DOLE - Dole: Is The Market Overlooking The Potential Increase In Margins?

2023-09-24 07:05:27 ET

Summary

- Dole is the product of a merger between Total Produce and Dole Food.

- This merger created the largest company in the sector, with vertical integration and global presence. Despite this seemingly great merger, Dole is trading below its IPO price.

- The creation of synergies and the sale of a division that was not profitable may bring significant margin expansion.

- This, together with the quality of the business compared to its peers, could also generate an improvement in the valuation multiple.

Investment Thesis

Dole plc ( DOLE ) resulted from the merger of Total Produce, the largest fruit and vegetable company in Europe, with the Irish company Dole Food. Both held strong positions in their respective markets, but after the merger, they emerged as the undisputed leader with a global presence, vertical integration, and significant diversification of sales within the fruit and vegetable market itself.

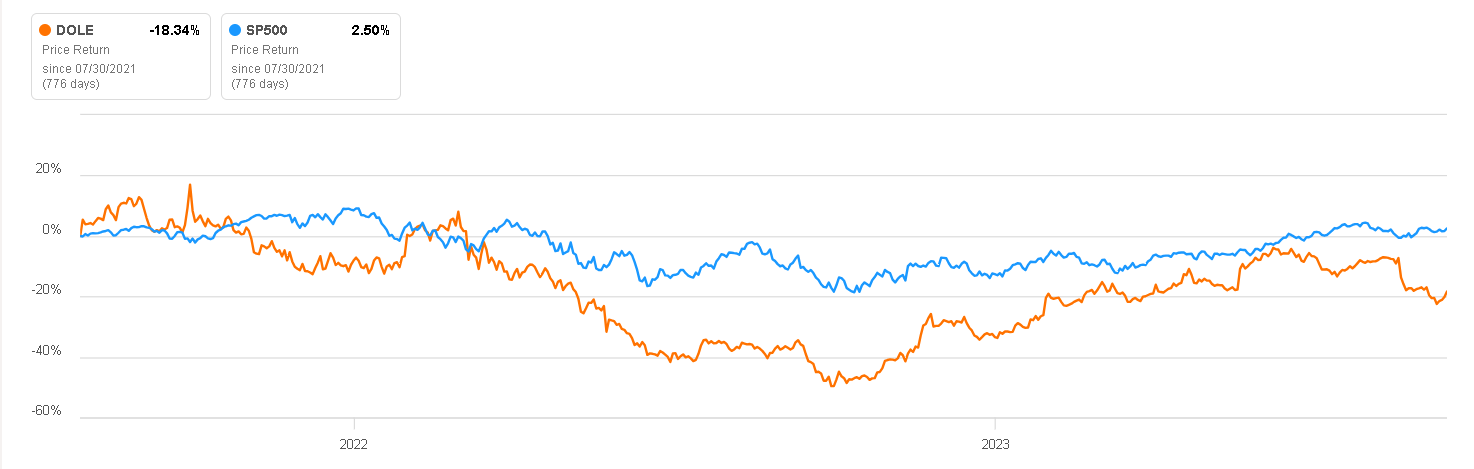

While this introduction might suggest that we are discussing one of the most successful mergers in the stock market, that is not the case. Two years after its IPO in July 2021, the company continues to trade below its IPO price. In this article, I aim to explore the factors that have led to this seemingly excellent decision yielding a poor return and analyze whether it could still be considered a promising investment.

Price Return vs S&P500 (Seeking Alpha)

{kind=link}

Business Overview

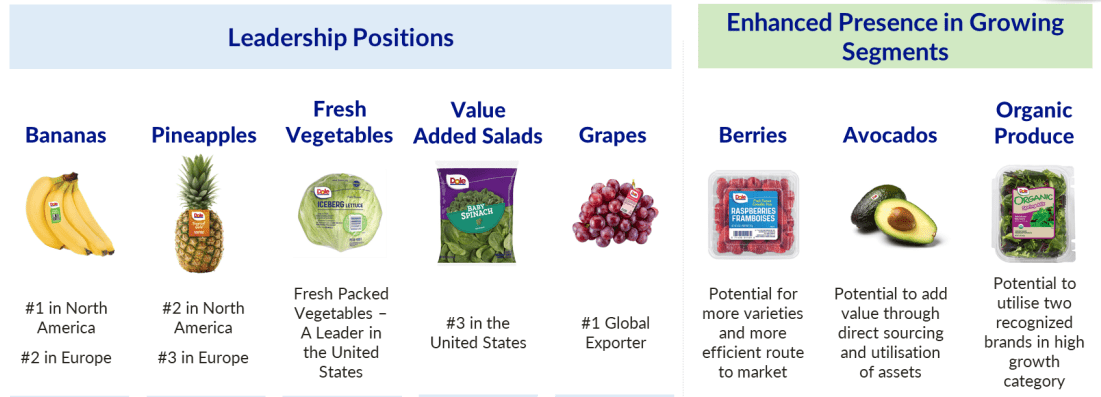

As previously mentioned, thanks to the merger of both companies, the new Dole Plc became the market leader in terms of sales.

