DLB - Dolby: An Unwarranted RoR Stretches Valuation Further

2023-04-12 05:20:05 ET

Summary

- I've written about Dolby Labs a few times over the past few years. It's a stock I'd love owning - but a stock that, unfortunately, is always relatively expensive.

- This is also in the context of the broader market and other stocks we're taking a look at. Dolby is simply expensive for what it is, and what it offers.

- The recent set of market outperformance - over 8% - has further made this a stance I now consider to be even more valid.

Dear readers/subscribers,

It's not easy to be exactly negative on a company that essentially owns the patents that make large parts of our global audio and other parts work, as it were - but I believe any investment made should be able to generate alpha on a medium or long-term basis. I continue to believe that Dolby ( DLB ) is a solid investment at the right price, with exactly this ability - but I do not believe the company is currently at or close to that valuation.

My price target for DLB stock in my last article was around $70/share. I am not changing this target for this article or going forward into 2023.

In this article I will show you why.

Updating for Dolby Labs for 2023

17 years do not necessarily make for a market-beating company - but 17 years of market-leading patent ownership in the areas of analog and digital noise reduction, encoding, compression, Audio and Video processing, and digital cinema, does make for a potential market leader here.

The market leader might be the somewhat strong language for what Dolby presents here. By most accounts, Dolby is being compared to business service companies, a segment where Dolby is better than average in most respects in terms of profitability, but not all. Perhaps what I want to showcase is that compared to Dolby's own historical numbers, is that margins are actually growing less as we move forward. Dolby is still profitable and excellent, but the company is not a market leader in RoE, and most of the margin KPIs versus its history is declining (Source: GuruFocus).

The company does, however, have market leadership in other crucial segments. Take the company's financial strength for instance, where we look at things like cash, debt, interest coverage, and so forth - here, the company consistently scores in the 90th percentile in its coverage spectrum. Taking those indicators, profitability together with financial strength, are the company's two main selling points here.

Why those two? Well, Growth isn't really a thing for Dolby - at least not that much. The 3-year revenue growth rate is less than 2%, which is less than average, and its overall valuations in terms of P/E, EV, and others aren't really that good. So growth and valuation is the problems for this company - but we knew that already, it's what I've been talking about in the last articles on the company.

Licensing is a great business model - if you're fine with a small, slightly growing stream of revenues. The composition in turn of these licensing fees comes mostly from broadcast- meaning television and the like, as well as mobile licensing.

Dolby IR (Dolby IR)

The latest set of results we have are the 1Q23 ones - and these were presented about two months back. Revenue for that quarter was down by about $15M, GAAP net was nearly flat, but slightly up on a diluted EPS basis, or slightly up on a non-GAAP basis.

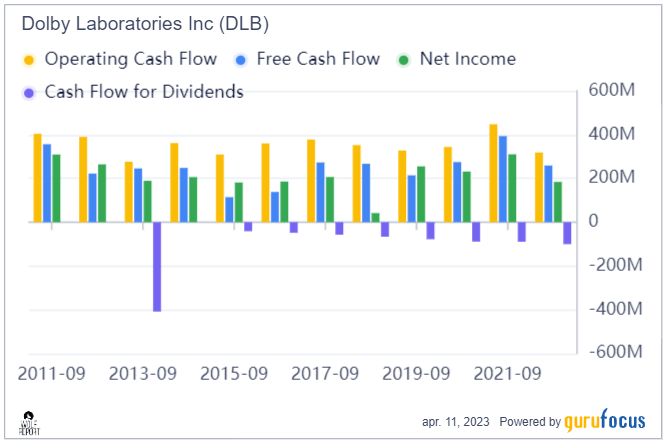

Company cash flows continued to show strength in relation to the historical trends for Dolby.

{kind=link}

The company recently, back in 2022, did a significant amount of buybacks. OCF has turned around somewhat in 1Q23, with over $50M for the first quarter, up more than 50% from 1Q22. Buybacks continued during this first quarter, and Dolby ended with a net buyback of 700,000 shares for the first quarter, which still leaves over $300M worth of buyback authorizations going forward.

Operational highlights for the company include new launches of flagship products with Dolby Vision technology, such as the Vivo Phone, the OPPO OnePlus 11, and TCL announcing that Dolby Vision and Atmos will not only be included but included on all 4K TVs in the US market.

