DLY - DLY: Shares Delivering Misleading Information Fund Is Overdistributing

2023-09-24 01:42:58 ET

Summary

- The DoubleLine Yield Opportunities Fund offers a high level of income with a current yield of 9.53%, significantly higher than most equity income funds.

- The fund has outperformed other debt funds, with a 5.03% increase in share price and a 15.94% total return over the past year.

- The fund's focus on total return is surprising given its investment in debt securities, but its performance may be attributed to investments in floating-rate securities and emerging markets.

- The fund's shares in the market have delivered a substantially higher total return than the portfolio, which may be misleading investors.

- The fund has been failing to cover its distribution over the past eighteen months, as its net asset value has been consistently declining. As such, a cut may be coming.

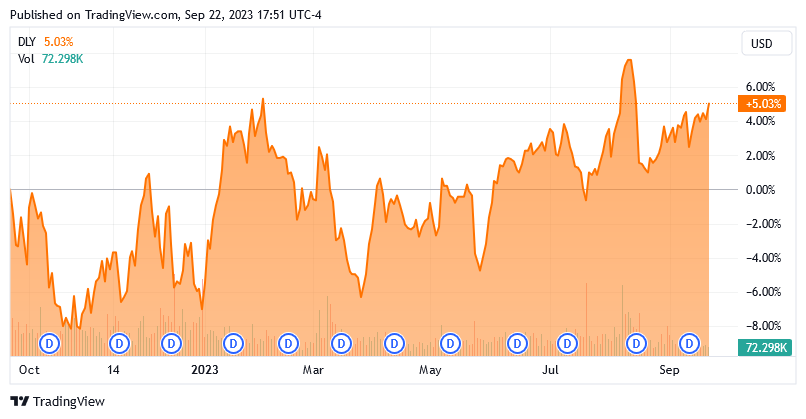

The DoubleLine Yield Opportunities Fund ( DLY ) is a closed-end fund that can be used by investors that are seeking to earn a very high level of income from their portfolios. The fund’s income-generation potential is immediately apparent in the fund’s current 9.53% yield, which is significantly higher than the yield of most equity income closed-end funds as well as the S&P 500 Index ( SPY ). However, there are several bond funds that boast a higher yield than this one, but this can partly be explained by the performance of this fund relative to many other closed-end funds that also invest in debt securities. Over the past year, the DoubleLine Yield Opportunities Fund is up 5.03% with respect to its share price:

{kind=link}

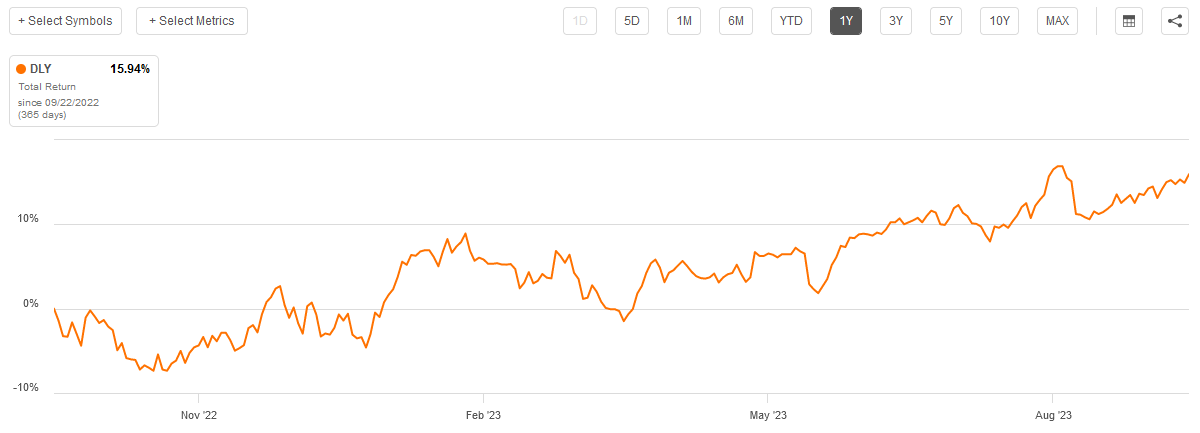

The fund’s total return over the period is even more impressive, as investors who purchased shares of this fund a year ago would now be 15.94% richer:

{kind=link}

This is, to put it mildly, a performance that greatly exceeds that of most other debt funds on the market. After all, the rising interest rate environment has caused the prices of just about any bond fund to decline. It would be wise to investigate the factors that differentiate this fund from other debt funds in order to determine the source of the market attraction for this fund, as well as its potential to continue this strong performance going forward.

