DNBBY - DNB Bank: Strong Fundamentals But Overvalued 'Hold' For Now

2023-07-19 12:24:24 ET

Summary

- I discuss my investment in Scandinavian bank DNB ASA, which I bought during the COVID-19 crash and sold when it became overvalued.

- Despite underperforming the S&P500 in terms of total return excluding dividends, the bank has outperformed with dividends and other considerations.

- I believe DNB ASA is fundamentally attractive and would consider buying shares again if the price is right.

Dear readers/followers,

Scandinavian banking remains one of my primary investments. One of those investments is my position in DNB Bank ASA ( DNBBY ). The position is nowhere near as big as it once was, because I have rotated much of my position in it when the company went to what I viewed as overvaluation. But I have written about the bank before, all the way back in 2021. I invested in the bank well during the COVID-19 crash and sold it when it became expensive. My latest rating was "HOLD", and despite that, this was almost 2 years ago, and everything that's happened since the total return excluding dividend payouts has actually underperformed the S&P500.

Seeking Alpha DNB (Seeking Alpha)

With dividends and other considerations, we have a clear outperformance here - but not as much as you might think for a bank like this. The fact is, since I sold at above 200 NOK/share, the company has underperformed quite a bit. It's been buyable a few times since, but I never sized up my position again (unfortunately). If we see another dip, I may do so, but I don't think such a dip on a forward basis is all that likely.

Instead, let's see why I believe this bank is fundamentally attractive, and why at the right price, I would start really buying shares once again.

DNB ASA - Perhaps one of the best banks in Scandinavia

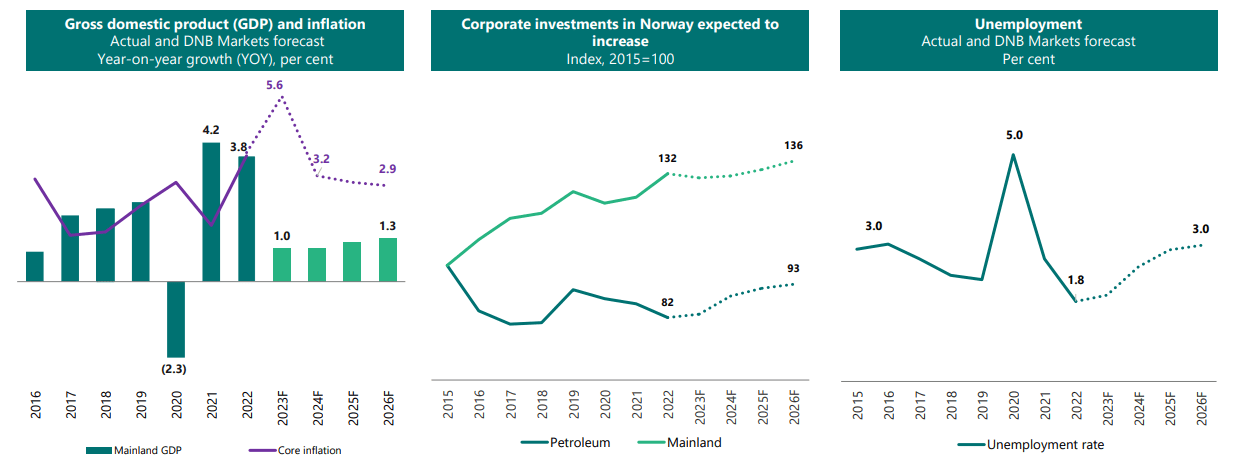

DNB is a great bank. The company can be argued to be a proxy of the Norwegian economy, and the Norwegian economy, despite continued unfavorable FX, is an economy that's in great overall shape, with high amounts of corporate investment, allow amounts of inflation and good unemployment, as per the numbers presented here.

