FMY - DMO: Deeper Discount But Risks Also Increase

2023-03-27 06:06:08 ET

Summary

- DMO is invested in mortgages, both residential and commercial MBS, as well as other mortgage-related debt securities.

- With all the uncertainty, a wider discount could be appropriate as credit risks become a real issue.

- At the same time, we are now trading near all-time-wide discounts for this fund that had historically traded at premiums.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 25th, 2023.

Western Asset Mortgage Opportunity Fund (DMO) had been a long-term winner relative to its peers. However, as I noted in our previous coverage of DMO, the fund's performance hasn't been nearly as strong outside of the 10-year time frame. While still competitive in the middle of the pack on a total NAV return basis, it's been primarily its widening discount pushing down its total share price results.

The fund is now trading at near an all-time wide discount level (excluding the COVID spike). At the same time, this fund had a rather long history of trading at a premium. So the latest discount near these levels could entice some investors.

That being said, perhaps it's for an appropriate reason. As the fund's name would suggest, it is invested in mortgage-backed securities. That includes commercial and residential mortgages and other mortgage-related debt and asset-backed securities. While there are assets backing these forms of debt, during a potential recession, there are still likely to be significant losses experienced. Therefore, patience or a dollar-cost average approach could be more appropriate, and I feel that a "hold" rating is still appropriate.

Since our last update, the fund has started to make some positive moves upward before turning lower once again. Below is the performance relative to the S&P 500. That index isn't an appropriate benchmark, but it can help provide some context.

DMO Performance Since Prior Update (Seeking Alpha)

The distribution rate on this fund is quite attractive, but another note of caution is that coverage is lacking despite floating rate exposure and a cut in the distribution.

The Basics

- 1-Year Z-score: -1.28

- Discount: -15.09%

- Distribution Yield: 11.59%

- Expense Ratio: 1.77%

- Leverage: 39.53%

- Managed Assets: $232.51 million

- Structure: Perpetual

DMO's investment objective is "current income, with a secondary investment objective of capital appreciation." To achieve this, they "provide a leveraged portfolio, consisting primarily of non-agency residential mortgage-backed securities ((RMBS)), commercial mortgage-backed securities ((CMBS)) and mortgage whole loans."

The fund utilizes an elevated amount of leverage, meaning that while times are good, the fund can benefit by producing outsized gains. On the other hand, losses can be amplified through any sort of downturn. Additionally, the leverage cost through reverse repurchase agreements will increase with rising interest rates. The cost of this leverage came in between 5.94% and 6.472% at the end of 2022 .

DMO Reverse Repurchase Agreements (Western Asset)

The fund's effective duration comes to 4.26 years, so we have interest rate sensitivity here on the fund's underlying portfolio too. A sizeable portion of the underlying debt securities is floating rate, which can benefit from rising interest rates.

However, the other benefit to the fund against higher interest rates was the fund shorting U.S. Treasury Notes and utilizing interest rate swaps in the fund in the last year.

During the reporting period, we utilized Treasury futures and options and interest rate swaps to manage the Fund's duration and yield curve exposure. CMBS index swaps ("CDS") were used for credit hedging purposes. Overall, the use of these derivatives contributed to performance. Finally, we actively utilized leverage in the Fund. When the reporting period began, the Fund's leverage as a percentage of gross assets was roughly 32%. At the end of the period, approximately 38% of the Fund's gross assets were levered. Overall, leverage detracted from results given the negative total return of the assets of the Fund in 2022.

With a large amount of leverage in the fund, it takes the fund up to a more reasonable size. However, it would otherwise be a fairly small fund. That can make it more difficult for larger investors to move in and out of the fund if there is a lack of volume for trading. The expense ratio comes up to 3.80% when including the fund's leverage expense.

Performance - Attractive Discount, But Uncertain Time

Besides, during COVID, we are near an all-time wide discount for this fund. The last time we were at these levels was earlier in 2022.

Ycharts

Given the risks in the market at this time, this appears to be what one could expect. For a longer-term investor, it could still be presenting an opportunity. As we've highlighted previously, this fund's performance was one of the better ones against its peers historically. In more recent years, the results have been more middle of the pack for a total NAV return basis.

However, since the fund has gone to a significant discount from being at a premium, the fund's performance actually looks weaker on a total share price return basis despite the fund's underlying portfolio performing much better. This is a good reminder of why buying CEFs at a large discount can be a dangerous gamble.

