DLB - Dolby Laboratories: Economic Moat Meets Slow Growth

2023-06-23 11:10:20 ET

Summary

- Dolby Laboratories is a company specialized in audio noise reduction, audio encoding, and compression as well as HDR imaging.

- While Dolby Laboratories has an economic moat based on patents and switching costs, the company has been struggling in the last few years to grow.

- The stock might be fairly valued at this point, but I would be cautious and do not see Dolby Laboratories as a great investment.

A few days ago, I published my first article about Brookfield Asset Management ( BAM ) and mentioned the podcast "Business Breakdowns" which has provided a good list of high-quality companies that might have a wide economic moat around the business. Another company I identify that way is Dolby Laboratories ( DLB ).

In the article, we will describe the business model of Dolby Laboratories, explain why the business has a wide economic moat, and answer the question of if the stock is a good investment at this point.

Business Description

Dolby Laboratories (also known as Dolby Labs or Dolby) was founded in London in 1965 by Ray Dolby. Four years later, in 1969 he filed his first U.S. patent for the Dolby Noise Reduction System. Today, the company is specialized in audio noise reduction, audio encoding and compression as well as HDR imaging. Dolby Labs is best known - among others - for Dolby Atmos and Dolby Surround. Additionally, Dolby is offering its Dolby Cinema - a premium cinema experience that makes it a direct competitor to IMAX Corporation ( IMAX ). Today the company, which had its IPO in February 2005 and is headquartered in San Francisco, has about 2,300 employees.

Dolby is generating most of its revenue by licensing its technologies to consumer electronics manufacturers. The second source of revenue is "Product and Services" however this segment is only responsible for 7% of revenue in the last few years.

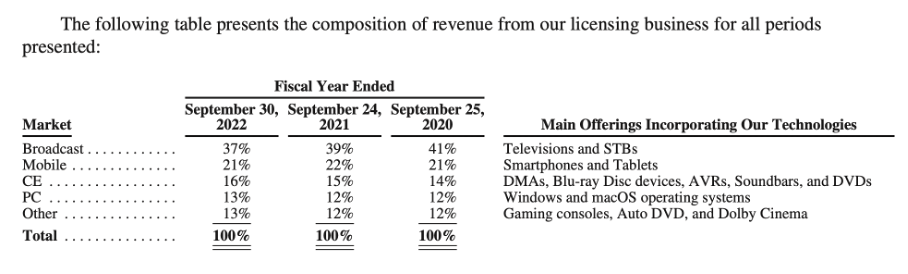

When looking at the licensing revenue in more detail, Dolby is generating its revenue in different ways. The biggest part of licensing revenue is generated by the "Broadcast" market, which includes television and set-top-box [STB]. In 2022, Dolby Labs generated 37% of its licensing revenue here. The second biggest segment was "Mobile" which was responsible for 21% of revenue and is including smartphones and tablets. The other three segments - CE (including for example Blu-Ray and DVD), PC (including Windows and macOS operating systems) and "Other" (including for example gaming consoles) - generated between 13% and 16% each.

Dolby Laboratories Annual Report 2022

{kind=link}

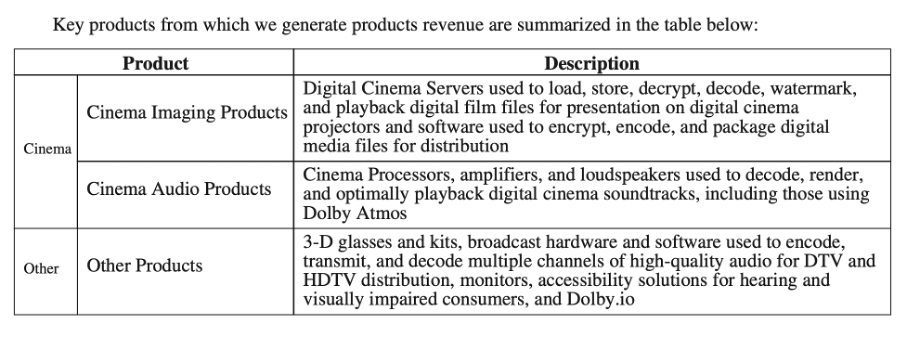

Additionally, Dolby Laboratories is generating revenue from products and services. These include the developer platform Dolby.io and key product offerings especially for cinema.

Dolby Laboratories Annual Report 2022

{kind=link}

Although Dolby Laboratories is a U.S. business, it is generating about two-thirds of its revenue outside of the United States. This is rather untypical for U.S. businesses as most of them generate the biggest part of revenue inside the United States.

