DOCU - DocuSign: The Sales Force May Be Underestimated

2023-12-04 00:10:33 ET

Summary

- DocuSign's stock has declined by 85% from its all-time highs due to post-pandemic revenue slowdown and increased competition.

- Despite challenges, DocuSign maintains a dominant position in the e-signature industry with over 60% market share.

- The company has the potential to reaccelerate growth due to its strong sales force, customer loyalty, and a growing market for e-signatures.

DocuSign ( DOCU ), specializing in electronic agreement and signature technology, gained significant popularity during the COVID-19 pandemic as businesses rapidly digitalized their agreement procedures. However, the company has experienced a roughly 85% decline from its all-time highs, attributed to a post-pandemic slowdown in revenue and increased competition from larger entities like Adobe ( ADBE ), as well as emerging startups.

Despite these challenges, DocuSign's competitive position, robust free cash flow generation, and a growing market for E-Signatures could lead to a potential re-acceleration of growth going forward. The company's beaten-down stock also positions it as a potential takeover target. With its considerable market share and the expanding e-signature and agreement market, DocuSign could be poised for a growth acceleration heading into Q3.

{kind=link}

Statista

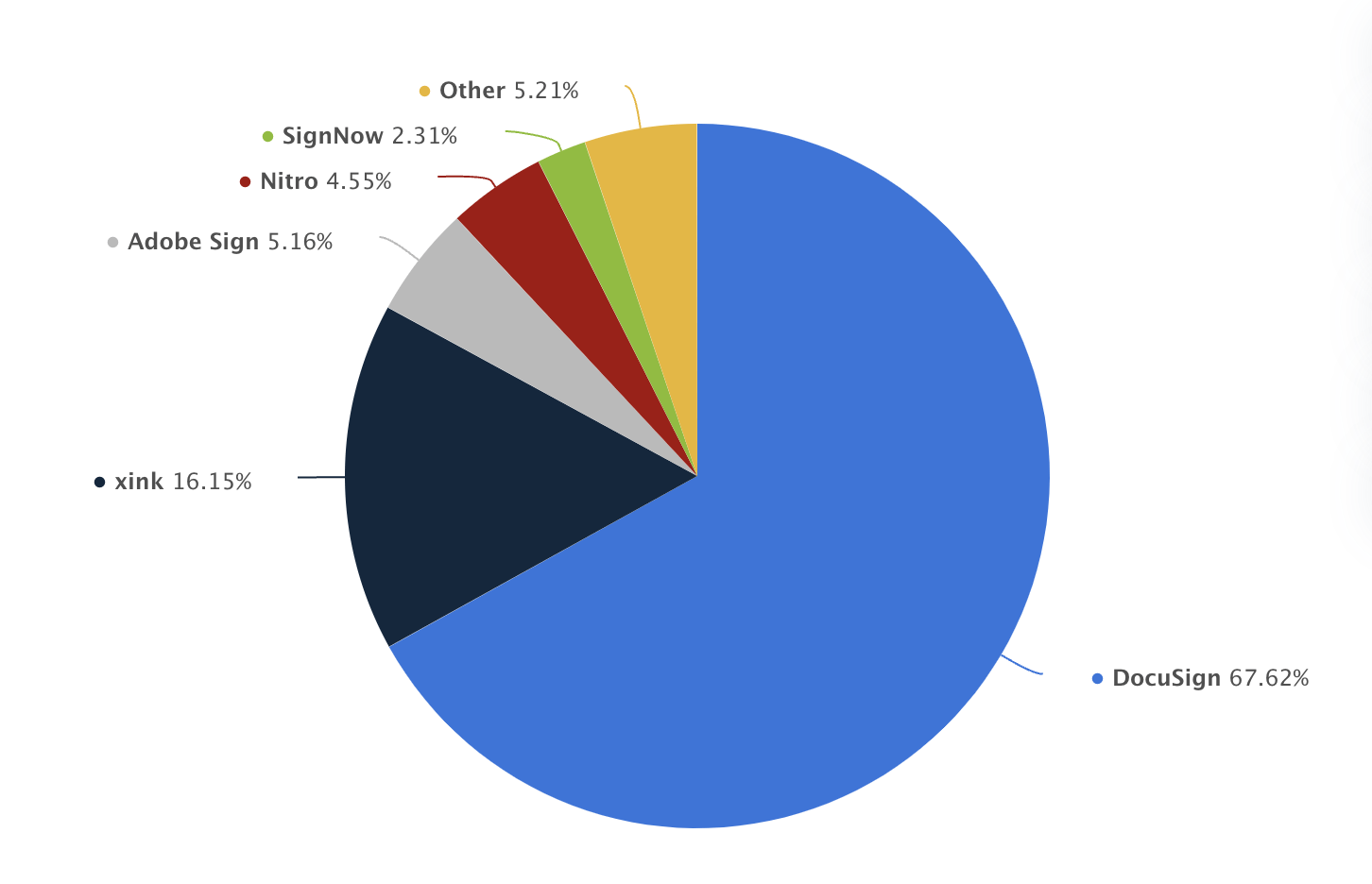

DocuSign continues to lead the e-signature industry with a >60% market share, despite the growing competition from new vendors. The dominant position offers DocuSign considerable brand visibility and customer familiarity, which can be potent advantages in the tech sphere. Even when faced with competitors that might offer lower costs, DocuSign's market presence suggests that current customers could be reluctant to switch providers.

For large enterprises, in particular, the hassle and potential disruption of migrating to a different e-signature service can outweigh the benefits of reduced costs. DocuSign has a strong position in the e-signature market because once customers start using it, they usually stick with it. While its market share slightly dipped from over 70%, this isn't a sign that DocuSign is losing its moat, in my opinion. Its quickly moderating dollar net retention rates toward 100% shouldn't be an issue either, as DocuSign has a long runway in growing its customer base, which it has continued to do in recent quarters.

{kind=link}

Statista

Overall, I believe a large part of its slowing revenue growth can be attributed to pulled-forward demand for e-signatures during the pandemic, which has now moderated as several large customers and small businesses have installed DocuSign's software. Similarly, Adobe also saw a meaningful deceleration of growth from well over 20% to just above 10% as of its latest quarter. However, in contrast to DocuSign, its valuation rebounded sharply over the past year.