DMO Annualized Results (CEFData)

{kind=link}

Of course, CEFs can get rather niche and finding 'peers' can be quite difficult. I've highlighted this before with DMO specifically, but it's worth touching on again.

These results should also be considered that some of the peers listed by CEFData - despite their best efforts - probably aren't the most appropriate peers. One of the funds that jump out at me immediately here is that the RiverNorth/DoubleLine Strategic Opportunity Fund ( OPP ) fund is considered a peer.

{kind=link}

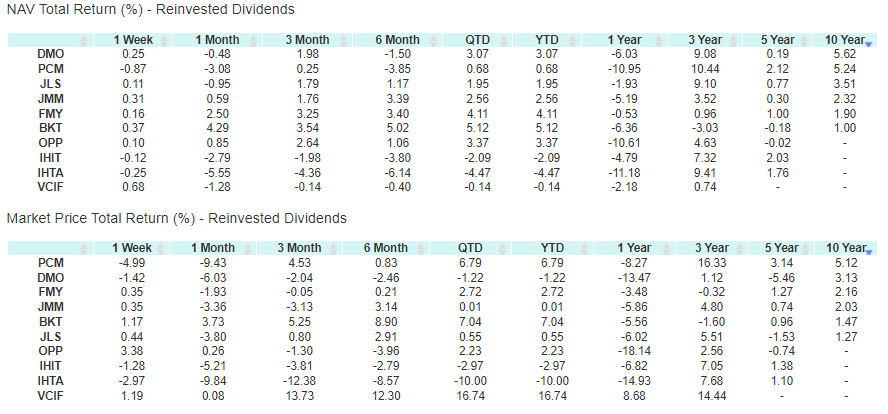

In my opinion, OPP shouldn't be listed here despite some exposure to MBS. The two names that come out as closer peers would be PCM Fund ( PCM ), Nuveen Mortgage and Income Fund ( JLS ) and First Trust Mortgage Income Fund ( FMY ). Against those funds, DMO is one of the cheapest alongside JLS. At one point, DMO competed against PCM in terms of wild premiums.

Ycharts

Over the last 10 years, the fund's total NAV returns have been nearly identical between DMO and PCM.

Ycharts

In fact, in the last year, DMO has outperformed PCM significantly in terms of the underlying portfolio as measured by the total NAV return. Worth noting is that JLS and FMY have held up significantly better more recently but were significantly underperforming over the longer term.

Ycharts

Given this, an investor in PCM in the following years could be in the position that DMO investors find themselves in now. Due to the valuation of PCM being at such a high premium, the losses could be amplified if it does go back closer to NAV or to a discount. That being said, PCM is an older fund, and it has exhibited a premium throughout the majority of its life.

Distribution - Lack of Coverage

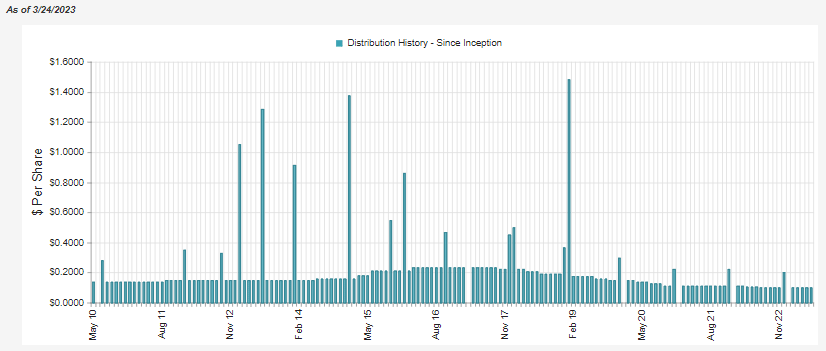

A fund carrying an 11.59% distribution rate can be quite attractive. Unfortunately, this one doesn't appear to be covered. They've been cutting the distribution; the last cut was in mid-2022.

