MUB - DMB: Very Disappointing Yield But A Decent Muni Bond Fund

2023-12-11 18:05:28 ET

Summary

- The BNY Mellon Municipal Bond Infrastructure Fund, Inc. offers a tax-free yield of 3.57%, which is not attractive compared to other fixed-income options.

- The DMB closed-end fund's performance has been disappointing, with a decline of 28.46% over the past three years.

- The DMB fund failed to cover its distributions during the most recent period, but it has cut the payout since that time.

- The fund is very highly diversified across states, especially when compared to other municipal bond funds.

- The DMB fund has a very attractive valuation, but it is uncertain if the distribution will prove sustainable at the new lower level.

The BNY Mellon Municipal Bond Infrastructure Fund, Inc. ( DMB ) is a closed-end fund, or CEF, that aims to provide its investors with a high level of current income that is free of federal income taxes. In many cases, investors in high tax brackets tend to like municipal bonds because they can provide competitive yields once the taxes are taken into account. Unfortunately, this fund is unattractive even when we consider the tax-free nature of its distributions.

As of the time of writing, the BNY Mellon Municipal Bond Infrastructure Fund yields 3.57%. That is the equivalent of a 5.67% yield for an investor in the 37% marginal income tax bracket. This is not especially attractive unless you compare it to money market funds or U.S. Treasury securities. Investors who are willing to take on a bit more risk would be happier with corporate bonds or even junk bonds, as a good junk bond fund is yielding about 11% right now. An investor in one of those funds would still wind up with more money even if you take the tax bite into account. As such, municipal securities may not have the appeal that they once did.

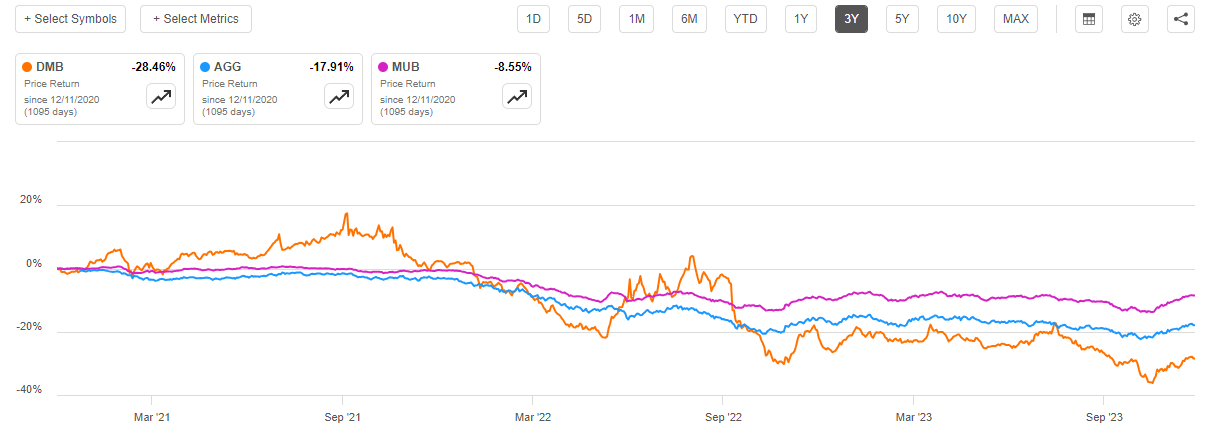

As has been the case with most bond funds over the past three years, the BNY Mellon Municipal Bond Infrastructure Fund's performance in the market has been rather disappointing. As we can see here, the fund's share price is down a whopping 28.46% over the past three years. This is considerably worse than the 17.91% decline of the iShares Core U.S. Aggregate Bond ETF ( AGG ) or the 8.55% decline of the iShares National Muni Bond ETF ( MUB ).

