DLO - DLocal: Emerging Market Exposure With High Growth And Margins

2023-05-22 12:21:25 ET

Summary

- DLocal Limited operates a payment processing platform globally.

- Revenue has grown at a CAGR of 93% in the last 3 years due to a rapid increase in new customers and markets.

- DLocal's margins are highly attractive, with an EBITDA-M of 30% and a NIM of 25%.

- Continued economic development should help the business drive continued growth in the next decade.

- We are concerned by the short report issued several months ago, which implies nefarious activities by Management. We suggest patience and alternatives, until the FY23 audit.

Investment thesis

Our current investment thesis is:

- DLocal (DLO) is a high-growth business, exploiting technological and economic development, to gain market share in the payments industry.

- The company has a compelling offering that will exploit global development over time, allowing the business to continue its strong growth trajectory.

- Margins may continue to trend down slightly, but should normalize at an attractive level.

- Our concern is the findings from the short report, which leads us to recommend other stocks.

Company description

DLocal Limited operates a payment processing platform globally. It enables merchants through its payments platform to get paid and to make payments online.

Share price

Similar to other LatAm payments companies, DLocal experienced a bountiful period on the stock market, receiving a premium valuation and much fanfare. Unfortunately, the payments bubble popped, and we saw a rapid decline in valuations, despite resilience in financial performance.

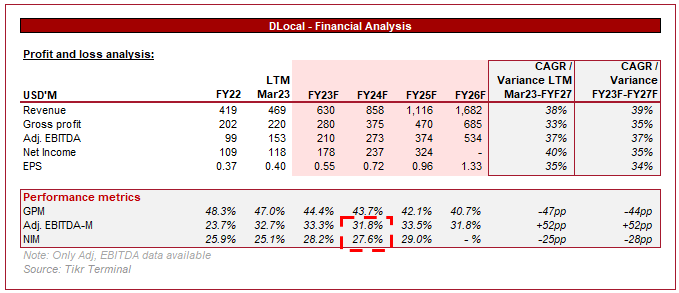

Financial analysis

DLocal financial (Tikr Terminal)

Presented above is DLocal's financial performance for the last decade.

Revenue

DLocal has grown its revenue at a CAGR of 93% in the last 3 years, as widespread adoption has spearheaded the company into global prominence on the payments stage.

The fintech industry has witnessed significant innovation in the last decade, particularly in the payment sector. This has been driven by cost-effective payment network development, as well as improved digital data analytics. Although this development has been led by the West, the rate of adoption in developing nations has been rapid. This is likely due to consumer trust in traditional institutions, with greater trust placed in mobile banking where finances can be easily tracked and understood.

For this reason, the adoption of smartphones has been the conduit for the development of the Fintech industry in these regions. This represents a strong runway for the fintech industry, as continued economic development lifts individuals out of poverty and toward the industry.

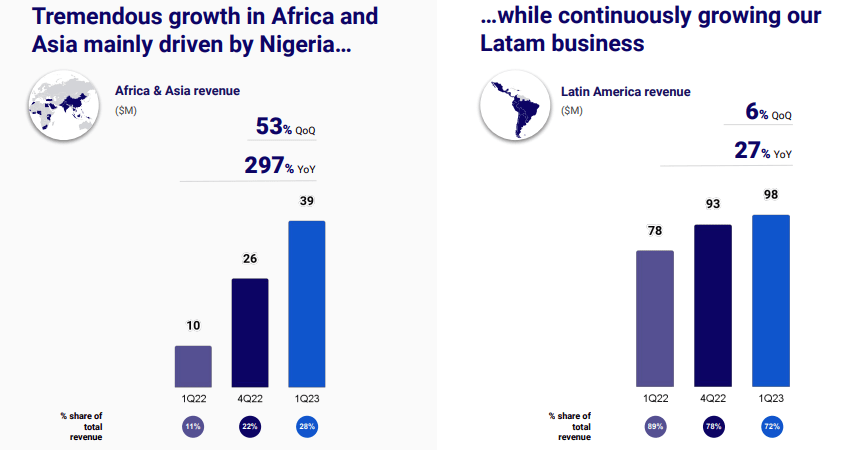

Further, this development will drive payment volume and the development of new businesses, as economies become consumer-centric. As the following data illustrates, DLocal has achieved impressive growth in both Africa and LatAm.

