive relationship between the derivative yield and the expected volatility risk premium return, but this is overshadowed by the negative equity impact.

- DIVO targets a lower yield than JEPI and is hence designed to outperform JEPI.

Recently some interesting covered call ETF research was published. We had already a slight preference for Amplify CWP Enhanced Dividend Income ETF ( DIVO ) from my article last January and the research strengthens our case to have that slight preference for DIVO over JPMorgan Equity Premium Income ETF ( JEPI ).

Are covered call ETFs a bad idea?

A study from October 2023 by Roni Israelov and David Ndong calls covered calls " A Devil's Bargain ". The researchers found that " the round-trip transaction of selling an S&P 500 index call option over the full period, on average, had lost money. Selling (covered) calls on its own didn't, on average, add value. "

The full title of the research paper is " A Devil's Bargain: When Generating Income Undermines Investment Returns ". One could interpret this title as a claim that buying covered call ETFs is a bad idea. But the main finding of the research paper is actually the following: " High-yield covered call strategies underperformed the low-yield covered call strategies, and materially so. "

So the devil's bargain doesn't refer to covered call ETFs in general, but to the higher yielding ETFs. The higher yield is tempting and looks beneficial, but it leads to negative longer-term consequences in the form of lower total returns.

In the words of the researchers: " Covered call strategies, depending on their implementation, can be an appropriate allocation within well-constructed, diversified investor portfolios. Covered call strategies have positive equity exposure - which delivers the equity risk premium - and when writing options, they are short equity volatility, which delivers the volatility risk premium. In fact, for many investors, a covered call strategy is perhaps the most natural and accessible approach to earn the volatility risk premium. "

The higher the yield, the better?

Covered call ETF managers have control over the yield they want to generate. If they pick a call strike price closer to the current stock price they receive a higher option premium and generate more yield. If they select a higher strike price they receive a lower premium and hence generate a lower yield. In the latter case, the managers enjoy a higher equity upside potential of course.

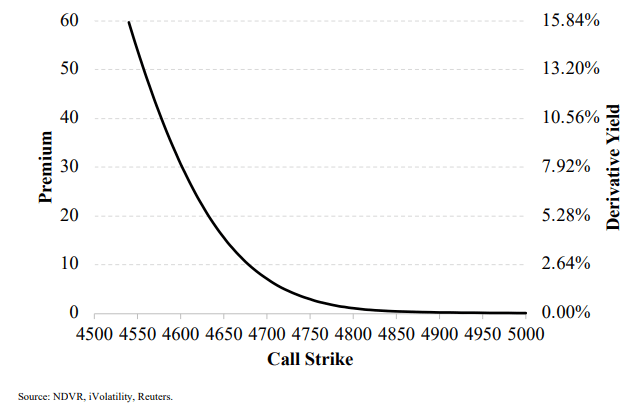

Figure 1 displays what we just discussed. The lower the call strike, the higher the premium and the yield.

Figure 1: Call strike vs derivative yield (Israelov and Ndong)

{kind=link}

The researchers use a so-called toy model to paint a clear picture. They assume a 2% dividend yield, a 3% risk-free interest rate, a 6% market equity risk premium, 15% realized volatility, and a flat 16% implied volatility. The options have a the time-to-maturity of 30 days. Figure 2 shows also, using the toy model, that higher call option strike prices result in lower yields and vice versa.

Figure 2: Moneyness vs derivative yield (Israelov and Ndong)

Equity call options have a positive exposure to their underlying stock, and this relationship is quantified by the option delta. Delta represents the sensitivity of the option's price to changes in the price of the underlying stock. At the money call options have a delta of around 0.5, while out of the money call options have a lower delta (closer to zero).

Figure 3: Moneyness vs option delta (Israelov and Ndong)

Higher yielding covered call strategies use lower strike prices and have hence a greater option delta compared to lower yielding covered call strategies.

Figure 4: Derivative yield vs option delta (Israelov and Ndong)

But covered call ETFs are selling equity options and as a result they are introducing a negative equity exposure. Stocks have an equity risk premium and being short equity delta should lead to negative expected returns. Higher yielding covered call strategies have a bigger negative equity exposure (due to their higher option delta) and this leads to lower returns.

Figure 5 shows, again using the toy model, that higher yielding strategies have indeed a lower equity risk premium. This premium is defined as the short call delta multiplied by the market equity risk premium (which is 6% in the toy model).

Figure 5: Derivative yield vs short call equity risk premium (Israelov and Ndong)

So there is a negative relationship between the derivative yield and the (negative) expected return impact introduced by selling calls.