{kind=link}

This is quite concerning, to say the least. However, it is not unusual for closed-end funds to overshoot their benchmark indices to the downside during market selloffs. This is partly due to their use of leverage, as the leverage amplifies losses. In many cases, the closed-end fund is able to make up for this through a higher distribution yield. This fund certainly has a higher yield than the municipal bond index, so that is the case here.

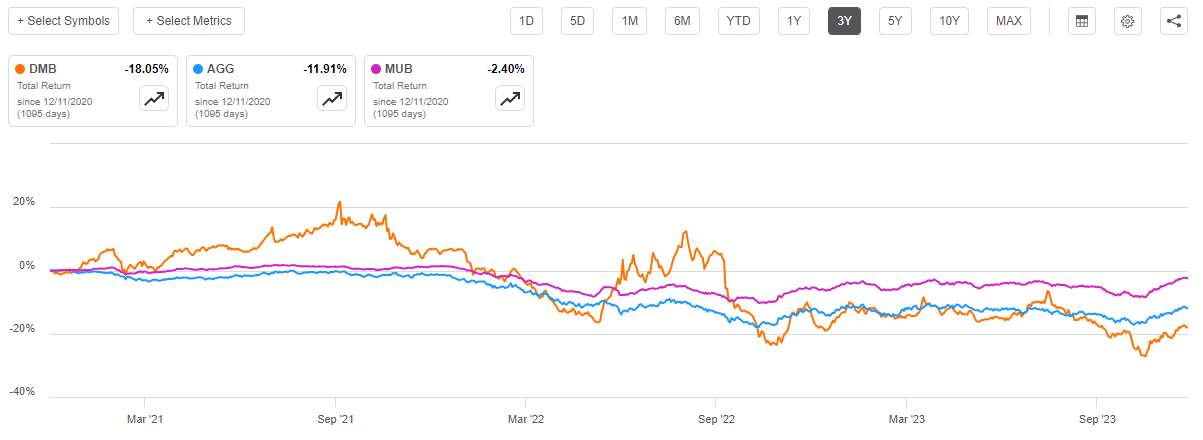

In the case of closed-end funds, and especially closed-end bond funds, total return is a much more appropriate measure to use to evaluate its performance than simply looking at the price. This is due to the fact that bonds deliver the overwhelming majority of their total returns in the form of direct payments to their investors. Unlike common stocks, these securities have no net capital gains over their lifetimes. As such, we want to incorporate the fund's distribution into the performance evaluation, as these distributions can sometimes be sufficient to offset price declines. When we do that, we see that the BNY Mellon Municipal Bond Infrastructure Fund still underperformed the indices, although its three-year performance does not look nearly as bad:

{kind=link}

As we can see here, investors in this fund lost 18.05% of their total investment over the past three years. This is hardly going to endear this fund to anyone, but it is important to keep in mind that every bond fund has been completely devastated over the period due to rising interest rates. Fortunately, it seems likely that the worst is behind us and the next few years will probably be better for bond funds, including this one, than the last three years have been.

About The Fund

According to the fund's website , the BNY Mellon Municipal Bond Infrastructure Fund has the primary objective of providing its investors with a monthly federal tax-exempt dividend. The fund's strategy to achieve this objective certainly works pretty well, as the fund invests in a portfolio of municipal securities that make payments to their owners that are generally free from federal income taxes. This tax-exempt nature is due to a provision in the tax code designed to make it easier for local and state governments to obtain financing at affordable rates.

The fund's website appears to be a bit outdated though, as it makes this statement:

{kind=link}

Yield is no longer scarce across bond securities, and it has not been for a year or so. As noted in the introduction, money market funds and short-term U.S. Treasury securities have similar tax-equivalent yields to this fund, and they do not even need to rely on leverage to achieve such yields. Corporate securities and especially junk bond funds deliver much higher yields. The fund's statement about yields being scarce may have been correct in late 2020 or early 2021 but it is no longer the case.

Investors who are not in the highest tax bracket will almost certainly be able to find better yields elsewhere. Of course, that is pretty much always the case regardless of the market environment.

