DOLE - Dole's Dual Focus On Scale And Efficiency Drives Free Cash Flow Growth

2023-07-02 00:32:29 ET

Summary

- Dole's supply chain optimization and multi-channel growth are key factors supporting margin and scale expansion.

- The company on a multiples and growth value basis is materially undervalued relative to peers.

- Expect material price stability with Dole's inclusion into the Russell 3000 Index and the small-cap Russell 2000 index.

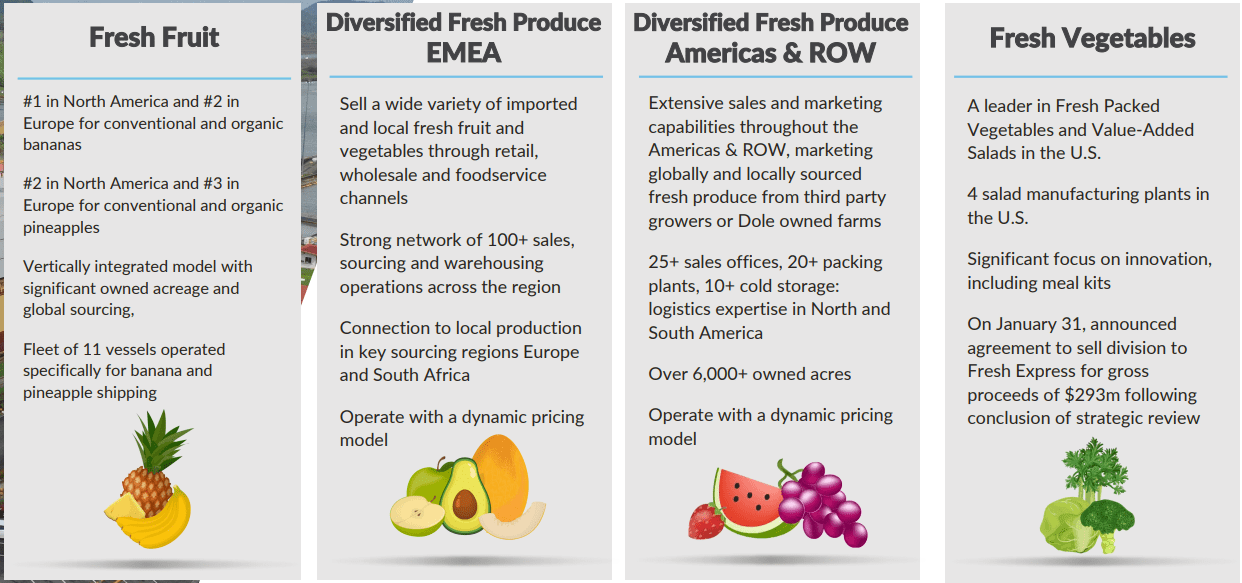

Dole ( DOLE ) is a Dublin, Ireland-based international agrifood corporation operating across four primary verticals; Fresh Fruit, which includes Dole's banana business, Diversified Fresh Produce EMEA, which encompasses imported and locally produced fruit products in Europe, the Middle East, and Africa, Diversified Fresh Fruit in the Americas and the rest of the world, and the company's fresh vegetables products.

{kind=link}

These activities have enabled Q1 revenues of $1.99bn, up 0.96% YoY, a same-period net income of $28.66mn, up 20.26%, and free cash flow reverting from negative levels at -$4.66mn, up 97.13% over the past year.