Economic Moat

To be honest, when I first read the name Dolby Laboratories, I imagined a company producing laboratory equipment - like Waters Corporation ( WAT ). It took a few minutes before I realized that I know Dolby - followed by the realization that almost everybody knows Dolby. It is one of the names and brands almost everybody that listens to music or goes to the cinema has heard (and not really thought about it again). But the name is probably "stored" in our brain as synonymous with great sound and this is generating a wide economic moat around the business.

One source of economic moat are certainly the patents . According to its last annual report, the company has approximately 16,900 issued patents and approximately 4,100 pending patent applications throughout the world. Of course, some patents have already expired, and the current patents will expire at some point till December 2046, but I could not get more specific information.

A second source for the moat are the switching costs that arise from the fact that Dolby is deeply embedded in the music and film industry. Over the last few decades, many Dolby technologies have been adopted by many important players in the industry and have therefore become an industry standard for broadcast or streaming. Once a technology has become the standard and adopted by content creators as well as the manufacturer of the devices, it is extremely difficult to change that. And the fact that Dolby licensing costs represent only a fraction of the product's total costs (a Hollywood blockbuster for example) is also increasing switching costs as companies will seldom switch just to save a few bucks. The above-mentioned podcast also does a great job to describe the competitive advantage of Dolby Laboratories.

I don't want to question that Dolby Laboratories has an economic moat around its business. However, when looking at some of the metrics, the picture presented is not the best. Let's start by looking at the performance of Dolby Laboratories compared to the S&P 500, and we can see that the S&P 500 slightly outperformed in the last almost two decades. I don't want to call the performance of Dolby Laboratories terrible, but based on the stock performance we must question the economic moat a little bit.

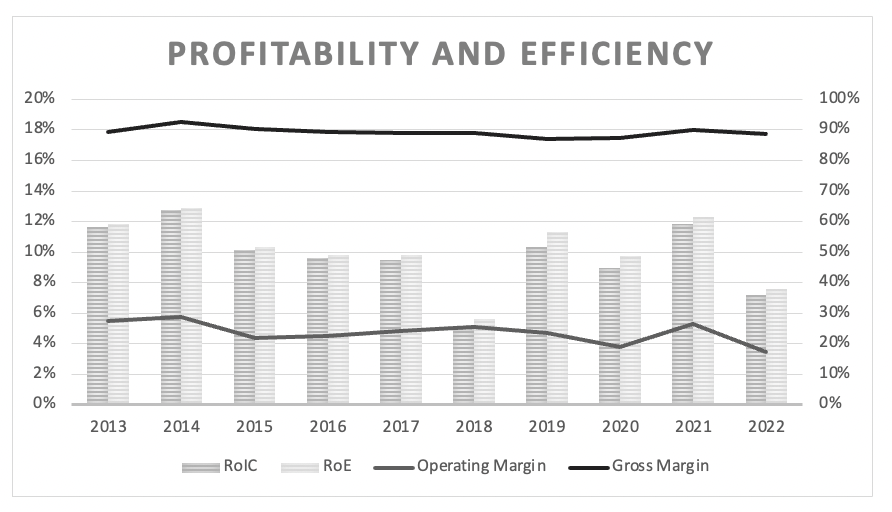

Aside from the stock performance, especially the gross and operating margins can indicate a wide economic moat. And while high margins are great, it is more the stability and consistency over time that is important for a wide economic moat. When looking at the company's gross margin we see not only an extremely high number (close to 90% during the last decade) but also a very stable margin over time which is a good sign that Dolby Labs has pricing power. The operating margin is fluctuating a little more, but overall, I could call the margins stable.

Dolby Laboratories Margins and RoIC (Author's work)

{kind=link}

Additionally, we can look at return on invested capital as an important metric for a wide economic moat. A rule of thumb is a return on invested capital above 10% over a longer timeframe as indication for a wide economic moat. The average RoIC in the last ten years was 9.7% and therefore slightly below the threshold. We could argue that the RoIC might indicate a wide economic moat, but there are certainly other companies reporting a higher RoIC.

Finally, I like to mention that Dolby is a family led business. I have already explained in a previous article why I consider family-led companies as great investments and what the strengths of these businesses are. In that article I wrote:

It is the structure that matters and an economic moat is an example for such a structural advantage that leads to high growth rates and outperformance of a company over several decades. And being a family-run or family-led business seems to be a similar structural advantage. As it seems extremely unlikely that every member of a family is a great CEO or strategic thinking manager, it is quite striking that some companies see several generations of successful family members leading the business. We could argue that the structure of a family-run business is the key to the success and not the person which is CEO right now. This structure can be seen by several aspects - like the company's decision making, its leadership or even the long heritage(...)