As regular readers may recall, we last discussed this fund back in July. At that time, I mentioned that the fund could have some risks surrounding it, particularly because it has been consistently failing to generate sufficient investment profits to cover its distribution. That was a few months ago though, so it is conceivable that some things have changed since that time. Let us revisit this fund today and see if we need to update our thesis.

About The Fund

According to the fund’s webpage , the DoubleLine Yield Opportunities Fund has the primary objective of providing its investors with a high level of total return. This is an unusual objective considering that the name of this fund suggests that it is investing in debt securities. The description of the fund’s objective from its webpage confirms that assumption:

The Fund will seek to achieve its investment objective by investing in a portfolio of investments selected for its potential to provide a high level of total return, with an emphasis on current income. The Fund may invest in debt securities and other income-producing investments of issuers anywhere in the world, including in emerging markets, and may invest in investments of any credit quality.

Technically, the term “income-producing investments” could refer to anything that has a yield, including dividend-paying common equities. In fact, there are some closed-end funds that use that phrase to describe common equity investments in master limited partnerships or real estate investment trusts. However, in this case, the fund appears to be specifically referring to debt securities such as bonds. As of the time of writing, 96.57% of the fund’s assets are invested in bonds, with the remainder in a variety of other things:

CEF Connect

The fact that the overwhelming majority of the fund’s assets are debt securities is what makes the fund’s focus on total return surprising. I explained why this is the case in my previous article on this fund:

As a rule, bonds provide all of their investment return in the form of direct payments to their investors. A bond investor purchases a newly-issued bond at face value, collects a regular coupon payment from the issuer that corresponds to interest on the loan, and then receives the face value back when the bond matures. There are no net capital gains over the life of the bond because bonds have no inherent link to the growth and prosperity of the issuing company. Thus, the bond’s yield is the only source of net investment returns.

As bonds have no net capital gains over their lifetime, they are current income vehicles, not total return vehicles. This is why the fund’s focus on total return is a bit surprising, even if it does state that it expects the majority of its total return to come in the form of direct payments from the securities that it holds.

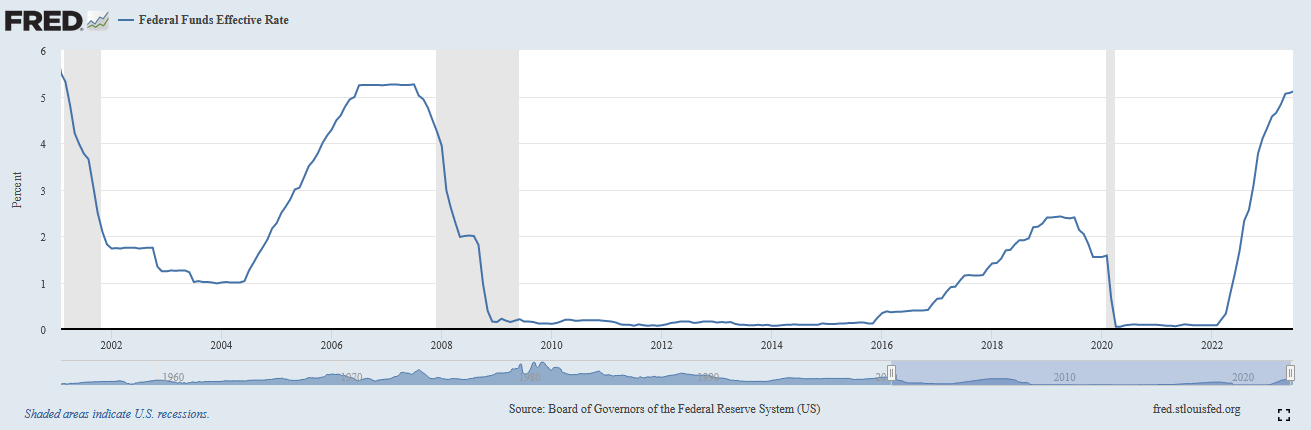

With that said, the price of bonds varies inversely with interest rates, so it is possible to make some profits by exploiting price fluctuations. This inverse correlation makes the fund’s price performance over the past year rather surprising. As everyone reading this is no doubt well aware, the Federal Reserve has been very aggressively raising interest rates in an attempt to combat the very high inflation that we have been experiencing in the United States. As of the time of writing, the effective federal funds rate is at 5.33%, which is the highest level that has been seen since February 2001:

{kind=link}

We immediately note two things here:

- The current interest rate is quite a bit higher than the last time that we discussed this fund. At the time the last article was published, the effective federal funds rate was at 5.08%. Thus, the benchmark interest rate in the economy has risen by 25 basis points.

