DLO - DLocal Q3 Earnings: Foreign Fintech Fears Overcoming Skepticism

2023-11-22 06:04:45 ET

Summary

- DLocal's Q3 results slightly missed estimates, causing a premarket dip in the stock.

- DLO stock is attractively priced at around 14x EBITDA for a rapidly growing fintech.

- Despite some short-term challenges, the underlying business's profitability is robust, and Q4 revenues are expected to maintain a strong growth trajectory.

Investment Thesis

DLocal ( DLO ) delivered Q3 results that marginally missed estimates on the top and bottom lines. And the stock fell premarket. That's the headline. But the more nuanced results underscore plenty of positive aspects.

Yes, the outlook here is far from blemish-free. But I maintain that there's a lot to like in this stock, particularly that paying around 14x EBITDA for a rapidly growing fintech is an attractive entry point.

Rapid Recap

In this excerpt that follows I highlight the crux of my position from my bullish analysis back in August:

[...] when the underlying business matures, DLocal should be able to get its EBITDA over gross profits higher than 75%, compared with 74% reported in Q2. In other words, DLocal is clearly highly profitable already, and it doesn't take too much imagination to see its profitability improving further.

Author's work on DLO

As we know now, the stock is down premarket, as DLocal's underlying profitability didn't live up to investors' expectations. But I get ahead of myself. In the first case, let's discuss what DLocal does and its near-term prospects.

DLocal's Near-Term Prospects

DLocal is a Uruguay-based fintech and international payments company. DLocal specializes in cross-border payment solutions and payment processing for businesses in emerging markets.

Through its "One DLocal" model, it simplifies and transforms the online payments landscape by enabling global enterprise merchants to receive payments and make payments using a single API.

Its platform offers a suite of products, including pay-in and pay-out solutions, local-to-local capabilities, catering to both cross-border and local transactions. The company's focus is on facilitating online commerce in emerging markets, enhancing acceptance and conversion rates for businesses operating in diverse regions.

Moving on, investors wanted to back a rapidly growing fintech with exposure to South America and Africa. And they'd be guided to expect that a devaluation of the Nigerian Naira would see a slowdown in its revenues, but not compress its gross profit line. But as you'll soon see, when its results got posted, its gross profit margins did compress. Hence, even though the results were strong for the company, they did have some pesky detractions that weighed on the stock.

