DOLE - Dole: An Incredibly Accretive Move To Sell Its Vegetable Division

Summary

- I think Dole plc selling its Vegetable division is an incredibly accretive move.

- After the sale, even at today's depressed multiple, Dole plc stock offers a 45% upside potential, all else being equal.

- A re-rating to its closest peer would offer Dole plc a 100% upside.

Background

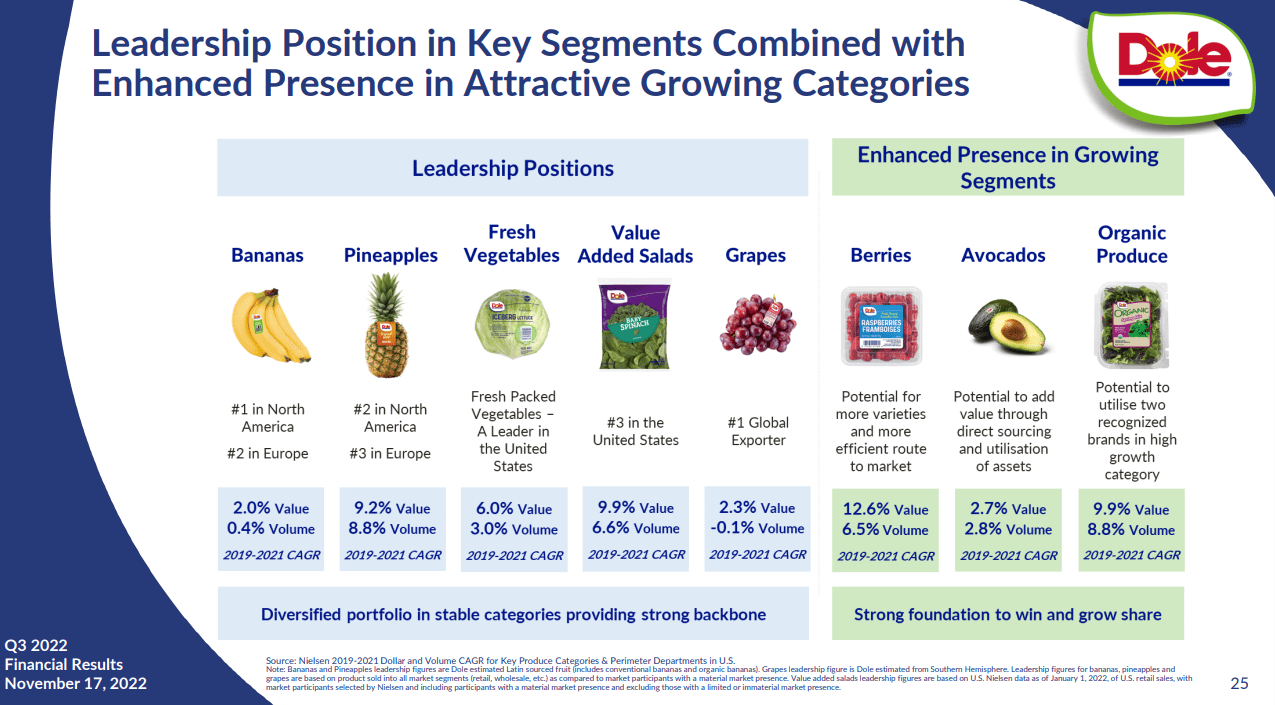

Dole plc ( DOLE ) is a vertically integrated fresh produce powerhouse. In both North America and Europe, Dole has market-leading positions in Banana, Pineapples, Packaged Salad, and Grapes, with annual sales of ~$9Bn a year.

{kind=link}

Dole was IPOed in 2021 after a series of complex capital market operations, including Total Produce merging with Dole (C&C as a 55% Dole equity owner), Total Produce delisting from Euronext Growth, and the new entity relisting/IPO in NYSE. For those interested in one of the most complicated IPO in 2021, contributor Value Situation has an excellent analysis with great details.

Subsequently, two of my trusted investor peers, Fishtown and Kingdom Capital, wrote 2 articles laying out their bull thesis that can be found here and here , respectively.

These 3 articles provide comprehensive qualitative and quantitative analysis of Dole plc as a company. Obviously, there is no reason to reiterate the well-established bull thesis.

So, why am I here? I'm here to discuss today's breaking news and how I think it impacts Dole plc's valuation in a quite dramatic fashion.

What's New?

The news comes out this morning that Dole is selling its U.S. fresh vegetable division to Fresh Express, a unit of Chiquita Holdings, for a total of $293 Million.

Fresh Vegetable is one of 4 Dole business segments. This segment generated around ~$35Mil Ebitda a year pre-covid. During the covid peak (i.e., from 3Q20 to 2Q21), due to the surging customer demands, it reined in $45Mil Ebitda.

At a first glance, the current sales price values the business at 6.5x normalized and 8x covid peak Ebitda, which is within the range of Dole's current valuation multiple. Thus, one might consider that a neutral move.

However when I dig deeper, it shows a quite different and bullish story. Let us dive in.