DMO Distribution History (CEFConnect)

{kind=link}

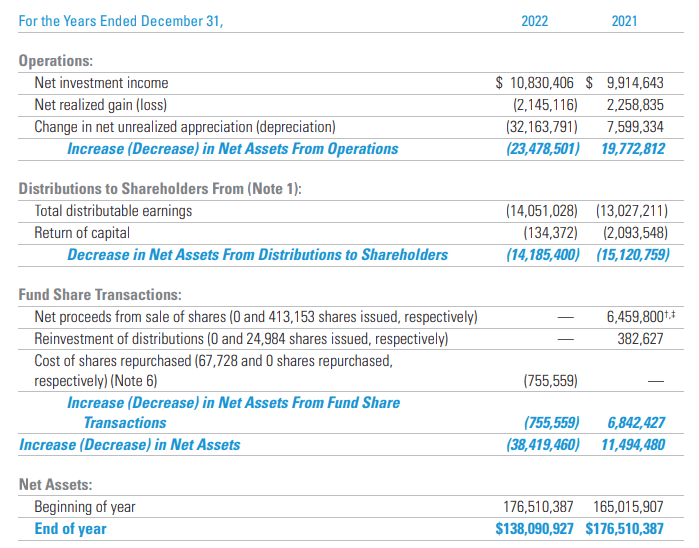

Despite that cut, the distribution still isn't looking like it can be covered through net investment income. In 2022, the NII coverage came to 76.35%, up from 65.57% in the year prior. The distribution for the next twelve months based on the last number of known outstanding shares, and the $1.20 would mean they are paying out $13,677,028 annually.

NII should continue to trend higher as the Fed continued to increase interest rates after this period. This is also reflecting a period where half-the-year rates were significantly lower as the Fed ramped up aggressively through the end of 2022.

The second half of the year saw an increase of around 4% in NII over the previous semi-annual report and a 9.24% increase in NII year-over-year. Given that trajectory, it would still suggest a lack of coverage going forward. That being said, the fund announced the same distribution until May , so they seem to be comfortable with the current payout.

DMO Annual Report (Western Asset)

{kind=link}

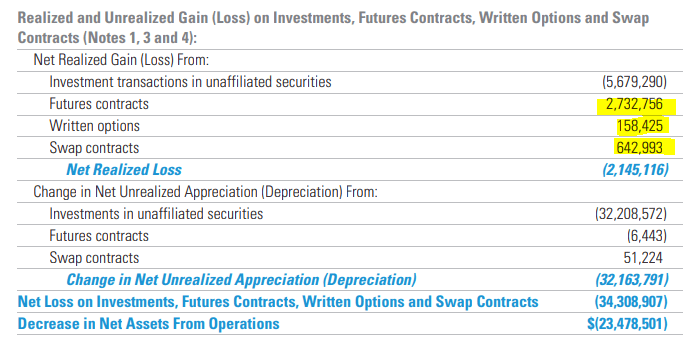

With realized losses, it also isn't being covered with capital gains either. That being said, they did make a good attempt through their derivatives to counteract some of the losses realized from their portfolio. Futures contracts, written options and swap contracts all contributed positively to the realized gains bucket.

DMO Unrealized/Realized Gains/Losses (Western Asset)

{kind=link}

DMO's Portfolio

A breakdown of the sector allocations of debt gives us an idea of what we are gaining exposure to in this fund. The largest exposures here come through residential, but commercial exposure is a significant part of the pie as well. They don't carry a significant portion of any agency debt, which would be considered much safer.

DMO Sector Allocation (Western Asset)

While it would appear the market is uncertain of the future of this type of portfolio, managers are otherwise more optimistic. That isn't going to be that unusual; a manager in a fund they are managing will paint a rosier picture . They feel that the market is too pessimistic and that they should be benefiting from inflation.

The combination of strong fundamentals with attractive income and valuations suggests significant potential for the asset class to generate strong performance over the long-term. The largest dislocated opportunities are in residential and commercial mortgage credit where spreads are implying a significant deterioration in collateral performance that we believe is overly pessimistic. The team believes mortgage credit offers value backed by real assets that benefit from a rising inflation environment and can generate attractive risk-adjusted returns, and that the strong total return potential and diversification benefits will provide value to investors.

They carry a diverse pool of assets to help mitigate some of the risks in the portfolio. They list 326 total holdings at the end of February 2023. That being said, most of their positions are some form of pooled debt security, meaning that there are hundreds or thousands of loans within those.

