DLB - Dolby Laboratories: High P/E Is Not Justified A Hold For Now

2023-09-13 13:27:05 ET

Summary

- Dolby Laboratories' financials show a strong cash position and no debt, allowing for potential growth initiatives or shareholder rewards.

- The company's current ratio is high, indicating potential for more aggressive market expansion.

- Dolby's efficiency and profitability metrics need improvement, and revenue growth has been slow, making the current valuation unattractive.

Investment Thesis

I wanted to take a look at the sound giant Dolby Laboratories' (DLB) financials and see if the current TTM P/E ratio of 37 and FW P/E of 25 is justified and is a good entry point for a new investor who has no position in the company. For these ratios to be justifiable for a new investor, the company's revenue growth and/or profitability has to improve significantly in my view, therefore, I give Dolby a hold rating until the risk/reward improves.

Outlook

The company is looking to push forward its Dolby Atmos and Vision technologies to be available across living rooms through streaming services like Max, which are offering enhanced sound experience through its higher-tier subscription plan.

The company does have a lot of opportunities to expand these technologies further, and we can see this happening already through the partnership with TCL, who announced earlier that all their 4K TVs will have Atmos included going forward. That is a big deal because TCL has become 2nd in terms of market share in the US after Samsung.

Acer has recently launched its TVs with Atmos and Vision in India, which is also a fast-growing market.

These technologies are finding their way into the biggest economies in the world like China, India, and the US. The technology is fantastic and is very premium. This is going to be what will drive revenues for years to come.

A potential big problem could be coming from Alphabet (GOOG) (GOOGL), who is trying to develop a free alternative to Dolby's Vision and Atmos and will offer these for free to other manufacturers like Sony (SONY), Samsung, and LG. How big of a problem this will be, is still uncertain, however, Samsung tried the same for their TVs with its HDR10+ to avoid paying the licensing fees and offered it to other OEMs royalty-free, it did not take off as Vision and Atmos did, which could mean that Alphabet's attempt may not work either. Most TVs run either Android TV or Google TV, so it may potentially be a big problem, however.

Financials

As of Q3 '23, the company had $765m in cash against zero debt, a great position to be in. It lets the company focus on further growth initiatives like acquisitions to improve revenue growth or reward loyal shareholders. I would rather the company went with the former because, as you will see later on in the section, the growth has not been very good in the last decade.

