BBMC - Do Not Cherry-Pick Your Data

Summary

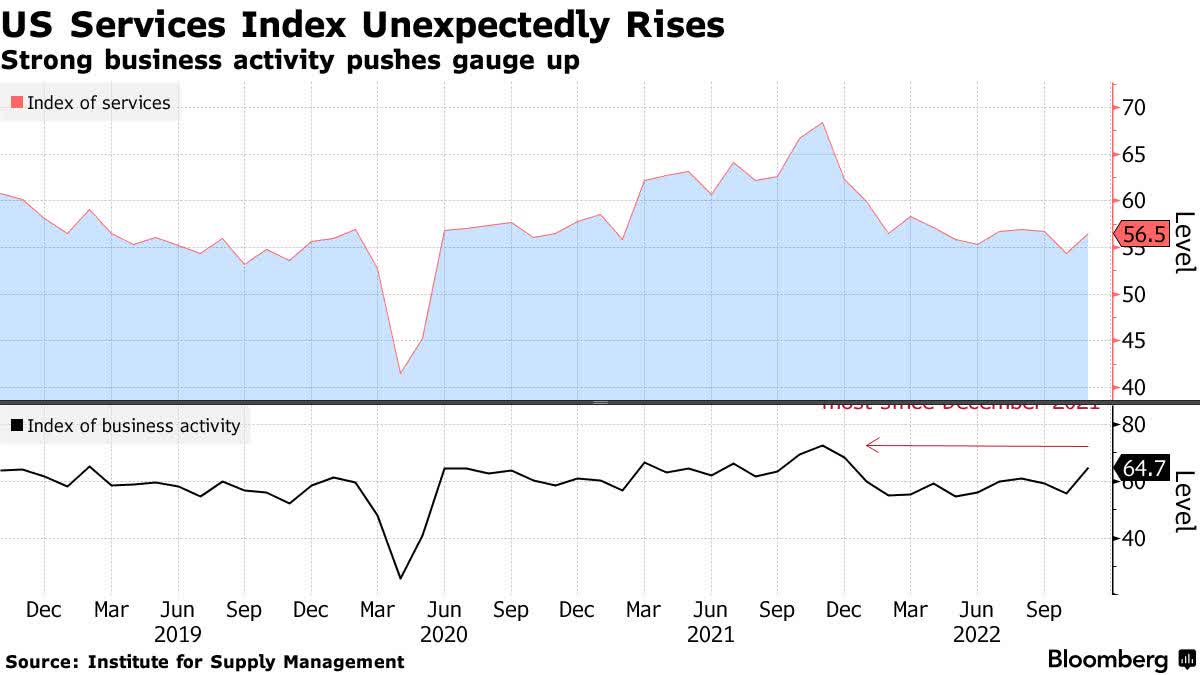

- Yesterday's ISM Services Index for November rose unexpectedly, signaling a rebound in the rate of economic growth.

- That sent bond yields higher and stock prices lower, fueling fears the Fed will raise rates higher for longer.

- Yet the consensus ignored a similar survey from a competitor that signaled a contraction in service sector activity.

- The truth lies somewhere in between, as the data in aggregate shows a slowing but still positive rate of growth.

- Investors should avoid the mistake of cherry picking data to support a specific narrative.

I spent the summer arguing with my critics that our economy was stronger than the consensus perceived it to be to quell recession fears. Now I'm arguing with the same lot that the economy is not as strong as they purport, which is refueling concerns that the Fed will raise rates higher for longer in 2023. If the bears want to draw a negative picture that fits a particular narrative, they can cherry pick the data to do so, but if you consider all of the data in aggregate, it points to a slow but steady rate of growth in the economy, as we start the new year. The path to a soft landing is a very fine line, but I still see it as plausible. Stocks did not agree with me yesterday, as a stronger-than-expected PMI report drove bond yields higher and raised doubts about the less aggressive tone Chairman Powell spoke with last week.

{kind=link}

Last week's jobs report for November was clearly not as strong as initially thought because the household survey showed job losses, but investors focused on the payroll survey's job gains. Investors repeated the same mistake again yesterday when reacting to the purchasing managers index (PMI) for the service sector from the Institute for Supply Management. The bears honed in on the upside surprise in the headline number, ignoring a nearly identical survey from S&P Global that came out minutes earlier.