- The economy in 2001 was quite a bit stronger than the one that we are currently in. There was much less debt in the economy, the national debt was a lot lower, and the economy as a whole was not addicted to extremely low interest rates.

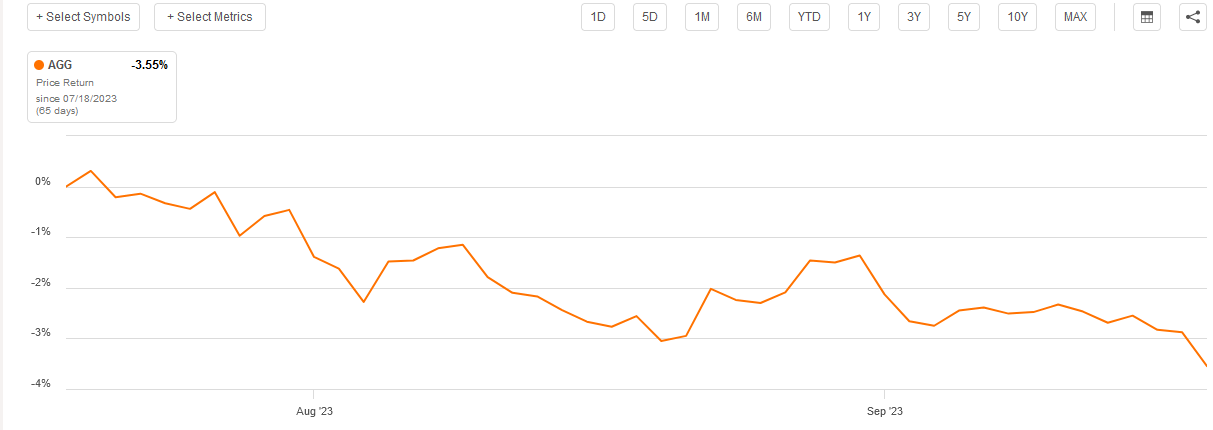

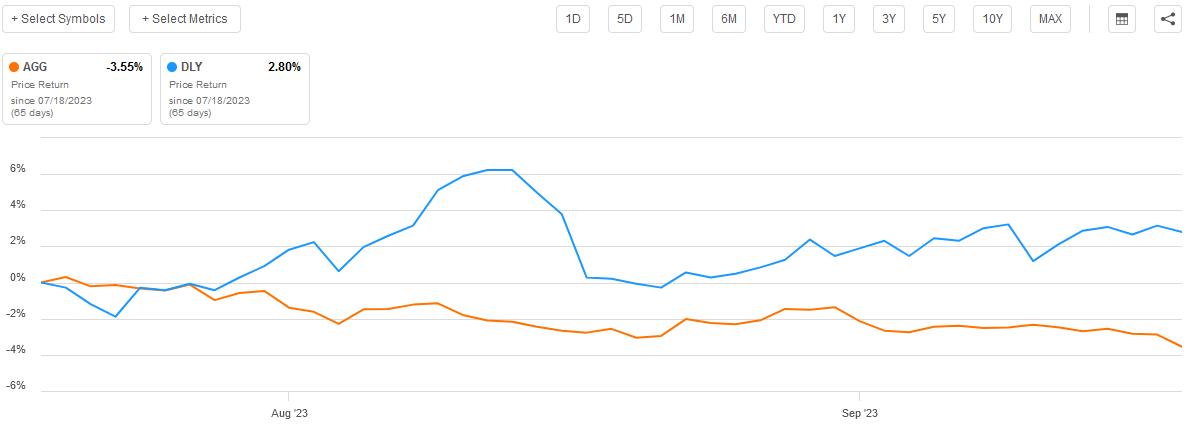

Of the two items, the first is the most important for the purpose of our analysis. The fact that the effective federal funds rate has risen by 25 basis points can be expected to have a negative impact on bond prices. In fact, that is what happened as the Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 3.55% since July 18, 2023, which is the date that the prior article on this fund was published:

{kind=link}

Curiously though, the DoubleLine Yield Opportunities Fund is up 2.80% over the same period:

{kind=link}

This fund has clearly managed to outperform the index by quite a lot. This has been the case over most of the past year.