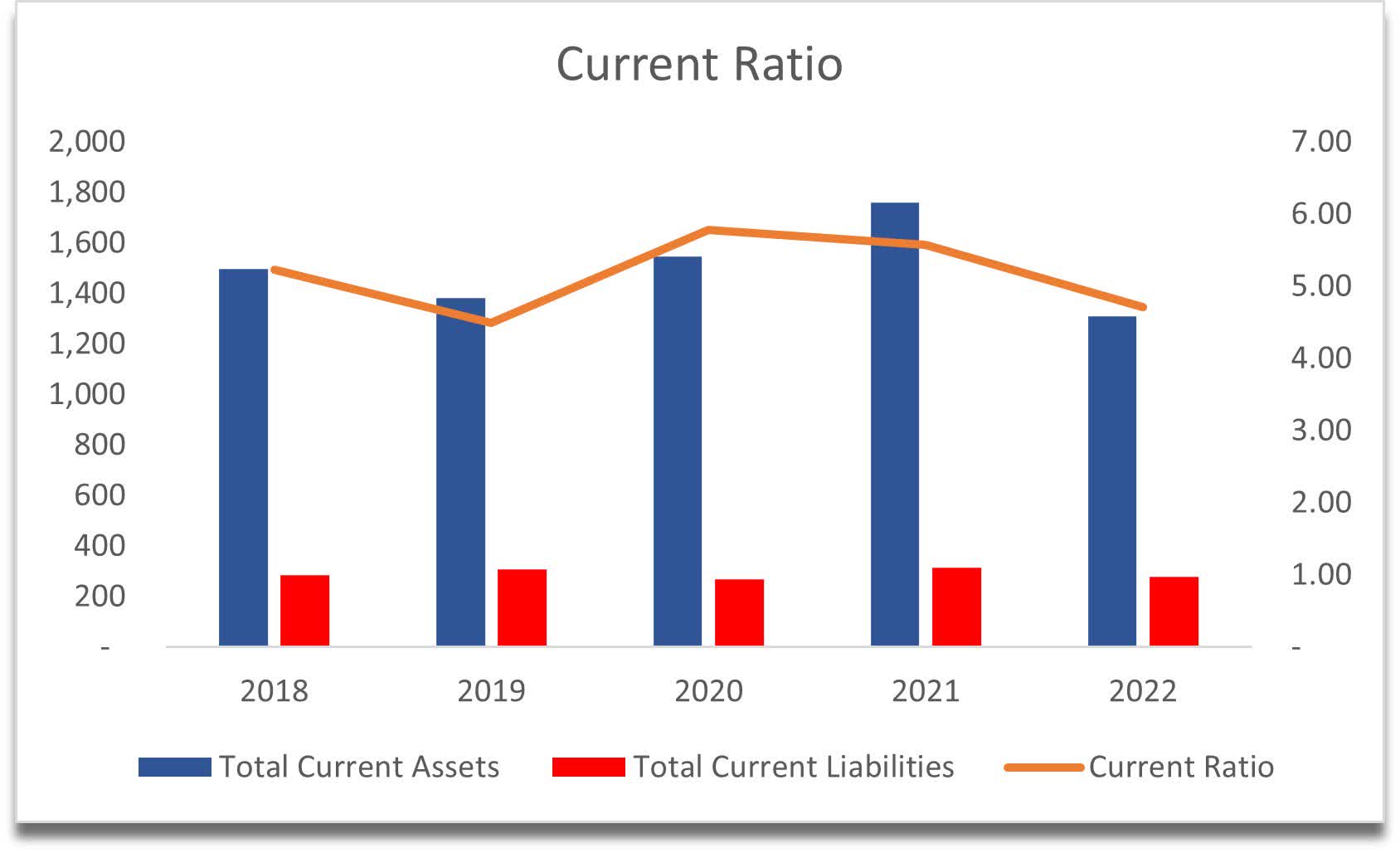

As for the company's current ratio, it is a little too high, which tells me the company could be putting that cash pile to better use in the form of taking a more aggressive approach to expanding its market share to further the growth of the company. The historical current ratio has been anywhere from 4.0 to 6.0, which is too high in my opinion. One good thing about is that it has no liquidity issues as it can pay its short-term obligation 5 times over. I consider an efficient current ratio to be around 1.5-2.0, which seems like a good balance between being able to pay off its ST obligations and utilizing cash more efficiently for growth initiatives. As of Q3 '23, the company's current ratio has come down to around 3.5, which is good to see.