Introduction

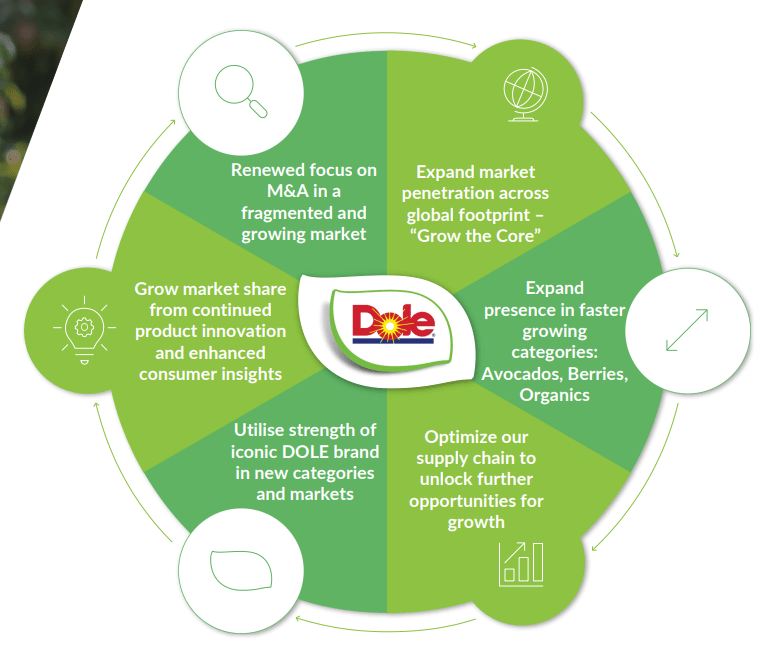

Dole's value creation blueprint is centred around its sixfold macro strategy, encompassing a focus on global geographic market penetration, expansion across high-margin and fast-growing product categories, supply chain optimization to reduce costs and accelerate logistics, use of the Dole brand to upsell its products, the use of technology and data analytics for enhanced consumer engagement, and M&A to successfully achieve all the latter objectives.

{kind=link}

The combined accretive effects of cost optimization and growth across geographic and segmented categories, alongside a general undervaluation, leads me to rate Dole a 'buy'.