With that said, the fact that this fund does invest in local governments as opposed to the Federal government might have a certain appeal. According to a recent Gallup Survey , Americans in general tend to hold far better opinions of their own local governments than they do of the Federal government. This also extends to other local governments, especially ones governing areas similar to their own hometowns. As such, there may be a certain charitable appeal to investing in local governments with a portion of your assets, even though it may not necessarily be the most profitable option available to you. Ultimately, bond prices are more of a function of supply and demand than they are of the Federal Reserve's monetary policy, so this general favoritism that people hold towards state and local governments could cause these bonds to deliver somewhat better performance than comparable U.S. Treasury securities.

The BNY Mellon Municipal Bond Infrastructure Fund has a portfolio that is fairly well-diversified across the various states. As we can see here, there is no single state that occupies an outsized proportion of the fund:

CEF Connect

This is a bit different than some other municipal bond funds. For example, the iShares National Muni Bond ETF has 21.28% of its assets invested in New York State and its local governments. The same exchange-traded fund has 19.38% of its assets invested in California and local governments in the state of California. That is an enormous percentage of the fund's assets tied up in two states. This fund is obviously much more diverse as there is no state that accounts for more than 10% of the fund's assets.

This is probably a very good thing considering that certain states (such as Illinois) have much weaker financial positions than other states (such as South Dakota). As such, the risks of having a substantial percentage of assets tied up in only one or two states could be fairly high. Naturally, though, no state has ever defaulted on its debt obligations. There are some municipalities that have defaulted in the past, however. As this fund is investing mostly in the debt of local governments and agencies, not exclusively state governments, default risk is still possible so maximizing diversity is a pretty good thing.

The fund's diversity extends beyond simply not having outsized positions in the entities found within any individual state. There is, in fact, no asset that accounts for an outsized position in this fund. We can see this by looking at the largest positions in the fund and their weightings:

BNY Mellon

As we can see, there is no single position that accounts for more than 5% of the portfolio. In fact, there is no individual position that accounts for more than 2.5% of the portfolio. However, both of the two largest positions - Buckeye Tobacco Settlement Bonds and Muskingum County Ohio Hospital Facilities Revenue Bonds - are from the state of Ohio.

The Buckeye Tobacco Settlement bonds are interesting bonds that securitize the payments that Ohio receives from the Master Settlement Agreement that was reached in 1998 between the attorney generals of 52 states and territories and the four largest tobacco companies in the United States. The Ohio Office of Management and Budget describes how these bonds work on its webpage:

The 2020 deal refinanced bonds originally issued in 2007 that securitized the State of Ohio's annual payments received under the 1998 Tobacco Master Settlement Agreement with tobacco companies. The tobacco settlement bonds are special revenue obligations and are not at Ohio taxpayer or General Revenue Fund expense.

…

The General Assembly created the Authority in 2007 for the sole purpose of exchanging Ohio's annual revenue stream of tobacco settlement proceeds for a one-time upfront payment that financed the cost of improving facilities of Ohio's K-12 schools and universities statewide. In turn, those annual payments are pledged to repay bondholders, and once repaid, the annual proceeds from the settlement will return to the State of Ohio.

In short, Ohio sold these bonds because the state wanted a large amount of money upfront to use to fund schools and universities. It is using the money that it receives from the tobacco settlement to pay off the bonds. Obviously, in this case, the fund is receiving the money from these bonds and using it to pay distributions to its shareholders.

The Muskingum County Ohio Hospital Facilities Revenue Bonds are pretty much exactly what they sound like. These are simply bonds that are backed by the revenue generated by a hospital that was constructed with the proceeds of the bond issue. Hospitals tend to be pretty reliable revenue generators, so we probably do not need to worry about these too much.

