DNIF - DNIF: The Ugly Duckling CEF

2023-11-06 09:08:46 ET

Summary

- The Dividend and Income Fund is a closed-end fund that trades at one of the deepest discounts.

- The fund has struggled with mismanagement and dilution, but has recently shown improved performance and exceeded peers.

- DNIF offers a high distribution yield due to the discount, but its OTC trading and lack of catalysts may deter some investors.

Written by Nick Ackerman, co-produced by Stanford Chemist.

The Dividend and Income Fund (DNIF) is a bit of an ugly duckling when it comes to the closed-end fund space. The fund is a pretty standard, mostly equity fund, but they do carry some corporate bonds and a few preferred holdings. The fund has even put up halfway respectable results against the S&P 500 Index in more recent years.

At the same time, this fund trades at one of the deepest discounts in the CEF universe. They switched to trading on the OTC market in 2020 voluntarily, so that move didn't help. Prior to that, the fund's ticker was ( DNI ). However, even before that, the fund's discount was quite large for a number of years.

Besides going OTC, there are several other issues that have caused the results we see today.

The Basics

- 1-Year Z-score: -1.08

- Discount: -35.23%

- Distribution Yield: 9.83%

- Expense Ratio: 1.41%

- Leverage: 14%

- Managed Assets: $213 million

- Structure: Perpetual

DNIF's primary objective is "high current income" with a secondary "capital appreciation" goal. To achieve that, the fund will invest "under normal circumstances, at least 50% of its total assets in income-generating equity securities."

The fund targets "companies with strong operations showing superior returns on equity and assets with reasonable valuations. Generally, the Fund purchases and holds income-generating equity securities of profitable, growing, and conservatively valued companies across a broad array of industries."

The fund employs some modest leverage in the form of borrowings. They pay a rate of SOFR plus 1.28% on that leverage, which is higher than usual. As most funds that incorporate borrowings, they are experiencing rising costs, and that's pushed the fund's total expense to 2.18% as of their last semi-annual report .

Given the fund's small size and trading OTC, there is a serious lack of liquidity here. So, buying and selling shares of the fund in a hurry probably isn't going to be something one can count on, and if that was the goal, one should look elsewhere.

Performance - Discount Near All-Time Low

The largest selling point for the fund would be the massive discount presented. This is near an all-time low since the fund's inception back in 1998. The fund even carried a significant premium prior to the Great Financial Crisis.

However, Bexil Advisers LLC took over the fund's operations on February 1, 2011. Prior to that, it was quite a different fund, so that can give us some more background on a potential catalyst to see this discount open up. George Spritzer, in an older article , had more details on that topic.

Ycharts

He also highlights how the fund has issued new shares that had significantly diluted NAV as well. Which really starts to paint the picture of where we are today. They continue to issue new shares when investors reinvest their distributions, which puts a bit of pressure on the fund as well. It's only been a few cents in each of the last several years. They haven't had a rights offering since 2018, which is really when the dilution kicks into high gear, as that gave the fund a -$0.52 NAV hit.

Of course, the other problem is there is no catalyst for closing this discount. It is a perpetual fund, and there are no activists targeting it at this time, at least according to the latest filings (or the lack thereof.)

We see that a lot of generally straightforward, older equity funds carry sizeable discounts. Adams Diversified Equity Fund ( ADX ), Central Securities Corp ( CET ) and General American Investors Company ( GAM ) are all fairly similar funds.

Ycharts

Of this group, and I've also included the Eaton Vance Tax-Advantaged Dividend Income Fund (EVT), DNIF has performed the worst. This wasn't by a small degree either, as the underperformance had been pretty substantial not only on a total share price result but with the underlying portfolio, too. This is a performance comparison over the last decade, so it is well into when Bexil was managing the fund.

Ycharts

I've included EVT because, like DNIF, these funds tend to position themselves in the value-oriented sectors rather than a heavy emphasis on tech.

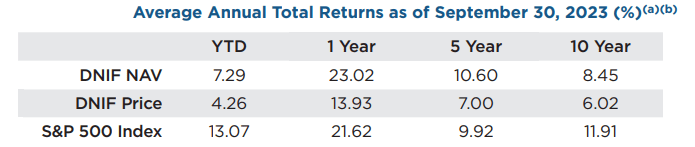

That being said, if we look at their last fact sheet, it's still put up fairly respectable results against the S&P 500 Index. When looking at the last ten years, we see that's where the fund struggled the most against that index. However, over the last 1 and 5 years, it has outperformed.