Valuation & Financials

General Overview

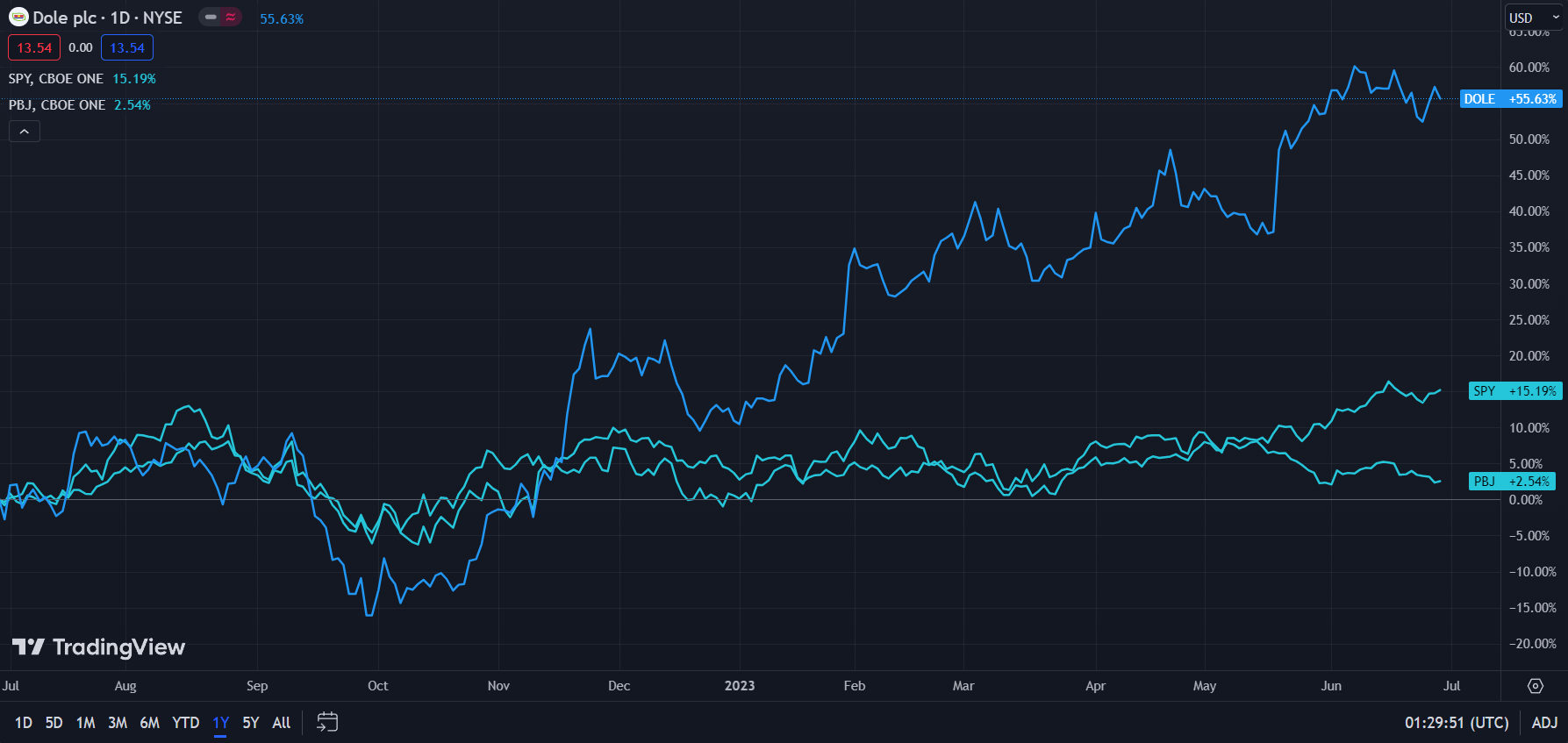

In the TTM period, Dole- up 55.63%- has experienced superior price action to both the Food & Beverage Index ( PBJ )- up 2.54%- and the broader market, represented by the S&P 500 ( SPY )- up 15.19% in the same period.

{kind=link}

This overperformance manifests Dole's operational capabilities alongside outsized sales and net income growth across the company's fresh fruit segment, representing cash flow generation not experienced by the rest of the agrifood industry and market.

However, due to undervaluation and continually strong fundamentals, I believe Dole has considerable room to grow.

