DNBBY - DNB Bank: I Expect An Upside Going Into 2024

2023-11-24 04:00:59 ET

Summary

- DNB ASA's share price has declined about 5.5% since July, but the company remains heavily invested in Scandinavian finance and banking.

- The bank's recent results show a strong performance, with a CET1 capital ratio of over 18.2% and quarterly profits of over 10B NOK.

- DNB ASA's NII is growing, and the company's capital position remains strong, making it an attractive investment option.

Dear readers/followers,

In this article, I'll update my thesis on DNB ASA ( OTCPK:DNBHF ). In my last article, which by the way you can find here , I went "HOLD" on DNB ASA. This article was back in July of this year, and since the piece, the share price has declined about 5.5% compared to an S&P500 of around 0.4% decline. I still hold a small position in DNB ASA, but other banking investments have taken a larger position compared to this one. Still, I remain heavily invested in Scandinavian finance and banking given the sheer fundamental upside related to the 2024-2025E NII tailwinds, which I consider to be absolutely massive.

In this article, I will take a look at the recent results for this bank, to sort of confirm this overall upside and implied forecast for the company. Despite underperforming the S&P500 in terms of total return excluding dividends, the bank has outperformed with dividends and other considerations, if we look at any sort of longer-term timeframe.

Let's look at what we have going for us with DNB.

DNB ASA - The upside here is fundamentally attractive

Selling overvalued equities has been part of my portfolio for the past few years. While DNB is a fundamentally qualitative bank, it's also a perfect example of why you do not hold stocks ad infinitum, unless you want to underperform the market in the short term.

The fact is, since I sold at above 200 NOK/share, the company has underperformed quite a bit. It's been buyable a few times since, but I never sized up my position again (unfortunately). If we see another dip, I may do so, but I don't think such a dip on a forward basis is all that likely.

