DMO - DMO: Not Your Usual Mortgage Fund 11% Yield

Summary

- Western Asset Mortgage Opportunity Fund Inc. (DMO) is a closed end fund focused on mortgages.

- Unlike some of its peers in the space, DMO takes on significant credit risk through its holdings.

- The fund is trading at a -10% discount to NAV, and has seen discounts in its pricing since the Covid crash.

- The CEF's distribution is not fully supported, with roughly 30% of the dividend being composed of return of capital.

- This article covers CEFs from our suite of products.

Thesis

Western Asset Mortgage Opportunity Fund Inc. ( DMO ) is a closed end fund focused on mortgages. The fund achieves this exposure mainly by purchasing securitizations which offer the desired risk profile. Unlike some of its peers in the space that solely purchase Agency MBSs , DMO has a diversified portfolio that includes Legacy RMBSs, GSE Risk Transfer securities and CMBS bonds. The fund is fairly leveraged, with its ratio running at 37%.

The mortgage space is an interesting one to visit now, given the meteoric rise in mortgage rates. The substantial strain put on the system via historically high rates, should translate into high returns once the market normalizes.

The CEF is now trading at a -10% discount to net asset value, and it has been trading at discounts since the Covid crisis. We are assuming the fund experienced some forced liquidations during the crisis given its vertical move down in price and slow recovery afterwards. We expect the discount to persist until the next bull market in risk assets develops.

DMO Holdings

The fund focuses on mortgages, under different formats:

Allocation (Fund Fact Sheet)

To note that all above sector allocations are done via securitizations. Unlike traditional mortgage funds that invest in Agency securities which do not have credit risk (the principal is guaranteed by the U.S. Government), DMO takes credit risk via its portfolio.

For example, ' GSE Risk Transfer ' bonds:

CRT securities were created in 2013 to effectively transfer a portion of the risk associated with credit losses within pools of conventional residential mortgage loans from the GSEs to the private sector. Unlike Agency MBS, full repayment of the original principal balance of the CRT securities is not guaranteed by the GSEs ; rather, “credit risk transfer” is achieved by writing down the outstanding principal balance of the CRT securities if credit losses on the related loans exceed a certain threshold. By reducing the amount that they are obligated to repay to holders of CRT securities, Fannie and Freddie are able to offset credit losses on the related loans.

To translate the above in English - the holder of GSE Risk Transfer bonds represents the first loss portion if a homebuyer defaults on their loan and there is not enough equity in the house value to cover the taken mortgage. So these bonds are very risky, especially in the case of houses with high LTV ratios.

Similarly 'Legacy Residential Mortgages' represent pool of mortgages which are not guaranteed by Fannie Mae or other government agencies, and thus represent credit risky instruments, depending on where they are in the capital structure. The bonds are seasoned though, which represents a credit mitigant.

We can get an overall feel for the credit riskiness of the DMO collateral pool by looking at their rating profile:

Ratings (Fund Website)

We can see a very large 'Not Rated' bucket here, which indicates, all else equal, credit risk. Not all securitizations are rated, but usually the riskier ones fall in the not rated bucket because the originator and credit rating provider cannot always see eye to eye on how to model the cash flows.

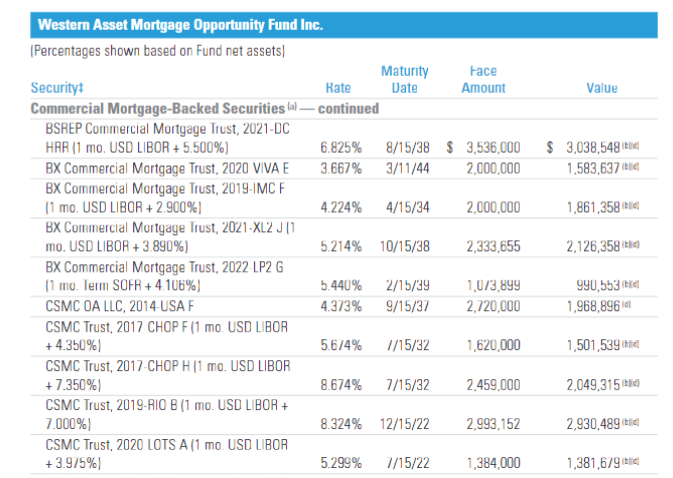

This fund also takes commercial lending risk via its CMBS portfolio:

CMBS Holdings (Semi-Annual Report)

{kind=link}

As per their definition:

Commercial mortgage-backed securities ((CMBS)) are fixed-income investment products that are backed by mortgages on commercial properties rather than residential real estate. CMBS can provide liquidity to real estate investors and commercial lenders alike.

