DLB - Dolby Laboratories: On A Positive Hold As Shareholder Rewards Continue

2023-12-05 21:00:26 ET

Summary

- Dolby Laboratories has experienced steady growth in the audio and image technologies market.

- The company has a strong presence in various sectors, including cinema, mobile devices, and automotive audio.

- While the company has a stable business and a history of rewarding shareholders, its current valuation does not offer enough incentive for buying.

Investment Rundown

The growth for Dolby Laboratories, Inc. ( DLB ) has been quite steady over the last several years and that seems to have been reflected in the share price as well as it's up around 26% in the last 5 years. It's operating in a pretty niche market focused on audio and image technologies. The audio equipment market for example is expected to grow at a steady 7% CAGR until 2028 and be valued at over $20 billion by then. Seeing as DLB has revenues of around $1.3 billion I believe they still have a decent amount of room to grow. The problem arises however when we look at the valuation of the company, which to me doesn't offer enough incentive to be buying right now in all honesty.

Historically DLB has been trading at a slightly richer p/e than the broader information technology sector, about a 1 - 2% premium or so. In a higher interest rate environment the spending of customers seems to have halted somewhat as the sales for DLB only rose by 4% YoY to $1.3 billion in total. In the last 5 years, the annual top-line growth has averaged around 4.27% instead for the company, so this was a slight decline on that. I think that DLB still has a very bright future for itself but without strong double-digit growth numbers for either the top or bottom line I think it's hard to argue paying 23x earnings for example is worthwhile. What the company has made very clear though is their intention of rewarding shareholders as the dividend has been raised for 9 consecutive years and going forward there is over $200 million in authorized funds for buying back shares too. This all means I am a holder and not a buyer at these price points.

Company Segments

DLB is a trailblazer in the creation of cutting-edge audio and imaging technologies that redefine the entertainment experience across various platforms. The company's innovative solutions have a profound impact on cinema, DTV transmissions, mobile devices, OTT video and music services, home entertainment systems, and automotive audio. At the forefront of DLB's contributions are its proprietary audio technologies, including AAC and HE-AAC, digital audio codec solutions that find applications across diverse media platforms. These technologies play a pivotal role in delivering high-quality audio experiences, enhancing the immersive nature of entertainment content in today's dynamic and evolving digital landscape.

{kind=link}

Dolby cultivates client relationships through strategic engagements with original equipment manufacturers in the audio and visual equipment sector, as well as collaborations with software developers. By fostering partnerships with key industry players, Dolby ensures the integration of its cutting-edge audio and imaging technologies into a diverse range of devices and software applications. This type of approach I think has led DLB to continue its steady growth path, but being a smaller company than a lot of competitors the amount of capital they have available to spend is of course lower. With major companies like Apple ( AAPL ) or Sony Group Corporation ( SONY ) being in some of the same markets as DLB I think the competitor they are going up against is immense. Apple for example set out some years ago to be a major player in the high-end audio market and it seems they have managed that as AirPods are one of the company's best selling products.

The consumer audio products market is currently experiencing robust growth, fueled by an increasing demand for high-quality audio experiences across various consumer segments. Notably, the surge in popularity of wireless audio devices, such as headphones and earbuds, has been a major driver of market expansion. Consumers increasingly seek immersive and convenient audio solutions, driving manufacturers to innovate and introduce cutting-edge products.

