ETV - DNP: A Golden Utilities CEF Currently Extremely Overpriced

Summary

- DNP is a utilities equities closed end fund with a substantial track record.

- The fund is one of those rare, golden standard CEFs that have always traded at premiums to NAV in the past decade.

- With the entire Utilities sector trading at historic high P/E ratios on the back of a market-wide defensive stance, DNP is now trading at a record 27.15% premium.

- We love this fund (and own it), but nothing escapes mean-reversion when overbought conditions are present.

- The FAANG exuberance seen in 2020/2021 has been replaced by Utilities / Healthcare overweight positioning on the back of recessionary fears.

Thesis

DNP Select Income Fund ( DNP ) is a closed-end management investment company that first offered its common stock in 1987. The fund's primary investment objectives are current income and long-term growth of income. DNP seeks to achieve its objectives by investing primarily in a diversified portfolio of equity and fixed income securities of companies in the public utilities industry.

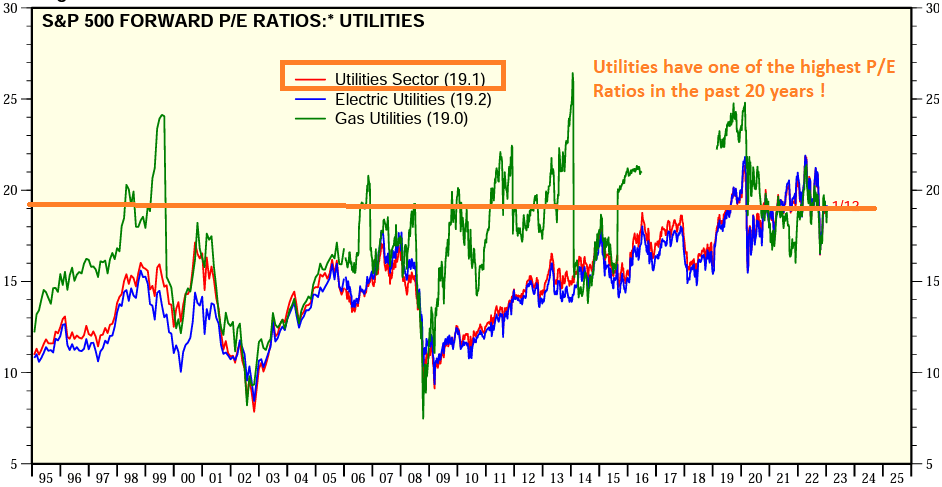

DNP is a golden standard of the Utilities CEF structures. Utilities are a defensive asset class, and they have seen a massive inflow of capital as investors have started to price in a recession. Massive inflows into an asset class not matched by an equivalent move up in fundamental performance, end up inflating the numerator of the 'P/E' ratio:

{kind=link}

As we can see from the graph above, courtesy of Yardeni, the Utilities sector displays one of the highest P/E ratio observed in the past 20 years. Why is this the case? Because it is a defensive sector:

{kind=link}

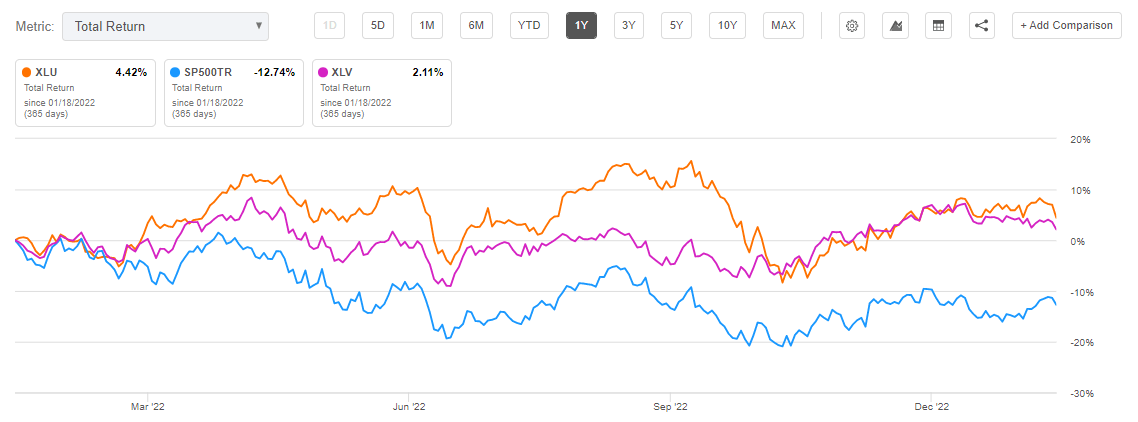

We can see in the above total return graph that the Utilities Select Sector SPDR ETF ( XLU ) and the Health Care Select Sector SPDR Fund ( XLV ) had very shallow drawdowns in 2022 as the S&P 500 cratered. The reason for this performance is the crowding-out trade. Unlike retail investors, many large asset managers have defined, maximum cash buckets which usually tend to be in the 5% to 10% range. That means that a large fund cannot hold cash more than those levels, which translates into the fund managers moving into defensive stocks/sectors when they believe a recession is around the corner. As retail investors we have the luxury of sitting 100% in cash if we choose to do so, whereas large asset managers need to somehow justify their fees, thus always remain invested in the equities markets to a certain extent.

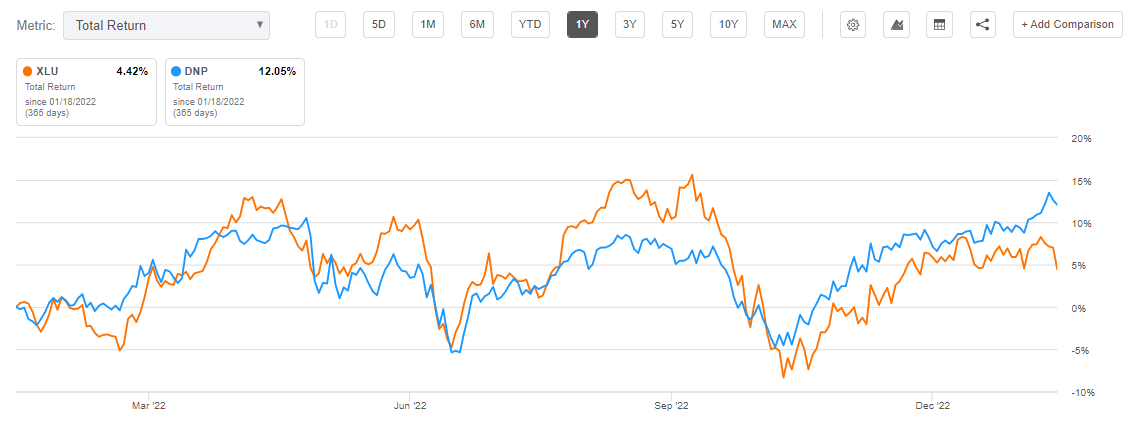

We can see how DNP's total return closely mirrors what we observed in XLU:

{kind=link}

DNP is a structural transformation of Utilities equity exposure into monthly dividends. The CEF structure though has its pitfalls as well, namely the premium/discount to NAV. When investors love a CEF too much, they tend to bid it up substantially, but unlike an ETF which just issues more shares, a CEF just ends up having a large premium to NAV. So you have a bit of a double whammy here - a massive, unsustainable premium to NAV for DNP (which we discuss in detail in the below 'Premium / Discount to NAV' section), and a historic high P/E ratio for the underlying asset class, namely Utilities.