In FY2022, Dole achieved sales of $9.2 billion USD, while Fresh Del Monte ( FDP ) recorded sales of $4.4 billion, and Greenyard reached $3.6 billion. This demonstrates that Dole's sales are double those of its closest competitor, even when considering the ongoing process of creating synergies and structuring the merger between Dole Food and Total Produce.

{kind=link}

Despite its initial unattractiveness, this business model offers remarkable resilience during challenging times, primarily because it revolves around providing one of humanity's most fundamental needs: food. The enduring demand for food products, driven by population growth and evolving consumer preferences, contributes to its stability. According to various research sources , the global food market is expected to continue its growth trajectory, with estimates ranging from 3% to 5%. This sustained growth potential makes the food industry an enticing prospect for investors seeking stability and consistent returns in an ever-changing economic landscape.

Verified Market Research

Vertical Integration

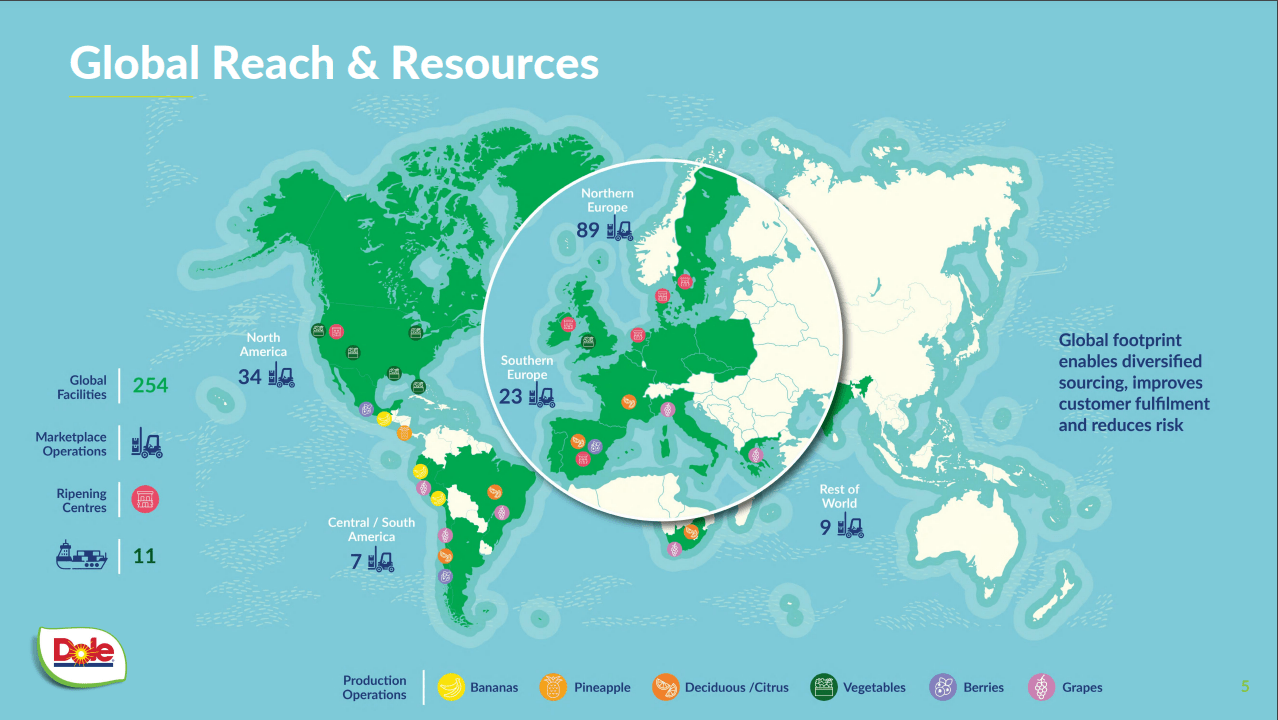

A significant feature of Dole Food, and likely one of the reasons Total Produce became interested in it, is its vertical integration. As of March 2021 , the company owned approximately 109,000 acres of land worldwide and leased approximately 14,000 acres. By December 2022 , that figure had already reached 114,000 acres in its possession.