Earnings Highlights

{kind=link}

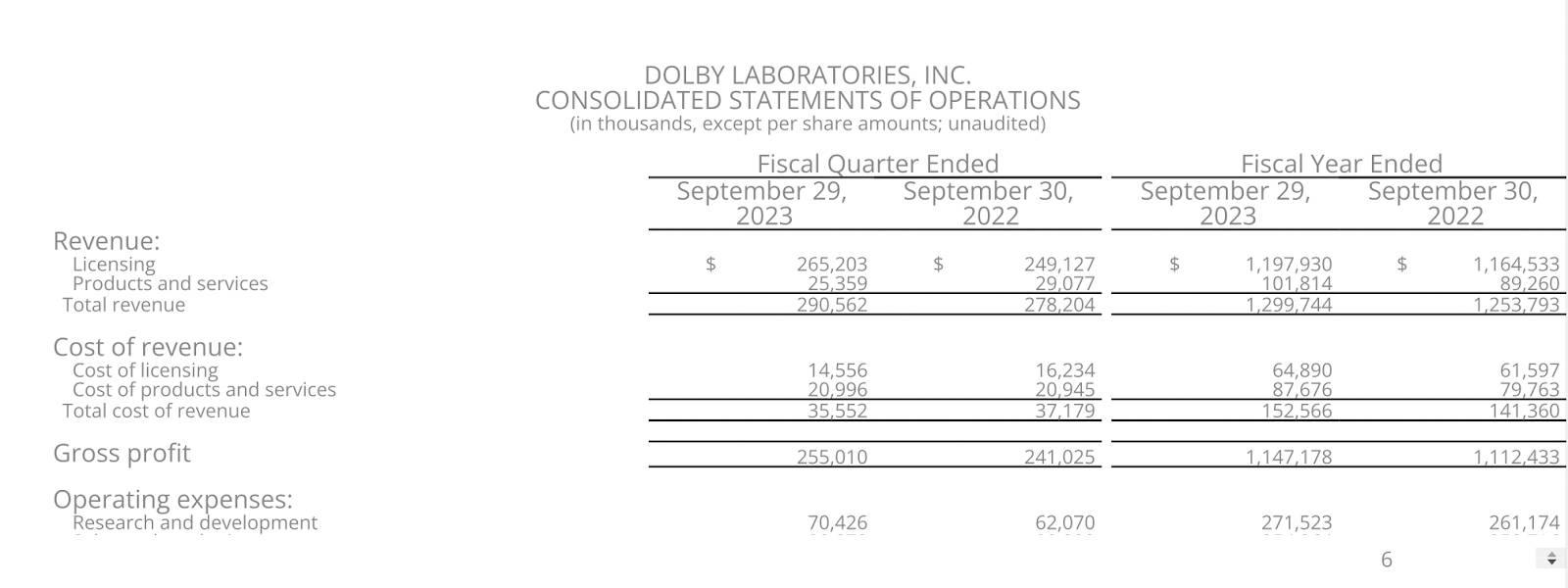

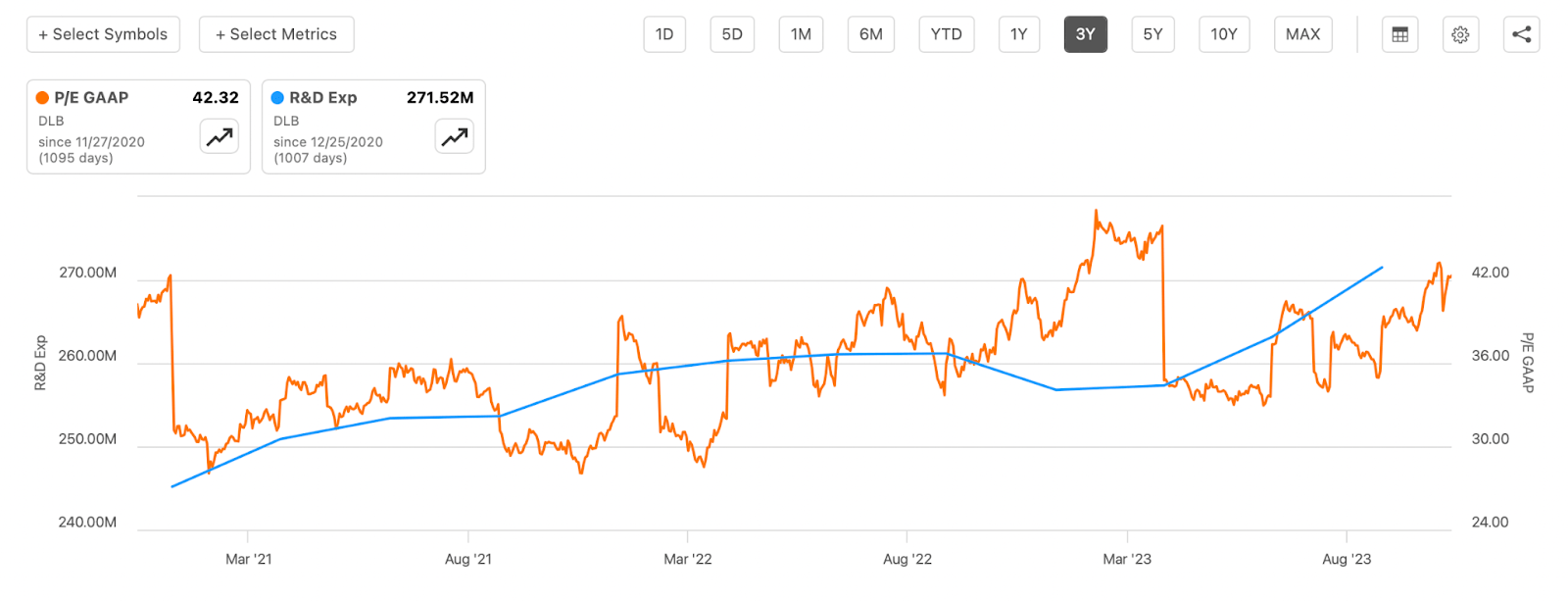

From the last earnings report by the company, it has become quite visible that DLB needs to improve its profitability and showcase some more MOAT. They have seen quickly rising R&D expenses which is the direct result of more and more companies entering the space and competition intensifying. But that means DLB needs to have superior products and be able to pass on costs to customers. The YoY growth of sales was under 5% for the business and trading at a p/s of over 6 I think there is a lack of realistic value here if I can go as far as say that. DLB has a 140% sales premium to the rest of the sector and I think most investors are on my side saying that a 4% YoY growth rate of sales does not equate to such a vast premium. So what is the cause of the premium? Well, I think it comes back to the stability of the business and how they barely lost any revenues even in 2020 when the world went into lockdown. Without any debt a strong buyback program and a history of growing the dividend I think it's viewed as a haven.