{kind=link}

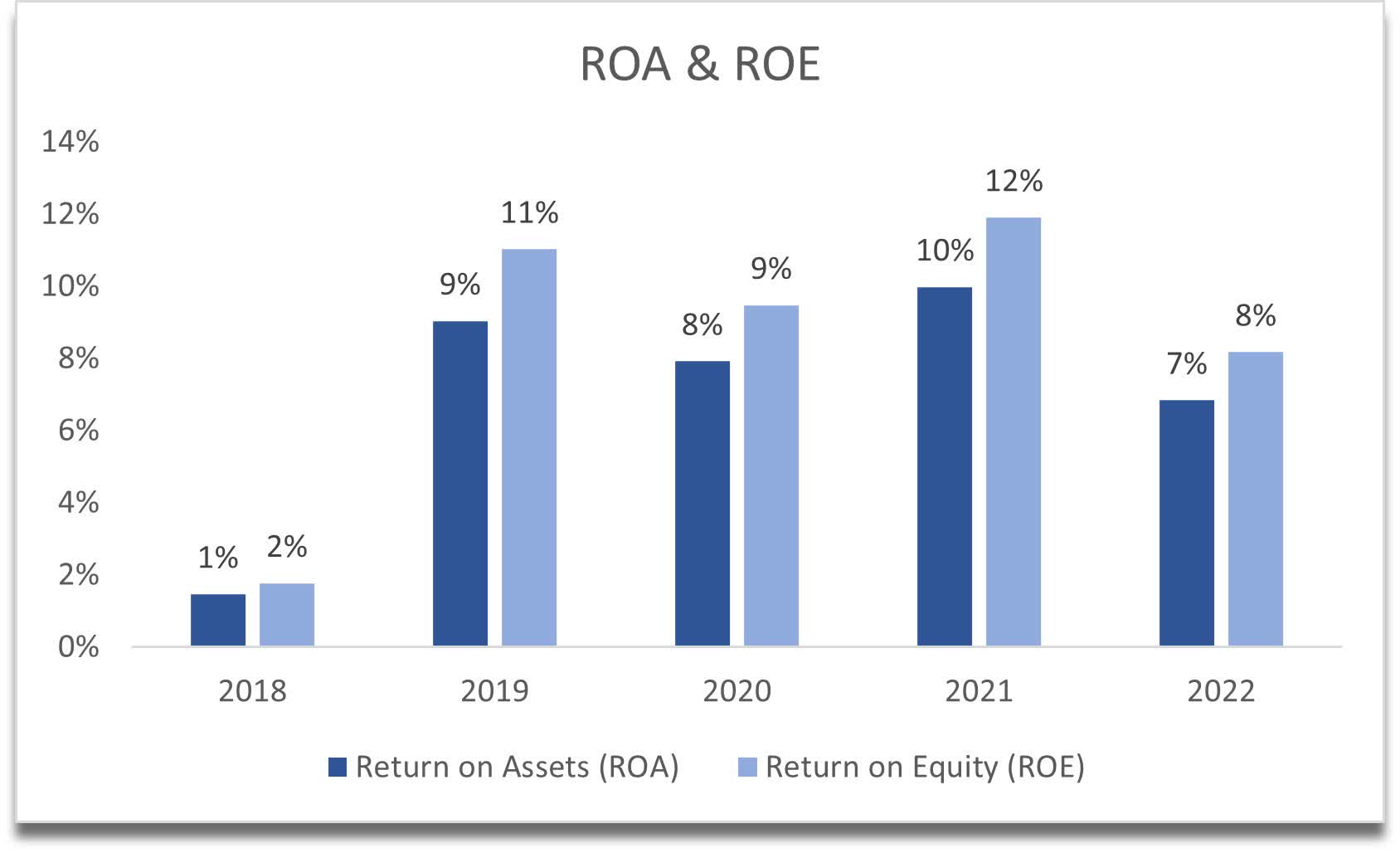

I would like to see the company's efficiency and profitability metrics like ROA and ROE come back up above my minimums of 5% for ROA and 10% for ROE in the future. The company is reporting the full-year results sometime in November. I would like to see these metrics improve further. FY21 was a recent top for the company, which I would like to see return in the next year or two. ROA and ROE are at about the same levels as of Q3 '23, which tells me that we will need to wait a little further to see some improvements in efficiency and profitability in the next year. Hopefully, sales of TVs and other products will pick up and that will increase Dolby's revenues.