Additionally, the company owns a fleet of ten self-sustained refrigerated container carriers and six pallet-friendly conventional refrigerated ships as of March 31, 2021. This configuration results in the company having a more flexible cost structure. For example, by owning the land, it can save on rental expenses, equivalent to lower lease costs. Furthermore, it maintains a substantial fleet of containers and ships, resulting in additional cost savings on transportation.

With all of these advantages, especially in an inflationary environment like the current one, Dole could better withstand price increases because its lease and transportation costs would not rise as significantly, thanks to reduced exposure to them. This is why, in terms of valuation, I believe that in the long term, it has the potential to generate better margins than its peers have historically maintained.

{kind=link}

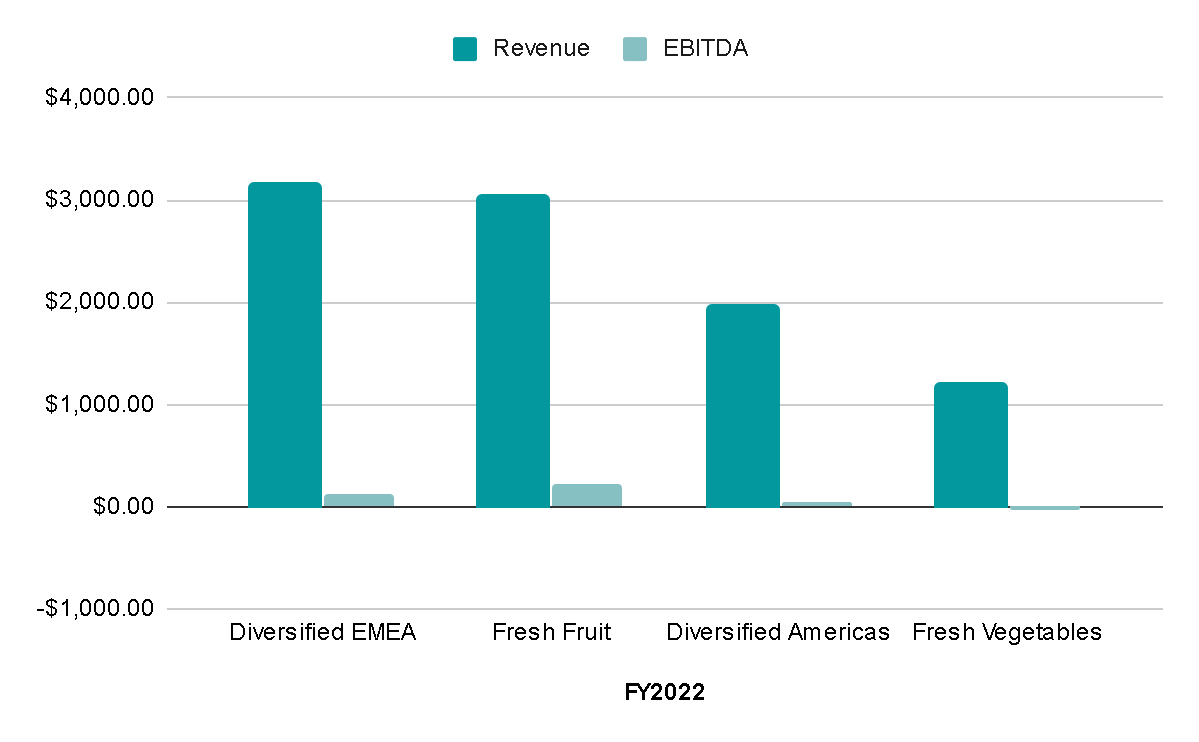

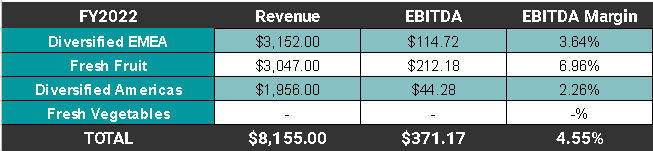

The company is currently divided (or was divided, as we will see below) into four main divisions: Fresh Fruit , Fresh Vegetables , Diversified Products in Europe, the Middle East, and Africa, and Diversified Products in the Americas. During FY2023, the Diversified Products division in EMEA held the largest share of sales at 34%, while the division with the highest EBITDA margin was Fresh Fruit, with nearly 7%. On the other hand, the division with the smallest share of sales was Fresh Vegetables, which also reported negative EBITDA margins, meaning that the company incurred losses in this division.