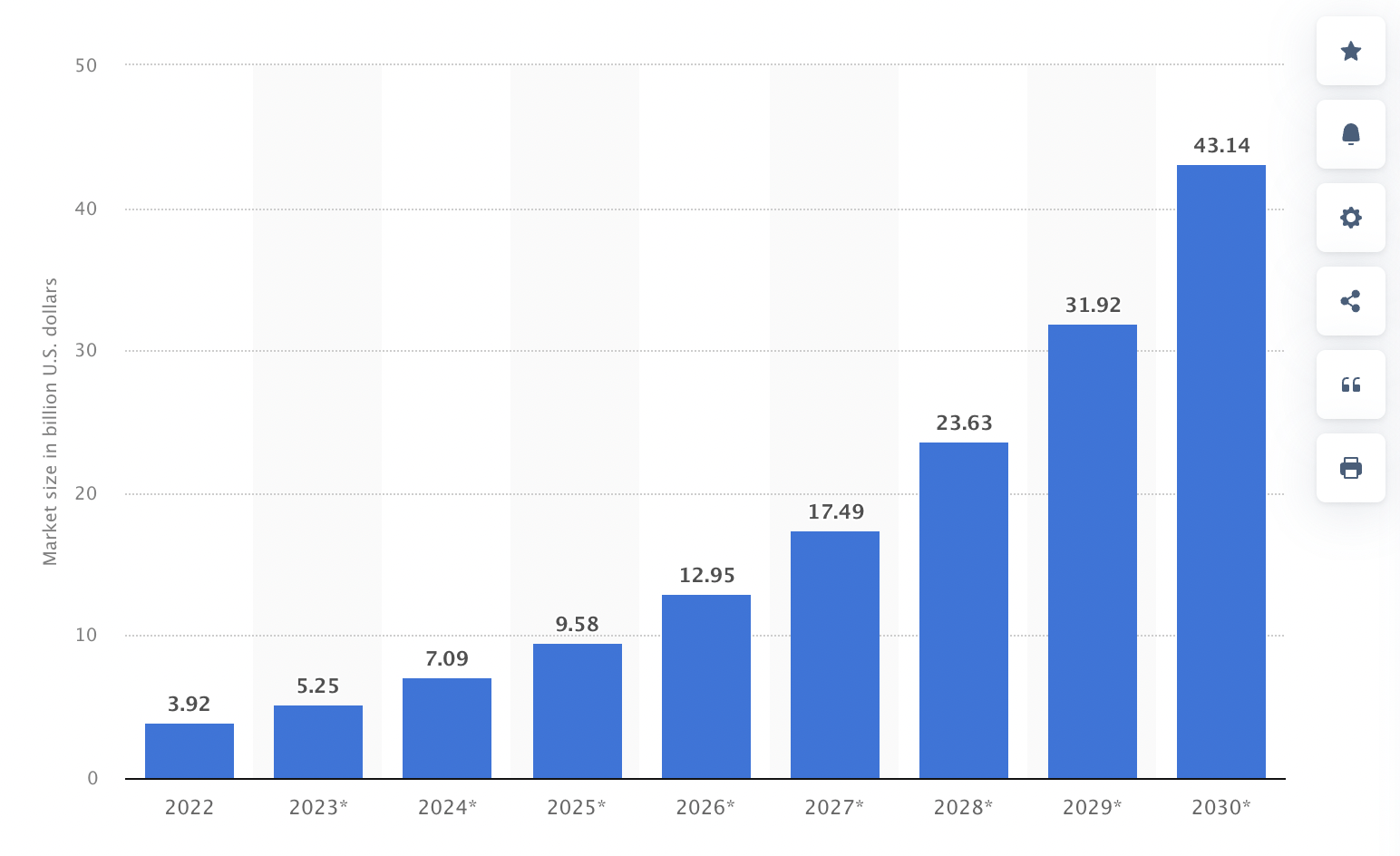

Given the large and growing long-term opportunity for e-signatures and document analysis, DocuSign's runway for growth is still there. With an estimated $50 billion market opportunity by 2030, even just a 30% market share could translate to $10 billion in annual revenues. With current free cash flow margins of around 30%, this could potentially translate into $3 billion in annual cash flows.

Valuation

As DocuSign's growth substantially dropped over the last few quarters, it can be compared to other pandemic darlings such as Zoom Video Communications ( ZM ), Twilio ( TWLO ), and Pinterest ( PINS ). These companies hold similar free cash flow margins and growth rates.

Although Adobe demands a three times higher valuation than DocuSign, Adobe arguably deserves a higher premium due to its more diversified business, larger scale, greater free cash flow margins, and a higher moat due to more offerings. Nevertheless, the two are somewhat similar in their growth rates, as DocuSign still has greater room to expand in terms of its revenue and margins. Here, DocuSign even trades at a lower valuation than Zoom and Dropbox ( DBX ), which have much lower growth rates.