{kind=link}

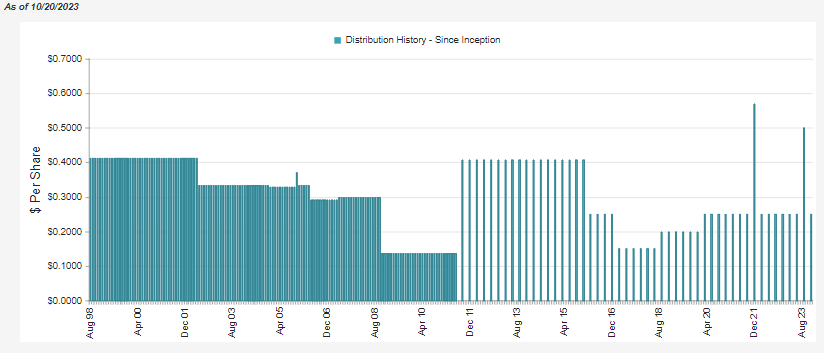

Distribution - Deep Discount Leads To Massively Juiced Rate

They had paid a monthly distribution, but it appears when Bexil took over, they switched to a quarterly distribution. They then cut a couple more times since then, and that can be one reason why investors also choose to avoid this fund. (There wasn't a special declared recently; the most recent one being included on the chart is an error.)

{kind=link}

Most CEF investors tend to prefer monthly distributions with limited adjustments. For me, that isn't necessary to invest in a fund and especially with a dramatically shifting environment, we are likely to see more distribution changes going forward.

That being said, a big selling point for DNIF goes back to the fund's discount. Due to the massive discount, the fund's distribution rate on NAV only comes to 6.37%. At the same time, investors get a distribution yield of 9.83%. That puts them in a situation where the fund has to earn significantly less to sustain the distribution while investors see a massively juiced-up payout.

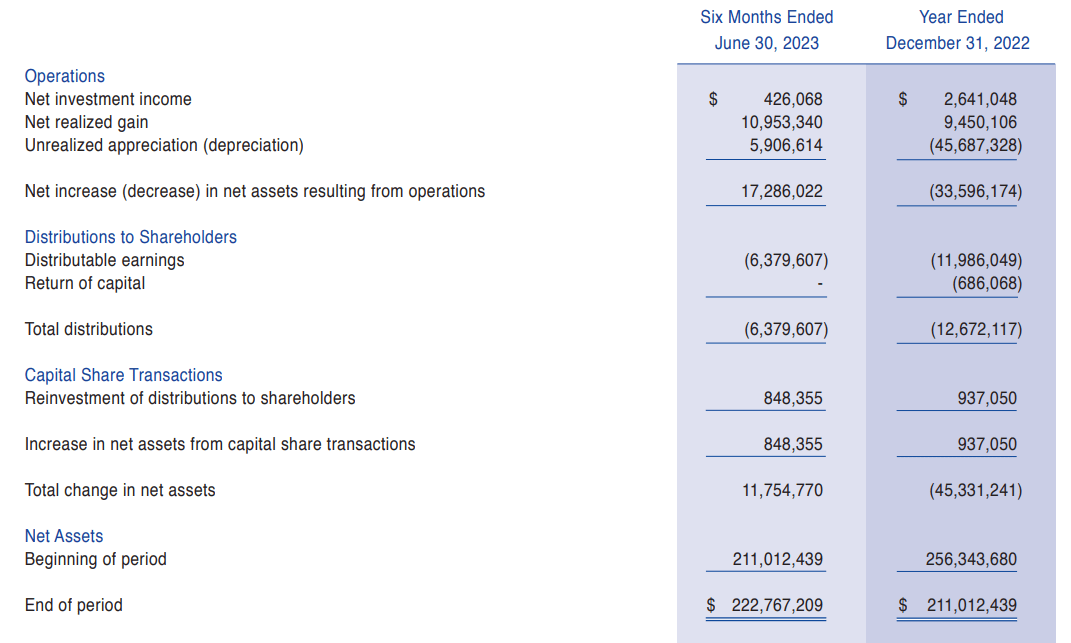

In the first six months of the year, the fund had enough net investment income and realized gains to have covered the payout. Enough that the back half of the year's distribution is already 'covered' to a sizeable degree as well. That was even though the fund's NII took a big hit this year and would come in much lower this year relative to last year.

