DMO - DMO: Recent Hike Pushes The Yield On This Mortgage CEF Above 11.5%

2023-08-03 04:08:48 ET

Summary

- We last discussed DMO about a year ago, highlighting the strong potential for a dividend hike due to a rising net income trajectory.

- As expected, the fund has indeed hiked the distribution which, along with its wide discount, translates to a 11.55% current yield as of this writing.

- The fund's primarily residential mortgage allocation provides an attractive diversifier in income portfolios and is anchored off strong household credit metrics.

- We continue to hold the fund in our High Income Portfolio.

In this article we provide an update on the Western Asset Mortgage Opportunity Fund ( DMO ). In our last update about a year ago we suggested the fund was very likely to hike its distribution as it benefits from higher rates.

Although distribution hikes are a dime a dozen in Loan CEFs, they are quite rare outside of that sector. In fact, DMO is one of the very few Multi-sector CEFs that have hiked over the last year (other ones like WDI and JLS are also ones that we have highlighted as beneficiaries of the current environment).

DMO trades at a 11.55% current yield and 10% discount. We continue to hold the fund in our High Income Portfolio.

Fund Snapshot

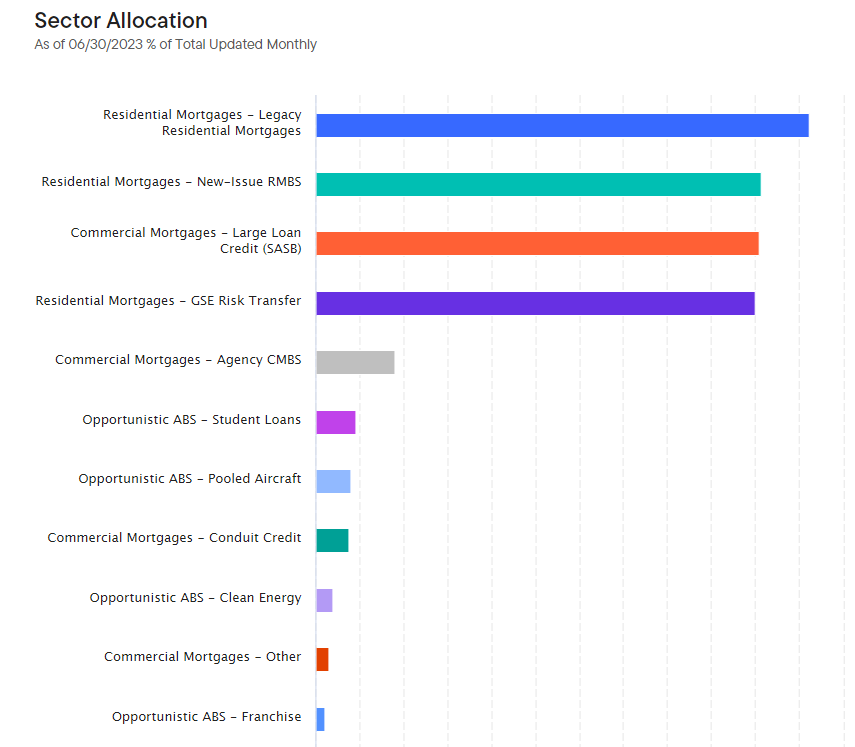

The allocation profile of the fund is fairly unusual in that it primarily holds mortgage securities with a greater focus on residential mortgages. These securities are not the more common Agency MBS which carry no credit risk. Rather, they are either legacy non-agency securities (i.e. those issued prior to the GFC) or CRT securities (issued by US housing agencies after the GFC to offload borrower credit risk). This allocation profile makes DMO fairly unique in the CEF space.

{kind=link}

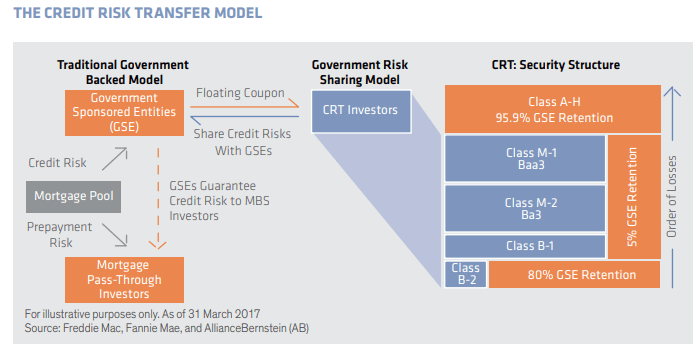

By way of background on the fund's portfolio, after the GFC, the US government looked for a way to derisk the business profile of its housing agencies and settled on the so-called CRT securities as a way to partially offload the household credit risk to the broader market. The schematic below shows how CRT securities work. The basic idea is that losses from mortgage defaults flow from the bottom-up with lower / higher-yielding tranches in the CRT structure absorbing losses first while the agency retains some skin in the game across the entire structure.