| Company |

| Levered Free Cash Flow margin ((TTM)) |

| Market Cap. |

| Employees |

| Market Cap. / Employees |

| Adobe ( ADBE ) |

| 40% |

| $288 billion |

| 29,239 |

| 9.85M |

| CrowdStrike ( CRWD ) |

| 32% |

| $56 billion |

| 7,745 |

| 7.2M |

| Dropbox ( DBX ) |

| 31% |

| $10 billion |

| 3,118 |

| 3.2M |

| Zoom Video ( ZM ) |

| 29% |

| $21 billion |

| 8,484 |

| 2.5M |

| Zscaler ( ZS ) |

| 28% |

| $29 billion |

| 5,962 |

| 4.9M |

| Snowflake ( SNOW ) |

| 27% |

| $61 billion |

| 5,884 |

| 10.4M |

| Datadog ( DDOG ) |

| 26% |

| $39 billion |

| 4,800 |

| 8.1M |

| Workday ( WDAY ) |

| 23% |

| $72 billion |

| 18,369 |

| 3.9M |

| DocuSign ( DOCU ) |

| 21% |

| $9 billion |

| 6,748 |

| 1.33M |

| UiPath ( PATH ) |

| 15% |

| $14 billion |

| 3,833 |

| 3.7M |

| Elastic ( ESTC ) |

| 7% |

| $11 billion |

| 2,866 |

| 3.8M |

As demonstrated in the table above, DocuSign's value per employee is amongst the lowest in the software sector with comparable free cash flow margins. Although companies like CrowdStrike hold high free cash flow margins and higher growth rates on a trailing 12-month basis, DocuSign's free cash flow margins have improved substantially over past quarters and reached over 30% in its last two quarters.

Therefore, its relatively low value per employee compared to software stocks like Dropbox suggests that DocuSign may be undervalued. While it can be argued that the value per employee is even lower for companies such as RingCentral ( RNG ) or Teladoc Health ( TDOC ) with values per employee of less than $1 million, they hold significantly lower free cash flow margins. Thus, it is difficult to find software companies with comparable growth rates and free cash flow margins trading at such low multiples.