{kind=link}

Yes, the Institute for Supply Management's measurement of service sector strength rose from 54.4 to 56.5, which was an increase when the consensus was expecting a decrease. The 50 level is the dividing line between growth and contraction. Still, while the business activity sub-index spiked last month, the overall level of strength has been in a downward trend since peaking in September of last year at 65. Furthermore, the delivery times sub-index fell to its lowest level since February of 2020, indicating a significant easing in the supply-chain bottlenecks that have put upward pressure on prices.

S&P Global's PMI survey for the service sector also was released yesterday morning, but it showed a much weaker result, falling further into contractionary territory from a reading of 47.8 to 46.1. This index is in a similar but much steeper downtrend. I saw no mention of this index after the ISM services index was reported. Which one is correct?

S&P Global

There's some truth in both surveys, and I think the sensible thing to do is average them to recognize a service sector that is still growing modestly but at a declining rate. The most important difference between the two surveys is that ISM and S&P Global speak to different companies with different sector weights, which can influence the results. Secondly, they are both diffusion indexes, which means they measure direction (strengthening or weakening) and not magnitude. That means that if one company hired 10 workers, while another fired 100 workers, the two would offset each other because one is strengthening and the other is weakening. Regardless, it comes as no surprise that a Wall Street consensus resoundingly bearish would focus on the ISM and ignore S&P Global. It does not jive with the recession and ongoing bear-market narrative.

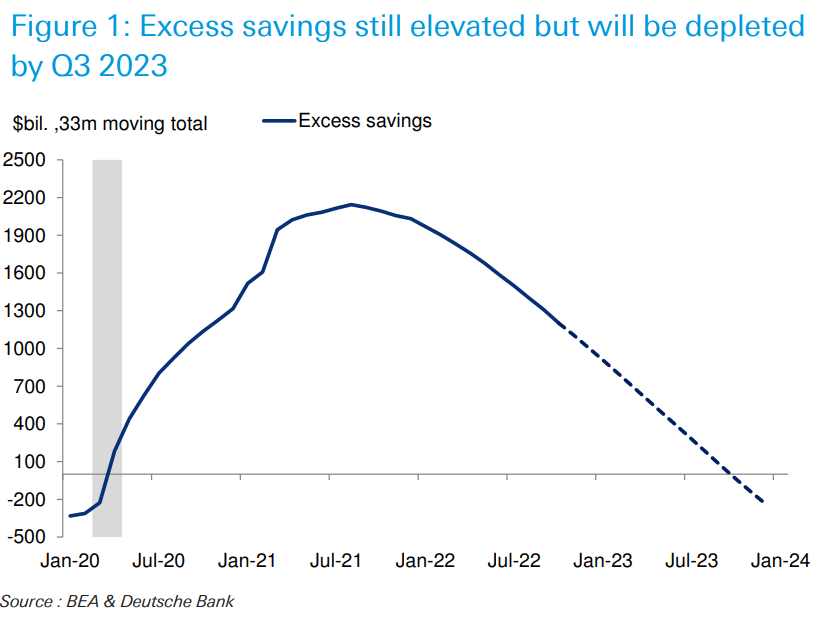

I have discussed repeatedly that this post-pandemic economy is very unusual and difficult to read, because it sends a lot of mixed messages. There are pockets of strength in certain sectors, while others are weakening, due largely to the shift in consumer spending preferences. What most economists also continue to ignore is the mountain of excess savings that still bolsters consumer balance sheets. It has served to offset the temporary increase in prices for goods and services, maintaining very modest real (inflation-adjusted) growth in spending and prolonging this expansion.

{kind=link}

The savings will not last forever, which is an important point for the Fed to remember. The savings rate already has plunged below 3%, and excess savings are projected to fall back to pre-pandemic levels by the end of next year. Yet that's when I project the rate of inflation to fall close to the Fed's target of 2%, resulting in a return to real-wage growth, which should take the baton from excess savings to support real spending growth and avoid recession in 2023.

For further details see:

Do Not Cherry-Pick Your Data