{kind=link}

DNB IR (DNB IR)

With over 80% of the group's revenue coming from its Norwegian units, the company lacks meaningful outside exposure or diversification such as in the case of Nordea ( NRBAY ). Norwegian households, on average, are far better prepared than households in Sweden for upticks in interest rates, with on average debt-servicing ratios of above 17x even with upticks in interest burdens. On a macro level, households have over 260B NOK in excess savings in 3 years, and leverage towards housing prices remains modest. Unlike Sweden, Norwegian customers have also shown strong tendencies and habits to amortize their loans.

There are a lot of things that are "better" in Norway than Sweden or Denmark. The nation's central bank and monetary policy have been far more aggressive than in other nations, and key policies are already at levels where Sweden should have been years ago. Furthermore, the nation's pension fund acts as a massive buffer , with a nearly 12,000B, or 12T NOK valuation.

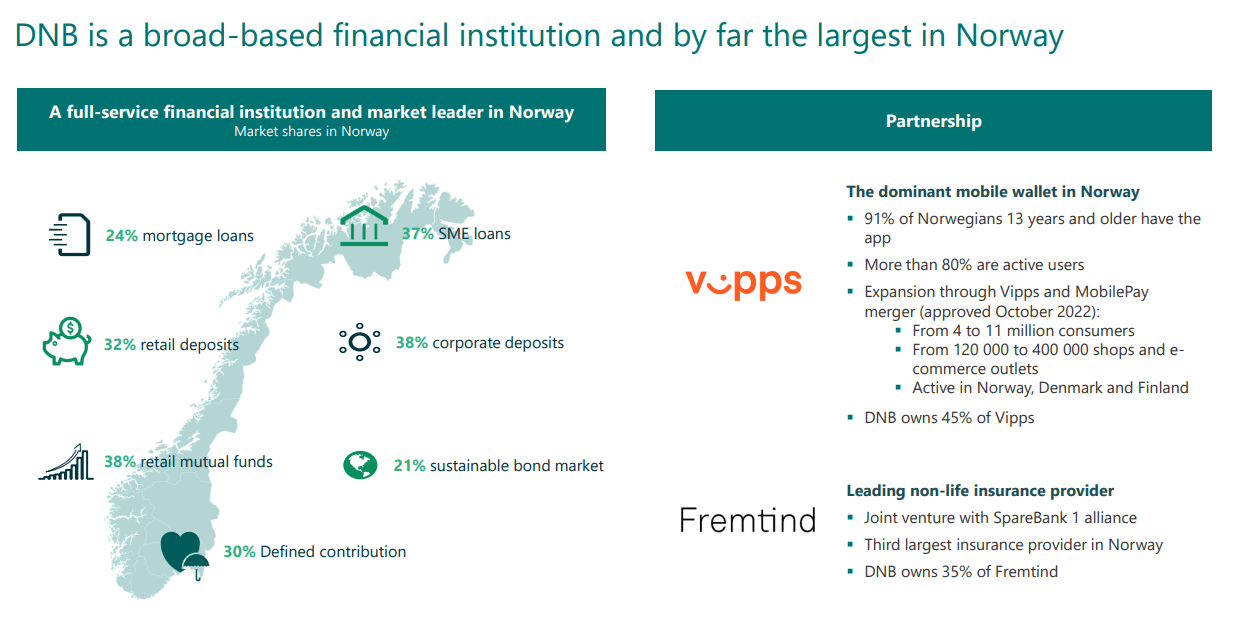

DNB is a proxy to this economy and is the largest financial institution in Norway - by far. It also has partnerships with key digital players, such as the dominant mobile wallet (more than 91% of all Norwegians above 13 have it), and the leading non-life insurer.

{kind=link}

DNB IR (DNB IR)

This makes DNB the leading financial, not even bank, but a financial institution, to invest in all of Norway.

And that is why, at one point, DNB was 5% of my portfolio at an RoR of over 90%.

However, every company in the world is capable of what I would consider to be "unacceptable amounts" of overvaluation. That is why I, in the end, ended up selling the company when it became too expensive.