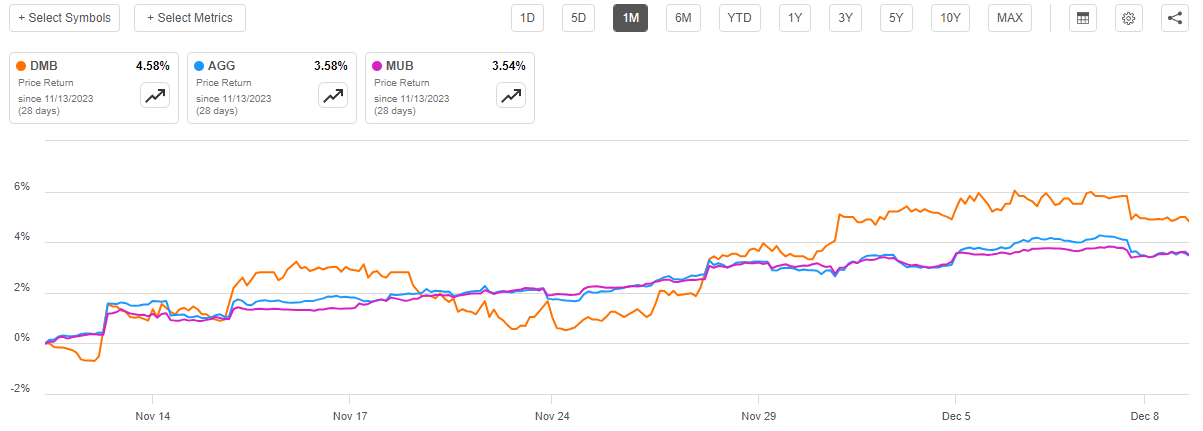

Overall, the biggest risk here is probably interest rates. The BNY Mellon Municipal Bond Infrastructure Fund has a 15.25-year effective duration, which implies that the fund's share price will exhibit a great deal of volatility with respect to changes in interest rates. That is, in fact, what we generally see in this fund. As we saw in the introduction, the shares of this fund declined to a much greater degree than either the Bloomberg U.S. Aggregate Bond Index or the national municipal bond index. However, over the past month, this fund's shares have gone up by more than either index:

{kind=link}

Thus, we can expect that this fund's price movements will probably be pretty similar to that of the broad bond market indices, but to a greater extent. Thus, it will decline more than the indices during periods of rising interest rates but should outperform the indices during periods of falling interest rates.

Right now, the market is expecting about 125 basis points of interest rate cuts over the next twelve months. As I have pointed out in recent articles, I doubt that we will see a federal funds rate of 4% to 4.25% next December. There have been several other articles published by other analysts suggesting the exact same thing. As such, there might be some short-term pain for anyone buying this fund at today's levels once the market realizes that it is wrong.

Leverage

As is the case with most closed-end funds, the BNY Mellon Municipal Bond Infrastructure Fund employs leverage as a method of boosting the effective yield that it generates from the assets in its portfolio. I explained how this works in a variety of previous articles. To paraphrase myself:

In short, this fund borrows money and then uses that borrowed money to purchase municipal bonds that are generally free from federal income taxes. As long as the yield that the fund receives from the purchased assets is greater than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this strategy will usually work to boost the fund's effective yield but admittedly that might not always be the case considering the incredibly low yields of most municipal bonds.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to an excessive amount of risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for that reason.

As of the time of writing, the BNY Mellon Municipal Bond Infrastructure Fund has leveraged assets comprising 34.91% of its portfolio. Obviously, this is a bit higher than the one-third ratio that I would prefer to see with a fund such as this. However, when we consider that the fund is invested in municipal bonds, the leverage is probably okay. As I have pointed out numerous times, fixed-income securities in general tend to be less volatile than common equities. It is ultimately volatility that causes problems with a leveraged portfolio, so a fixed-income fund can usually carry a bit more leverage than an equity closed-end fund can. Municipal bonds also have an incredibly low rate of default, so we probably do not really need to worry much about defaults wiping out the fund's assets.