{kind=link}

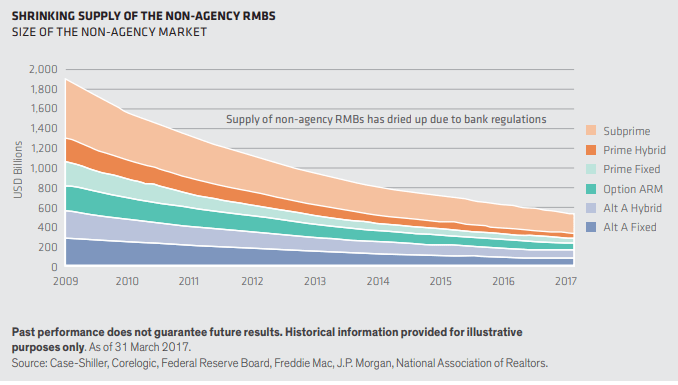

The legacy non-agency RMBS set of securities, on the other hand, are those that were mostly issued prior to the GFC. This market continues to shrink as it has been largely replaced by CRTs.

{kind=link}

DMO holds both types of securities with the primary focus being residential mortgages, though there is some commercial exposure as well.

Households Are Doing Well

The bulk of risk in the DMO portfolio is linked to households. This aspect of the fund is an attractive one for two main reasons. First, most of the income market is linked to corporate credit risk so having another kind of risk in the portfolio allows investors to diversify their ultimate sources of returns.

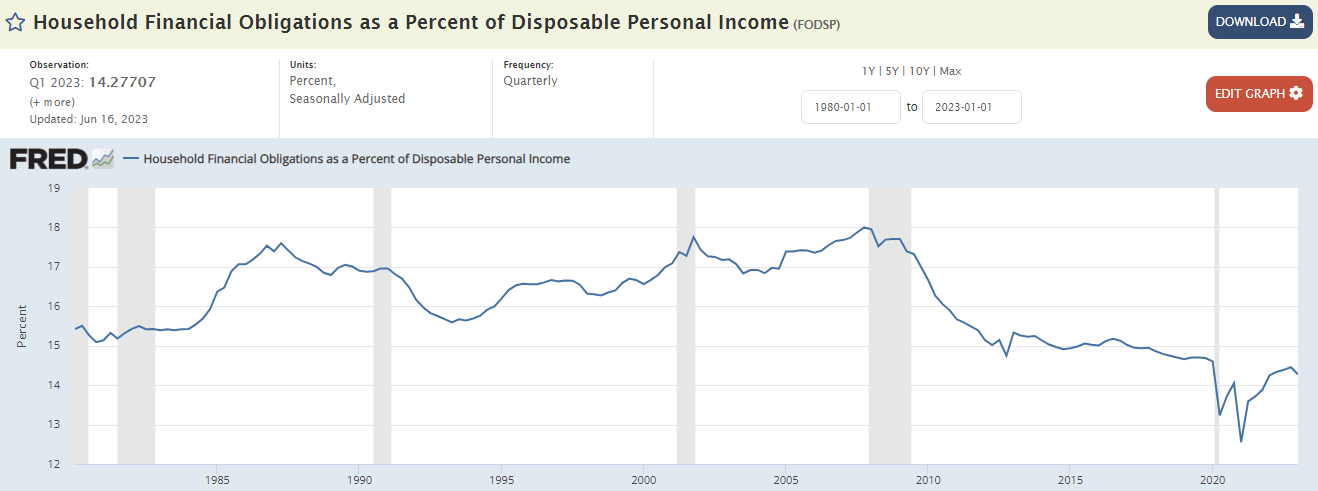

And two, households are in fairly decent economic shape so far, even if some leading indicators such as consumer confidence and retail sales have turned lower. For instance, household financial obligations as a percentage of disposable income is not far off a historically low level.