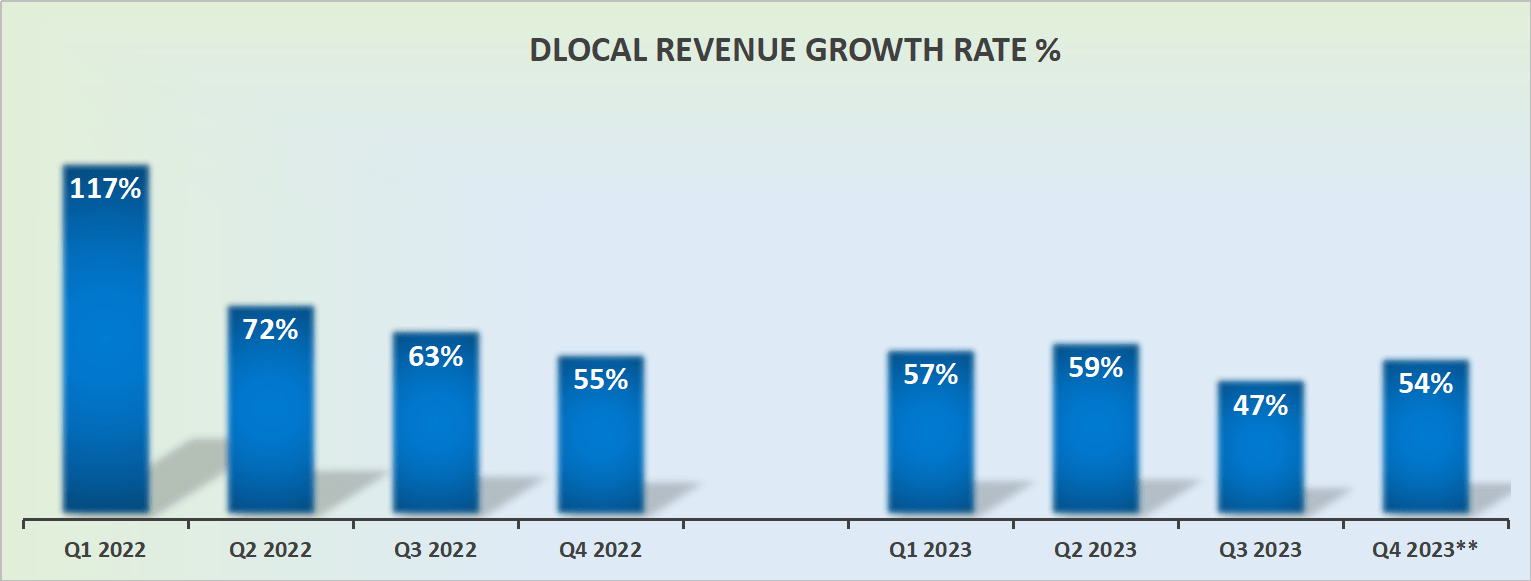

Revenue Growth Rates Remain Strong, With a But

{kind=link}

Ultimately, I believe that DLocal will see its Q4 2023 revenues reaching around 54% y/y CAGR. However, this is where things get complicated, management only reaffirms its guidance and thereby only reiterates what they'd been guiding towards since earlier in 2023.

To put this more concretely, Q4 could very much come in at around 54% y/y increase, but management didn't want to firm up its guidance for Q4, which means that there's some room for revenues to not come in quite as strong as the market had been hoping to see.

In other words, investors wanted to be blown away by DLocal's Q4 guidance, but the fact that management left some room for negative expectations wasn't taken positively by investors.

But I do not believe this room for doubt changes the medium-term prospects that this business is on a path to deliver.

DLocal's Profitability Has Many Moving Parts

DLocal's gross profit margins in Q3 2023 were just over 45%, whereas in Q3 2022 its gross profit margins were slightly over 48%, meaning that there's a 300 basis compression y/y, which is a meaningful compression in gross profits in a short period of time.

Even though management sought to reassure investors that its gross margin compression was short-term in nature and that its medium-term prospects remain alluring, investors didn't take this noteworthy change in gross profit margins too well.

Looking ahead it leads one to believe that there's a change in underlying profitability. Case in point, Q4 points to around $65 million of EBITDA at the high end of its guidance, which is around 66% y/y increase from the prior year.

However, given that its gross margin compressed by approximately 300 basis points from the prior year, investors are weighing up this strong guidance in EBITDA and questioning just how sustainable it's likely to be.

Thinking Through DLocal's Valuation

When it comes to it, investors are attempting to build conviction on whether or not the underlying business is cheaply valued.

As it stands right now, one must form some sort of view on 2024. And if one presumes that in 2024, its EBITDA line was to grow by around 45% y/y, this would see its EBITDA reaching approximately $320 million, which means the stock is priced at 14x EBITDA, a valuation that is typically highly enticing.

That being said, the problem here is that this stock is viewed as foreign. As such, when it comes to investing overseas in overseas companies, investors are extremely risk-averse, so unless the company's results are pristine, there's always some level of embedded skepticism that weighs on the stock.

Consequently, unless the stock is truly in the bargain basement, investors are easily spooked and looking to cash in at any hiccup in the road. Even though I argue that investors are not going to find too many profitable fintech companies growing at very rapid rates, with strong profitability priced cheaply. Not in this market.

The Bottom Line

While DLocal is facing a premarket dip following Q3 results that marginally missed estimates, a closer analysis reveals several positive indicators for the stock.

Despite some short-term challenges, the stock is positioned attractively, trading at around 14x EBITDA for a rapidly growing fintech.

The dip in stock post-results may be an opportunity for investors, as the underlying business's profitability is robust, and the anticipated Q4 revenues could maintain a strong growth trajectory.

Despite temporary gross profit margin compression, management reassures investors of the medium-term attraction, and the valuation at 14x EBITDA suggests an enticing investment opportunity, especially considering the scarcity of similarly profitable fintech companies with rapid growth.

Even though it's a foreign stock and therefore is often more volatile than US-based companies, the underlying fundamentals and potential for sustained growth make DLocal an intriguing prospect for investors seeking exposure to the burgeoning fintech landscape.

For further details see:

DLocal Q3 Earnings: Foreign Fintech Fears, Overcoming Skepticism