DLB - Dolby Laboratories: Atmos And Vision Growth Yet Fairly Valued

2023-12-06 10:41:05 ET

Summary

- DLB reported strong 4Q23 and full-year 2023 results, with growth in licensing revenue which forms the lion's share of its total revenue.

- DLB's growth is expected to be boosted by the recovery of the automotive industry.

- Growth potential in licensing revenue linked to rising adoption of Dolby Atmos and Vision technologies.

Synopsis

Dolby Laboratories (DLB) specializes in developing audio and imaging technologies for a broad range of applications, including cinema, TV, broadcast, home entertainment, and mobile devices.

Overall, I am recommending a hold rating for DLB. My decision stems from my conservative DCF, which indicates that DLB is currently fairly valued. Despite DLB reporting robust 4Q23 and full-year 2023 results, highlighted by growth in licensing revenue and the anticipated further growth driven by its Atmos and Vision software, it currently lacks a sufficient margin of safety. I usually recommend a margin of at least 15% but its current share price lacks it. Therefore, the combination of my DCF and the lack of an adequate margin of safety leads me to recommend a hold rating.

Historical Financial Performance

Over the past four years, DLB's revenue growth has fluctuated due to its business being impacted by rising inflation and the COVID pandemic. This stems from the simple fact that DLB's software operates in the entertainment sector, such as cinemas or in-home entertainment. With the COVID lockdown, the cinema market took a big hit, and it has had a direct impact on DLB. On the other hand, high inflation will deter consumer spending on non-essential items such as devices or streaming services. Hence, it also has a direct impact on them.

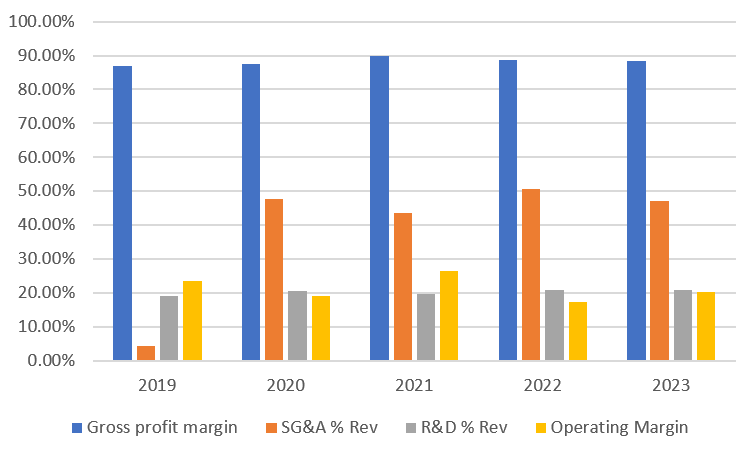

In 2020, revenue was down 6.43% , then went back up in 2021 to 10.28% when COVID subsided. In 2022, it went down by 2.14% and back up by 3.66% in 2023. Therefore, when we look at its CAGR, it will give a moderated view of its annual growth rate. Its 5-year CAGR is ~0.9%. In my opinion, this is quite low for a company that spends quite a large portion of its revenue on R&D and SG&A. As you can see, DLB actually has a very commanding gross profit that averages ~88%. However, its operating margin is only ~20%. This means that it is spending heavily on SG&A and R&D, with SG&A doubling R&D. With such aggressive selling and research development, I would expect DLB's growth to be higher, but its revenue's 5-year CAGR is almost near 0%.

{kind=link}

Moving onto its balance sheet, it is looking really strong. Its debt/equity ratio is almost negligible. It averages about ~2% in the last half decade. As a result, interest expense doesn't pose any risk to its margins at all.

Author's Chart

Strong 4Q23 and Full Year 2023 Results

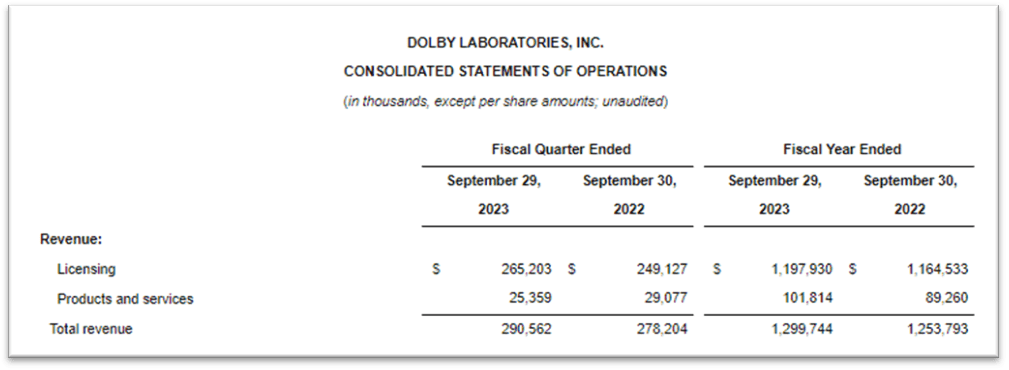

For DLB's 4Q23 results, it reported total revenue of $290.6 million, which represents a growth of ~4% year-over-year. Looking at the segment level, its licensing revenue grew 6% year-over-year to $265 million. Its segment revenue [product & services] declined 13% year-over-year to $25 million, as a result of lower volume in cinema related sales. Although 13% might sound worrying, when we look at its revenue segment weightage, it is clear that licensing, which accounts for ~92% of its total revenue, forms the lion's share and is growing.