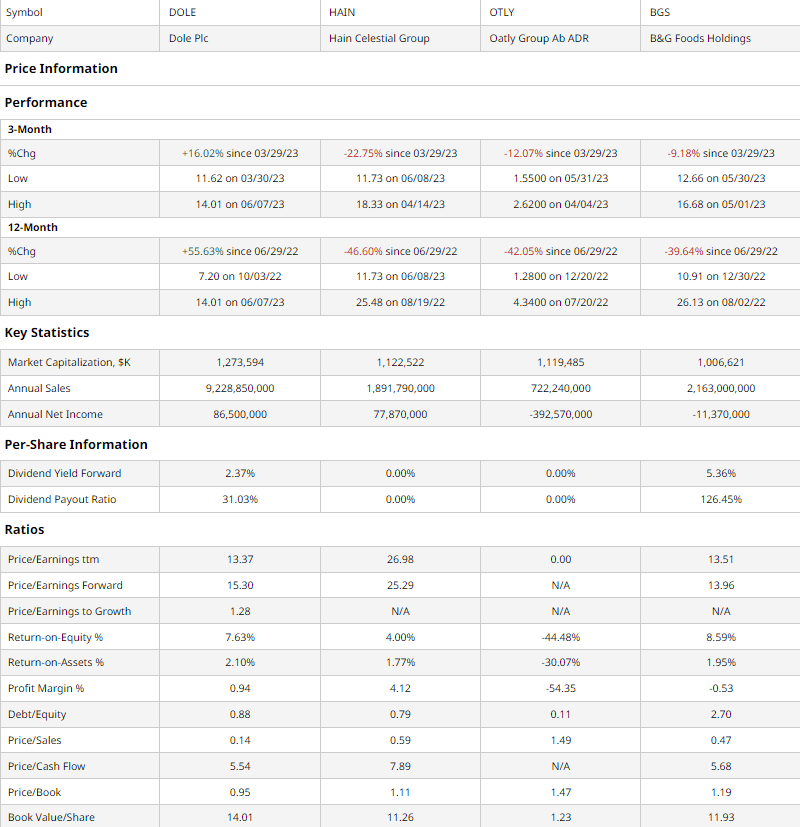

Comparable Companies

The fruit and vegetable agricultural industry is highly fragmented, with low barriers to entry and rampant protectionism and regulation, making it difficult for companies to differentiate and scale massively. As such, Dole is most comparable to food production companies of similar size if not similar operational segments. These include firms like The Hain Celestial Group ( HAIN ), which focuses on herbal teas and natural body products, Swedish-based Oatly ( OTLY ), which creates alternative dairy products with oats, and B&G Foods ( BGS ), a New Jersey-based producer of pickles, relish, and other condiments.

{kind=link}

As demonstrated above, despite experiencing the best-in-class quarterly and yearly price action, Dole, on a multiples and growth value basis, is materially undervalued relative to peers.

For instance, Dole has illustrated the lowest trailing and second-lowest forward P/E ratio, alongside a strong PEG, the lowest P/S, the lowest P/CF, the lowest P/B, and the highest book value per share, exemplifying the firm's fortress financial position.

Furthermore, Dole maintains convincing growth metrics, with the second-highest ROE and highest ROA, alongside a respectable debt/equity which enables effective reinvestment.

Valuation

According to my discounted cash flow valuation, at its base case, the fair value of Dole is $16.66, meaning, at its current price of $13.52, the stock is undervalued by 19%.

My model, calculated over 5 years without built-in perpetual growth, assumes a discount rate of 9%, addressing Dole's averaging debt levels and higher ERP as a result of greater positive volatility in recent times. Additionally, to be more conservative, I calculated an average revenue growth rate of 7%, despite a trailing 4Y average growth rate of 21.66%, anticipating a general slowdown in scale growth alongside upwards expansion cost pressure from a higher cost of capital and supply chain shifts.