This is another sector that has seen substantial weakness recently due to higher risk free rates. There are a number of large commercial loans having maturities in the next few years which will have a tougher time refinancing than the usual process.

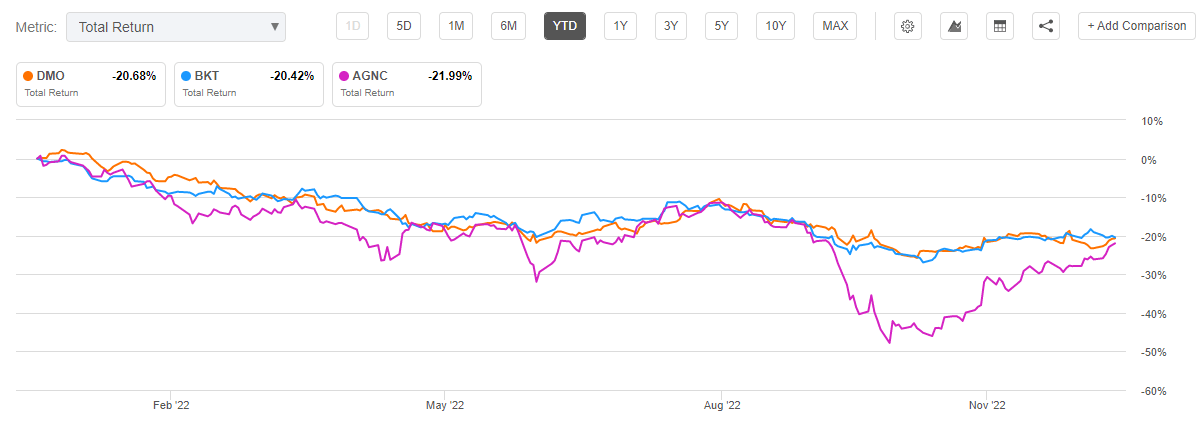

DMO Performance

The fund is down -20% year to date:

{kind=link}

We are comparing DMO here with an Agency MBS CEF, namely BKT , and a mortgage REIT, namely AGNC . We can see that all vehicles are down roughly the same on a total return basis this year.

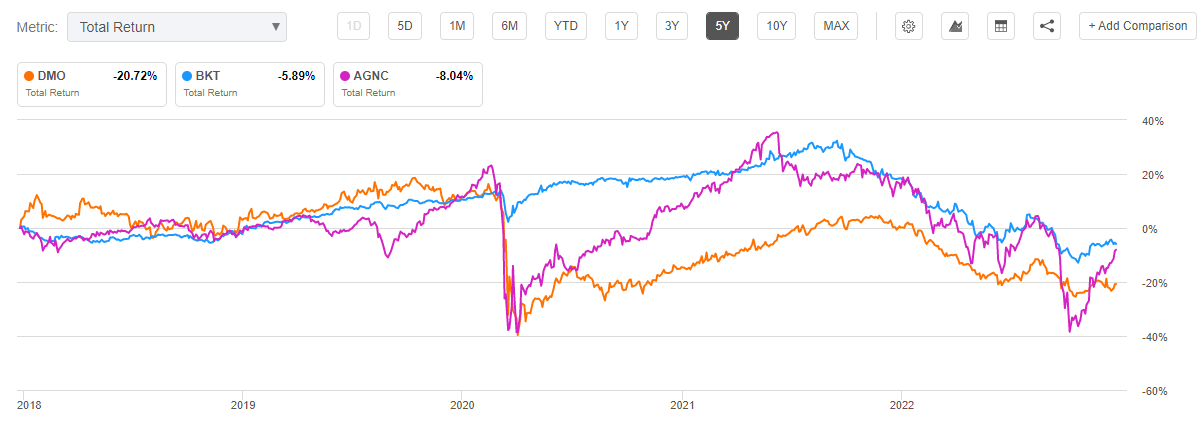

Longer-term, we can see that DMO experienced forced deleveraging during Covid:

{kind=link}

After experiencing a 50% drawdown during the Covid crisis the CEF was extremely slow to recover, and never entirely did. We presume the fund was forced to liquidate some of its holdings at the lows. As a reminder, the securitizations the fund holds are illiquid, and in a forced selling scenario they can get really poor pricing.

