ADYEY - DLocal: One Of The Best Emerging Markets Bets

2023-12-06 12:39:50 ET

Summary

- DLO offers payment solutions and currency conversion services for businesses expanding into emerging markets.

- The company reported strong financial results in Q3, with increased payments volume and gross profit, and reaffirmed its 2023 guidance.

- DLO's valuation is attractive compared to its peers and presents a potential upside of 55% according to a DCF model.

Investment Thesis

DLocal ( DLO ) was one of my favorite stocks during 2022 until the short report from Muddy Waters caused the stock to crash by 50% (luckily, I wasn't holding the stock). After that, I lost track of the company. However, it recently caught my attention again after reading that they hired the former CFO of Mercado Libre as co-CEO.

DLO helps companies solve a crucial issue when operating in emerging markets: how to pay and get paid. As we will see, it is a very profitable and fast-growing market. But more importantly, I see the stock trading at a reasonable to cheap valuation. So, a fast growing company trading at a discount? Yes please.

Business Overview

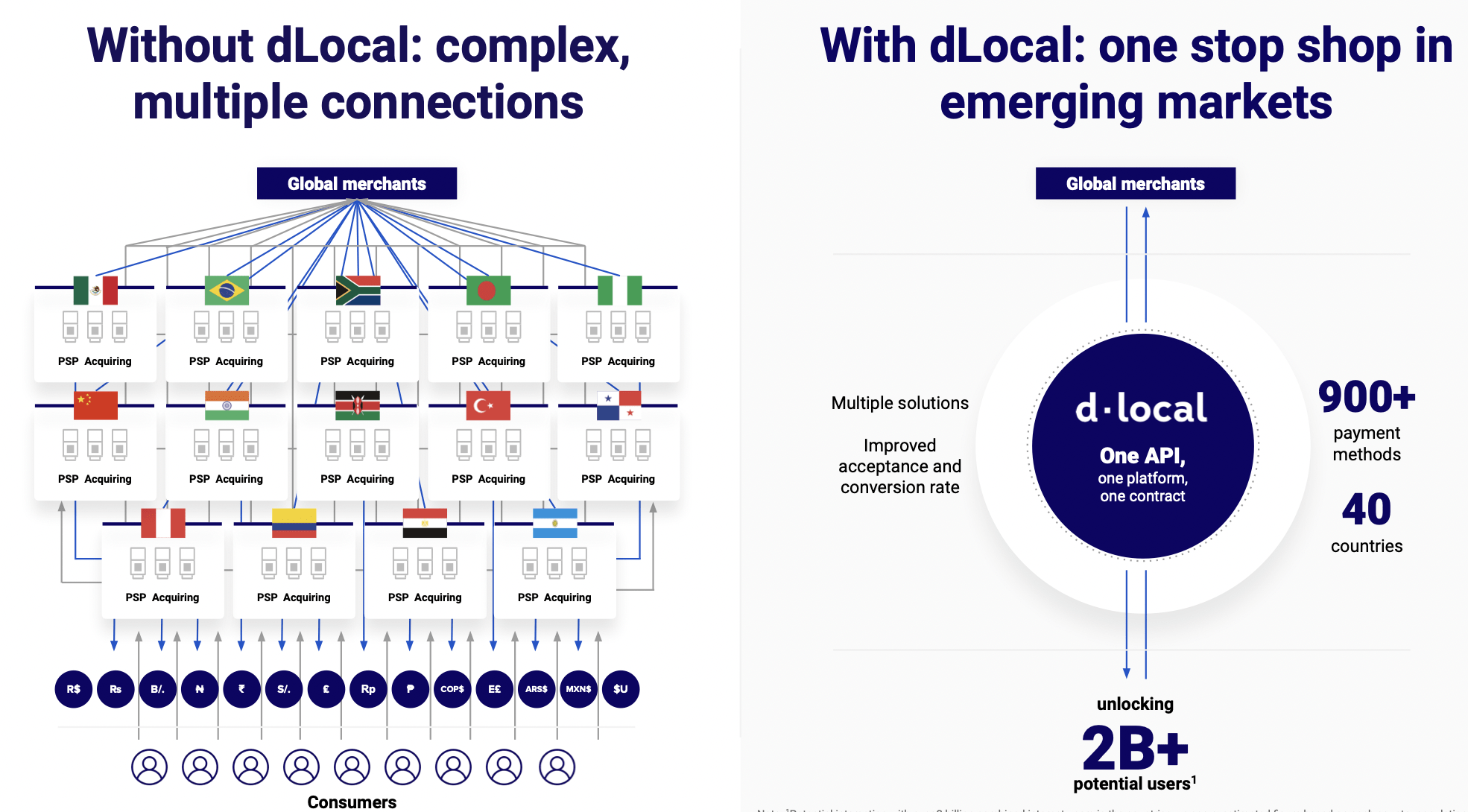

Let's say Spotify (SPOT) is thinking about expanding its services to Argentina. The main challenge they face is figuring out how to bill their customers there and comply with taxes and regulations. Enter DLO – they step in and say, 'Hey Spotify! We'll handle charging your customers in Argentinian Pesos, transfer the funds to you in Euros in Sweden, and take care of taxes and compliance with all the rules.' Of course, in exchange, DLO takes a nice fee.

And what if Spotify needs to pay a local supplier in Pesos? Well, they can simply send the Euros to DLO, and DLO takes care of converting the currency and paying the supplier in Argentina. This type of transaction is what they refer to as pay-outs.

However, DLO can also manage pay-ins, which means handling the transactions inside of a country. Pay-ins don't involve FX conversion, causing the take rate to be lower. To complete their ecosystem they also have a feature for fraud prevention and an "issuing-as-a-service" platform.

The company currently operates in 40 countries and is able to accept more than 900 payment options. As of the end of 2022, they had more than 600 merchants including Google (GOOG) (GOOGL), Meta (META), Shopify (SHOP), Salesforce (CRM), and more.