{kind=link}

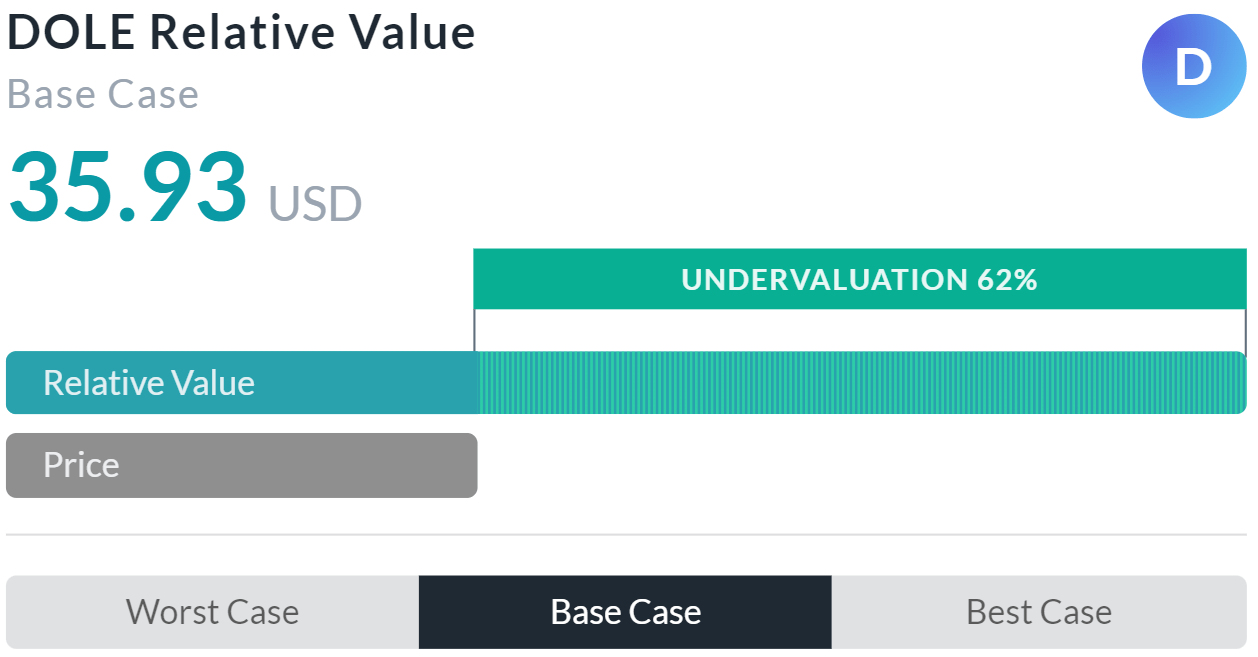

Alpha Spread's multiples-based relative valuation model more than corroborates my thesis on undervaluation, calculating that Dole is undervalued by 62%, with its relative value being $35.93.

However, I believe Alpha Spread actually overvalues Dole, since Alpha Spread uses the multiples of more mature and larger firms such as Nestle and General Mills, which operate with fundamentally different scales and value chains.

As such, taking a weighted average- skewed towards my DCF- of my model and Alpha Spread's relative valuation, the true value of Dole should be $19.66, with the company being undervalued by 31%.

Supply Chain Optimization and Multi-Channel Growth Support Margin & Scale Expansion