This reduced equity exposure is also reflected in the betas of covered call strategies. Higher-yielding covered call strategies tend to have lower betas while lower-yielding covered call strategies have a beta closer to 1.

Figure 6: Derivative yield vs equity beta (Israelov and Ndong)

Covered call writing is a defensive, low(er) beta, strategy. When the markets rise, you get a nice return. That return is capped and will probably lower than the return of the equity markets itself, but that's something you know in advance.

When the equity markets fall, you outperform thanks to the collected option premiums. Of course, when the market really tanks, you will still have a negative return.

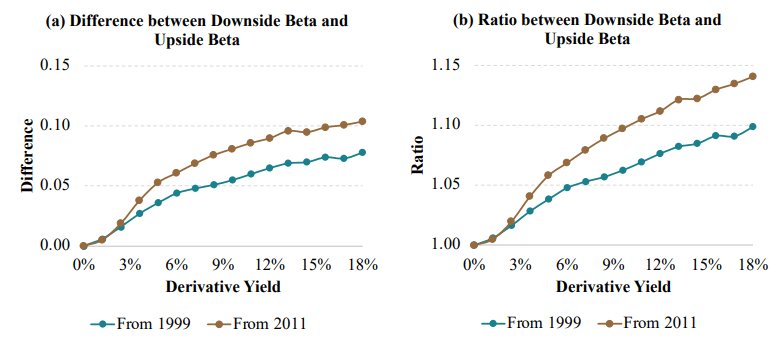

Another way to frame this: the upside beta is lower than the downside beta.

There is also a clear relationship between the up- and downside beta and the targeted yield level of the covered call strategies. The spread between the downside beta and the upside beta increases when the targeted derivative yield increases.

Figure 7: Derivative yield vs upside and downside beta (Israelov and Ndong)

{kind=link}

Bottom line: there is a negative relationship between the derivative yield and the (negative) expected equity risk premium return impact introduced by selling calls.

Volatility

When you sell (call) options you are short equity volatility, and this delivers you the volatility risk premium, because the implied volatility tends to be higher the realized volatility.

A covered call ETF's short position is profitable when realized volatility is low relative to implied volatility and unprofitable when realized volatility is high relative to implied volatility. Historically, we observe a propensity for the option market to price in slightly more expected volatility than what is subsequently realized (as is the case in the insurance business): the implied volatility tends to be higher the realized volatility.

The exposure to volatility tends to be higher the closer the option strike is to the current stock price. The higher yielding covered call strategies use such options and hence have a higher short volatility exposure and earn higher volatility risk premium returns compared to the lower yielding covered call strategies.

Figure 8: Derivative yield vs short call volatility risk premium (Israelov and Ndong)

Bottom line: there is a positive relationship between the derivative yield and the (positive) expected volatility risk premium return impact introduced by selling calls.

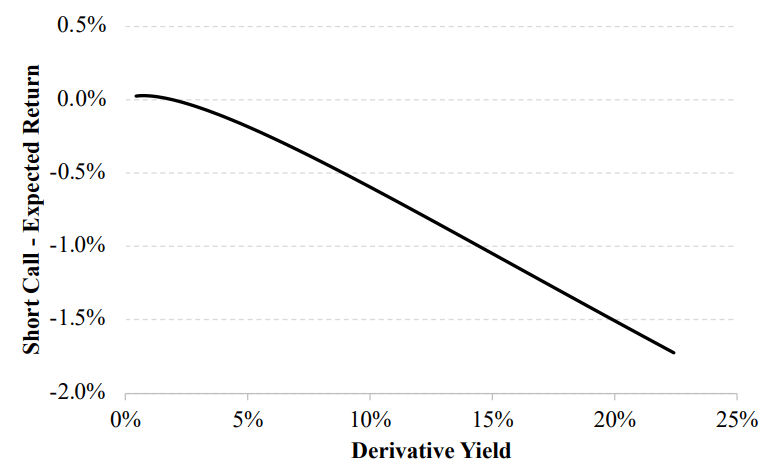

This positive volatility return is however overshadowed by the negative equity impact introduced by selling calls.

Figure 9 shows, using the toy model, the short call expected excess return against the derivative yield. The short call expected return is the sum of the equity risk premium, defined as the short call delta multiplied by the annualized market risk premium, and the volatility risk premium, defined as the difference between the call price under implied volatility assumption and the call price under-realized volatility relative to the stock price, annualized.