Overall, this fund's leverage is probably okay right now. The big risk here is that the leverage is an added factor that will amplify the fund's upward or downward movements relative to the bond indices. We have already discussed this.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the BNY Mellon Municipal Bond Infrastructure Fund is to provide its investors with a regular source of income that is generally free of federal income taxes. In order to accomplish this objective, the fund invests in a diversified portfolio of municipal bonds that deliver the majority of their total returns in the form of direct payments to the investors. Unfortunately, as these are government bonds and enjoy tax-free status, the yield will not be as high as other types of bonds. In fact, municipal bonds generally have lower coupon yields than U.S. Treasuries.

The fund does use leverage to control additional securities, but its own expenses partially offset some of the payments from these. The fund collects all of the payments that it receives from all of the bonds that it controls and then distributes them to the shareholders, net of its own expenses. Unfortunately, the incredibly low yield on municipal bonds leads us to conclude that this probably will not result in an especially attractive current yield.

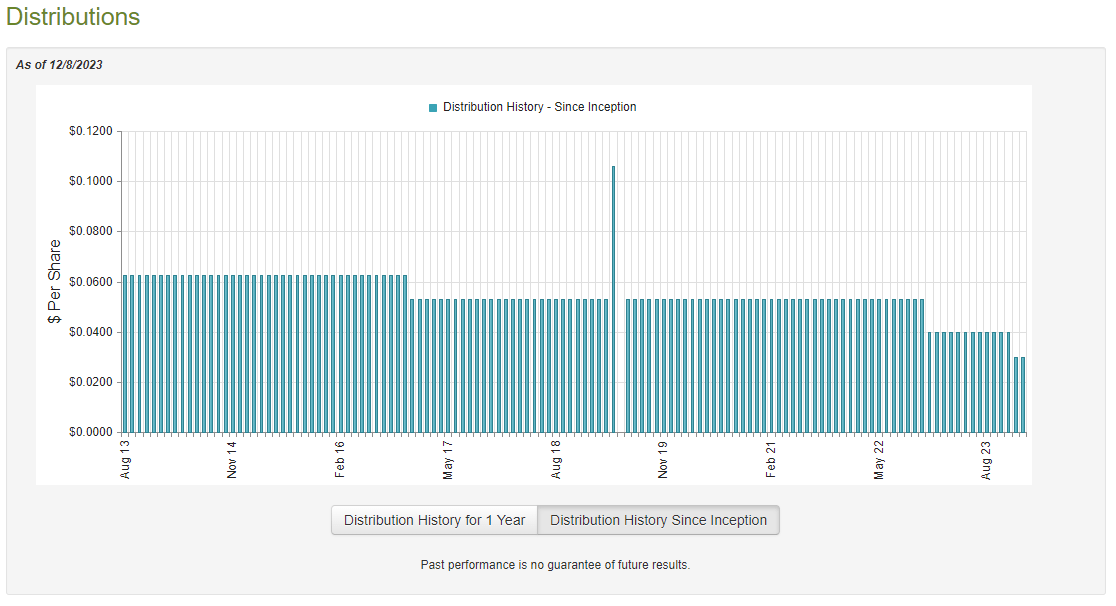

This is certainly the case, as the BNY Mellon Municipal Bond Infrastructure Fund currently pays a monthly distribution of $0.03 per share ($0.36 per share annually), which gives it a 3.57% yield at the current share price. That is the equivalent of a 5.67% yield for someone in the 37% marginal tax bracket, but even that is not particularly impressive compared to other options that are available in the fixed-income market today. The fund has also not been particularly consistent with its distribution, as it has been steadily declining since the fund's inception in 2013:

{kind=link}

That distribution history seems likely to be a bit of a turn-off to anyone who is seeking a safe and consistent source of income that can be used to pay their bills or finance their lifestyles. However, it is not really surprising that a bond fund would have to cut its distributions as rising interest rates have caused a lot of these funds to take fairly large losses as bonds have been declining in price for the past three years. This bond fund is hardly alone in having to reduce its payout over time.