Premium / Discount to NAV

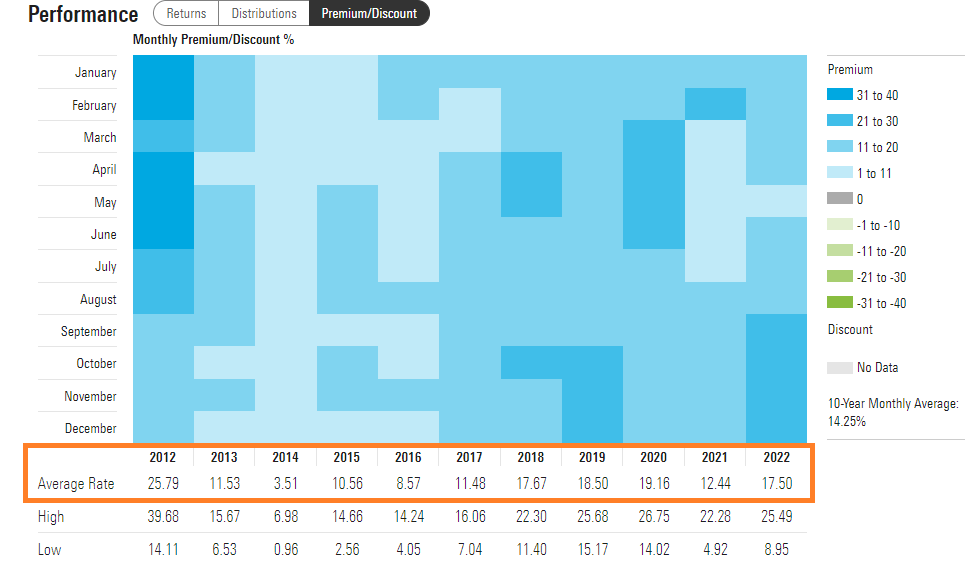

DNP is one of those rare, golden standard CEFs that have always traded at premiums in the past decade:

{kind=link}

The above table, courtesy of Morningstar, presents the monthly premiums/discounts for DNP in the past decade. Blue is indicative of a premium to NAV, while green shows months when the CEF was trading at a discount. We can only see blue in the table above, signifying a voracious investor appetite for this name.

The orange box we have drawn above shows the average premium exhibited by the fund, by calendar year. Outside 2012, we can see the CEF having an average premium of 15% to 17%. Moreover, if we look at the next row, again outside 2012, the fund never exhibited a premium higher than 26.75%, achieved in 2020. Which brings us to today's premium level, which is currently 27.15%:

DNP Premium to NAV (YCharts)

Today's premium level is basically the second largest in the past decade. Is it sustainable? No. Simply put, the CEF's shares trade at a premium of 27.15% to the actual NAV of the fund. If DNP were to liquidate today, investors would lose 27.15% right now. Framing the premium from this angle should give a retail investor a better understanding of the magnitude of this dislocation (for avoidance of doubt, there is 0% chance of a fund liquidation; however, the crux of a CEF structure is the basis between NAV and share price).

Conclusion

DNP is a 6.7% yielding CEF. The fund transforms Utilities equities returns into monthly dividends. The vehicle is a golden standard in the CEF space, having an extremely robust historical performance and long tenure. Investors have recognized the long term value in the CEF by bidding it up in the past decade. In the past ten years the CEF has spent its time at a market value above its net asset value. On average, when measured monthly, the premium to NAV has been around 15%. Currently DNP is trading at an extremely high historic level of 27.15% above NAV. This is due to the ongoing recession and the defensive market positioning in Utilities.

We love DNP and own it, but have trimmed it substantially from our 401(k) account and exited it from our personal, actively traded account. We are strong believers in mean reversion, and overbought conditions tend to be followed by a reversion to historic averages. We have seen this time and time again, most recently with the FAANG cohort in 2020/2021 and with another CEF we love, namely ETV . We called out the fund when its premium reached historic highs mid 2022 in our article here , and surely enough the premium contracted by more than 12% in the subsequent months.

We have a similar situation on our hands with DNP, but with a double whammy feature - the CEF is overbought from a premium perspective, while the underlying asset class is also overbought via historic high P/E ratios. Overall Utilities is a great, defensive asset class with amazing long term results, but do expect a mean reversion here. As the recession gets priced in and equities start bottoming out, market participants are going to rotate out of defensive stocks (Utilities and Healthcare) into more aggressive names that are now beaten down. We are lightening up on our DNP position now, looking to re-enter the name later in the year at levels -10% to -15% lower than today's price.

For further details see:

DNP: A Golden Utilities CEF, Currently Extremely Overpriced