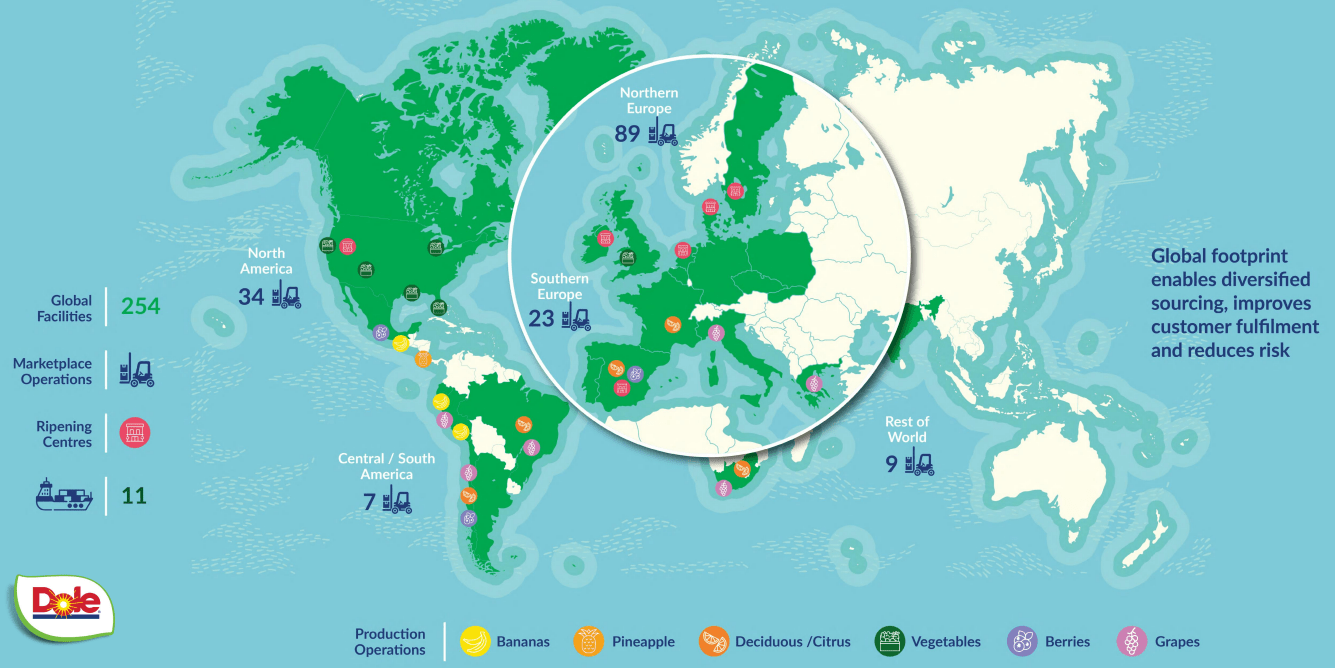

Since, as previously discussed, the agrifood business is highly commodified with little product differentiation, companies can principally compete only through operational strategy. For Dole, this has centred around its geographic and product diversity and scale. This enables resilience against economic and agricultural uncertainty in any particular region while enhancing supply chain capabilities. Through its global footprint, Dole commands a considerable presence across the Americas, and the EMEA region and sustains major impressions across South Asia and parts of Africa.

{kind=link}

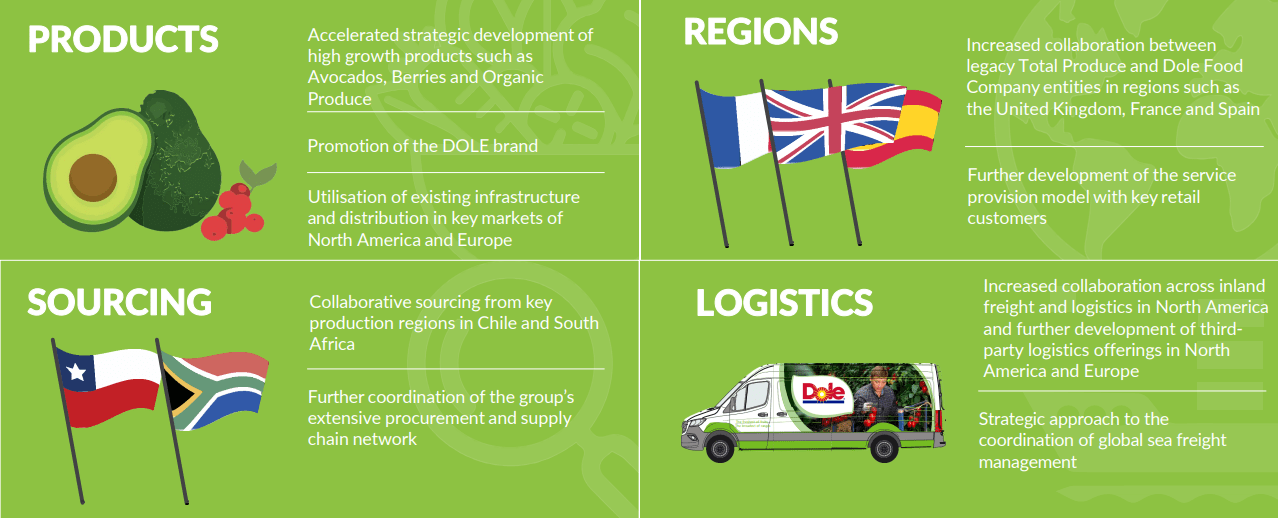

Dole's international strategy is undergirded by its fourfold value chain strategy, with a concentration on a versatile range of products, diverse sourcing and end markets for the development of superior sales models with multinational retailers, and collaborative freight and logistics frameworks. These methods serve the objective of margin expansion, with avocados, for instance, being higher margin than products such as bananas, and optimized sourcing strategies reducing logistical overhead.