In case of Dolby Labs, the Dolby family owns about 36.5 million shares (and therefore about 37% of total outstanding shares). While this is making the Dolby family already the biggest shareholder, we also must mention the share structure of class A and class B shares. As of September 30, 2022, the Dolby family had 85.7% of voting power when combining the A shares and B shares. The Dolby family is holding almost all B shares and as holders of B shares have 10 votes per share and holders of A shares have only one vote per share, the Dolby family is dominating here (see Annual Report 2022, p. 28).

Summing up, I would see a wide moat around Dolby Laboratories - despite the lower RoIC and only mediocre stock price performance. However, there is another problem: the rather low growth rates.

Long-term Growth

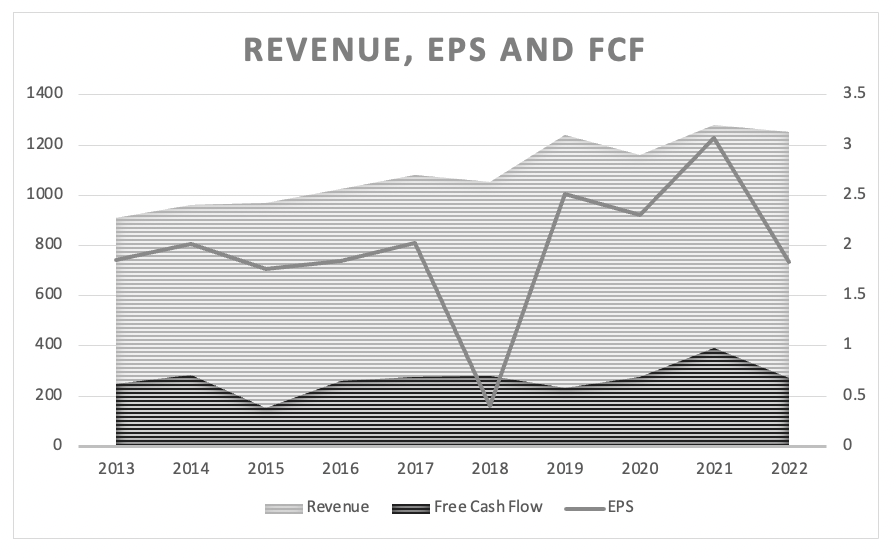

While Dolby Labs has an economic moat around its business, there is another problem - the business is struggling to grow in the last few years. In the last ten years, revenue increased with a CAGR of 3%, which is solid but not impressive. But when looking at earnings per share and free cash flow, we see rather stagnating numbers during the last ten years and not real growth. In the last ten years, earnings per share declined with a CAGR of 3.02% and in the last five years, earnings per share declined with a CAGR of 1.48%.

Dolby Laboratories Growth Rates (Author's work)

{kind=link}

When looking at the results for the first half of fiscal 2023, we see solid results. Revenue increased from $686.0 million in the first half of 2022 to $710.8 million in the first half of 2023 - resulting in 3.6% year-over-year growth. Operating income increased 51.8% year-over-year from $133.9 million in H1/22 to $203.3 million in H1/23. And finally, net income per share increased from $1.13 to $1.80 - resulting in 59.3% year-over-year growth.

When looking at the guidance for fiscal 2023, the company is expecting revenue between $1.27 billion and $1.33 billion. Compared to $1.25 billion in 2022 this is resulting in about 1.5% to 6.5% year-over-year growth. And diluted earnings per share are expected to be between $2.01 and $2.51 (compared to $1.84 in the previous year). And while revenue is at record highs, Dolby Labs has reported higher earnings per share before (for example in 2019 and 2021).

Despite the solid results and guidance for fiscal 2023, I would not expect high growth rates for earnings per share or free cash flow in the years to come. The company will be able to grow its top line with some consistency, but right now we have almost no reference point to assume high growth rates in the years to come.

Intrinsic Value Calculation

The major problem I see with Dolby Labs is the mismatch being the valuation and the growth rates. When looking at the price-earnings ratio of 33.7, this is below the 10-year average of 36.53, but I would see it as a rather high P/E ratio, which can only be justified by high growth rates. But when looking at the price-free-cash-flow ratio, we see a more reasonable P/FCF ratio of 23.6, which is not extremely cheap, but could be seen as acceptable.