{kind=link}

Sale of Fresh Vegetables Division

In January of present year 2023, Dole announced the sale of its Fresh Vegetables division to Fresh Express for $293M in cash. In this division the company sold lettuces, cauliflower, broccoli, celery, asparagus, artichokes, green onions, salads, meal kits, among others.

In Q3 2022, before the sale was announced, the revenue of this division had decreased 5% and as we mentioned, it was the only division that was not operationally profitable, so this sale seems extremely appropriate to me. During the Q4 conference call it was mentioned that with the cash from the sale it was planned to pay debt, which seems like excellent news to me because Dole has a lot of debt, it has low margins and that in an environment of rising interest rates was going to be very dangerous.

And you noted the cash coming in the door from the sale of Fresh Vegetables. I think the primary objective is to pay down debt.

In summary, Dole has divested a business line that was neither growing nor profitable and represented a small percentage of its sales. The proceeds from this divestiture will be used to reduce debt and maintain a Net Debt/EBITDA ratio between 2 to 3 times.

Another noteworthy aspect is that, in a company with narrow profit margins, even a small change that reduces losses can yield significant benefits. For FY2022, the EBITDA margin stood at 3.6%, factoring in the $33 million losses incurred by the Fresh Vegetables division. However, if we exclude the income and losses associated with this division, the EBITDA margin increases to 4.5%, representing a 25% improvement in EBITDA margin simply by divesting this division.

{kind=link}

Valuation

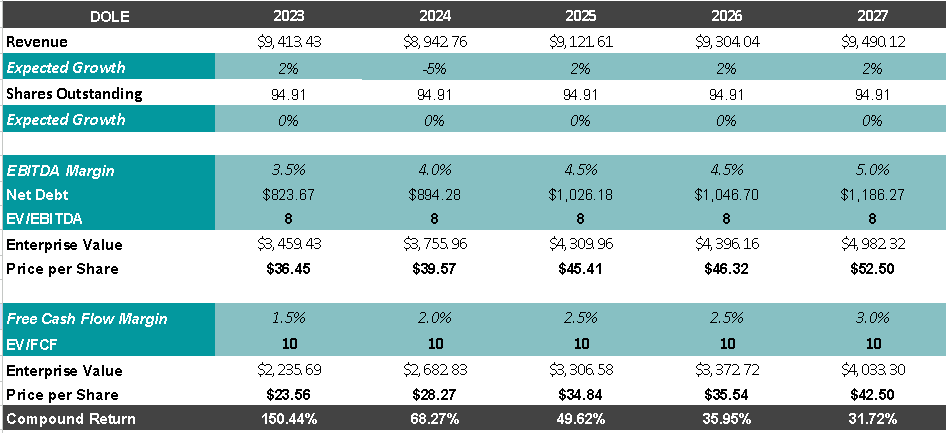

For the valuation, I will assume that the sale of the Fresh Vegetables division will be completed by 2024. During this period, I will decrease sales by 5%, reflecting the loss of revenue from this division. For the remaining years, I will conservatively estimate a sales growth rate of 2%, given the mature nature of the sector.

I will use an exit multiple of 8x for EV/EBITDA and 10x for EV/FCF. Additionally, I will consider that Net Debt levels will stabilize at 2.5x EBITDA.

