WDI - DLY: A Strong ~9.6% Distribution Yield From This Multi-Sector Fixed-Income Fund

2023-12-28 06:22:19 ET

Summary

- DoubleLine Yield Opportunities Fund is trading at a reasonable discount, while its underlying portfolio is also trading at a deep discount.

- The fund's discount has been more volatile lately, but its underlying portfolio and the latest report show a mostly stabilized fund.

- At the same time, other alternatives outside of the DoubleLine trio of closed-end funds could still be more interesting choices.

Written by Nick Ackerman, co-produced by Stanford Chemist.

When we last discussed the DoubleLine Yield Opportunities Fund ( DLY ), I suggested that Western Asset Diversified Income Fund ( WDI ) may be a better alternative to holding DLY. That continues to remain true, with WDI being the more attractively priced multi-sector bond fund; however, DLY also continues to be the best value in the DoubleLine trio of closed-end funds . With the caveat, the trio of DoubleLine funds are all quite differently tilted, meaning that an argument could be made that holding all three could still provide sufficient diversification.

That could be true between DLY and WDI as well. In fact, I still own both funds because the discount for DLY has been quite volatile since that prior update. Additionally, WDI's discount has tightened up meaningfully since the update and has come down to a high-single-digit from the nearly 14% discount it was at the time. Overall, it has been a fairly short period of time, but swapping to WDI would have been the better choice on a total share price basis.

Interestingly, the total NAV results during this period for each fund were quite close. That's what we want to see in a good swap pair, but over longer periods of time, these funds could diverge more significantly due to different exposure.

With all that being said, we are going to give DLY another look today after the latest annual report is posted. For the most part, it really hasn't been anything too exciting, as the fund has been able to perform fairly steadily in terms of distribution coverage. The fund remains tilted towards non-agency MBS, and the portfolio over the last year stabilized considerably relative to the prior year.

The Basics

- 1-Year Z-score: -0.17

- Discount: -6.61%

- Distribution Yield: 9.53%

- Expense Ratio: 3.42% (including interest expense)

- Leverage: 19.49%

- Managed Assets: $869 million

- Structure: Term (anticipated liquidation date February 25th, 2032)

DLY's investment objective is quite simple: "seek a high level of total return, with an emphasis on current income." To achieve this, the fund will "invest in a portfolio of investments selected for its potential to provide a high level of total return, with an emphasis on current income. The Fund may invest in debt securities or other income-producing investments of issuers anywhere in the world, including in emerging markets, and may invest in investments of any credit quality."

DLY is a multi-sector fixed-income fund with the flexibility to really invest in just about anything and anywhere and at any time. That flexibility leaves the portfolio managers to invest where they feel capital might be best put to work. While the fund carries a diverse basket of exposure to a wide mixture of assets, they have tended to tilt more into mortgage-backed security exposure in both residential and commercial.

The fund's expense ratio climbed from their prior fiscal year, but that is to be expected due to the higher interest expense on their borrowings - which is what we had already previously noted.

However, it is also worth noting that this fund continues to remain only modestly leveraged relative to their CEF multi-sector bond fund peers such as PIMCO and also including WDI. They once again took leverage down from the prior fiscal year.

{kind=link}

The fund pays a rate of one-month SOFR plus 0.10% plus 1.15%. The latest average interest rate in their report comes in at 5.92%.

Discount Looking Attractive

Shortly after the launch of this fund, it screamed higher to an unusual premium. However, that was short-lived, and it quickly sank to a discount. That's just the usual pattern for a new CEF IPO, even a CEF 2.0, which was aimed at addressing that issue.

While the fund's discount has narrowed from where it was a year or so ago, it remains at an attractive level. It currently is trading right around the fund's average since its launch. That would put it at a more neutral level; certainly not overly priced, but it isn't necessarily looking cheap either. That said, given the underlying portfolio is already discounted from its own par levels, the argument could be made that it is still cheap at this time.

We'll discuss that more below, but the main argument against that would be that most multi-sector fixed-income funds are seeing the same thing. That is, if DLY's portfolio is trading at a deep discount with a fairly attractive discount on the fund level, then another fund, such as WDI, will also be seeing a deep discount on its underlying portfolio. At the same time, it also carries an even deeper discount on the fund level.

Latest Distribution Coverage

Since the fund's launch, they've paid out a monthly distribution of $0.1167, and they continue to do so today.

Despite taking leverage down year-over-year, the fund didn't experience a negative impact on its net investment income. In fact, we even saw a small positive lift. This is because the cost of borrowings rose dramatically for the fund as they borrowed at the short-term rate, as described earlier in this article. Therefore, the hurdle of investments that they have to invest in has to have an even higher yield to have the borrowing costs make sense, plus the fund's other operating expenses.

Simultaneously, the fund's floating rate exposure, such as their collateralized loan obligations, bank loans and MBS holdings, all helped lift yields of their underlying portfolio names as well.

Putting both of these moving parts together has translated into the fund's NII staying relatively stable despite rocketing interest rates. The NII rate rose to 8.52% from 7.01% the prior year.