{kind=link}

For tax purposes, the fund's distribution has largely been classified as capital gains, as one might expect. Capital gains taxes are taxed favorably and that could make it more appropriate for a taxable account.

DNIF Distribution Tax Character (Bexil)

DNIF's Portfolio

The problems of the fund seem to stem from mostly the mismanagement of the fund, as the fund's portfolio is fairly straightforward. We've even started to see some decent results in more recent history when the fund stopped diluting the fund so much with rights offerings. They are still having small dilution due to DRIP issuing new shares, but in the last five years, that wasn't enough to hold back the fund. In fact, during that time, the fund outperformed EVT.

Ycharts

The fund is most heavily weighted to financials, basic materials, industrials and consumer cyclical. Even with this more value-oriented approach, the fund has performed quite well this year. 2023 has been a year where the results have been mostly driven by the Magnificent Seven, with little participation elsewhere.

DNIF Sector Allocation (Bexil)

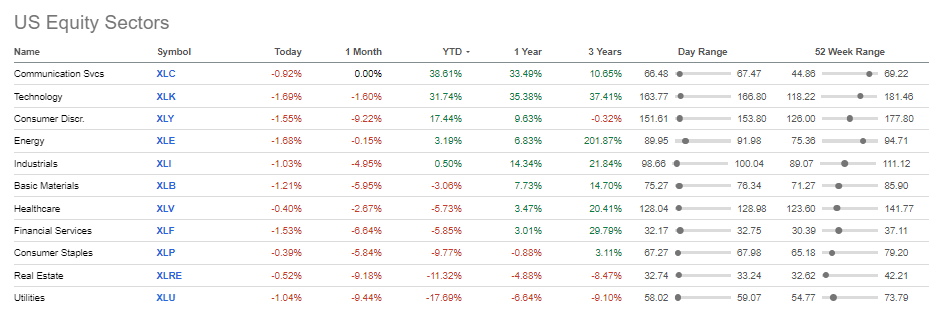

At the same time, DNIF's weighting to tech is rather small. Fortunately for the fund, it has mostly avoided real estate and shows no listings for utilities at all. With utilities being the worst-performing sector, that's gone a long way in avoiding that space. Still, it's not as if financials are performing well either; financial services are down 5.85% YTD as of writing. Additionally, basic materials are also down, and industrial are about flat lines.

{kind=link}

So clearly, DNIF is finding what is working in mostly rubble. That's showing some promise for the fund to be able to show positive performance when most of your largest sector weightings are down or barely showing positive results.

DNIF Top Ten Holdings (Bexil)

Here's a look at the fund's current top ten holdings and how they've performed YTD so far.

Ycharts

The biggest loser here has been U.S. Bancorp ( USB ). That was one of the regional banks that were ravaged in March's banking crisis and has still been languishing.

As an actively managed fund, they are constantly buying and selling, so these holdings may not be representative of how they were positioned previously. The fund's last reported turnover was 16%, which is down from 42% in the prior year. For some context, though, we do see a few different names they were holding at the start of 2023 that don't make it into the top ten in the latest update.

DNIF Top Ten Holdings December 2022 (Bexil)

Conclusion

DNIF is the ugly duckling of the CEF world, but perhaps it's starting to turn the corner. The results of the fund more recently suggest they've been able to put up respectable results and even exceed peers. They've managed to invest in a more value-oriented portfolio this year and still put up rather solid results relative to what the broader sector performance has been.

If they can continue to stay away from the dilutive rights offerings, that would certainly help. Due to the massive discount, investors receive a substantially higher distribution yield than the rate that the underlying portfolio has to earn for it to be covered. That's certainly another positive for the fund.

On the other hand, the fund trades OTC. The move to go OTC certainly didn't help its investors and only made its discount widen further. Being traded OTC and being a small fund means trading volume is a prohibiting factor for some investors.

Additionally, there is no catalyst in play to see the fund's discount narrow, and it really appears that the trend is still going to an even wider discount. So, it is yet to be determined whether this discount is a good value. It would suggest it is on an absolute basis and relative to its own history, but where it ends up eventually is unknown for now. At this point, it wouldn't seem to hurt for shareholders who are in this fund to sit tight with what they have.

Is this ugly duckling ready to shine, or will it continue to be mired? Only time will tell.

For further details see:

DNIF: The Ugly Duckling CEF