Quantitative Analysis

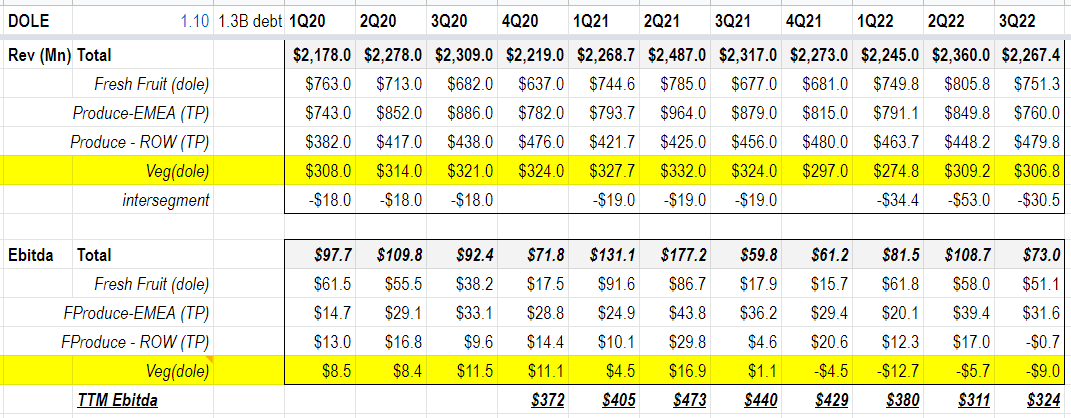

The table below shows Dole plc's quarterly revenue and Ebitda breakdown by business segment since 2020.

{kind=link}

You might notice that Dole's quarterly Ebitda has changed quite significantly and has been in a sharp decline in the last 4 quarters.

Fresh Fruit's peak earnings during 1Q and 2Q 2021 certainly played an important role, while the other important factor is its Fresh Vegetable segment deteriorated from making ~$40Mn/year to losing ~$30M+/year due to its multiple salad recalls in 2022 over listeria contamination concerns.

While one might argue ((HOPE)) this is a one-off setback, a further look shows there is some systemic weakness/risk in that segment, as this isn't the first time Dole has had to recall its packaged salad mix, e.g., see one in 2017.

Now, let us understand how this transaction impacts its valuation.

Its sell price is $293Mn, and as mentioned in the release, the proceeds will go to debt reduction.

Taking tax into consideration, I model a $250Mn debt reduction, and Dole can pay off its highest interest rate debts at SOFR + 2.75%. SOFR is currently at 4.3%, so that debt reduction will save ~$17.5Mn/year in interest payment.

The Fresh vegetable segment incurred a total of $32M loss in the last 12 months.

Assuming all other business remains the same, Dole plc's next 12M Ebitda would be $374M ($32M avoided loss + $17M interest saving). Even with today's 10% surge after the news, that values its current business at 5.8x Ev/Ebitda NTM.

To maintain the same Ev/Ebitda multiple today (7x), the stock need to rise to $17/share. You can find the calculation in the table below.

3 scenario valuation (Dole)

Shareholder-friendly Management

As the napkin math above shows, Dole plc's sales of the Fresh Vegetable segment is an incredibly accretive move, as it boosts earnings and shrinks debts at the same time. But more important than that, it shows the management team has an owner mentality (to be clear, Chairman McCain has 7.8% ownership of the company, so he is an owner), and is willing to take principled and shareholder-friendly actions, with no interest in empire building.

That, together with Total Produce's past track record, shall give investors comfort and confidence in Dole's path forward.

Increased Institutional Ownership

3 institutional players recognized Dole plc's value and took sizeable stakes by the summer 2022, as I mentioned here:

Since then, Jan Barta has increased his stake to 5.9% (from 5.2% in Aug 2022), and Dole had its 4th 5%+ shareholder - Pale Fire Capital - with a 7.8% stake by year-end 2022. Thus, we have 4 large institutional shareholders holding ~25% of total shares.

Together with 12.6% ownership from Murdock Group (via C&C), and 7.7% ownership from the McCann family (via Balkan Investment), Dole gets a solid shareholder base holding over 45% total equity today.

It is worth noting that neither Murdock nor McCann families have unloaded a share since the IPO, despite Murdock's initial intent for the IPO was to unload its equity stakes.

Banana Prices in 2023

Banana distributors/producers negotiate a base wholesale price with large grocery stores once a year, usually at the beginning of a year, with relatively minor price adjustments during the year.

Dole management has been hinting that they feel pretty confident going into this year's price negotiation given the overall market conditions. We shall certainly observe how it goes, just to highlight one thing, for this low-margin huge-volume (~$2B/year) banana business, a 1% price bump brings $20Mn straight to profit, roughly a 6% bump, powerful leverage.

Summary

In closing, this Fresh Vegetable division sale is an incredibly accretive move for Dole plc and makes a compelling bull case.

To maintain its below-peer current Ev/Ebitda multiple of 7x, the Dole plc stock price needs to rise to $17/share (assuming all else being equal), a 45% upside. A re-rating to 9x, where its closest peer Fresh Del Monte Produce Inc. ( FDP ) is currently valued, would equate to $25/share, about a 100% upside for Dole plc even considering today's 10% surge after the news.

For further details see:

Dole: An Incredibly Accretive Move To Sell Its Vegetable Division