Despite the wide economic moat around the business, the growth rates are rather underwhelming in the last few years and do not justify the current stock price. Of course, we also must take into account that Dolby could grow with a higher pace in previous years, and we saw double-digit growth - but the question is if Dolby can return to these growth rates.

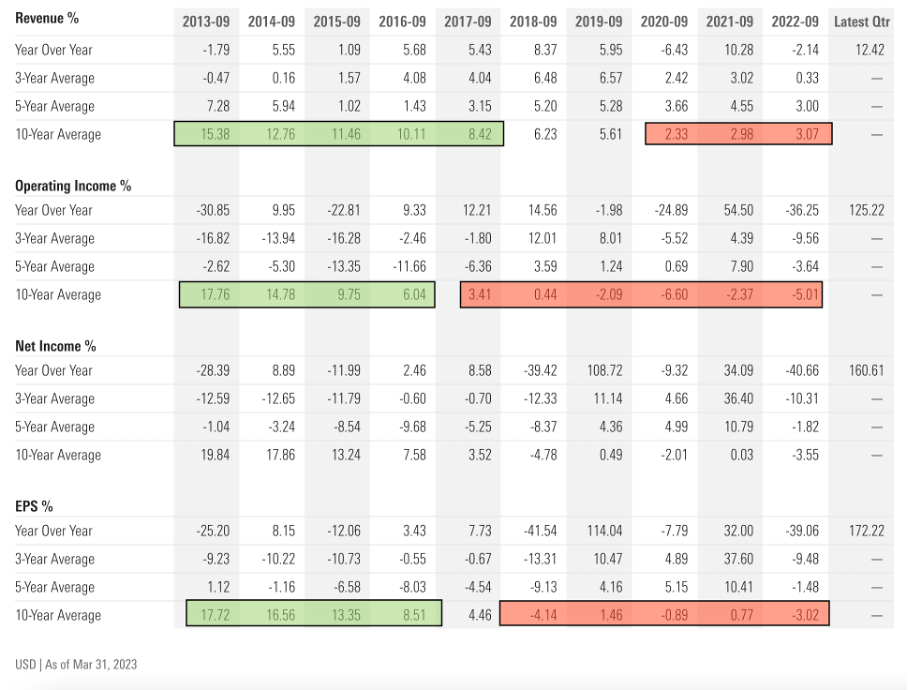

Dolby Laboratories Growth Rates (Morningstar)

{kind=link}

Marked in red are the rather low growth rates in the last few years that can't really justify the current valuation multiples. But in green I have marked growth rates in previous years - and we are seeing impressive double-digit growth rates over 10 years - that could easily justify the current stock price.

When using a discounted cash flow calculation to determine an intrinsic value, we must calculate with 97.3 million outstanding shares (and a 10% discount rate as always). As basis we can take the free cash flow of the last four quarters, which was $384.3 million. When calculating with these numbers, Dolby Labs must grow its free cash flow between 5% and 6% from now till perpetuity to be fairly valued. And when looking at the chart above, we can either make the case for these growth assumptions being too optimistic or being too pessimistic as the company demonstrated its ability to grow in the double digits.

We could see an intrinsic value between $70 and $80 as realistic for Dolby Labs. And I would see the stock as fairly valued at this point, but it is certainly not a bargain and not an investment one has to make. It might be a solid investment, but there also might be better investments in this market right now.

Healthy Company

Finally, we can make the case for adding the cash, cash equivalents and short-term investments on the balance sheet to the intrinsic value. When looking at the balance sheet, Dolby Labs has no debt, which is a good sign. And while it is good news to have no debt on the liabilities side of the business, we can also look at the asset side of the business and see $688.4 million in cash and cash equivalents as well as $126.4 million in short-term investments. Out of $2,836 million in total assets, the company has 28.7% in very liquid assets.

The great balance sheet of Dolby Labs would enable the company to either use its cash for acquisitions (for example) or share buybacks. And when considering a market capitalization of $7.95 billion, the cash, cash equivalents and short-term investments are enough to repurchase 10.2% of the outstanding shares. And when returning to the intrinsic value calculation, it would increase the value per share about $9.

Conclusion

Dolby Labs seems to have a wide economic moat around its business based on its patents and switching costs. However, the company seems not to be able to grow with a high pace in the last few years - despite the economic moat - and therefore the current stock price might not be justified. The great balance sheet and family-led business are certainly a net positive, but at this point I don't see the stock as a great investment.

For further details see:

Dolby Laboratories: Economic Moat Meets Slow Growth