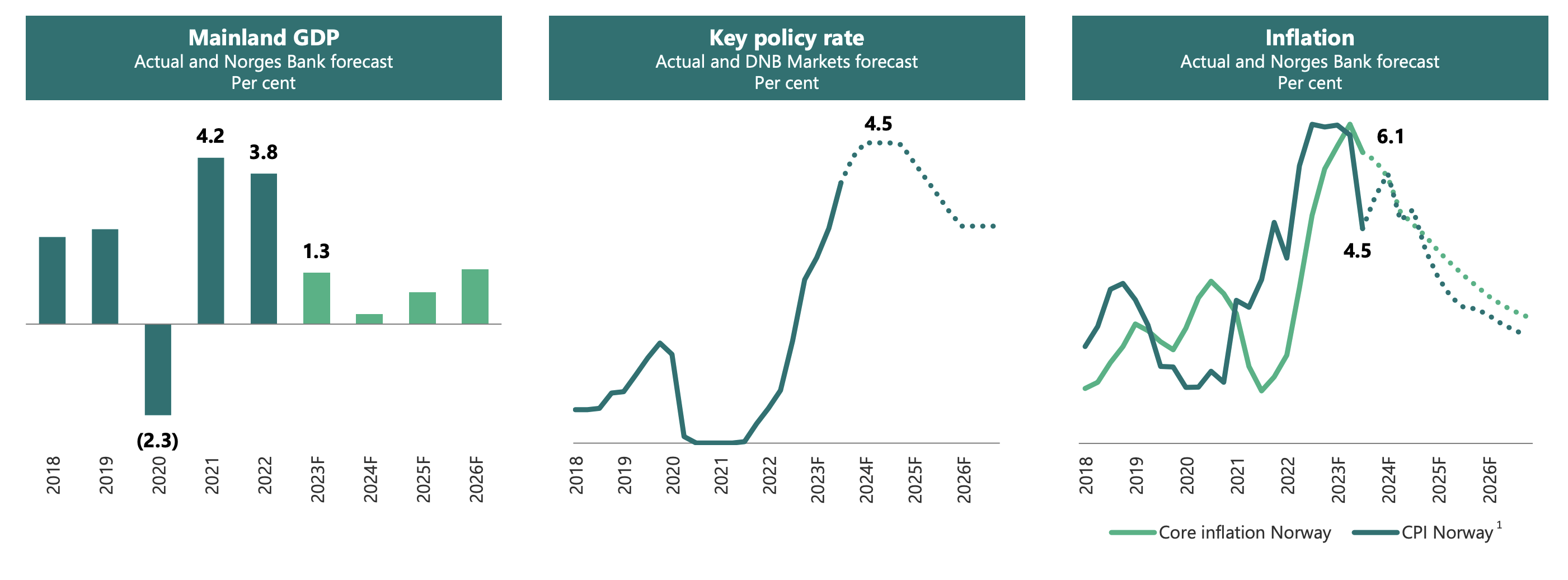

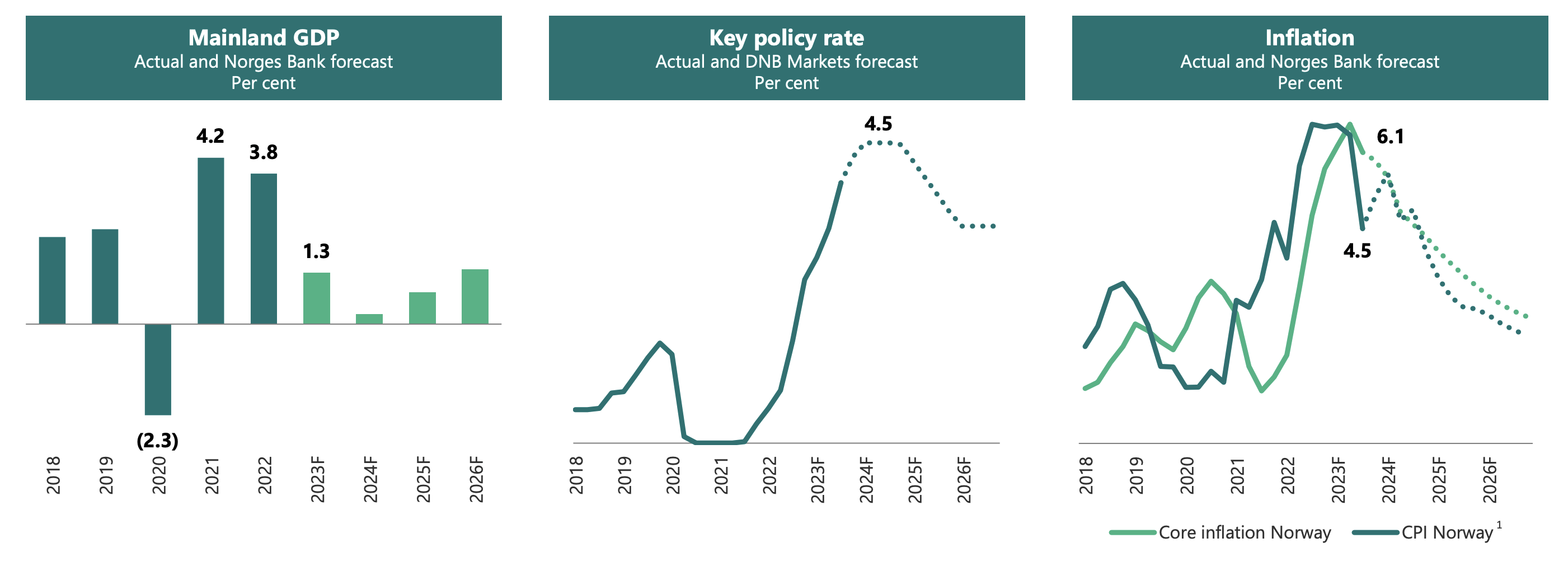

And DNB is a great bank. The company can be argued to be a proxy of the Norwegian economy, and the Norwegian economy, despite continued unfavorable FX, is an economy that's in great overall shape, with high amounts of corporate investment, allow amounts of inflation and good unemployment figures, even if we look at the 3Q23 numbers.

To expect any sort of decline in the 3Q numbers would have been illogical given the economic backdrop. Every single other bank in Scandinavia is recording and reporting record results for the short term. DNB is no different. We're talking a 3Q23 CET1 capital ratio of over 18.2%, we're talking over 10B NOK in quarterly profits , and the bank managing an RoE of over 16.5%. This trend is visible across all business areas .