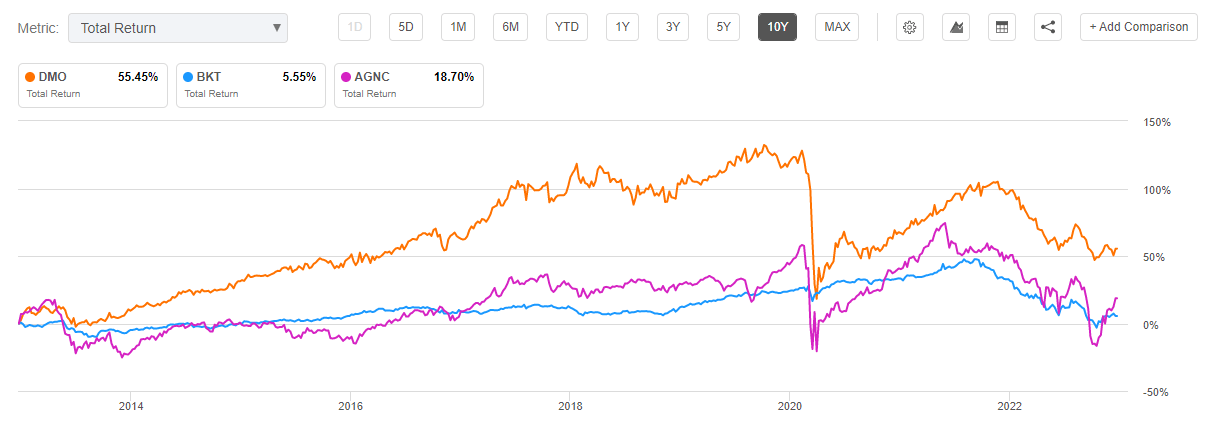

Prior to the Covid crisis the fund was doing well:

{kind=link}

DMO is ultimately susceptible to a credit driven black-swan event. As we have seen in Covid the fund can take a substantial beating if forced to deleverage its illiquid collateral. During normal market cycle times the vehicle is able to achieve good risk adjusted results, but a left tail event can negate a decade's worth of returns.

DMO Premium/Discount

The fund was trading at a premium to NAV prior to Covid:

We can see how the market pricing substantially changed here after the Covid drawdown. Ever since 2020, the CEF has usually traded at a discount. Expect this to persist until we have a new bull market in risk assets.

DMO Distribution

The CEF aims to have a steady distribution, which currently is $0.1 monthly:

Indications (Semi-Annual Report)

{kind=link}

The distribution is not currently fully supported though:

Distributions (Semi-Annual Report)

The ROC utilization here is on the wide side. We do not like this because it eventually results in NAV erosion, and we can certainly observe a very significant decrease in NAV in the past decade here.

Conclusion

DMO is a mortgage CEF. However, unlike other peers in the market, DMO takes significant credit risk through its holdings. The fund invests in non-Agency MBSs, GSE Risk Transfer securities and CMBS bonds, all which carry significant credit risk. As an example, GSE Risk Transfer securities represent a first loss piece if homeowners do not pay their mortgages, the house is foreclosed and the sell value is below the taken mortgage. With a 37% leverage ratio, the fund is susceptible to vertical falls in prices and being forced to liquidate collateral. On the flip side however, the vehicle does represent an interesting play on the mortgage market, at a time when we are seeing historically high rates. With the housing market frozen and more pain to come in terms of house price declines, DMO can represent an interesting play on a nice gap down in price. The CEF will have an explosive recovery when the waters settle but is set for a volatile price performance in the next six months. In a normalized economic environment, DMO has exposed above average returns. Some sort of a capitulation move in pricing here on the back of market-wide risk-off sentiment would represent a good, safe entry point.

For further details see:

DMO: Not Your Usual Mortgage Fund, 11% Yield