But at any time there is undervaluation to be had here, I go in. I go in due to a Cost-income ratio of below 40%, a CET-1 of above 17%, a dividend policy of over 50% of earnings, and a core, overriding target of 13% or above RoE. This is the "gold standard" of banks, next to some Scandinavian ones here.

DNB has managed consistent, growing dividends for a period of no less than 12 years at this point, and the latest dividend in 2022 came at a then-yield of 6.4% and 12.5 NOK/share. There is absolutely zero reason why this dividend should not grow on a forward basis, making this a very decent prospect at the right price.

Its strong and diversified product offering offers a very solid foundation for dividend growth. Operating income from customers do not only come in the form of NII or Commissions, but fees for investment banking, FICC customer income, asset management and defined-contribution pensions, and other attractive avenues. Furthermore, these incomes are showing positive trends.

The company has one of the strongest positions in existence across products, industries, and services, and this includes investment banking services

It's equally crucial to note that this is a part-state-owned bank. 34% of DNB is owned by the Norwegian government, another 8.4% by DNB Savings Bank Foundation, and another 6.8% is owned by Folketrygdfondet, which in itself is partially state-managed. This means that almost 50% altogether is somehow under Norwegian public/DNB management, making for an extremely motivated owner.

Another solid point in the bank's favor is that it's almost a sector leader in terms of net margin. When it comes to DNB, the company is one of the very few banks to manage 50%+ net margin, with only 40% total noninterest expense for the entire operation, compared to overall annual revenues, which as of 2022 were at over 65B NOK.

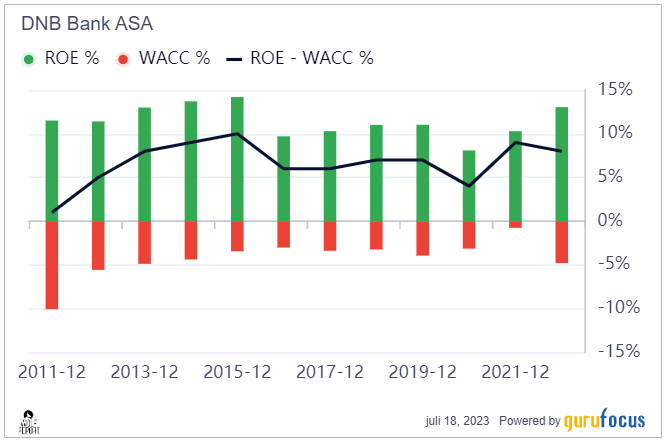

This is a consistently profitable and market-beating bank, that hasn't been close to being ROIC/WACC negative for over 10 years.

{kind=link}

DNB ASA IR (GuruFocus)