{kind=link}

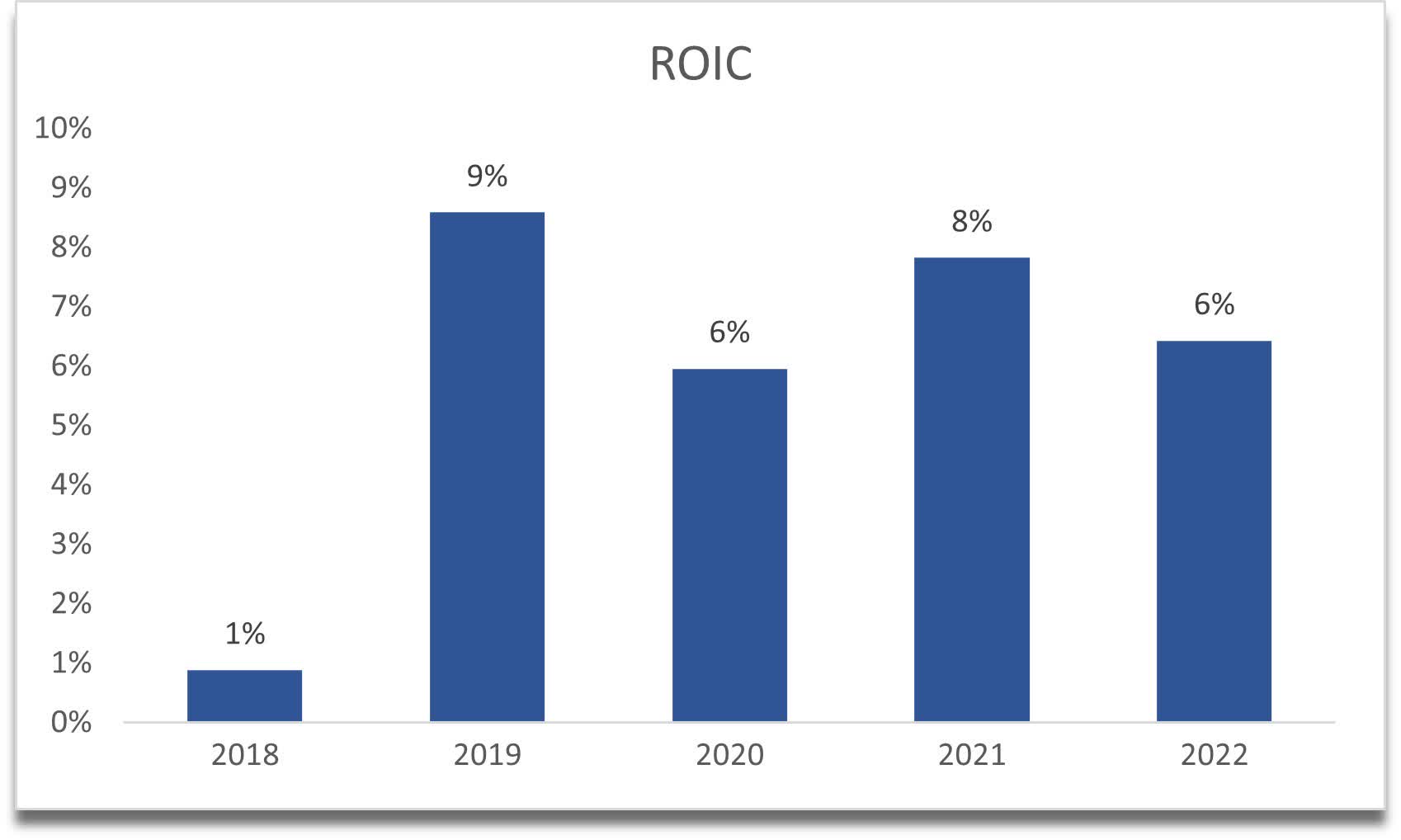

I am also not a fan of the company's return on invested capital, which has been on a slight downtrend since FY19. This tells me that the company is losing its competitive edge and its moat is deteriorating. I am looking for a minimum of 10% ROIC, and if the company cannot reach that shortly, then I will have to be more conservative in my assumptions.