{kind=link}

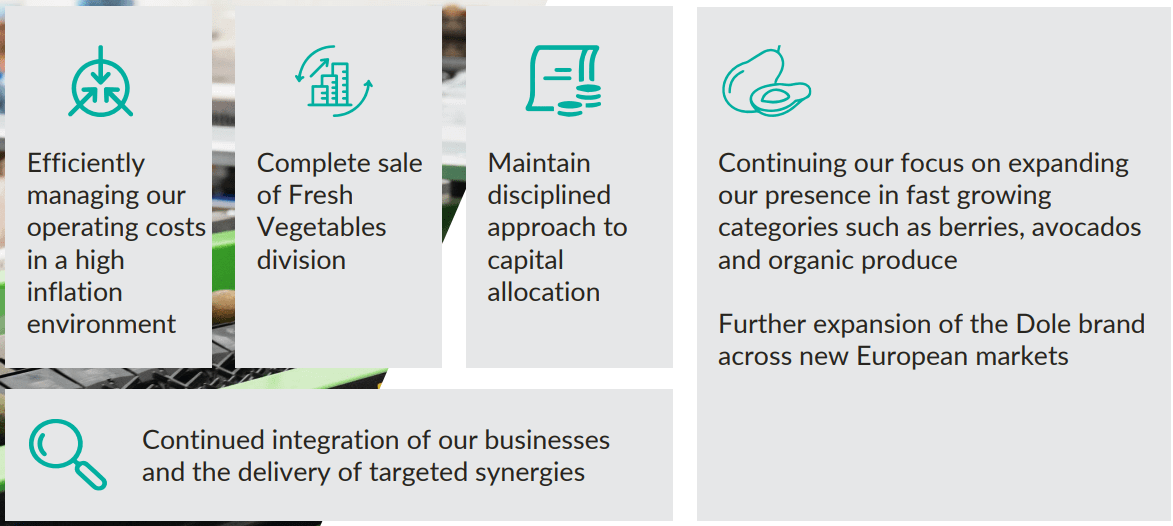

The firm's focus on margin expansion is further epitomized by its efforts to streamline the company's organizational capabilities. The integration of its different verticals, on the sales and logistics ends, in conjunction with the sales of its lower margin vegetables business, has enabled superior profitability and long-term cash flow generation throughput. Parallel to a disciplined capital deployment strategy which emphasizes a balance between reinvestment and shareholder return through its 2.36% dividend and opportunistic buybacks.

{kind=link}

Investors can also expect material price stability with Dole's inclusion into the Russell 3000 Index and the small-cap Russell 2000 index, thus being better able to weather commodity price impacts and temporary headwinds.