{kind=link}

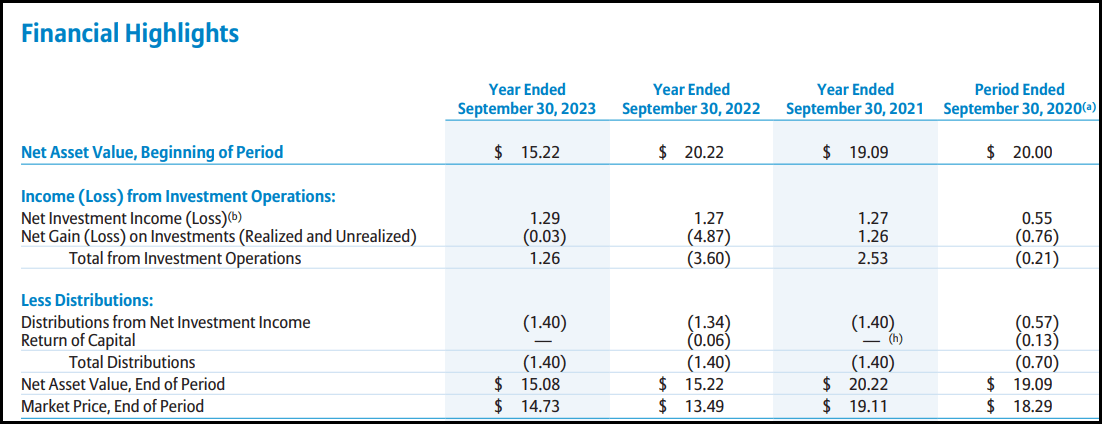

Instead, the underlying holdings had been the more volatile piece of the puzzle for this fund. In the last fiscal year, as rates stabilized, so too did the fund's portfolio. With a realized/unrealized loss of only $0.03, things are looking much more stable than what was essentially the crash of $4.87 per share in fiscal 2022.

Given the stabilization of the portfolio and stable NII, I would suspect that the fund will continue to maintain the current distribution. Although the fund has a lack of coverage, with NII coverage at ~92%, this is something they seem comfortable with. It's also not that excessively large of a gap that some potential future appreciation couldn't cover. However, I do generally want to see NII coverage of fixed-income funds at over 100%.

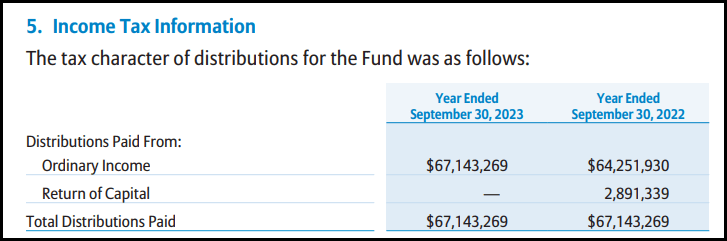

The tax character of the distribution is largely ordinary income, making it more appropriate for a tax-sheltered account. This makes sense and is what we would expect to see with a fixed-income fund.

{kind=link}

DLY's Portfolio

The types of losses in the underlying holdings are also something we would expect to see due to the interest rate sensitivity of fixed-income investments. That being said, credit risks will play a role in DLY because of the higher exposure of below-investment-grade quality in their portfolio. Junk-rated debt comes to ~62% of their portfolio, with another ~16.4% allocated to unrated securities.

With a lower-rated credit quality portfolio, the trade-off is a relatively lower duration or interest rate sensitivity. For DLY, they put the duration of the portfolio at 3.82 years with a weighted average life of 6.08 years.

DLY Portfolio Credit Quality (DoubleLine)

Defaults remain low but have been accelerating and are expected to do so going forward. So, the stabilization of the portfolio was great to see, and if rates continue to go down or even stabilize, that should also bode well for DLY's portfolio. The risk would be that next year, the economy slips into a deeper economic slowdown, and that would damage the fund's portfolio. The damage would be worse given the leverage; even if it is modest, the fund is still subject to more volatility.

Besides DLY carrying a discount, these underlying holdings are also reflecting the pricing of default risks rising going forward. The average market price for the underlying holdings comes to $82.45, reflecting a deep discount. This was nearly the same as it was earlier this year when the average market price was $82.67 - as we would expect, given the stabilization of the fund's NAV.

Overall, the fund's portfolio hasn't had any drastic changes. However, they did change what colors coordinate with which sleeve of the portfolio, so that makes it more fun to look for differences. Most changes were within a few percentage points of each other, which simple gyrations of valuations in the portfolio could cause. The fund's turnover rate was 14% in the last fiscal year, putting it on the low end of the fund's historical turnover rate.

DLY Sector Breakdown (DoubleLine)

Conclusion

DLY is trading at an attractive discount, and its underlying portfolio is trading at an even more substantial discount. The fund provides diversified exposure as a multi-sector bond fund. The fund's positioning and deleveraging have resulted in the fund's NII being stable, and that should bode well for the continuing distribution being maintained.

The fund might have peers that are looking a bit more attractive, but I'm still comfortable holding this fund at the current level. At the very least, I'm getting exposure to the DoubleLine name, and that means management diversification.

For further details see:

DLY: A Strong ~9.6% Distribution Yield From This Multi-Sector Fixed-Income Fund