{kind=link}

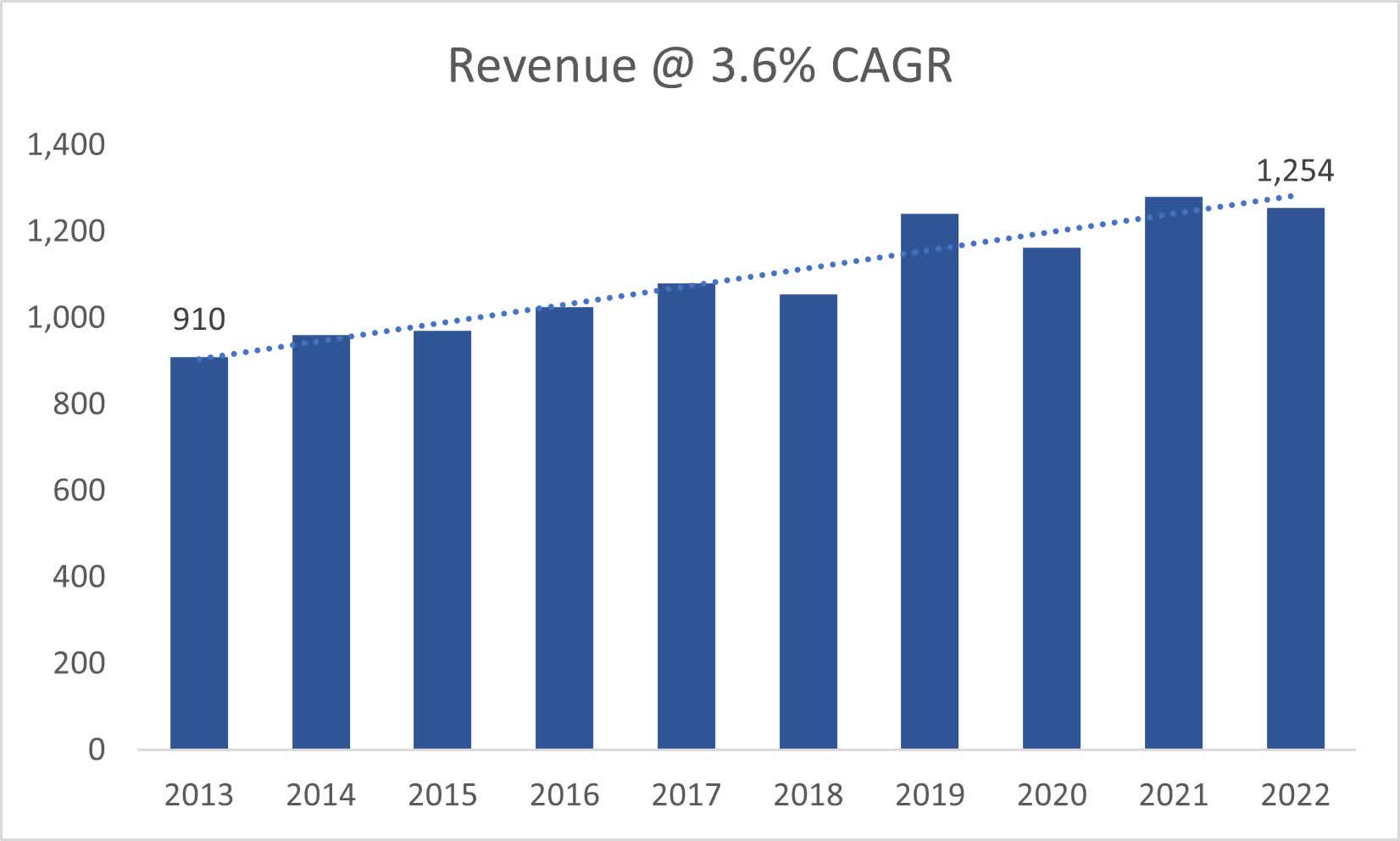

In terms of revenue, as I mentioned earlier, the growth has not been very good. It also looks like the growth isn't going to improve this year and there's no indication that the company will see a shift in the following year either. I wish I could model a better-than-average figure over the last decade of growth; however, I like to keep it conservative and have a higher level of margin of safety. Anything is possible in the future; however, I will go for the likely outcome for my model.

