DLTR - Dollar General Vs. Dollarama: Value Vs. Quality

2023-10-30 12:02:17 ET

Summary

- Dollar General and Dollarama are similar companies in the dollar store industry but operate in different countries.

- Dollar General focuses on rural areas in the US, while Dollarama has a significant presence in major Canadian cities.

- Dollarama is considered a higher-quality business with higher margins, superior return on capital, and stronger growth prospects.

- I'll assess the risk-reward balance between the two with a final Buy rating on Dollarama and a Hold for Dollar General.

Introduction

Dollar General (DG) and Dollarama (DLMAF) are similar companies operating in the dollar store industry, each in a different country. I believe Dollar General presents a compelling value proposition, a perspective shared by prominent investors such as Seth Klarman and Christopher Bloomstran. On the other hand, Dollarama, while not as attractively priced as Dollar General, is, in my view, a high-quality company to consider for investment. In this article, I will provide a detailed comparison between the two.

Similar Yet Different Business

Dollar General's business model is based on efficiently operating stores in rural areas across America, serving local populations with limited shopping options, effectively creating a local monopoly. The company provides low prices, catering to low-income customers, typically those with an annual income of around $40,000. Dollar General primarily offers consumer goods at relatively low prices, emphasizing a convenient and fast shopping experience.

In contrast, Dollarama follows a different model. It also offers goods at affordable prices but places more emphasis on merchandise like office equipment and cleaning supplies, with less focus on food items. Dollarama is not predominantly located in rural areas; it has a significant presence in major Canadian cities, boasting an extensive store network, including 590 stores in Ontario alone.

While the U.S. market is highly competitive, with rivals like Dollar Tree and Family Dollar, the Canadian market appears more stable for Dollarama. The company doesn't view large retailers like Walmart as its primary competition in Canada, and Dollar Tree has only 200 stores in the country, which could be a potential concern for its growth in the future.

Organic Growth

Both companies have growth plans centered around opening new stores and enhancing comparable sales growth.

Dollar General's store opening CAGR since 2007 has been 5.8% . Combined with same-store sales growth of 5% since 2018 (including the COVID-related increase), it results in approximately 10% sales growth. However, with the company operating nearly 20,000 stores across America, one can assume that it will start to reach a level of maturity.

Dollarama, with its goal of reaching 2,000 stores by 2030, is also anticipating a similar 5% growth in store openings. Additionally, with the tailwind of Canada's population growth, this growth trajectory could trend even higher. The comparable same-store sales averaged a 6% CAGR in the last decade but stood at 15% in Q2 FY24. Interestingly, Dollar General failed to achieve growth in its same-store sales in the last report, highlighting differences in business quality during challenging times. We will delve into this topic later.

Comparing The Important Numbers

Dollar General has shown robust top-line growth over the past five years, with a CAGR of 9%. Until recently, it also exhibited operating leverage, as its EBIT grew at an even higher pace. However, in the most recent year, we've observed Dollar General slowing down and failing to generate a profit or positive FCF. This downturn can be attributed to its low-income customer base, adversely affected by inflation and higher interest rates. This is a critical point, as this significant setback has contributed to the substantial discounts we currently see.

Conversely, Dollarama achieved a comparable top-line growth of around 10%. Impressively, it managed to establish stable and substantial operating leverage, resulting in a remarkable 23% CAGR for FCF over the last five years. This impressive FCF growth can be attributed to the outstanding margins that Dollarama enjoys, a factor we will discuss shortly.

Dollar General's margins are quite similar to those of its main competitor, Dollar Tree ( DLTR ). These surprisingly high margins, for a retailer known for selling low-priced items, play a crucial role in the company's long-term growth strategy. High and stable margins offer a buffer, allowing the company to absorb losses arising from unforeseen factors without having to cut dividends or reduce capital expenditure investments for future growth. However, Dollar General has experienced recent margin compression, with EBIT margins dropping by 12% from the five-year average.

In contrast, Dollarama boasts remarkable numbers for a retailer, and, in fact, I believe it has some of the best margins I've seen from any retailer, not just in the dollar market but across the retail sector. These margins are surprisingly high, with EBIT numbers resembling those of a tech company more than a traditional retailer. This suggests exceptional operational management and is often a result of favorable deals with suppliers, as indicated by the high gross margin.

However, it's worth noting that there may be limited room for further margin expansion. Therefore, future earnings per share growth for Dollarama can come from two main sources: top-line growth and a buyback program. Another noteworthy point in favor of Dollarama is that, even in the current challenging economic climate, it has expanded its margins, particularly in the Free Cash Flow margin.

In my view, aside from top-line growth, one of the most critical factors for long-term success is achieving high returns on capital, often measured in the form of Return on Invested Capital and Return on Capital Employed. Recent research has emphasized the importance of a high and growing spread between a business's Weighted Average Cost of Capital and its ROIC, as it creates substantial value, reflected in the company's stock price.

Notably, the difference between these two companies is a key reason I consider Dollarama a higher-quality business. This difference is a direct result of Dollarama's impressive margins. This suggests that for each unit of capital invested, Dollarama is generating more than double the return compared to Dollar General.

Dollar General offers a solid dividend yield of almost 2% . In contrast, Dollarama (Dollarama) provides an insignificant yield of 0.3% . Both companies have been aggressive buyback monsters, reducing their outstanding shares by more than 30% over the past 10 years. This significant buyback activity contributes to a real yield of around 3% annually.

These buybacks play a crucial role in EPS growth since I don't believe these companies have much room for margin expansion.

Solvency

In my view, Dollarama is in a strong position from a debt perspective. It can cover its net debt within two years of generating free cash flow, and it maintains a current ratio above 1 , along with an Altman Z-Score above 3.