As I noted in a previous article , debt securities that have a floating rate tend to hold their value much better than fixed-rate bonds in a rising interest rate environment. This is because the interest rate that is offered by the floating rate securities will always be competitive with the interest rate on newly issued bonds. After all, the reason why bonds fell in price so sharply is that it makes no sense to buy a bond yielding 1% (for example) when any investor could easily purchase a brand-new bond yielding considerably more than that. Thus, if the DoubleLine Yield Solutions Fund is investing in floating-rate securities, it may explain some of the outperformance.

The fund’s description on its website says nothing about floating-rate securities. However, we do see that the fund has 15% of its assets invested in collateralized loan obligations and 9.6% of its assets invested in bank loans:

DoubleLine

These are generally floating-rate securities, and in fact, a look at the fund’s semiannual report does reveal that it has numerous securities in both categories that specifically state that the yield changes with some benchmark (such as LIBOR). However, that clearly does not account for all of the securities in the fund, and the fixed-rate securities that it holds will still decline in price as interest rates rise. Nevertheless, the floating rate securities in the portfolio do help to explain some of the outperformance of this fund against the fixed-rate bond index.

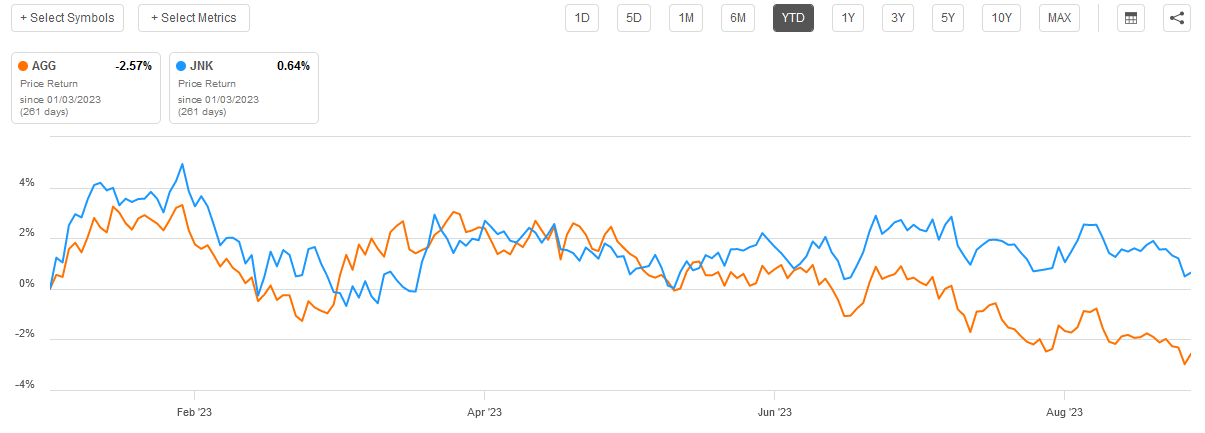

Another potential factor that could explain some of the performance differences is the fact that this fund invests in emerging markets, which tend to have lower credit ratings and higher interest rates than developed market bonds. For example, the semi-annual report makes mention of Ukrainian government bonds at 7.25% and 9.75%. That is not the current yield-to-maturity, these numbers are the coupon yield at face value. As I pointed out recently , investors have been increasingly willing to buy up junk bonds and other very high-yielding assets over the past few months. This is one reason why the Bloomberg High Yield Very Liquid Index ( JNK ) has been outperforming the aggregate bond index year-to-date:

{kind=link}

In fact, as we can see here, junk bonds are actually up year-to-date despite rising interest rates. The news media claims that this is because investors want to take advantage of the current high interest-rate environment and lock in attractive long-term yields for their money. That is as good a reason as any that I can think of. This same phenomenon might help explain the price performance of the DoubleLine Yield Opportunities Fund recently, as investors want to get the yield while it still exists.

However, there is one big problem that occurs with debt funds that does not occur with bonds. In the case of a bond, an investor can ensure that they do not lose money by holding the security until it matures. A bond will always return its face value at maturity unless the issuer defaults. A bond fund has open-ended maturity and will not necessarily always hold a bond until maturity. As such, investors trying to lock in high yields probably should not rely on a fund to do it. Thus, we may have a situation in which the fund’s shares do not reflect the fund’s actual performance.