{kind=link}

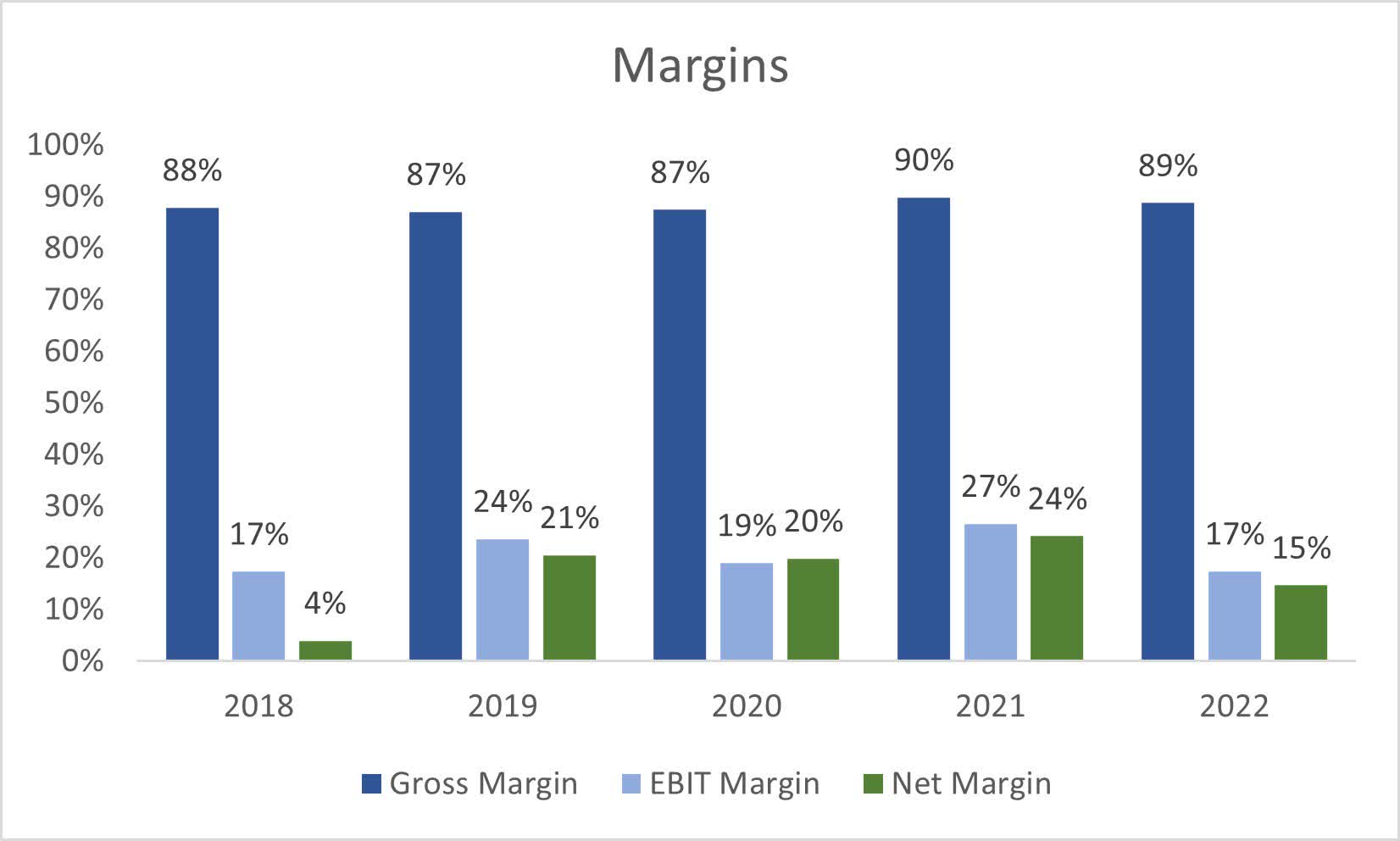

In terms of margins, the company has impressive gross margins because of how its business is set up, which is made up of over 90% from licensing fees of its technologies, while the remainder is products and services, which had around 11% gross margins as of FY22.

Operating margins and net margins have seen a hit in FY22, which makes sense. It was a tough year for most, if not all companies, and I wouldn't be surprised if these improved over the coming years. The company likes to report non-GAAP margins, which the company guided for FY23 to be around 30% operating margins and 88% gross margins. This should bring around 26% net margins according to my calculations.

{kind=link}

Overall, the financials are a mixed bag in my opinion. There is a lot of potential for this to improve over the next year or two, with the economic environment improving further. It will also depend on management's ability to find strategic growth opportunities, improve profitability and efficiency metrics, and overall sentiment globally.

Valuation

So, as I said, I will be operating on an assumption that the company's revenue growth will not see a substantial shift for the better, hence, I decided to go with around 4% CAGR over the next decade for my base case. For the optimistic case, I went with around 8% CAGR, while for the conservative case, I went with around 2% CAGR to give me a range of possible outcomes. I cannot justify higher revenue growth without some evidence that the company would be able to achieve it, given that the management is guiding for around 3% growth for FY23.

In terms of EPS, I went with the baseline of analysts' estimates, which are non-GAAP. I went with around $3.3 a share in FY23, which will grow to around $5 a share by '32. I am leaving the non-GAAP margins static for the model. The company could easily outperform, however, seeing the fluctuations in the last 5 years in EPS, I think my model is reasonable.

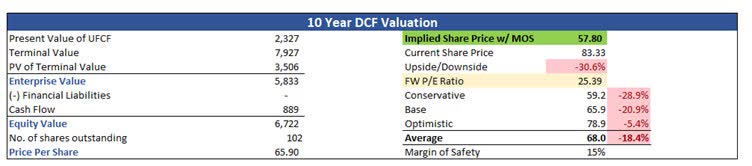

On top of these assumptions, I will add a 15% margin of safety to give myself more breathing room. With that said, Dolby's intrinsic value is around $58 a share, which means that at the current price, the risk/reward is not ideal for me, and I would like to see a pullback towards my PT.

{kind=link}

Closing Comments

The shares are too expensive in my opinion right now, and I would like a pullback for the company to prove it can grow at higher growth rates in the future or it can improve its EPS through cost-cutting measures and other initiatives. The FWD PE ratio is around 25x, which seems a little steep for a company that manages to grow at around 4% a year. If we take my PT of $57.8, the FWD PE ratio would sit at around 17x-18x, which is a little more enticing. The last time the company saw such a PE ratio was in 2015, which is not encouraging.

The company has been trading for a premium for a while now, and I don't see why it would be right now, with slow revenue growth and subpar profitability and efficiency metrics, in my opinion. For me to start a position, my risk/reward is around $60 a share. I will set a price alert closer to that price and wait until the next earnings report to reassess if needed.

There is also not enough volatility or liquidity for cash-secured puts at around $60 strike, so I will have to wait for implied volatility to pick up and the share price to come down further before a cash-secured put would be a viable strategy to entering into a long position.

For further details see:

Dolby Laboratories: High P/E Is Not Justified, A Hold For Now