{kind=link}

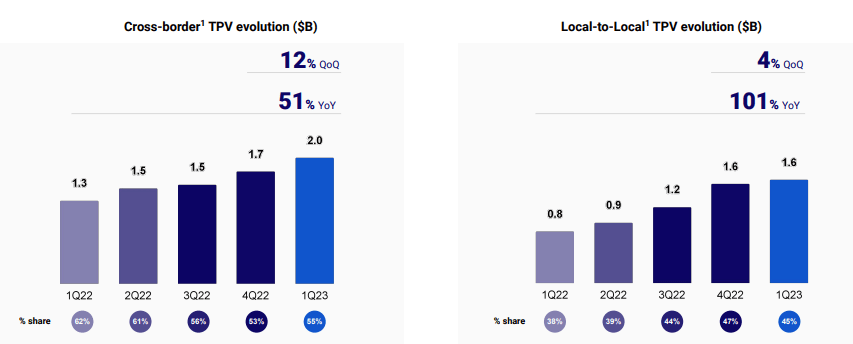

Cross-border e-commerce is on the rise globally, and emerging markets are becoming key players in this space. This has been supported by technological development, allowing for ease of transfer. Much of this traffic is from the West, where money is remitted to developing nations. Further, businesses are increasingly using these services as international firms expand into developing nations.

TPV and Cross border growth (DLocal)

{kind=link}

For DLocal, these factors represent a significant opportunity to continue its growth trajectory through economic development in its key geographies. As this occurs, the company will be in a position to develop its pricing strategy to be more lucrative, following the customer acquisition period.

With the growing volume of digital transactions, data privacy and security are a critical concern. Customer information is expected to be protected from cyber threats and unauthorized access, with legislation making it costly if there's a breach.

Muddy Waters' report

Muddy Waters Research is a research firm that conducts investigative research on public companies, generally looking to uncover anything from mismanagement to fraud (Imagine Hindenburg Research).

In Nov 2022, the company issued a short report on DLocal, stating "While we have found no pictures of its CEO wearing black turtlenecks , our research leads us to believe that DLO is likely a fraud."

Their key concerns are:

- DLocal used client funds to pay a special dividend to pre-IPO shareholders.

- Revenue manipulation through inflated FX income recognition.

- Mismanagement of clients' funds and lack of adequate controls, particularly segregation.

- Discrepancies in financial results. Examples include contradicting TPVs to receivables and payables to receivables.

- Series of "lies" within their reporting / disclosures.

DLocal refuted these allegations and conducted a share buyback package in response, which seems to have calmed markets.

DLocal is audited by PwC, which is one of the Big4 audit firms. These firms have been marred with scandals due to various cases of fraud/corruption globally, but are in the process of improving their internal processes.

Interestingly, many of the allegations relate to accounting transgressions. The expectation would be that at least one of these would be picked up by the auditor, especially as part of the FY22 audit process. PwC is seemingly continuing as auditor and issued a clean FY22 report.

Nevertheless, this is a major concern, especially if the non-audited metrics disclosed are incorrect. DLocal's short interest is currently c.11% , reflecting continued hesitancy around the business.

Economic consideration

Current economic conditions represent a risk for the business. With inflationary pressures negatively impacting consumers, we could see cross-border transfers and transaction volume decline.

Margin

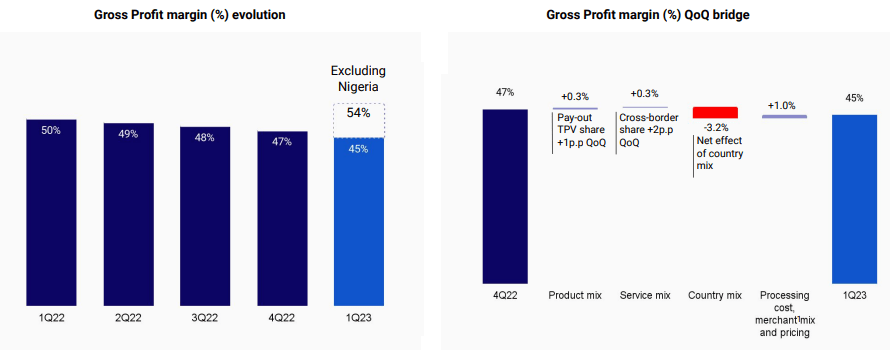

DLocal currently has an EBITDA-M of 30% and a NIM of 25%.