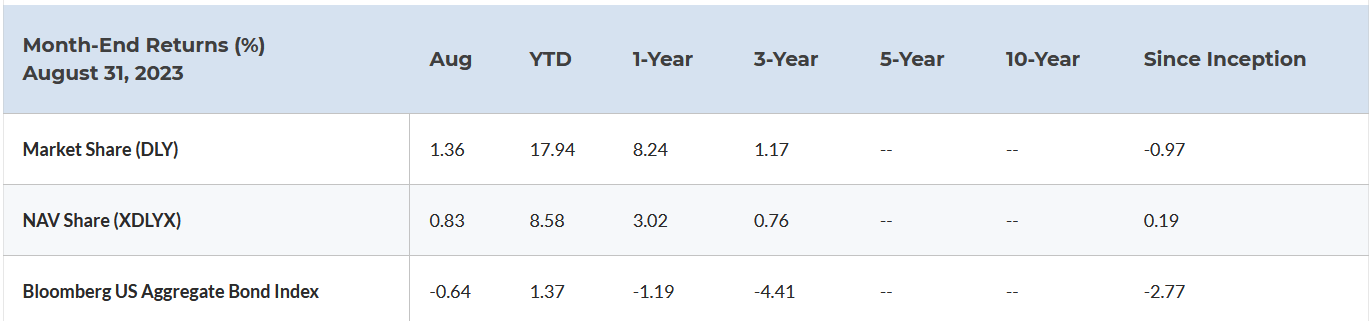

The webpage backs up this assertion. As we can see here, the DoubleLine Yield Opportunities Fund managed to generate an 8.58% total return year-to-date from its portfolio. However, the shares produced a 17.94% total return. The same thing happened over the trailing one-year period:

{kind=link}

Thus, we are seeing a case in which the fund’s performance drastically exceeds its actual market performance. As such, the fund may have become somewhat overvalued right now and that could represent a risk given the market’s optimism that the Federal Reserve will cut rates in the near future. We will discuss this in just a moment.

Leverage

As is the case with many closed-end funds, the DoubleLine Yield Opportunities Fund employs leverage as a method of boosting its total returns. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses that borrowed money to purchase bonds or other income-producing assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that leverage is much less effective at boosting the fund’s effective portfolio yield today with rates at 6% than it was two years ago when rates were at 0%.

Unfortunately, the use of debt in this fashion is a double-edged sword because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to too much risk. I generally like a fund’s leverage to be less than a third as a percentage of its assets for this reason.

As of the time of writing, the DoubleLine Yield Opportunities Fund has levered assets comprising 20.24% of the portfolio. This easily satisfies the one-third maximum limit and should represent a reasonably good balance between risk and reward. We should not need to worry too much about this fund’s use of leverage to finance its operations.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the DoubleLine Yield Opportunities Fund is to provide its investors with a high level of total return. The fund specifically states that it intends to provide the majority of its total return in the form of current income, which means that it wants the assets in the portfolio to pay it. The fund invests in a portfolio of bonds from around the world with this objective in mind and then applies a layer of leverage to boost the effective yield beyond that provided by any of the bonds in the portfolio. It then aims to pay out most to all of its investment profits, net of any expenses, to the shareholders via a regular distribution. As such, we might expect that the fund would boast a very high distribution yield itself.