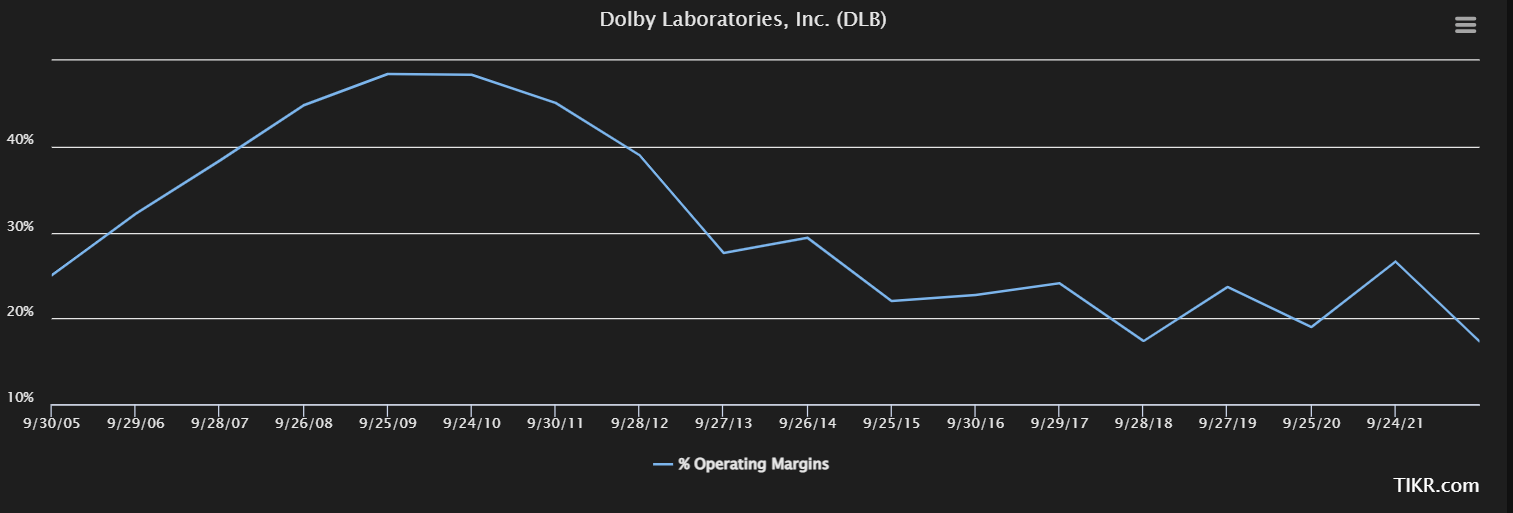

However, this is unlikely to change the near-term growth prospects for Dolby going forward. The company is still a royalty-based business, and income/revenue changes in these models are limited. Company revenue forecasts are at about low single digits YoY, with OpEx in slight decline, while non-GAAP OpEx is expected to climb about the same amount, so about the same. Company operating margins are, unfortunately, in slow decline, and are not expected to climb above 20% in the near term.

{kind=link}

The expected OM level for the company goes no higher than 19% for the coming 2023E fiscal, and this is by the company's own reckoning.

Dolby remains in a strong position for its business. With 13,200 patents and another 4,000+ patents pending, the company has no shortage of patent appeal, nor expiration worries. This is because expirations are tiered, and the earliest relevant ones are in May 2045 - a long time in the future, and at least a quarter-century more of completely exclusive business for the company. This is the very definition of a moat, as I see it.

Of course, a moat is really only as good as the company's appeal is in terms of valuation - at least during any one specific point in time. And as things currently stand, this is not in a great position. More on that in a while.

For the time being, there is positivity in the fact that the technologies Dolby offers are either actually mandated, or informally mandated in most streaming services including North America.