{kind=link}

In terms of profitability, DLB also reported strong results. If excluding a restructuring charge of approximately $30 million, net income was $63.9 million or grew 21% year-over-year. Cash flow from operation grew ~65% year-over-year. As 4Q23 is also its financial year end, DLB also reported its full-year 2023 results. Total revenue also grew by 4% to $1.30 billion. Net income grew 8.7% year-over-year. Its cash flow from operation grew ~15%.

Core Audio Technologies Bolstered by Growth Potential in Dolby Atmos and Vision

About ~92% of DLB's revenue comes from licenses, and its audio codecs and audio patent licensing account for about two-thirds of its licensing revenue. This shows that DLB has a strong base in the audio market. With constant innovation, DLB is solidifying its position as a leading provider of audio technologies, which have widespread adoption across various devices and end markets. Hence, I believe its innovation initiative, coupled with its strong market positioning in audio technology, will bolster its future growth outlook.

On the other hand, Dolby Atmos and Dolby Vision make up the bulk of its remaining licensing revenue. Both new technologies are in the early stages of being accepted and integrated into products by manufacturers and content creators, compared to its more established audio technologies. This means that new licensees and increased adoption from existing partners are the primary drivers of its growth potential.

So far, its Dolby Vision technology, which enables people to make and share high-quality videos, has seen increased adoption and use in sports broadcasting. This widespread use of Dolby Atmos and Dolby Vision in different types of content is making them a popular choice in the industry. Management believes this growing popularity will help them form more partnerships with companies that make devices like TVs and smartphones, leading to more growth for DLB in the future. This can be evident in its wins with companies such as TCL and LG .

During the quarter, DLB reported that its Atmos and Vision grew 20% year-over-year with anticipation that it would continue to grow at a CAGR of 20% at the midpoint of its guidance. From its current results and management's optimistic guidance, it shows a lot of strength in the growth potential of both softwares. Hence, it leads me to believe that both softwares are set to bolster its licensing revenue, especially when they account for one-third of licensing revenue.

Automotive Industry Recovery Poised to Bolster DLB Growth

During the quarter, DLB also scored a major agreement with BYD Company Limited ( BYDDF ), a publicly listed Chinese conglomerate. In addition to BYD, it also has a win with Mercedes-Benz ( MBGAF ). Ever since the COVID pandemic, the automotive market has been hammered with falling demand due to lockdown. In addition, the global chip shortage also resulted in a production halt.

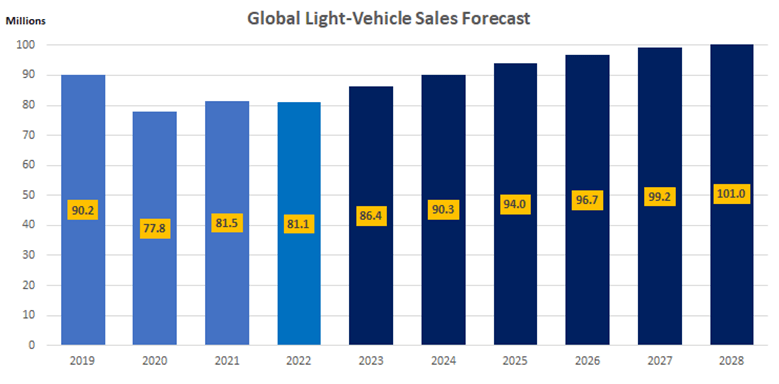

As a result, there is a lot of pent-up demand for motor vehicles, which is aiding in the recovery of vehicle sales. As you can see from the chart below, sales dropped by ~13.7% in 2020, and ever since, they have been on a recovery path. By 2024, it is expected to reach pre-pandemic levels and will continue to grow until 2028, reaching $101 million.

Hence, I believe its recent win with BYD and collaboration with other car manufacturers, such as Mercedes, is going to bolster DLB's future growth outlook as global vehicle sales continue to grow. A little fun fact: the Mercedes-Dolby Atmos sound system won the Autoblog Technology of the Year award just a few days ago. This accomplishment, although subtle and small, speaks volumes in regard to DLB's software. In addition, such an accomplishment will set DLB as the go-to company when it comes to vehicle audio systems, giving them a good head start as well as securing their market leadership in this growing market.