Figure 9: Derivative yield vs short call expected return (Israelov and Ndong)

{kind=link}

By increasing the targeted derivative yield you increase your exposure to the market volatility risk premium while you have at the same time a lower market beta and hence a lower exposure to the equity market risk premium. The latter effect is bigger than the former and results in a lower short call expected return for higher yielding covered call strategies compared to lower yielding covered call strategies.

DIVO vs. JEPI

In theory, reality and theory are the same, but in reality, they are not (always). Do we recognize the research findings of the toy model also in reality?

Compared to JEPI, DIVO is a lower yielding strategy. DIVO aims for a derivative yield of 2 to 4%.

Figure 10: DIVO Sources of return (Amplify ETFs)

JEPI on the other hand counts on a derivative yield of 5 to 8%.

Figure 11: JEPI Sources of return JPMorgan Figure 11: JEPI Sources of return (JPMorgan)

Based on this information, DIVO should have a higher beta and a higher total return. Is DIVO indeed designed to outperform JEPI?

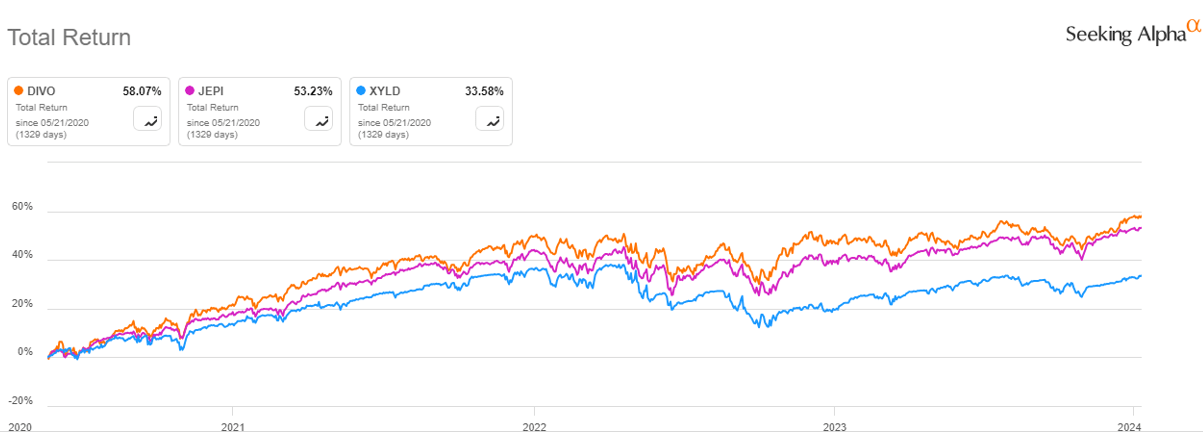

DIVO has indeed a higher beta than JEPI (and the Global X S&P 500 Covered Call ETF ( XYLD )). DIVO has a dividend yield of 4.7%, JEPI 8.4% and XYLD at 10.5%.

DIVO also has indeed a higher total return than JEPI and XYLD.

Figure 12: Risk and return (Portfolio Visualizer)

{kind=link}

{kind=link}

It looks indeed that the higher yield targeted yield by JEPI and XYLD results in lower total returns, compared to DIVO. The higher yield is tempting and looks beneficial, but it leads to negative longer-term consequences in the form of lower total returns: a devil's bargain.

To be clear the foregoing focused solely on the option selling part of covered call strategies. There are of course two other return sources: dividends and capital appreciation of the underlying equity portfolio. DIVO targets a slightly higher dividend income compared to JEPI. Its portfolio hence has a (slightly) higher value and small cap tilt.

{kind=link}

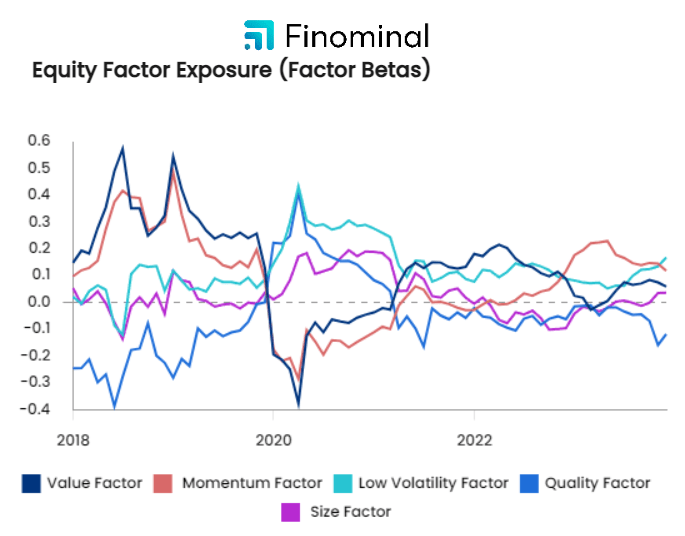

Both DIVO and JEPI have positive momentum and low volatility factor betas and (especially JEPI) a negative quality factor beta.