Margins have declined over the last 3 years as the business has rapidly expanded into less lucrative geographies in pursuit of growth. Management specifically highlights that without the impact of Nigeria, its GPM would be almost 10% higher.

Although subjective, we believe this is the correct decision. The company remains highly profitable, and so increasing scale is far more important in our view. If the company did not do this, new entrants into the market would bring the company's margins down through competition eventually anyway. The key is to actively protecting margins where possible, such as by launching products that utilize its current strengths.

{kind=link}

Q1 results

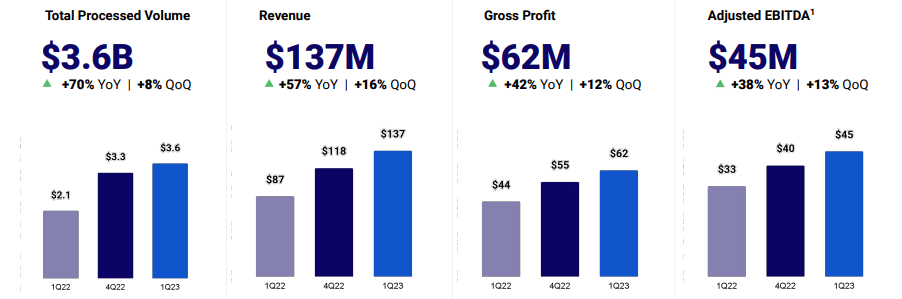

{kind=link}

Presented above is DLocal's most recent quarterly results.

The company has seen robust growth, although has certainly slowed Q/Q when compared to what has been achieved previously. This is potentially evidence of slowing conditions impacting the business.

Balance sheet

DLocal's balance sheet is relatively uneventful. The company does not use any material level of debt while gradually accumulating cash.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Revenue growth is forecast to be impressive, at a CAGR of 39%. This is a reflection of the company's current strategy, with global expansion allowing the business to gain market share quickly by utilizing its market expertise. This looks to be a reasonable directional assessment, but the reality will be dependent on new product launches, new markets, etc.

Margins are expected to remain flat, which looks to be a reasonable assessment given the dilution we have seen in recent quarters. We would lean toward further dilution, but Management will look to stem this as a priority.

Valuation

DLocal is currently trading at 25x LTM EBITDA and 35x earnings. If this was a Western business with these financial metrics, the company would likely be trading at a far higher multiple.

The issue is that forecasting where growth and margins will land in the coming decade is almost impossible, but with the added complexity that economic conditions in Africa and LatAm are equally unknown. What we expect is that economically, conditions will be further progressed, which should mean growth. If we consider mature fintech businesses in the West, it is possible to normalize in excess of 20%.

Based on these factors alone, DLocal would be a buy. The issue is this Muddy Water report, which muddies the assessment. We propose that investors remain patient with DLocal, to see if anything comes out of the FY23 audit and continued scrutiny of the business. Instead, investors should consider StoneCo ( STNE ) or PagSeguro ( PAGS ) if they are seeking Fintech exposure in emerging markets. StoneCo and PagSeguro are trading at 3x EBITDA, reducing investor risk relative to DLocal. We have analyzed both businesses in detail here and here , and consider them both a buy.

Final thoughts

DLocal has all the characteristics to be a long-term winner. It is growing quickly and has impressive margins. Economic development in LatAm and Africa should help drive volume growth in the coming decade and allow DLocal to reach scale.

Our only concern is the findings from Muddy Water, which, despite the market response to the news, remains a continued issue. DLocal is not a unique business, however. LatAm has several fintech businesses with an equally lucrative trajectory, and they represent lower risk for investors.

For further details see:

DLocal: Emerging Market Exposure With High Growth And Margins