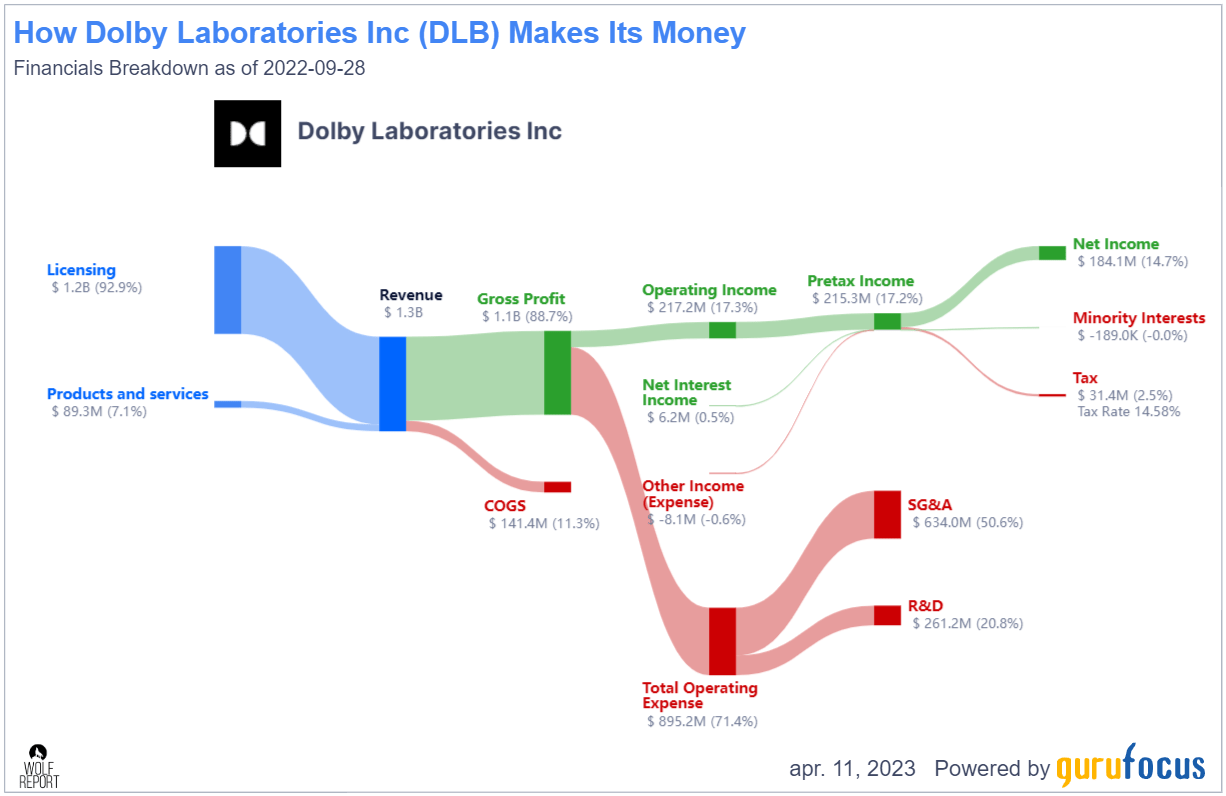

Worries and focus points for Dolby? Look at the company's revenue growth estimates, specifically long-term growth, and how slowly it's being expected to expand. While the underlying demand is solid - content continues to be more immersive and engaging, and this is helping with the fundamental appeal for Dolby - there exist several makers of electronics that do not use Dolby. This highlights the need to continue to look at first the number of customers Dolby is successfully acquiring, but also the cost of those customers which they are acquiring, which is expressed through the company's COGS and other costs - though as you can see, as things are structured, it's mostly OpEx when it comes to Dolby.

Dolby Revenue/income (GuruFocus)

{kind=link}

Overall, I see Dolby as attractive at the right price - but the company simply won't drop to those levels.

Let's look at company valuation here.

Dolby's Valuation - less attractive than before, the upside is limited

I would go ahead and say that Dolby is what I would consider being "fairly" valued, or without much potential to the upside. The company's valuation in terms of P/E is now at almost 41x P/E normalized, which is a prohibitive valuation for any company - I don't care if it's a company like Louis Vuitton ( OTCPK:LVMUY ), it's not worth 40x+ P/E.

Dolby has no more than a 1.28% yield, and while there is potential for earnings growth, I do not see the earnings growth that forecasts are accurate, seeing here of almost 25% annually going forward to 2025E. I base this on the fact that FactSet analysts are wrong negatively (meaning lower earnings) 50% of the time even with a high, 20% margin of error. Dolby has the potential for some volatility.

Analyst averages in terms of forecasts here are based on a price target range starting at $90 on the low side and $116 on the high side - these analysts have a consistent history of overestimating this company by about 20-40% over the past 2-5 years, on the basis of Dolby's extremely qualitative portfolio of patents.

Only 3 analysts from S&P Global follow Dolby - but 2 of them are "BUY", and only 1 "HOLD", with an average PT of $95/share.

I consider this to be far too positive and would discount Dolby by at least 20% to find a good price target. As it stands, that still puts me at $70/share PT. It's the simple fact, as I see it, that analysts are continually too positive. I do not, based on current sales trends and cost trends, believe that Dolby has the ability to increase earnings. This is due to cost increases (margins are decreasing, that's a proven trend over the past 10 years) not making up for the revenue/sales volume. This means that at best, I expect a lower, single-digit earnings growth rate and a single-digit EPS growth rate with a sub-2% yield that isn't worth 40x P/E.

In fact, anything above 30x P/E is not something I'd go for here. For 2023E, even with an EPS growth to $2.3 adjusted, that implies a 30x P/E valuation of just around $70/share - and that is the rationale for my current valuation.

I don't see any potential for a significant upside beyond this - if anything, I see reasons to assume things are actually going to be turning out worse, not better, due to the trend of declining margins.

For that reason, and for the other reasons mentioned here, I wouldn't consider those trends or this company to be anything close to fairly valued or interesting here, and I would consider the company a firm "HOLD" here.

The following is my thesis.

Thesis

- Dolby is a fundamentally sound, well-run company with a solid moat. It lacks the usual dividend safety and tradition as well as credit rating, but its portfolio of patents makes for revenue security for the next few decades. I view it as a sound investment at the right price - but the right price is way off at this time.

- Given the company's moat and premiums, I consider 20-25X P/E to be valid for Dolby, but 15-18x P/E to be a preferable one. The highest I would consider under any circumstance is just around 30x P/E.

- This calls for a current 2022E share price of $70 and a 2024E share price of $80, making the company overvalued and a "HOLD" here, as of April of 2023.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is yet to fulfill a single one of my criteria which is why I view it as a "Hold" here.

For further details see:

Dolby: An Unwarranted RoR Stretches Valuation Further