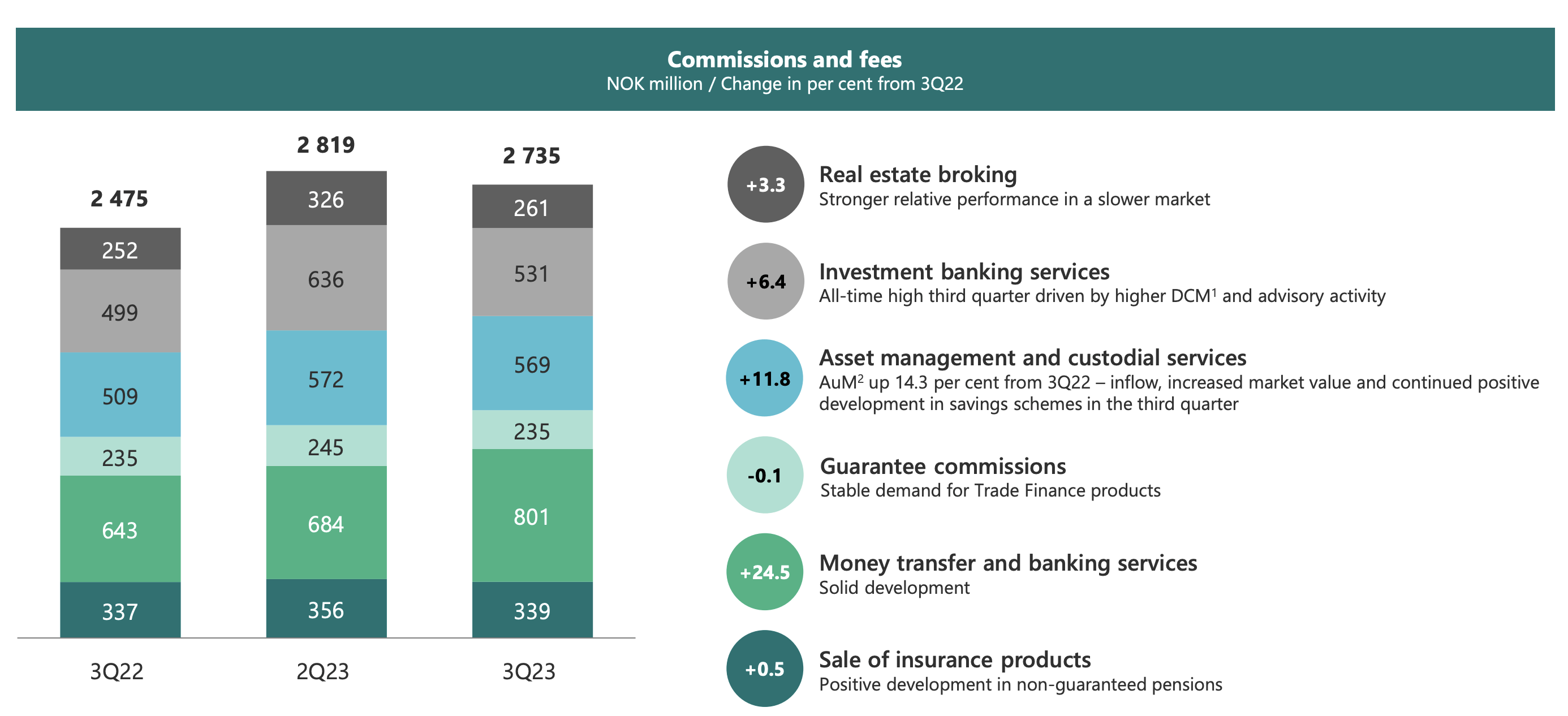

The NII which I mentioned is up 3.2% sequentially. Not only are we up significantly over time, but the overall trend and improvement is in fact still growing. Not only that, the company's instituted commissions and fees are up double digits YoY in terms of percent.

Some impairments were recorded - just below a billion NOK related to specific customer situations, but this does not impact the overall asset quality, with 99.3% of the company's assets in stage 1 or 2. The company may not have as stellar qualities as Handelsbanken, my largest Swedish bank holding, but it still manages to outperform most peers.

