DLO - DLocal Conducted A Major Buyback To Counter Short-Selling

Summary

- DLocal stock has been under pretty meaningful pressure thanks to a Muddy Waters Research report in November that points to oddities in historical reporting and performance data.

- They point to some red flags in auditor choice, oddities in historical reporting, some related party transactions but critically some odd trends in take rate performance.

- DLocal is buying back 2% of its shares in response and this has caused a sharp share rebound, but this doesn't directly address the claims.

- Muddy Waters goes far and is aggressive in its assertions. We take a very disinterested view and recognise that regardless of the quality of reporting, industry trends are somewhat negative.

- The buyback doesn't mean anything to us, it's small and we've seen some of our portfolio stocks buyback more than 25% in one go, and even on reported data DLO stock is not cheap.

DLocal ( DLO ) is a payments company that produced with its founders the first Uruguayan billionaires. The company generates substantial income from FX on the volumes that it processes from companies operating abroad who want to interface with buyers in LatAm. It's a payment processing business, and multiples can be really high here as they are with other payments processing companies like Adyen (ADYEY). The problem with this stock is first that it could become a battleground as major short-seller Muddy Waters' Carson Block takes aim at the company , making some pretty serious allegations on the quality of the books. With the war between Robinhood types and short-sellers we are going to stay far away from DLO on that basis already. While we don't even have to have an opinion on the quality of reporting, we have enough worries on industry level trends to be turned off, especially where pricing is an outlier and high for DLO at the moment. Much can erode that, so we stay far away.

Muddy Waters Report

So the big news is this Muddy Waters research report which came out in November. It's thorough , as these reports always are, and recognises oddities which we can't explain, although that doesn't mean it can't be explained by the company when they get around to addressing it. While they detect oddities, the reasons for these oddities are still very speculative, and while Muddy Waters tries to connect the dots, it remains conjecture.

Personally, we have enough industry level concerns to avoid the stock, so we don't care too much about the details of the Muddy Waters report even though it's still an interesting read, but for the benefit of the lazy reader (DISCLAIMER: Read the report yourself for the proper picture) the following are the key concerns raised by Muddy Waters for you to investigate yourself, in case your rejection thresholds aren't going to be met by suboptimal industry-level elements.

- Most of the revenue comes from a subsidiary in Malta, which is the unit through which payments are going. Malta is dodgy, and the subsidiary has apparently failed some capital requirements tests recently. This isn't a doomed sign, and we've had companies in the past, notably in the betting industry, that have utilised Malta a lot since it's a bit of a grey market business and Malta is indeed a little dodgy as a banking geography.

- The Auditor choices in general are strange, using PwC in Argentina, and then other much more marginal auditors for its subisidiaries located far away from Argentina both physically and legally. This is rarely good when multiple auditors are involved at multiple levels, because it only takes one informal relationship to hide a lot of critical things, going off Parmalat as a precedent. Still, it proves nothing.

- The company lent money to executives to exercise options and then changed materially their explanations of these movements in later reports. Muddy Waters speculates a great deal on how the money can be followed into other acquisitions and how that could have been a way to give these owners in acquired businesses a profitable 'in' to the DLO shareholder base. Whatever, we don't even care - we think things like this are happening all the time in finance.

- Muddy Waters thinks that DLO is dipping into customer funds for things. Again, read the report for this one they go into a lot of detail.

- The take rates, which are basically the commissions driven primarily by FX based revenues, are really high on the processed volumes compared to peers even in periods where low take rate cohorts growing in the mix should have pressured figures.