{kind=link}

Valuation

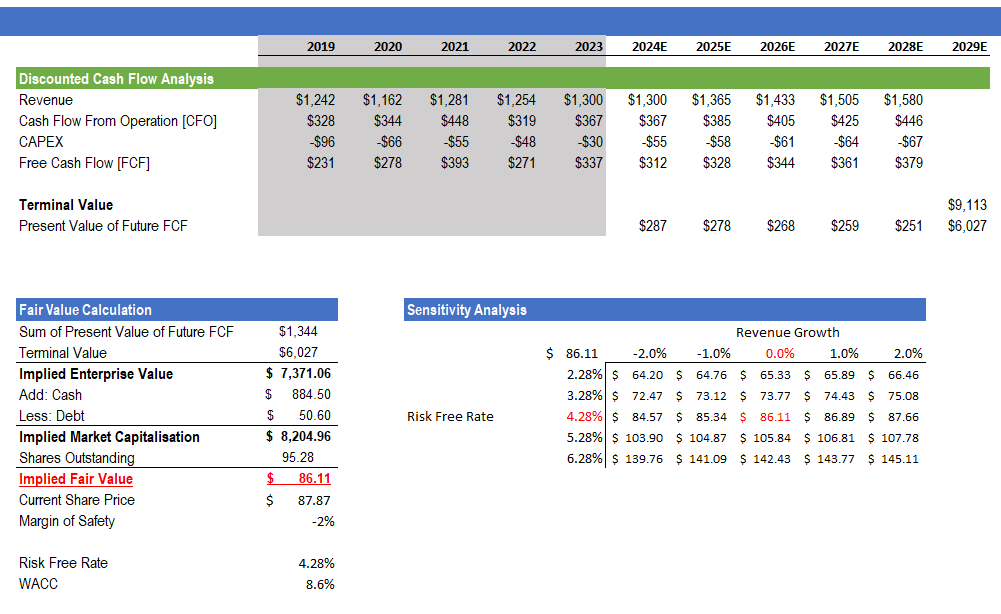

In order to determine the intrinsic value of DLB, I will be using a simplified 5-year DCF model with a terminal value [TV] exit. My model's implied intrinsic value will give us a snapshot of its current valuation and determine if it is over, under, or fairly valued.

{kind=link}

DLB's revenue growth for 2024 and 2025 is expected to be flat and approximately 5% growth, respectively, in line with market expectations as well as management guidance. These growth estimates, which I find to be reasonable, are supported by DLB's strong 4Q23 and full-year 2023 results, growth in Dolby Atmos and Vision, and the anticipated recovery in the automotive market-all of which I have covered in detail above. I anticipate growth rates for 2026-2028 to roughly match growth projections for 2025. As such, for these remaining years, my model uses approximately 5%, and I believe this to be conservative.

The 5-year median CFO as a percentage of revenue is approximately 28%, and I used that in my model for the following 5 years. For its CAPEX, its 5-year median was approximately 15% of its total revenue, and I used this rate for the next 5 years. I believe this keeps my CFO assumption conservative. CFO minus CAPEX will give us FCF. With these, I am able to forecast DLB's next 5 years FCF.

Next, I will use the Gordon Growth formula to determine its TV. The US 10-year Treasury yield current sits at 4.28%, and this will be used as my model's risk-free rate. Using 2028's FCF, a WACC of 8.6%, and a risk-free rate of 4.28%, and applying them to the formula, DLB's TV is calculated to be $9.113 billion.

Using DLB's WACC of 8.6% to discount its future FCF and TV, its implied present enterprise value is $7.371 billion. Based on my conservative assumptions, my DCF's implied intrinsic value for DLB is $86.11. Compared to its last traded price of $87.87, they are almost in line. As my DCF model indicates that DLB is fairly valued, I recommend a hold rating for the stock, despite my acknowledgment that it is a stock with a positive outlook.

{kind=link}

Risk

If the increasing adoption of DLB's technologies drives better than expected results for the next quarter, we might see an upward revision to its revenue growth outlook. If that happens, its implied fair value will increase, as you can see under my sensitivity analysis under valuation. With just a 2% revision to its 2024E growth outlook, it could move my target share price from $86.11 to $87.66, assuming the risk-free rate remains the same.

Conclusion

In conclusion, DLB reported strong 4Q23 and full-year 2023 financial results, where its revenue, net income, and cash flow from operations grew. To top it off, its licensing segment, which accounts for ~92% of its total revenue, also grew. In addition, I believe the anticipated growth potential of Atmos and Vision will definitely further bolster its Core Audio Technologies revenue. Lastly, I believe the anticipated recovery in the automotive market will also bolster DLB's growth outlook, as it is starting to anchor itself as the go-to leader for in-car audio. However, my conservative DCF model indicates that DLB is currently fairly valued. With a lack of margin of safety, which I usually recommend at least 15%, I am recommending a hold rating for DLB.

For further details see:

Dolby Laboratories: Atmos And Vision Growth, Yet Fairly Valued