{kind=link}

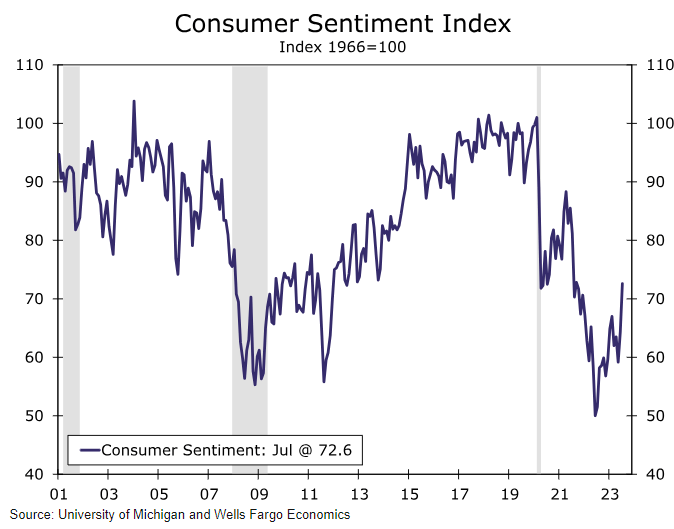

Consumer sentiment has increased sharply over the last few months, arguably, off a low base. An improving economic backdrop, a tight labor market and moderating inflation are supporting households.

{kind=link}

The labor market remains a key support of household financial health. Although job openings have moderated, they remain well above the pre-COVID trend.

BLS

The number of unemployed people per job is near a rock bottom level.

BLS

This has allowed real disposable income to continue to grow at a strong pace.

Wells Fargo

That said, we have to be mindful of some clouds on the horizon. Excess savings accumulated during the COVID shock continue to slide and will likely be exhausted over the coming months. This is at the same time that the Fed continues to push rates higher in order to cool off the economy. A key question is whether it will be happy with the recent disinflation trajectory and pause rates in short order.

Income Review

Unlike the vast majority of non-Loan CEFs, DMO net income profile has held up very well and is close to its peak as the following chart shows.

Systematic Income

This is largely a function of a significant amount of floating-rate holdings - at around 80%, net of inverse floaters. The Q1 net income figure is understating the fund's current net income which has increased further as short-term rates have risen around 0.8% from the levels that fed into Q1 income.

Separately, while many other fixed-income CEFs (and all PIMCO CEFs, for instance) deleveraged sharply, DMO has been able to add borrowings. This is largely a function of its relatively low NAV beta as well as a relatively low starting leverage. This borrowing resilience has allowed the fund to continue to generate additional income for shareholders.

Systematic Income CEF Tool

Although the fund's net income has been on an upward trajectory for some time, it only chose to hike recently. Part of this is due to its relatively low coverage though, as suggested above, coverage is still understated given net income has continued to increase from the most recently published figure.

Stance and Takeaways

Since the recent downshift in markets in early 2022, DMO has outperformed most other CEFs that have significant residential mortgage holdings as well as the broader Multi-Sector CEF space in total NAV terms.

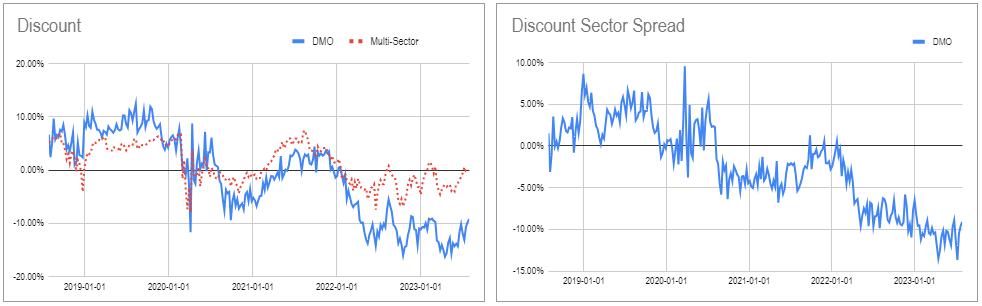

Its valuation remains very attractive. For instance, while the rest of the Multi-Sector CEF sector trades at a flat discount on average, the discount on DMO remains near a double-digit level.

{kind=link}

We have made several rotations involving DMO over the last couple of years. We added to our position in early 2021, then downsized in early 2022 as valuations got a bit too frothy. We then added a couple of times at the end of 2022 and more recently once the fund's price fell with the rest of the income space.

{kind=link}

At this point we continue to find DMO attractive and hold it in our High Income Portfolio.

For further details see:

DMO: Recent Hike Pushes The Yield On This Mortgage CEF Above 11.5%