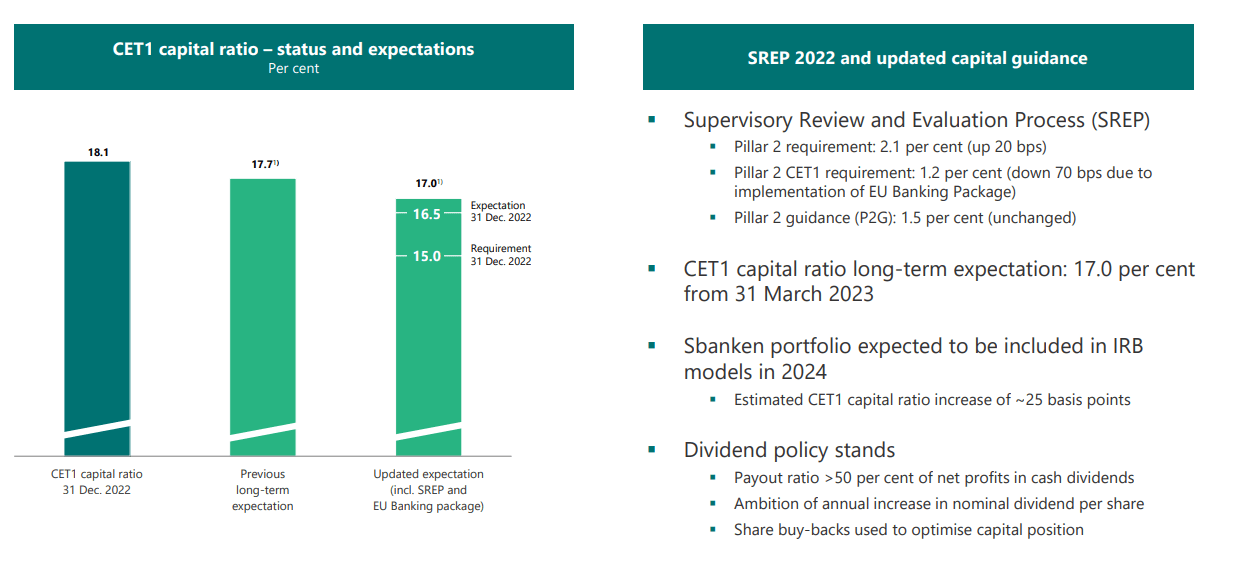

DNB has a very solid capital position and is continually stress-tested. The latest EBA stress test, about 2 years old here, sets the company at a reduction in CET-1 of 2.9%, compared to a Nordic peer average of 4.1% and an EU average of 4.8%. So as before, Scandinavian banks are better than the overall average, Norway is the best out of Scandinavia, and DNB is the best out of Norway.

{kind=link}

DNB IR (DNB IR)

Company operations are split into personal and corporate, both with reported improving trends including things like a growing loan book, and growing deposits due to the higher interest rates, which also puts NII and other incomes at a growing overall level. 2Q22 is out, in fact, it's out this week, and the results we see from here are encouraging.

2Q2 2 profit came in close to 9.5B NOK , up 1.5B+ NOK, or almost 19% from a YoY quarter. This is growth across personal and corporate markets, with many customers transitioning to the largest bank.

NII increased by 4.3%, driven both by growth and an increase in rates - some small provisions of less than 10% of profit due to legacy portfolio operations out of Poland, but nothing that's really worrying here, as I see it. The company has a continued level of very low overall defaults or impaired loans. RoE was well above the bank's target of 13%, coming in at 15.6% and up from 14.2%, with a C/I ratio on a quarterly basis of close to 35%, one of the lowest I've witnessed in a bank.

The company's CET1-ratio is also up, for the quarter, to a level of almost 19%, which puts it at the level of some of the leading Swedish banks in CET-1, but without the consideration of significant loan exposure to an under-amortized housing market - as we have here.

All of this forms the basis for my valuation thesis for the bank.

DNB ASA - Undervalued in case of significant outperformance, but not "cheap" here.

The problem is that there is so much cheap quality on the market today. With the recent crash in Telcos, my attention is on telcos and Real estate , they being the sectors I currently see the most value. Finance companies seem to be recovering, and while opportunities exist, we want to make sure that we buy the most undervalued at the highest potential quality we can find. And this may not, I say may not , be DNB.

S&P Global targets here are very lofty. 17 analysts give the company a range starting at 188 NOK to 290 NOK, with an average of 222 NOK. When I last wrote about DNB, my target came between 175-180 NOK. Of course, this was during ZIRP. This alone means that I'm bumping my range by 20 NOK, coming to a PT range of 195-200 NOK, with perhaps an average of 197.5. The picture I want to give you is that I consider DNB to even with its current outlook, to be overvalued and not a good enough "BUY" here, given what's available on the market next to this company.

Out of the 17 analysts following the business, only 4 have a "BUY" rating, which to me, despite their high averages, implies a worrying lack of conviction in a target range that goes as high as 290, which is well above 25% above the current share price. But it goes to show you that just because some analysts rate something a "BUY", does not mean you should listen - especially with no "skin in the game".

