DMB - DMB: 3% Total Return Over 5 Years But Prospects Improve From Here

2023-09-26 10:29:53 ET

Summary

- Our last article had a warning on BNY Mellon Municipal Bond Infrastructure Fund.

- Returns have been poor since then, and 5-year returns have been exceptionally bad.

- We tell you why things are likely to stay rough for a while but your prospects are improving.

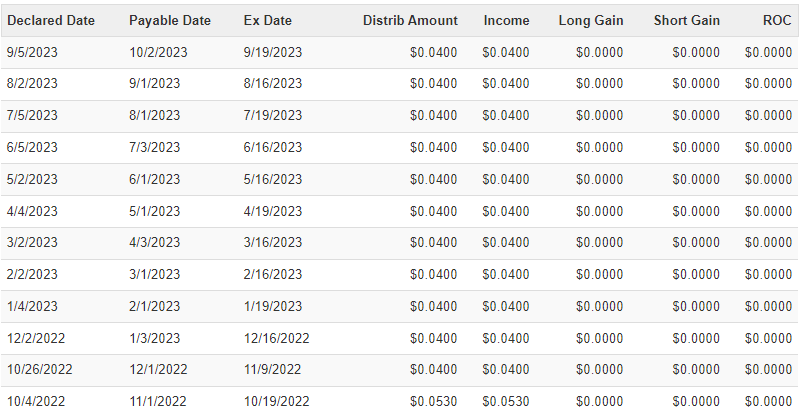

BNY Mellon Municipal Bond Infrastructure Fund ( DMB ) is a closed end fund that has a portfolio of municipal bonds. Municipal bonds are issued by state or local governments to finance their activities, be it operational or capital. In DMB's case, the portfolio mainly comprises bonds that are issued to finance infrastructure projects such as highways, bridges, etc. This fund decreased its monthly distribution from 5.3 cents to 4 cents back in November 2022 and has held it steady since then.

{kind=link}

Based on the current price of $10.00, it yields around 4.80%. Since municipal bonds are exempt from federal taxes and, depending on the residency of the unitholder, even from state taxes, investors cannot make an apples-to-apples comparison when deciding between a municipal and a taxable bond. The latter has to be considered in terms of its after-tax yield , resulting in a 4.80% yielding municipal bond portfolio generally coming out ahead in a head-to-head with a taxable bond portfolio of the same yield, provided one falls in a certain tax bracket. Generally, this tax bracket is more applicable to all those sage billionaires we keep hearing about on this platform.

{kind=link}

We covered this fund at the beginning of this year and gave it a neutral rating. While the price had descended from a year ago, and it was trading at a discount, we were not sold. 35% of the portfolio value was powered by borrowed funds at the time ($122 mil out of $346 mil) and the repercussions of this level of leverage were not fully reflected in the published data as yet. We predicted an increase in the annual expense ratio from 1.87% (February 2022) to over 3%, powered by the rising interest cost. That was our key reason for telling everyone to dial back their enthusiasm. The numbers that were released after that piece, for February 2023, showed that the fund was right on course to oblige.

CEF Connect

Note: DMB website still shows the February 2022 expense ratio of 1.68%. The literature section has the 2023 financial statements, which agree to the CEF Connect numbers shown above.

The semi-annual numbers for March-August 2023 are yet to be released, however, we can safely say that the interest expense will be higher still. We can conclude this based on the fund's debt structure. DMB's leverage is comprised of preferred securities and debt securities.

CEF Connect

The leverage is up slightly from the beginning of this year, when it was 35.26%. While there has been no change in the total amount of borrowings, the investment assets have declined from $346 million to $327 million. So that by itself would increase the expense ratio as the same borrowings and interest expenses are allocated over a small base.

The debt portion of the leverage structure comprises inverse floaters and is secured by its portfolio holdings. The weighted average annualized interest rate on the inverse floaters for the year ended February 28, 2023 was 2.19% (versus 0.70% in the prior fiscal year ), while that on the preferreds was 2.83% (versus 1.25% in the prior fiscal year ).

As we have seen above, the annualized expenses have been on a rise, and will do so even more in the next released report. More importantly, due to the delay with which generalized interest expenses flow through the financial statements, interest expenses will rise for the next semi-annual period as well. The distributions have taken some of the heat of the poor price performance of this fund since our neutral rating.

Returns Since Last Article

The discount that it trades to its NAV has also deepened from 7.14% to 9.59%.

Still, a far cry from the 20% discount that would perhaps warrant a buy rating from us. While the distributions of the fund enjoy a beneficial tax treatment, if the returns put the investors in a hole overall, the tax-exempt status is not really accretive. This type of fund still has a leg up over a regularly taxed fund, as those will have the investor in a deeper hole due to tax payments on the distributions.

Outlook & Verdict

That picture tells you most of the issues here. Total returns remain appalling.

The bulk of the pain comes from the average effective maturity of this fund at the end of last month was 18.95 years, in the same ballpark from earlier this year. The average effective duration on August 31 was around half that at 9.64 years, denoting the extent to which the market value of the portfolio would decline with every 100 basis points increase in the underlying interest rates. The relationship is inverse and works both ways. So far, the rise in interest rates has created a NAV stress that has been amplified by the leverage. We think a second round of the same will be seen in the next few months and the fund likely reduces positions (i.e., buys high and sells low) to maintain a constant leverage ratio. We may have even become buyers of DMB as it invests in an asset class that we can get behind at the moment, in limited amounts. But we are just saying "no" to leverage at this point. The overwhelming leverage will continue to harass its bottom line, and we anticipate another distribution cut within a year. That said, we think this is a slightly better entry point as the combination of the bond price drop and wider discount improve prospects for the next 5-year returns to be better than the last 5.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

DMB: 3% Total Return Over 5 Years, But Prospects Improve From Here