{kind=link}

DocuSign

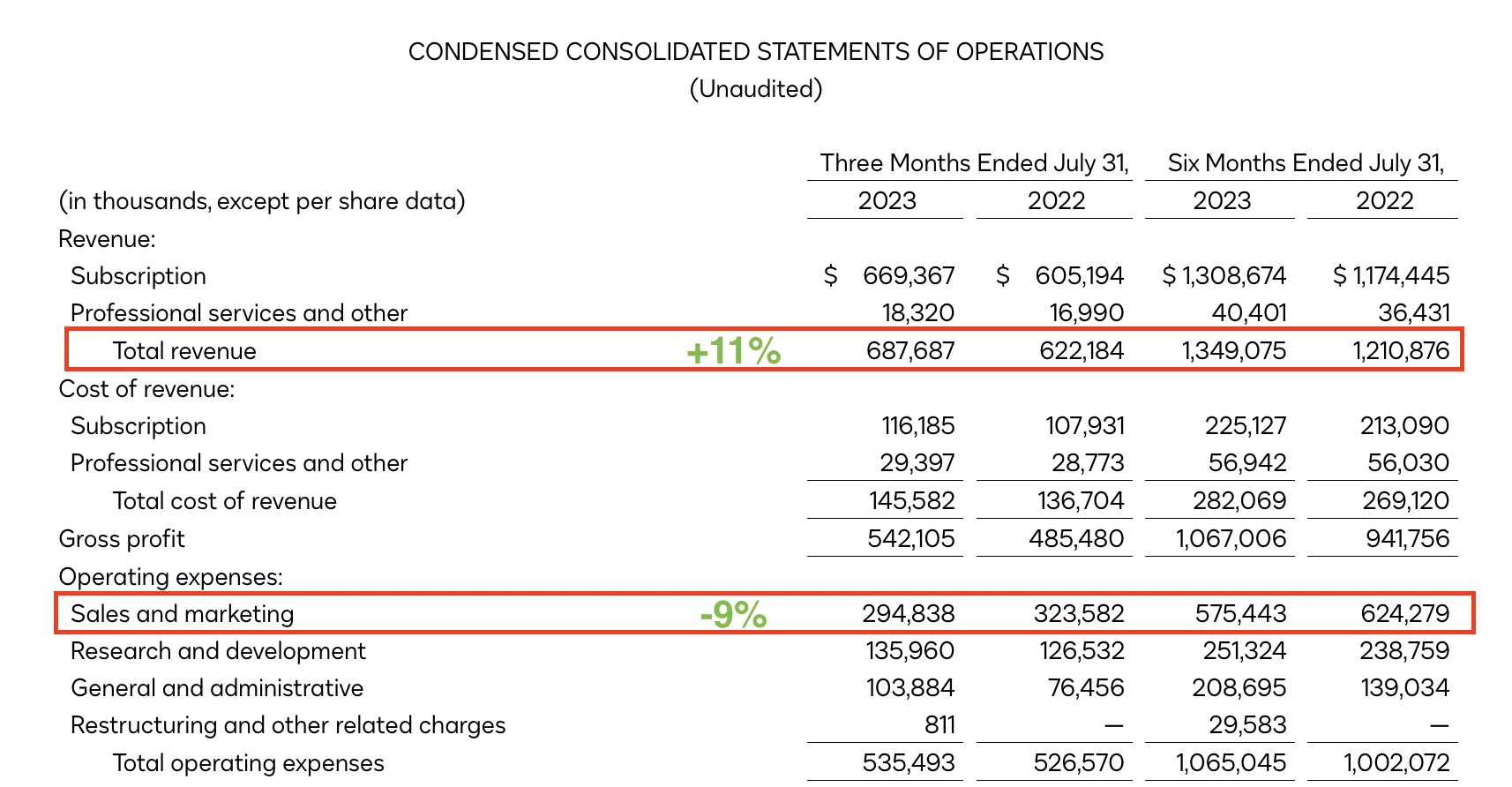

Having a strong sales force is arguably one of the most important factors to drive profitable growth for software products. DocuSign's large headcount of just under 7000 employees gives the company a strong presence and ability to sell. Its strong sales force will likely continue to drive growth in less saturated markets, as seen by its strong international growth in recent quarters. While international revenue grew 17% last quarter, it makes up only 25% of DocuSign's total revenue and will likely serve as a key catalyst to drive growth going forward.

It's important to note that while its revenue decelerated, DocuSign also substantially cut its marketing spend as it is focusing on profitability. If revenue growth saw a similar decline to its marketing spend, this would likely be worrying, but DocuSign is demonstrating its ability to drive organic growth.

Overall, I believe DocuSign's cost-cutting efforts will show in its bottom-line earnings in Q3. As software peers such as UiPath ( PATH ) and Elastic ( ESTC ) showed a reacceleration of growth in recent quarters, DocuSign could potentially see a similar reacceleration.

Takeaways

DocuSign still holds the crown for the largest market share in the market, which is set to continue growing quickly over the next decade. Despite experiencing a slowdown in growth, the company's strong underlying profitability shouldn't be overlooked. Its strong financial foundation not only supports potential inorganic growth but also opens the door for shareholder-friendly moves like share buybacks.

DocuSign's competitive market position and robust profitability seem somewhat underappreciated, especially with regard to its valuation, at just over three times its annual sales. In my opinion, its current valuation offers a margin of safety, as opposed to its pandemic highs.

Furthermore, the potential of DocuSign's extensive salesforce shouldn't be overlooked. This significant asset could be the key to driving customer growth, potentially leading to a surge in billings heading into Q3 and beyond. Furthermore, due to its beaten-down valuation, DocuSign could be a potential acquisition target for companies such as Salesforce ( CRM ) or SAP ( SAP ).

Nonetheless, there are potential risks with DocuSign. One significant risk is a potential erosion of its market share, especially with Adobe and other competitors aggressively expanding their foothold in the e-signature sector. Should the company's growth rates continue to decelerate, DocuSign's valuation could further be reevaluated based on its profitability. Nevertheless, if DocuSign can successfully address these concerns, shares could have upside potential beyond Q3.

For further details see:

DocuSign: The Sales Force May Be Underestimated