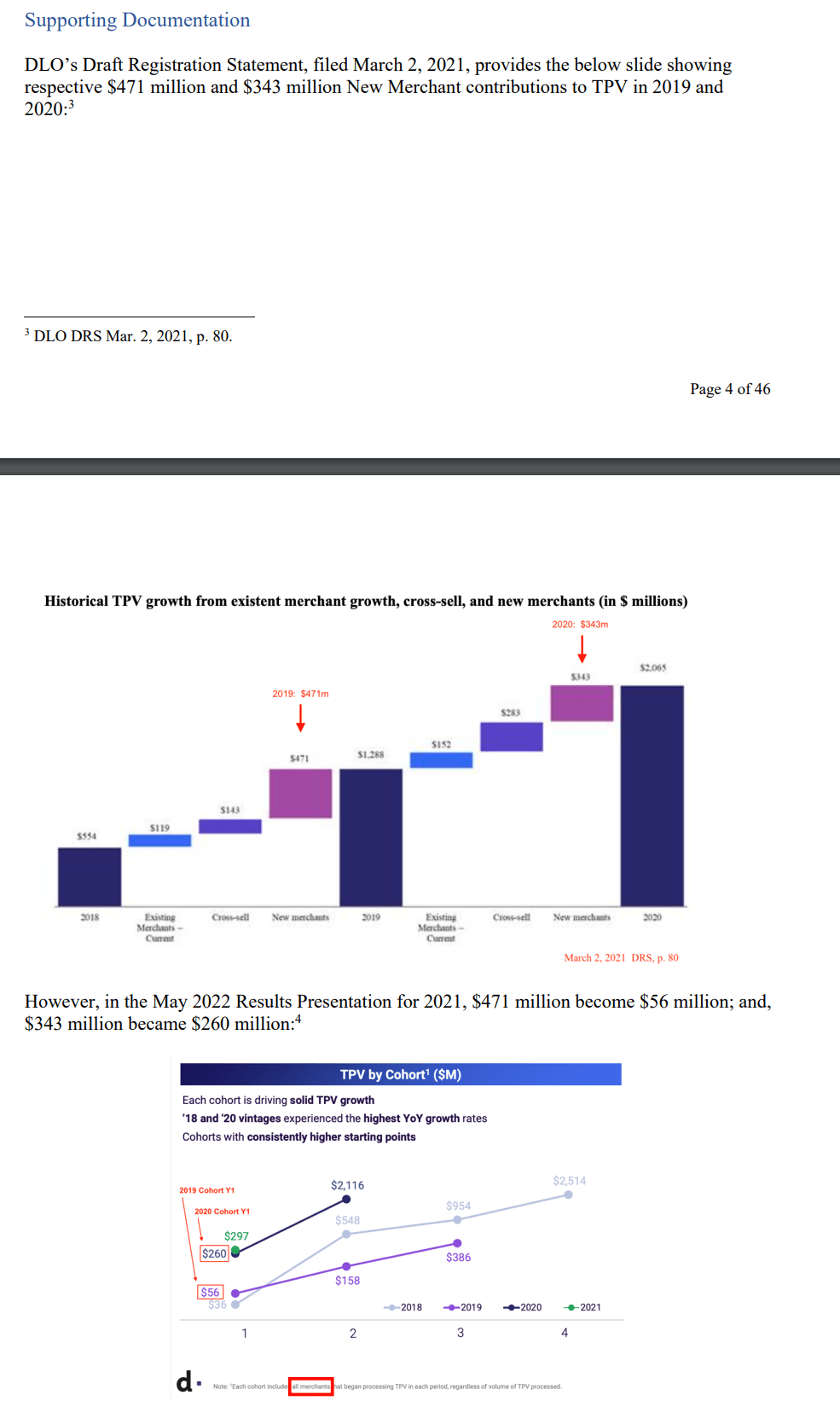

- Historical total processed volume figures, as well as some other figures like receivables, appear inconsistent across and within reports, including across SEC filings, and it's not clear why (there is growth regardless in all cases, just a very different trend line).

{kind=link}

Historical TPVs Appear Inconsistent (Pg 6-7 of Muddy Waters Report)

Remarks

Of course, the report raises concerns, and we don't like it when a stock we're looking at gets put in the crosshairs of a short-seller, correct or not. Moreover, with the risks in short selling nowadays due to short-squeezes being such a fresh mode of return for buyers, we really would never take a position.

But the real thing that got us looking elsewhere was just industry-level trends, related to the DLO business model.

DLO gets a lot of its take on processed revenue, more than half, from foreign exchange related fees, commissions and spreads. Their business is to provide a link between foreign, developed-currency businesses and emerging markets. This is a lite way for companies like Airbnb ( ABNB ) and others to dip a toe in foreign markets without getting their own local-to-local infrastructure in the country. The problem is when LatAm proves a good market for explorers, they eventually take the dive and make moves that cut out a lot of the value provided by DLO. In response, DLO chases volume with razor-thin payment processing contracts with major companies like Google ( GOOG ). Big companies like Google negotiate very low fees. The more companies dive into those markets themselves, the more the special value-add of DLO gets cut out. This should pressure take rates a lot.

While TPVs should grow, macro is getting a bit heavier, and the local-to-local markets that DLO has to compete in with contracts with Google and others are saturated. Still, they trade at 24x EV/EBITDA this year, forecast at 14x next year. We prefer businesses where the industry outlook is more stable, or conditions are likely to improve.

In response to the short-selling, DLO has declared that it will buyback $100 million in shares which is only about 2-2.5% of its market cap. This has rocketed the shares, maybe because it's putting pressure on short positions by the likes of Muddy Waters. Short interest is pretty high at 8.37% according to the Seeking Alpha figure. This doesn't address the short thesis points, but it's something of a non-silent counter. Still, it's a small buyback compared to what we've seen these last years.

Overall, we see no advantage in DLO, and with a high multiple in an environment where high multiples are not well-liked, on top of negative short-seller pressures, we'd pass on this as conservative investors.

For further details see:

DLocal Conducted A Major Buyback To Counter Short-Selling