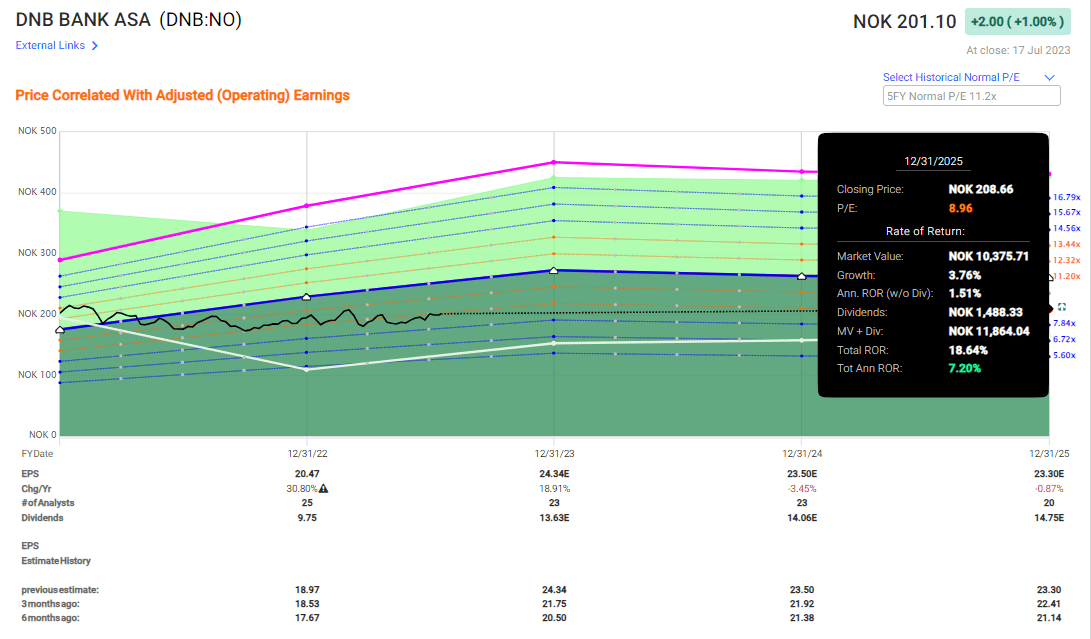

Looking at other avenues for potential upside, I want to emphasize that DNB is certainly not grossly overvalued, but it's based on a high earnings bounce in 2023 (which I believe will materialize), but a decline there as we see peak inflation, peak rates, and peak "upside" in Norway. FactSet analysts agree with those forecasts I set here and forecast an EPS growth rate normalized over 3 years of around 4.5%. The bank has, over the past 2 years, traded between 8-10x P/E. On the low side, this you an annualized RoR of around 7.2% at a P/E of around 9x, so around the midpoint here.

{kind=link}

F.A.S.T graphs DNB upside (F.A.S.T graphs)

Are you starting to see my problem here with the company and this valuation, despite its AA-? The reason my rating here is a "HOLD" is that the company, given its fundamentals and what we see in the next few quarters, is not favorable enough given the price.

I maintain that we should wait for the realization of peak inflation and interest rate to materialize, wait for the company to drop below 195 NOK per share, and then load up at yields of 6-7% overall.

Anything above that, and I argue that there are better "BUY"s to be had in this market.

What are your thoughts on the matter?

Here is my thesis.

Thesis

- DNB is an excellent Norwegian bank, one of the best, and a proxy for investing in Norway as a nation. I view it as one of the best Norwegian investments that can be made.

- However, at current multiples, this bank isn't offering a whole lot of upside or comparative positives, as I see it. The yield is good, and we might see stable development from here on out, but the bank is also trading at a significant premium that I consider too high.

- I wouldn't consider buying DNB above 175-180 NOK relevant - and even then, the upside should only be considered "acceptable" in the broader perspective.

- I consider DNB a "HOLD" here and would caution you to be similarly careful with investing here.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a high enough realistic upside based on earnings growth or multiple expansion/reversion.

DNB is currently a "HOLD" due to excessive valuation levels.

Thank you for reading.

For further details see:

DNB Bank: Strong Fundamentals But Overvalued, 'Hold' For Now