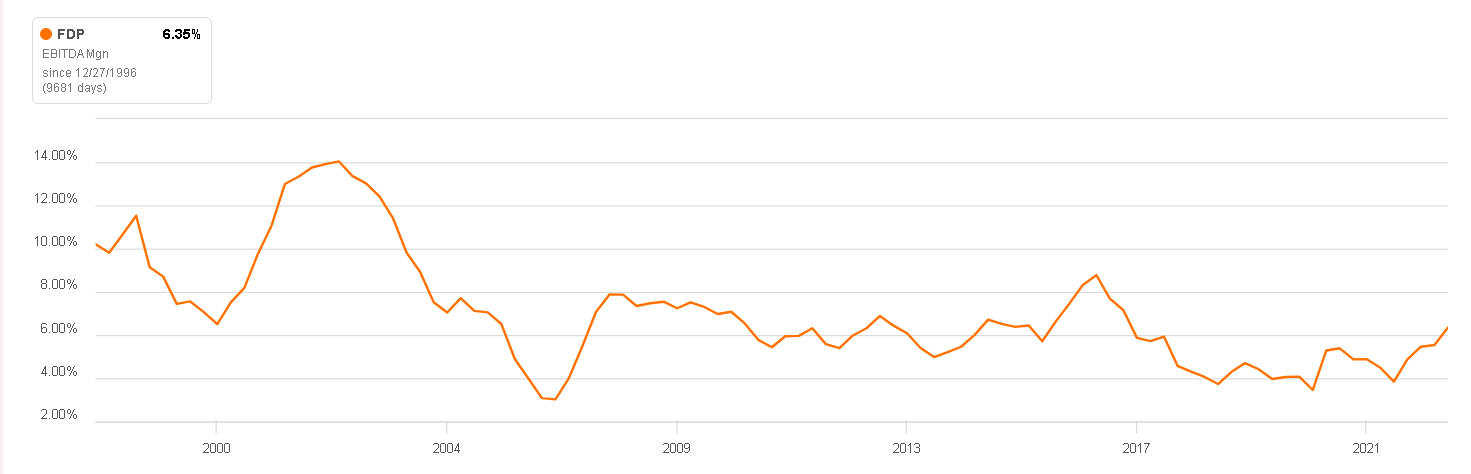

The key factor in this valuation is the gradual expansion of margins each year until reaching 5% EBITDA and 3% FCF. This projection is not unrealistic, especially considering that companies like Fresh Del Monte have achieved margins of 7-8% in certain years. Furthermore, Dole's advantageous cost structure, thanks to its vertical integration and dominant market position, makes attaining 5% EBITDA margins quite feasible. Notably, in FY2022, they already achieved margins of 4.5% when excluding the losses from the Fresh Vegetables division.

Fresh Del Monte EBITDA Margin (Seeking Alpha)

{kind=link}

With these estimates, which are intentionally conservative, we would arrive at a projected price per share of approximately $45 USD for 2027. This projection implies an impressive annual return of 30%.

The core of this investment thesis lies in the market's potential underestimation of Dole's ability to double its margins. This increase in profitability is anticipated to occur once inflationary pressures ease, the merger between Dole Food and Total Produce is successfully completed, resulting in visible synergies, and the sale of the Fresh Vegetables division leads to improved margins. These factors collectively contribute to the compelling investment opportunity in Dole.

{kind=link}

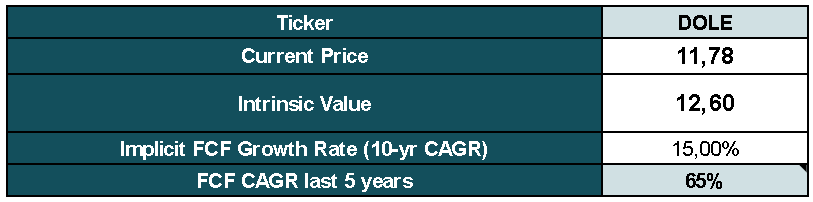

I was also somewhat skeptical of the valuation because it seems so no-brainer that something made me think, what am I missing?

So I ran a Reverse DCF to double-check what growth the market is assuming in FCF if we wanted to get a 15% return annually. Without going into much detail and purely as a double-check test, the result is 15% annual growth, which, again, is feasible considering margin expansion and creation of synergies.

Reverse DCF Results (Author's Representation)

{kind=link}

Risks

I consider these to be the biggest risks that could affect Dole's revenues and profitability:

Weather and Climate Risks : The agricultural industry in general is highly susceptible to adverse weather conditions, such as droughts, storms, frost, or unexpected temperature fluctuations. These can affect crop yields and quality, potentially leading to reduced revenue and increased costs for lost crops.

Pests and Diseases : Similar to the previous point, agricultural operations are vulnerable to pests and diseases that can harm crops too. In some cases, these threats can be difficult to predict and control, potentially leading to crop losses and increased expenses for pest management.

Transportation and Logistics Risks : As a company that owns and operates a fleet of ships, Dole is exposed to risks related to transportation and logistics. This includes rising fuel costs, disruptions in shipping routes (e.g., due to geopolitical tensions), and delays in transportation, which can affect the timely delivery of products and increase expenses.

Just as vertical integration has great benefits, it also exposes the company to specific risks like this. In any case, I think that the risk-benefit ends up compensating since the fleet and acres of land are well diversified and does not depend on a few.

Final Thoughts

In conclusion, I believe that despite the company's rally this year, there may still be significant room to achieve substantial returns at current prices.

In my opinion, this apparent undervaluation is due to the market overlooking this investment because it is situated in a sector that isn't considered very 'sexy.' It's not artificial intelligence or a biopharmaceutical company, so it doesn't attract the same number of investors. Nevertheless, if Dole continues to grow, create synergies, and improve margins, at some point, this will have to be reflected in the share price.

It's important to keep in mind that Dole holds an enviable position within its market, and due to the strategic move of selling Fresh Vegetables, I believe it also benefits from very competent management.

For further details see:

Dole: Is The Market Overlooking The Potential Increase In Margins?