The company's quarterly EPS improved nearly 8% sequentially and 31.2% YoY. This if anything, shows us the sheer magnitude of the interest rate impacts here - and also serves as part of the justification for why DNB began a new share buyback program of 1% of outstanding shares.

Unlike Sweden and other European nations, the expectation for a soft landing in Norway is pretty well-established.

{kind=link}

Yes, GDP growth is modest, but Norway is in a position where the key policy rate is expected to top out at around 4.5%, which is already lower than we have here today, and can start to be cut down as early as late 2024E, if these forecasts are to be believed and inflation numbers somewhat hold. CPI and Core inflation are lower than Scandinavian peer nations as well.

{kind=link}

We can combine this with a surprising resilience in Norwegian households. The unemployment rate in our neighboring country is not below 2% anymore but is still below 2.5%, which is stellar. The real difference is in the debt servicing ratios, which are materially better than similar numbers in Sweden. Norwegian households are typically far less leveraged than Swedish ones (Source: DNB markets)

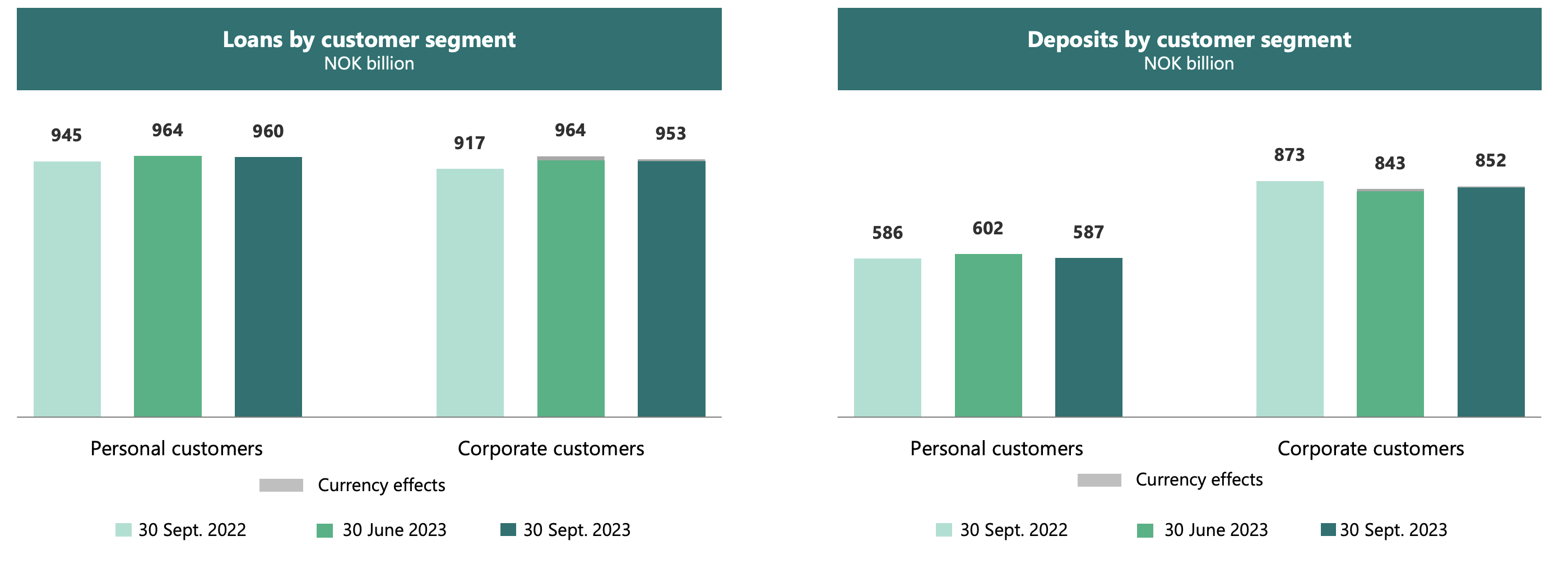

All this obviously leaves DNB in a very favorable position to drive growth across a multitude of vectors. The company is improving its digital offering. Segment-wise, both personal and corporate EBIT was up quite significantly. Compared to 2Q23 we're talking improvements of over 1.2B NOK for the personal side, and almost a billion on the corporate side as well - and this is with a volume headwind due to lower market activity.