However, as I have pointed out numerous times in the past, the fund's history is not exactly the most important thing for anyone who is considering purchasing the fund today. This is because today's investor will receive the current distribution at the current yield and will not be affected by actions that the fund has taken in the past. The most important thing for anyone purchasing the fund today is its ability to sustain the distribution at the current level. Let us investigate this.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on August 31, 2023. This is one of the newest reports that we have available from any closed-end fund. The period that it covers is certainly an interesting one for a bond fund as well. After all, the first half of this year was characterized by falling interest rates as investors bid up long-term bonds in the expectation that the Federal Reserve would pivot and cut interest rates during the second half of 2023. Obviously, the market was wrong, but the bonds in this fund's portfolio probably still appreciated in value. The final two months of this period saw the opposite happening, as bonds started falling in price once the market realized that it was wrong about the near-term policy of the nation's central bank. This report will give us a good idea of how well the fund handled both of these opportunities.

During the six-month period, the BNY Mellon Municipal Bond Infrastructure Fund received $7,648,945 in interest from the assets in its portfolio. It had no income from any other source, so that amount comprised the entirety of its investment income. The fund paid its expenses out of this amount, which left it with $3,841,393 available for shareholders. That was, unfortunately, not enough to cover the $4,417,433 that the fund paid out in distributions over the same period. At first glance, this is almost certainly going to be concerning since we would generally prefer a fixed-income fund to be able to completely cover its distributions out of net investment income.

However, there are other methods through which a fund can obtain the money that it needs to cover its distributions. For example, it might be able to sell appreciated securities for capital gains in a friendly market. Realized capital gains are not considered to be investment income for tax purposes but they obviously represent money coming into a fund. Of course, the distribution of such money may disrupt the fund's ability to claim that its distributions are income tax-free. This is a moot point anyway because the fund failed to generate any net capital gains. During the six-month period, it reported net realized losses of $1,716,415 and had another $1,223,991 net unrealized losses.

Overall, the fund's net assets declined by $3,516,446 after accounting for all inflows and outflows during the period. This is quite concerning, as it strongly suggests that the fund cannot afford to cover its distributions and indeed it failed to do so during the period. The same thing occurred during the full-year period that ended on February 28, 2023. As such, the fund has failed to cover its distribution for eighteen straight months.

The fund cut its distribution beginning in December 2023. As such, the entire period covered by this report was under the previous distribution regime. It remains to be seen if the fund will succeed in covering its distribution at today's lower level. It might be able to get pretty close, considering that the fund's net investment income was pretty close to its distribution in both the most recent reporting period and the previous full-year period. This is still something that we should keep an eye on, though.

Valuation

As of December 8, 2023 (the most recent date for which data is currently available), the BNY Mellon Municipal Bond Infrastructure Fund has a net asset value of $11.79 per share but the shares only trade for $10.04 each. This gives the fund's shares a 14.84% discount on net asset value at the current price. This is a very attractive entry price that is in line with the 14.35% discount that the fund's shares have averaged over the past month. As such, today's price certainly appears to be reasonable for anyone who wishes to add this fund to their portfolio today.

Conclusion

In conclusion, the BNY Mellon Municipal Bond Infrastructure Fund, Inc. is a reasonable fund as far as municipal bonds are concerned. The fund does manage to beat some other options in terms of tax-equivalent yield, but it can hardly compare with corporates right now. The fact that these bonds are a bit safer as far as default risk goes helps, but most bond funds of any type are reasonably well diversified against default risk. The recent distribution cut is also unlikely to help this fund in the eyes of anyone who is seeking income.

Honestly, I cannot see a reason why anyone who wants a high level of income would choose this fund over a taxable junk bond fund, but as far as municipal securities are concerned, this is a good fund right now.

For further details see:

DMB: Very Disappointing Yield, But A Decent Muni Bond Fund