{kind=link}

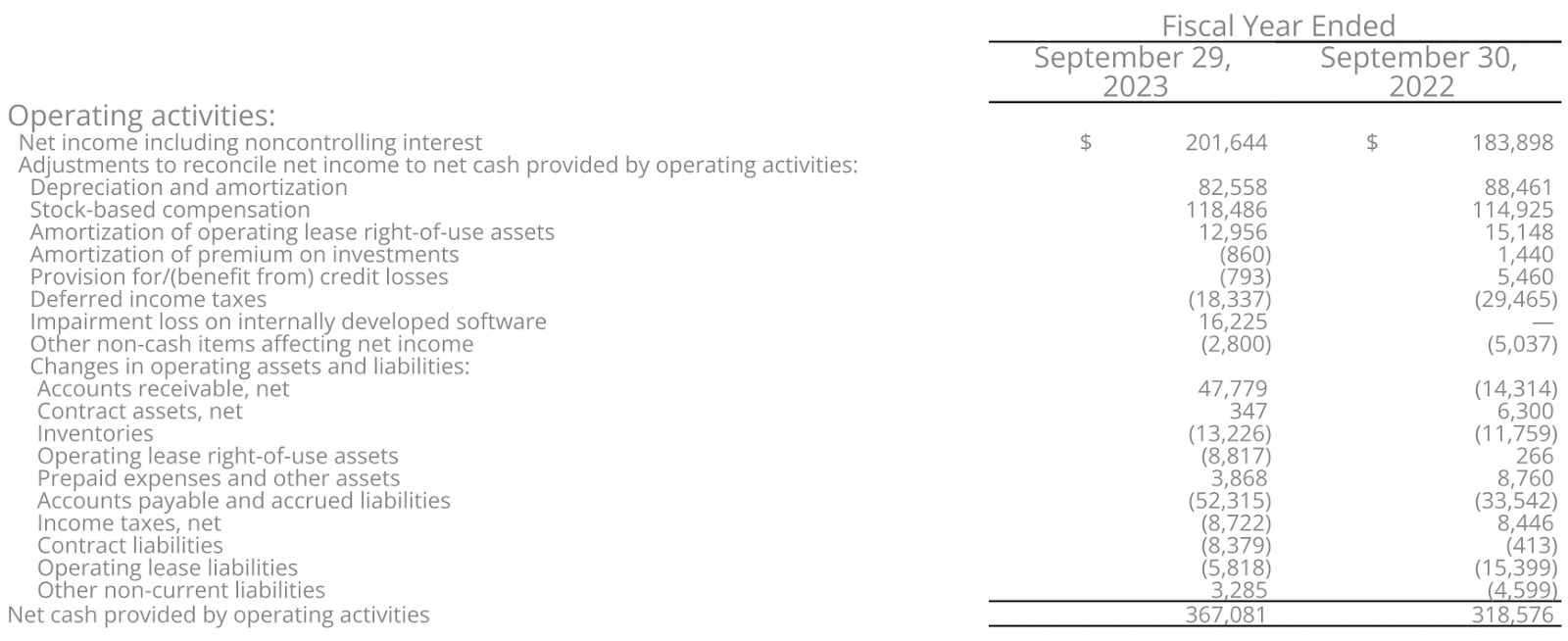

Where we saw some strong growth by the company was on the operating activities statement. Here the net cash provided by operating activities grew by 15.4% YoY primarily driven by the reduction in deferred income taxes and growth in accounts receivables too. However, I think that these results are not sufficient to be cause for a more positive rating than a hold right now.

{kind=link}

In the risk segment below I mention that I want a 20% margin of safety here at least and I think that is reasonable given the lack of growth from the business. With that in mind, I would be more interested in a p/e of 18.6 instead, and with 2023 EPS estimates of $3.7 that leaves us with a price target of $68, quite a bit below the current stock price. Getting a good entry point and a low purchase price is important, but perhaps above all that, one that is reasonable too.

Risks

Maintaining a hold recommendation at the current levels is primarily influenced by the absence of attractive entry prices. The company is currently trading at a premium compared to its historical P/E ratio of approximately 23.16. Considering that the growth figures are not surpassing double digits, the current valuation appears to carry a substantial premium. A prudent approach would entail seeking at least a 20% margin of safety, given the prevailing circumstances. This cautious stance is driven by the fact that the downside risk outweighs the upside potential at present, making a hold stance more advisable than an outright buy.

{kind=link}

With quickly rising R&D expenses, as well as the market, heating up and more and more companies spending heavily to get ahead means that less EPS growth might be visible for DLB going forward. What has been positive through the last few months is that DLB has not been widely affected by rising interest rates, at least not for its bottom line. The TTM interest expenses are under $1 million and with a net income of over $200 million it's not very significant. This may be a reason for the higher premium the company is right now receiving. But I think one could also make the case that if DLB sees it necessary to take on significant amounts of debt to get ahead of competitors, that may result in the valuation taking a hit as more risk is added to the business.

Final Words

DLB has been on a steady growth path over the last decade or so and has made strong strides in improving and rewarding shareholders through both buybacks and dividends. However, the company has not been that solid in terms of high growth numbers, yet it still receives a premium valuation. I want a 20% margin of safety from the current price levels and that means a buy can't be recommended. I do recognize the stability of the business though and that leaves me rating the company as a hold instead.

For further details see:

Dolby Laboratories: On A Positive Hold As Shareholder Rewards Continue