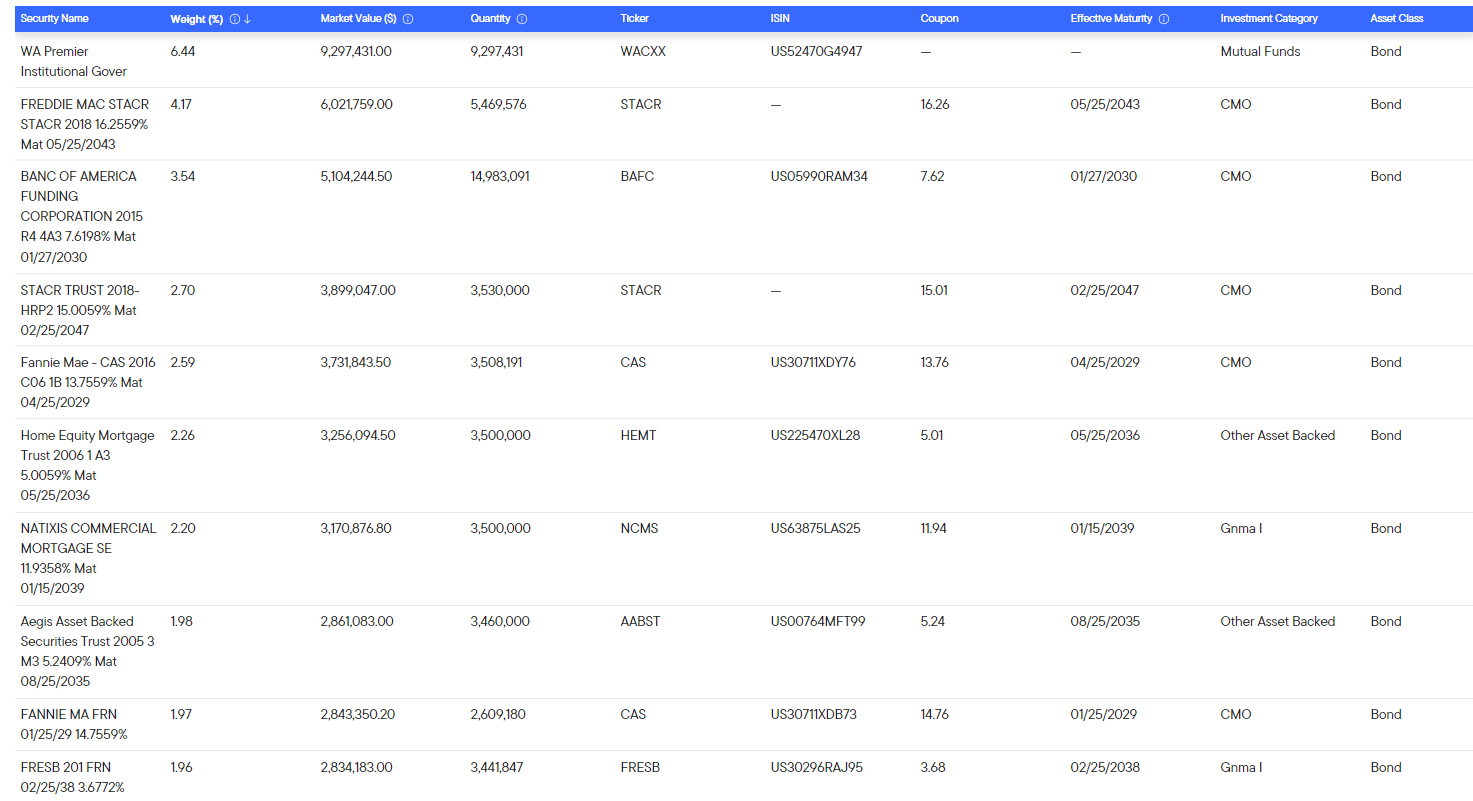

When looking at the fund's top holdings, we can start to get an idea of the types of coupons and more details on the holdings in the fund. At this time, a money market fund carries the largest exposure to the fund.

DMO Top Holdings (Western Asset)

{kind=link}

This is where it could get a bit confusing because we see STACR and CAS securities listed. These are issued by Fannie Mae and Freddie Mac. However, they aren't backed by the agencies. Instead, it's more like the other way around; the holders of these securities transfer risk from Fannie and Freddie to those other investors instead. It's these types of securities that absorb credit losses when they happen. In this case, it means DMO would potentially be the one experiencing the losses during defaults, and it would be an investor in the DMO fund that would experience those losses through NAV losses.

Conclusion

With so much market uncertainty, it would appear we are getting the chance to scoop up shares of DMO at a significant discount. However, this discount has appeared due to the risks that are out there when the recession hits. So it would seem that this fund, especially given its elevated level of leverage, should be considered more appropriate for an investor with a higher risk tolerance. That being said, if management is right in their more optimistic view, a contraction in the discount could follow and propel the returns higher as a higher discount or even a potential premium returns to the fund.

For further details see:

DMO: Deeper Discount, But Risks Also Increase