{kind=link}

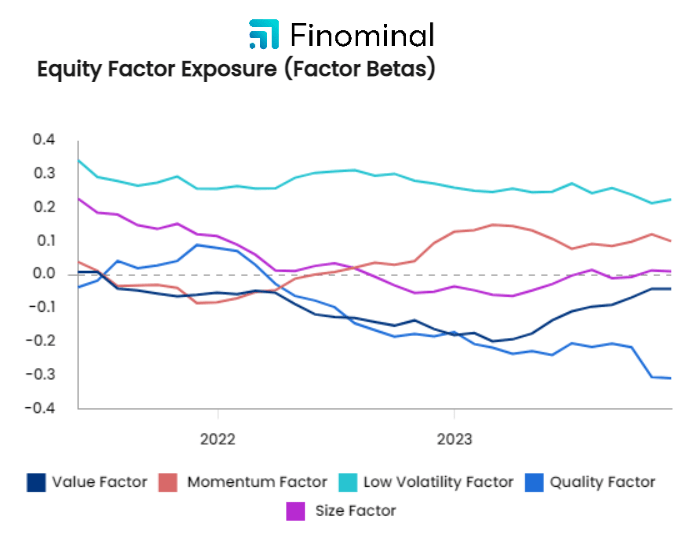

All equity factors are in a long-term uptrend. We can expect that the capital appreciation will be rather similar for DIVO and JEPI going forward.

{kind=link}

This positive trend for equities brings us to the outlook for covered call strategies.

The outlook for covered call ETFs

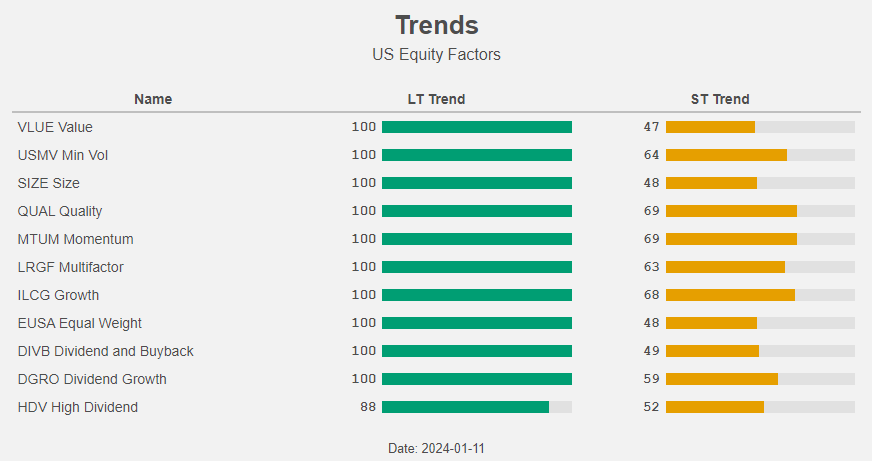

For the outlook for covered call ETFs we look foremost at the trend of the equity markets. And this trend is looking very well.

Figure 17: Trends (Radar Insights)

We also take the level of the VIX into account. The best scenario for covered call strategy is the combination of equity markets that are trending higher and a high VIX.

Currently the VIX is rather low.

Figure 18: VIX Index (CBOE)

Equity markets that are trending higher are often accompanied by a lower VIX (and vice versa a high VIX often accompanies falling equity markets).

So the outlook for covered call strategies is good. If these up-trending equity markets would be accompanied by a higher VIX, the outlook would be even better. As long as equities are not in a downtrend, the backdrop for covered call ETFs is favourable.

Please note that both DIVO and JEPI are in a long-term uptrend.

Conclusion

The following quote of researchers Israelov and Ndong is in our eyes very clear:

" Equity index covered calls are long equity and short equity index volatility. As such, they should earn the equity risk premium and the equity volatility risk premium. For those investors who seek to include these two risk premia in their portfolios, depending on their overall goals, covered call strategies may very well be a good fit. "

When implementing such a strategy it's advisable to opt for a lower yielding ETF like DIVO, because DIVO is by design expected to outperform JEPI. And DIVO is in reality indeed outperforming JEPI.

For further details see:

DIVO: Designed To Outperform JEPI