DLO Q4 2022 Earnings Presentation

{kind=link}

YTD Financial Results

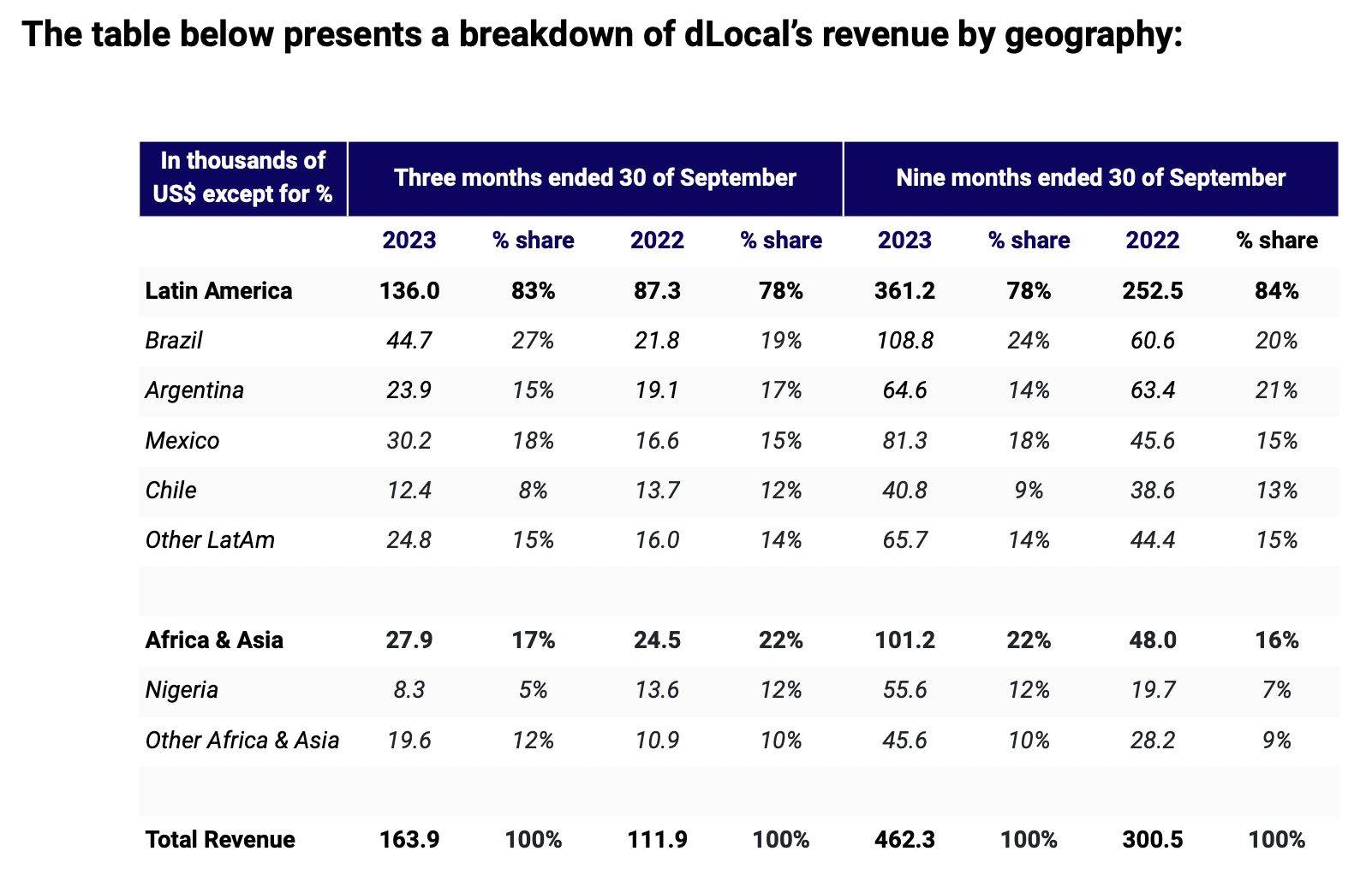

DLO reported Q3 financial results on November 21. TPV increased 69% year-over-year to $4.6 Billion. Cross-border transactions, where DLO collects in one currency and settles in another, constituted 49% of the TPV, growing 46% YoY. Local-to-local transactions comprised 51% of the TPV, up 99% YoY.

Sales were up 47% year-over-year to $164 million, while gross profit came in at $75 million up 38% year-over-year. The gross take rate (gross profit over TPV) decreased 60bps YoY and 20bps QoQ to 3.5%. The take rate was impacted by a larger share of local-to-local transactions in the TPV, which has a lower take rate since it doesn't involve FX conversion and additional fees.

The fastest-growing countries were Brazil and Mexico, both more than doubling revenue YoY. When asked whether these growth rates were sustainable in the earnings call , the management said:

A significant portion of that growth is a consequence of our platform product that we launched last year and is really solving complex payment flows for very large global marketplaces across those markets. And so everything seems to point to the direction of high levels of merchant satisfaction that we're solving complex problems for them across these markets. And therefore, we are still positive about those markets despite the fact that they are our largest markets and are quite stable markets.

{kind=link}

The company reported adjusted EBITDA of $56 million, an increase of 34%, and a net income of $40 million, up 25% YoY. The net take rate was 1.6%, constant QoQ but down 40bps YoY.

X: @7amahanti

DLO also reaffirmed full-year 2023 guidance, expecting to hit the upper range of revenue and mid-range of EBITDA guidance. Revenue is expected to be between $620 million and $640 million and adjusted EBITDA of $200 million to $220 million.

Valuation

One of the things that we most like about DLO is its valuation. The stock is currently trading at 21x expected 2024 EPS. When compared to its peers, it is not exactly the cheapest (Shift4 Payments ( FOUR ) trades at 17.6x, StoneCo ( STNE ) at 14.1x, and Adyen ( ADYEY ) at 47.6x), but we have to take into account that it is the fastest growing. Moreover, DLO has almost no share-based compensation (only $8 million in 2022), and its non-GAAP numbers are very close to the actual GAAP numbers. In other words, they don't add up costs to seem more profitable than what they really are.