{kind=link}

Combined spreads remain very stable despite overall headwinds and improvements in company income mainly in terms of net interest income, driven by the increased rates, repricing, and better spreads. Currency effects are minor in terms of weighing things down. NCIs were at all-time highs here.

{kind=link}

The company's capital position remains absolutely stellar, and unsurprisingly, at least for me, there is no change to the company's dividend policy. With quarterly earnings at the 6.39 NOK level for the latest quarter, this brings the expected full-year earnings, according to my forecasts, to between 23-25 NOK/share, which based on the current dividend policy implies a dividend of just over 14 on average. This in turn would imply a current company yield of 6.8%. Looking at where other banks are yielding and trading, this is actually below some of the company's closest Scandinavian peers, but DNB makes up for this by being one of the safest banks in all of Scandinavia, and the "best" Norwegian one to invest in, at least as I see it. This is despite whatever exposures to that 0.7% in non-stage 1 and 2 that the company may still hold at this time.

DNB has a very solid capital position and is continually stress-tested. The latest EBA stress test, about 2 years old here, sets the company at a reduction in CET-1 of 2.9%, compared to a Nordic peer average of 4.1% and an EU average of 4.8%. So as before, Scandinavian banks are better than the overall average, Norway is the best out of Scandinavia, and DNB is the best out of Norway.

There is nothing I see in the company's near-term or 2023-2026E that I view as realistic in derailing this company's longer-term upside and appeal. Based on this, I move to valuation and give you an update as well as a potential rating upgrade.

DNB ASA - The company had my PT for some time

If you followed my articles and my PT for the company, you'll know that the company in fact went under 200 NOK/share for a short time not that long ago. That was when I added shares to my position of DNB, and the recent 3Q23 was significantly better than I expected, which is why I'm increasing my PT for DNB to 200 NOK/share.

I believe the company, over the next few years, will see significant tailwinds from the combined NCI and NII trends, and this will result in far better dividend and earnings trends. When you combine this with the fact that DNB ASA is AA-rated, one of the few banks to sport this rating , and still trades at a P/E of sub-10x , you may start to see the underlying logic for my move here, and why my price target is actually still conservative , all things considered, and in light of the recent quarterly report.

The simple fact is I cannot be a valuation-oriented investor and not increase my PT when a company does this, and when compared to 2020, when DNB realized an adjusted EPS of 11.89 NOK, and is now expected to generate between 23-25 NOK for this year.

This company deserves a bump, and as of this article, I'm bumping it.

I view DNB as being fairly valued at around 205-220 NOK in range, and the company is currently at between 202-205. While this does not yet warrant a full rating upgrade, I went back and forth on doing so simply because I raised my PT and how close the company is to that level. The sheer level of upside here that's forecasted is also very certain in terms of forecast accuracy. DNB actually beats the forecasts 20-40% of the time on a 1-year and 2-year basis.

I changed my forecast and my stance here somewhat. In my previous article, I said that we should wait for peak inflation and a rate turnaround. In Norway, I now believe that we've reached peak inflation, and I believe we can realistically see an upside to this investment even based on the current forecasts. If we allow a 10x P/E and work from a 200 NOK/share price, we can see an upside of 15% per year with a 6%+ yield on a forward basis.

Combined with an AA-credit safety, I view this as good enough to work with here - and I give the company the following thesis update.

Thesis

- DNB is an excellent Norwegian bank, one of the best, and a proxy for investing in Norway as a nation. I view it as one of the best Norwegian investments that can be made.

- However, at current multiples, this bank isn't offering a whole lot of upside or comparative positives, as I see it. The yield is good, and we might see stable development from here on out, but the bank is also trading at a significant premium that I consider too high.

- I wouldn't consider buying DNB above 175-180 NOK relevant - and even then, the upside should only be considered "acceptable" in the broader perspective.

- I consider DNB a "HOLD" here, but only due to the fact that the company needs to move down to around 200 NOK, which is very close to the current level.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a high enough realistic upside based on earnings growth or multiple expansion/reversion.

DNB is currently a "HOLD" due to excessive valuation levels.

Thank you for reading.

For further details see:

DNB Bank: I Expect An Upside Going Into 2024