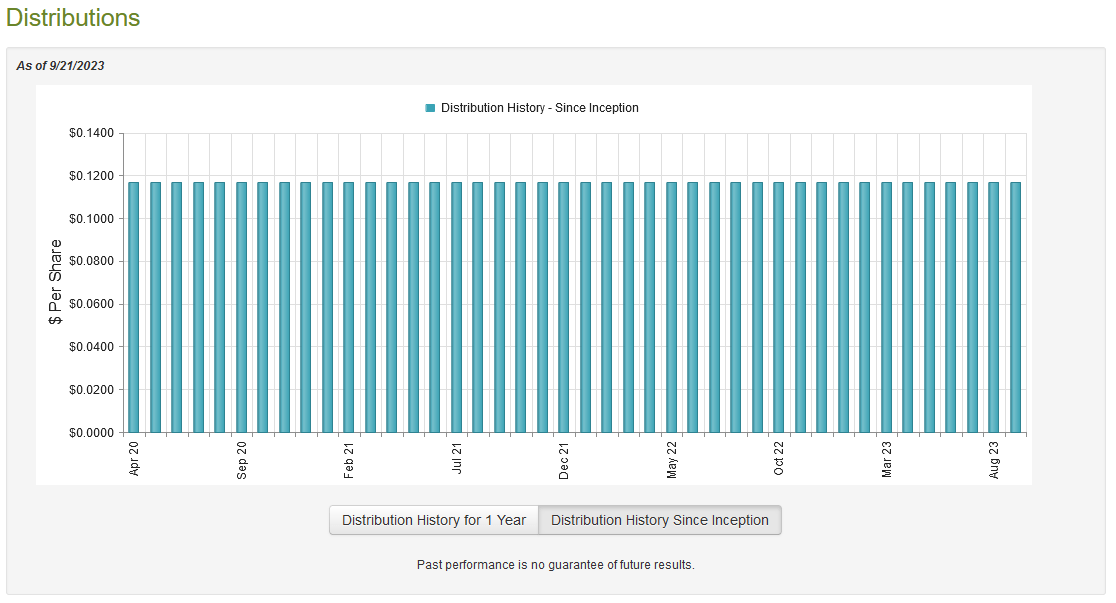

This is certainly the case, as the DoubleLine Yield Opportunities Fund currently pays a monthly distribution of $0.1167 per share ($1.4004 per share annually), which gives it a 9.53% yield at the current price. The fund has been remarkably consistent with its distribution over its lifetime:

{kind=link}

The consistency of this distribution may explain some of the appeal that we have seen with respect to this fund recently. After all, most debt funds have cut their distributions in response to the Federal Reserve’s monetary tightening policy so the fact that this one has not will undoubtedly appeal to those investors that are seeking a safe and secure source of income with which to pay their bills or finance their lifestyles. However, we do want to examine its finances since it seems odd that this fund could maintain a stable distribution when many of its peers could not.

Fortunately, we do have a fairly recent document that can be used for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report (linked earlier) corresponds to the six-month period that ended on March 31, 2023. As such, this report should give us a good idea of how well the fund managed the steep decline in bond prices that occurred in November and December of last year. Once the year turned though, the market got optimistic that rate cuts would soon be implemented and drove up bond prices. The fund may have been able to take advantage of this to sell some bonds at a profit. This will all be reflected in this report.

During the six-month period, the DoubleLine Yield Opportunities Fund received $41,561,081 in interest and $806,636 in dividends from the assets in its portfolio. This gives the fund a total investment income of $42,367,717 during the period. It paid its expenses out of this amount, which left it with $30,075,994 available to shareholders. Unfortunately, this was not enough to cover the $33,571,635 that the fund paid out in distributions. It did get reasonably close to covering the distribution though, which is encouraging.

The fund does have some other methods that can be employed to obtain the money that is needed to cover the distribution. For example, it might have been able to exploit changes in bond prices to generate some capital gains. Sadly, the fund failed at this task during the period. It reported net realized losses of $14,741,558 but these were partially offset by $11,510,376 net unrealized gains. Overall, the fund’s net assets declined by $6,726,823 after accounting for all inflows and outflows during the period. This is concerning as the fund’s net assets also declined during the full-year period that ended on September 30, 2022. Thus, the fund has failed to cover its distributions for eighteen months as of the most recent financial report. It is difficult to see how it can sustain its distribution should this continue. There could be some reason for concern here, and the fund’s investors should pay particular attention to its full-year report when it comes out in a few months. After all, we need to make sure that the fund does not have a full second year of failing to cover the distribution and declining net assets.

Valuation

As of September 21, 2023 (the most recent date for which data is currently available), the DoubleLine Yield Opportunities Fund has a net asset value of $15.21 per share but the shares currently trade for $14.82 each. This gives the fund’s shares a 2.56% discount on net asset value at the current price. This is substantially higher than the 5.66% discount that the shares have averaged over the past month.

I will admit that it is surprising to see this fund trading at a discount considering that the shares have been outperforming the portfolio performance for the past year. However, over the past 52 weeks, the fund’s shares have never been more expensive than a 1.17% discount on net asset value. The current price is a bit expensive based on the fund’s historical pricing, but it is still a discount.

Conclusion

In conclusion, the DoubleLine Yield Opportunities Fund has delivered a fairly strong performance in the market. However, its portfolio has not been performing nearly as well as the shares would suggest. So far, it has not resulted in the shares trading for a price that is above their intrinsic value though. There is definitely a risk here, especially if the market proves to be too optimistic about the Federal Reserve’s ability to engineer a “soft landing” for the economy, but that is a risk possessed by anything except for cash right now. My biggest concern is that this fund has been consistently failing to cover its distribution, which is unsustainable. While it is possible that it has managed to correct this problem in the time since the most recent financial report has come out, there is no guarantee of that so risk-averse investors may want to be cautious until we have more information.

For further details see:

DLY: Shares Delivering Misleading Information, Fund Is Overdistributing