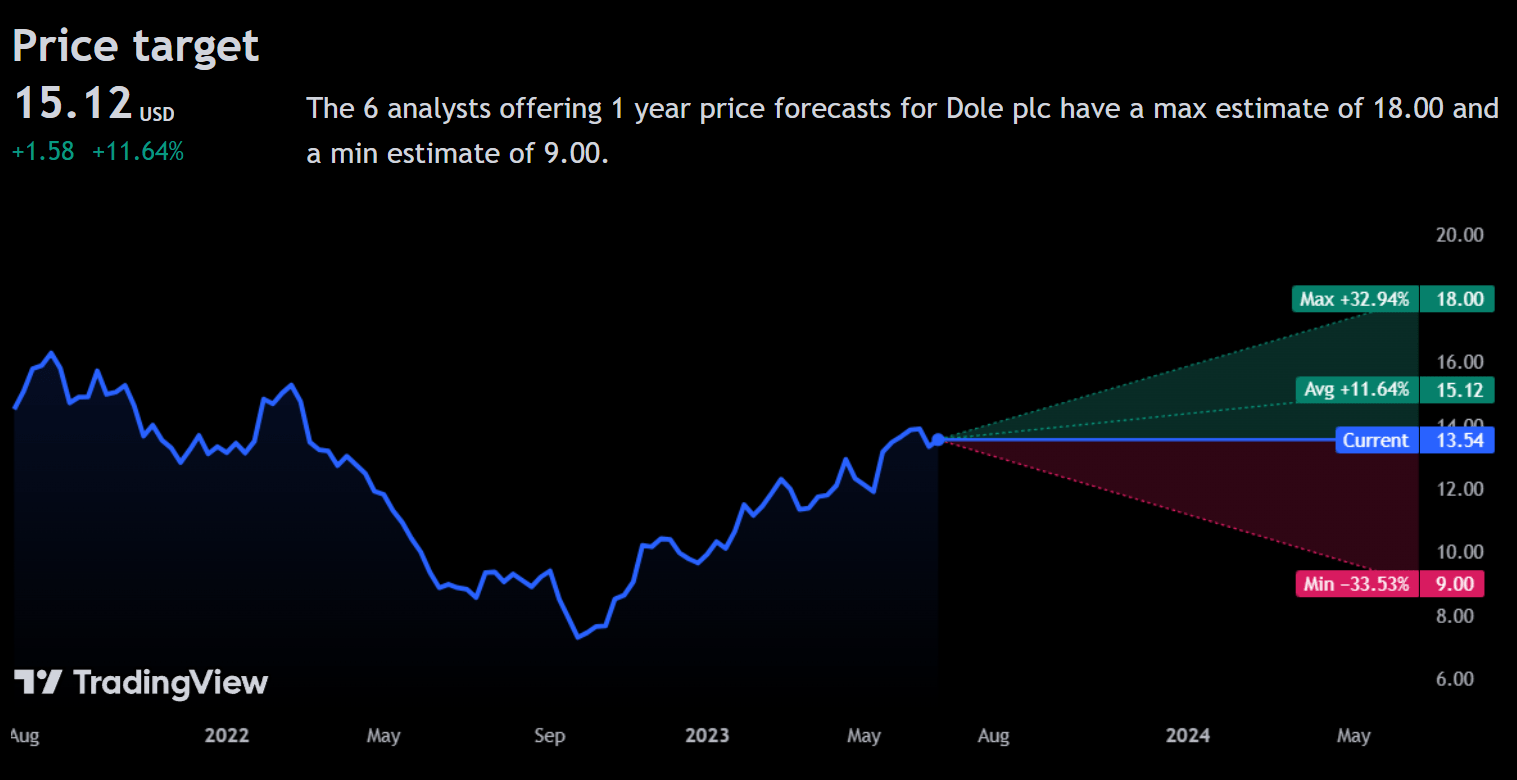

Wall Street Consensus

Analysts generally support my positive view of Dole, projecting an average 1Y price increase of 11.64% to a price of $15.12.

{kind=link}

However, at its minimum projected price level of $9.00, investors expect a 33.53% decline.

This volatility in investor expectations mirrors broader uncertainty regarding the stock's ability to support its scale and cash flow growth, though I believe Dole's index inclusion and operational capabilities largely insulate it from such a potential decrease.

Risks & Challenges

Competitive Intensity May Put Downwards Pressure on Profitability

Although Dole remains among the largest publicly traded fruit pure-play companies, the inherently fragmented and commodified nature of the industry means that there are few barriers to entry and excess production or superior operational capability of local producers or rivals may lead to lower prices, in turn reducing unit profitability. Extensive price reductions may lead to a long-term inability to grow margins and sustain investor returns.

Increased Costs From Regulatory & Inflationary Effects May Inhibit Growth & Cash Flows

With the international nature of Dole's businesses, the company is subject to regulatory pressures- on the production and end market side- from a multitude of regulators. Scale may thus be restricted on a regional basis or may lead to increased compliance costs. In addition to potential inflationary pressures from shipping or energy or hydro costs, Dole's inability to hedge adequately may reduce cash flow potential and geographic growth.

Conclusion

Going forward, Dole's combined geographic and product diversification strategy, alongside an overall streamlined business and supply chain optimization may lead to material margin and scale growth.

For further details see:

Dole's Dual Focus On Scale And Efficiency Drives Free Cash Flow Growth