ING - DNB Bank Hits The Middle-Ground Of Rate Hike Benefits

2023-05-03 08:00:00 ET

Summary

- DNB Bank benefits from the fact that the Bank of Norway is going lighter on the hikes, meaning there's the higher net interest income without the deposit beta issues.

- Spreads are rising, and so are loan books, even organically when considering the merger of Sbanken into DNB.

- We think the personal loan dynamics should remain strong, and there is quite a lot of opportunity in the Norwegian corporate space as well.

- As far as banks go, DNB is our top pick. They own a major share in Vipps, which was merged some years ago with BankID and now with MobilePay, and is a veritable payments giant.

- The PE is low, and the Vipps valuation could cover about 5% of the market cap and provides pretty meaningful scope for earnings growth. The 7.3% yield makes it a high-conviction all-rounder of value and income.

Published on the Value Lab 04/30/23

DNB Bank ( OTCPK:DNBBY ) is a top pick among everything in the global banking panorama. It's not going to have issues like we've seen in the US due to Norway's lighter rate hikes, which are giving them a boost on the net income margin side. Key markets like real estate are supported by S/D fundamentals, so personal loans should rise. On the corporate side, strength in key markets like oil and gas are a good thing for corporate development, as well as plentiful credit from the other institutions too, keeps the environment healthy and primed for further loan growth. Finally, DNB has an edge in being a major owner of Vipps, a Norwegian payments app, that is merging with peers in other Nordic geographies. We estimate the valuation of Vipps could cover about 5% of DNB's market cap as of today, and is a latent source of earnings growth since it only just became profitable in recent quarters. With yields above 7% and a low PE, this is a top pick for income and value investors.

Q1 Breakdown

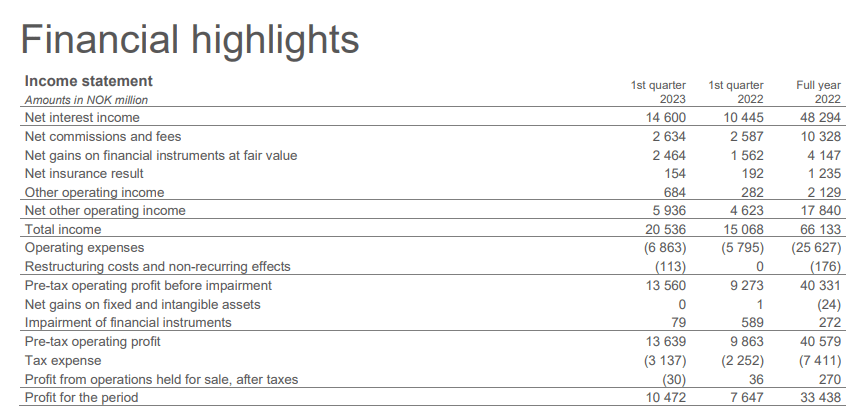

The headline figures are as follows , but they are exaggerated slightly by the merger with Sbanken late last year. While NII grew by 40% on a headline basis. Around 30% growth was achieved organically, and this is owed to continued double-digit growth in loan volumes but also increases in spreads on loans and deposits relative to last year thanks to the continued hiking, but rather slow hiking in 25 bps increments, of the Bank of Norway. The contributes of Sbanken to commission and fee income would be about 2%, and not very meaningful.

{kind=link}

{kind=link}

While both corporate and personal segments grew meaningfully in NII YoY, but personal grew in the mix with a more pronounce growth figure. Average loans grew by 14% in the personal segment, with loans in mortgages matching thanks to healthy trends in Norwegian real estate. The real estate market in Norway is still benefiting from relatively early stages of high-degree urbanisation, and relative to other western countries, Norwegian demographics are very strong. The S/D dynamics are strong in residential real estate, also helped by a tight labour market. The corporate income was being driven by solid loan growth and strong corporate conditions. Slow rate hiking keeps credit plentiful in Norway, and strong conditions in Norway's primary industry of oil and gas keeps major actors healthy.