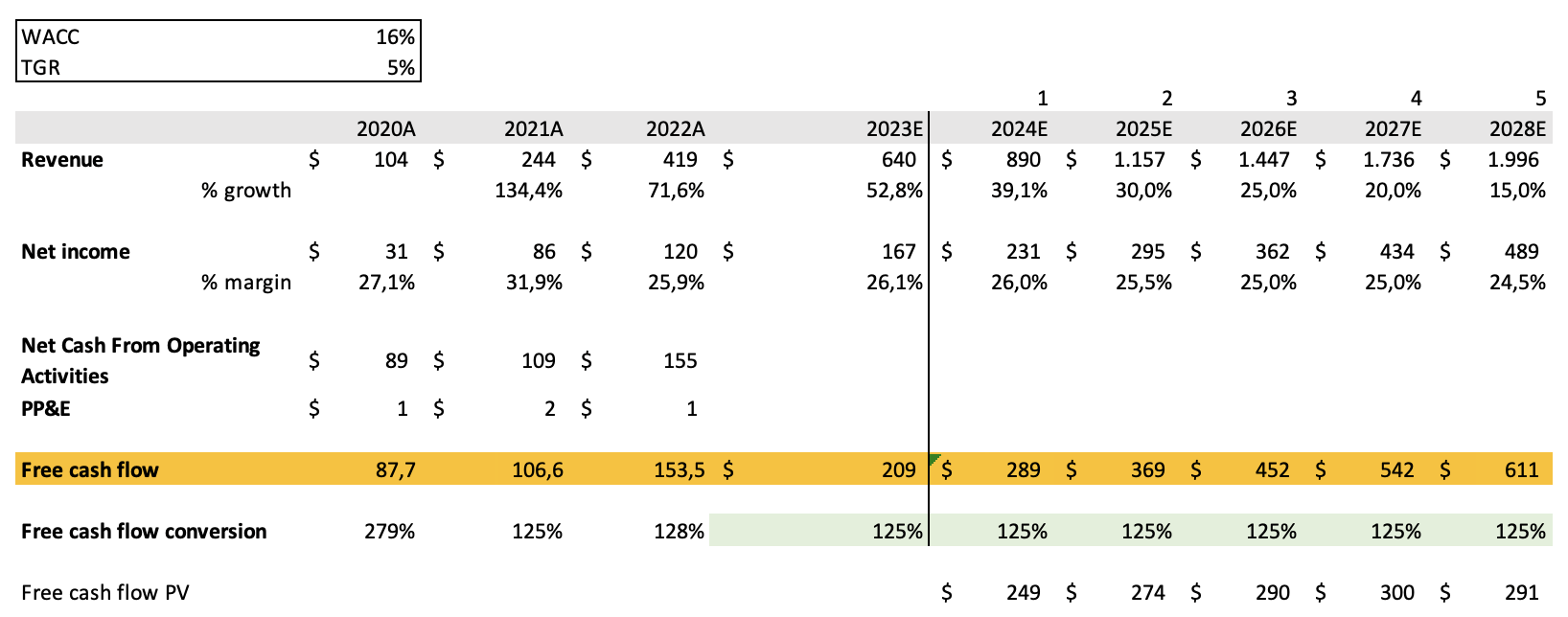

We also decided to do a DCF model. For the model, we assumed a conservative 125% free cash flow conversion rate, in line with previous years, although it might be higher in 2023. Moreover, we used the 2024 revenue estimate from analysts and projected a growth slowdown of 5% per year in the following years. Lastly, we estimated a net margin falling around 0.5% per year as the net take rate drops as well. We also assumed a WACC of 16% and a TGR of 3%.

{kind=link}

Although DCF's are not super reliable, the stock seems like a steal right now. We're looking at around $27 per share compared to the current $17.50. That's a potential upside of 55%.

Author

As rates head lower and the markets begin pricing in a rate cut in 2024, we believe there is a high chance that the stock will rally stronger than the market and re-rate closer to our DCF price target.

Risks

DLO operates in emerging markets, which can sometimes be politically and economically unstable. During Q3, the Nigerian Central Bank decided to devalue the Naira against the dollar . How does this affect DLO? The company will be booking a smaller amount in revenue. For context, if we excluded Nigeria from the Q3 results, sales would have been up 55% vs. 47% as reported. However, DLO will also be booking a similarly smaller amount in costs. This means that the margin remains more or less constant, but the profit amount in dollars will fall.

A similar situation is almost guaranteed to happen in Argentina in the coming months, where the official spot rate for the USD is $380 pesos, while the 'black market' swap rate is $950 pesos per dollar. Argentina represents 15% of DLO's total revenue.

Another risk we cannot overlook is the short report from Muddy Waters almost a year ago. Although it raised several red flags, things have been cleared up, and I think the best signal was the incorporation of Pedro Arnt as co-CEO of the company. Pedro was previously the CFO of MercadoLibre ( MELI ) and has an outstanding reputation. Why would he risk that by coming to DLO if, indeed, the short seller was right? I believe this is well past us now.

Takeaway

To sum up, DLO provides critical infrastructure for international companies to penetrate developing countries. I anticipate significant growth ahead, and despite the risks, I also envision considerable upside for the stock in the coming years.

For further details see:

DLocal: One Of The Best Emerging Markets Bets