{kind=link}

The commission and fee income grew but it was limited by headwinds to investment banking revenue and the asset management business. IB and AM is around 40% of fee and commission income, down from being 50% last year. Growth in card revenues offset these declines with large increases in money transfer and banking services.

{kind=link}

Vipps

The core business grew as you'd expect with loan growth combined with higher rates that aren't triggering deposit beta effects. What is more unique to DNB is their substantial, almost 50% holding of Vipps, which is a Norwegian payments app also combined some years ago with BankID , which is Norway's digital ID and signature app used to access state platforms and banking. DNB are the parent company of Vipps.

Now Vipps has merged with MobilePay which is the Danish Vipps equivalent, backed by Danske Bank ( OTCPK:DNSKF ). This will broaden its Nordic appeal but also prep it for becoming a more broadly used European app. DNB owns a little bit less than 50% of Vipps, and it will own about 33% of the new combined entity.

Vipps became profitable in 2022, but since we lack financial data, we need to value it on a cursory basis using customer number figures. The combined Vipps and MobilePay entity has about a third of the customers of Revolut , so a third of the valuation would put it at around $11 billion . Let's assume that Revolut was overvalued at its last fundraising, so bring it down to a $5 billion valuation for Vipps + MobilePay, and DNB owns about a third, so let's call it $1.7 billion in DNB's hands.

Vipps Customer Number (2022 AR)

This is a pretty conservative figure that can stand behind. The current earnings could also be used for valuing it with Wise ( OTCPK:WPLCF ) as a relatively close peer, which would value Vipps at around $700 million. Since the earnings have much more scope to grow than Wise, having just become a profitable entity, the $1.7 billion seems more fair.

Bottom Line

The current Vipps valuation is around 5% of the market cap and the earnings are growing quickly. There are other equity-accounted investments too in Fremtind and Luminor. Together they could probably cover about 10% of the market cap conservatively, where Fremtind and Luminor are also profitable, but Fremtind, which is an insurance company, had taken an earnings hit.

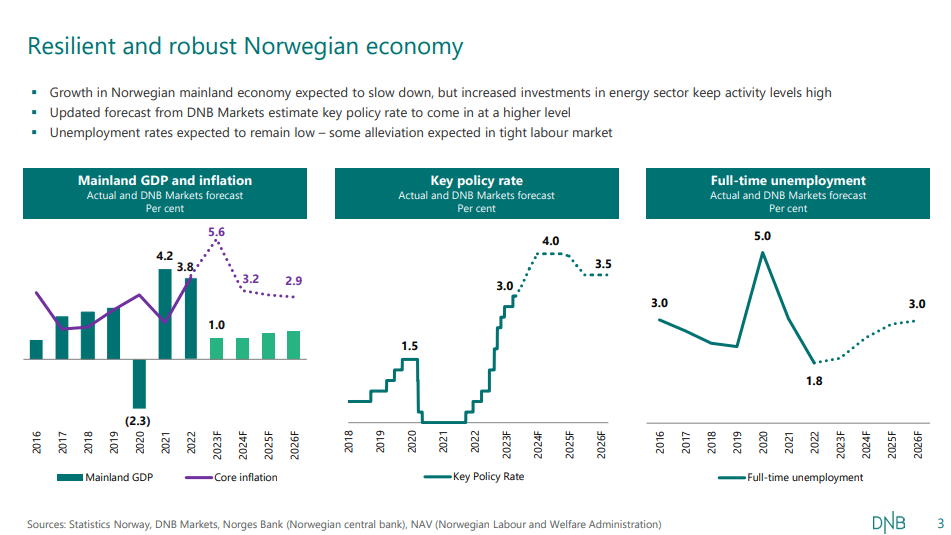

Otherwise, the DNB PE is low at below 8x, and the yield is above 7% and well covered. Trading in line with other European banking peers, but in much better shape and with some really nice equity-accounted exposures, we think that DNB is the better pick, certainly when stacked against companies like ING Groep ( ING ) and other European banks focused on deposits and lending activities. We see none of the risks in DNB that have hit other geographies in banking, and we remain bullish on the overall state of the Norwegian economy.

For further details see:

DNB Bank Hits The Middle-Ground Of Rate Hike Benefits