However, Dollar General is not in a secure financial position from my perspective. It currently has a low FCF, and even with its highest FCF achieved in 2021, just over $2 billion, it falls far short of covering its long-term net debt. Additionally, having an Altman Z-Score below three is less than optimal; I'd prefer it to be well above three. Nonetheless, a current ratio above 1 indicates it's in a relatively stable liquidity position.

The solvency risk presented by Dollar General is a factor that warrants attention in the valuation section.

So, prior to delving into valuation and risks, it's evident, at least in my view, that Dollarama is the superior business. It boasts higher margins, superior return on capital, stronger growth prospects, faces less competition and maintains a healthier balance sheet. However, in the stock market, price plays a crucial role in the success of an investment, and the game is all about risk and reward. Let's examine that.

Risk Reward Valuation

Investing revolves around risk and reward. Typically, when a company is exceptional, its excellence is reflected in the stock price. However, this isn't always the case, and it's precisely these exceptions that create opportunities. Conversely, there are times when the market overreacts to a company's setbacks, offering opportunities as well.

In my opinion, Dollar General carries a relatively high risk and doesn't align with the quality of businesses I prefer to invest in. Nonetheless, I believe its current low price compensates for the risks it presents. DG has a solid business model, as evidenced by its growth to 20,000 stores over the past decades. I anticipate that, once the economic climate becomes less challenging, we may witness DG's free cash flow numbers return to their previous levels in the billions.

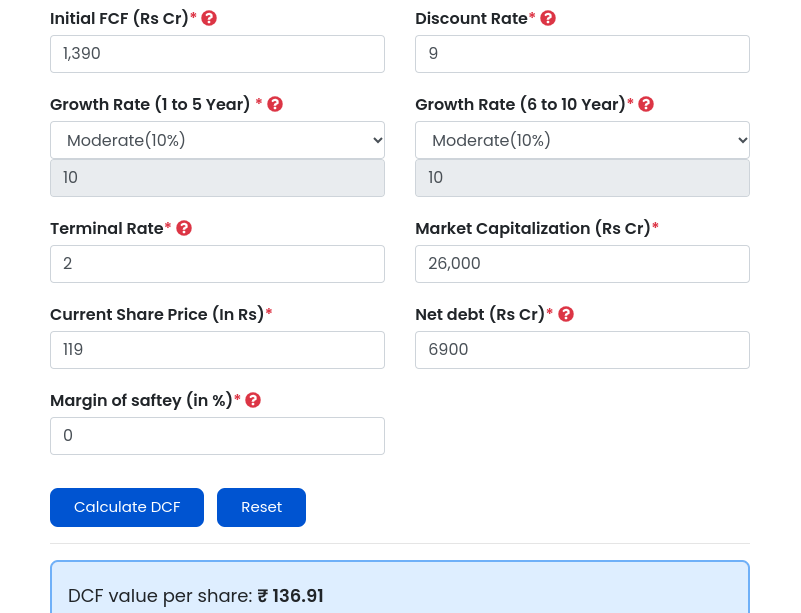

I'll be performing a conservative Discounted Cash Flow valuation to account for these risks. My assumptions include a 10% growth rate, 7% projected top-line growth by analysts for the next three years, a potential 3% reduction in shares outstanding through buybacks, 2% terminal growth, and a 9% discount rate, which is higher than the 7% WACC calculated by AlphaSpread to compensate for the associated risks. The initial FCF is based on a consensus forward revenue of $38.7 billion and the average FCF margin of the last 5 years.

The derived result indicates a 14% undervaluation, with an intrinsic value of $136. It's important to note that DCF models can be sensitive to changes. For example, if we assume a terminal growth of 3% instead of 2%, we get a 30% undervaluation, even with these fairly conservative inputs, suggesting that the stock is undervalued.

{kind=link}

Furthermore, Dollar General is trading significantly below its historical multiple averages , indicating potential for multiple expansions. This is a critical factor to consider in valuation, particularly for a company whose quality is in question.

{kind=link}

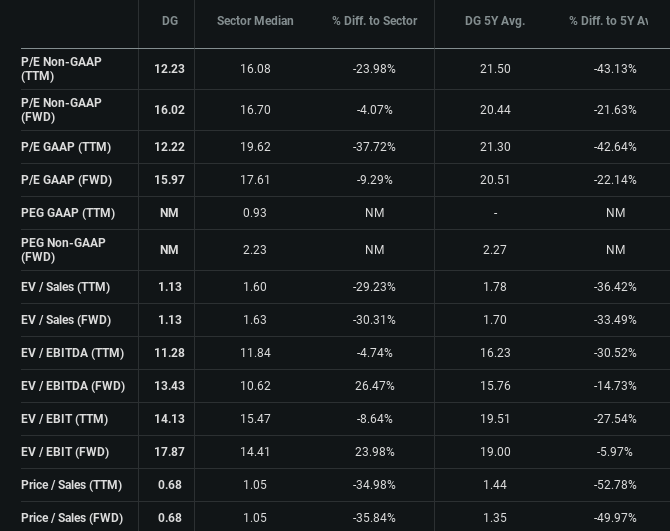

Dollar General is also priced attractively in comparison to its peers, which further suggests the potential for multiple expansion. However, this is contingent on a significant 'if' - if the uncertain economic environment stabilizes and DG manages to regain its previous free cash flow levels. I believe this is achievable.

In contrast, Dollarama hasn't experienced any significant setbacks recently, so we shouldn't expect significant discounts in its valuation. First of all, as shown in the chart above, Dollarama maintains a relatively high multiple, which indicates confidence in the company's quality and future prospects.

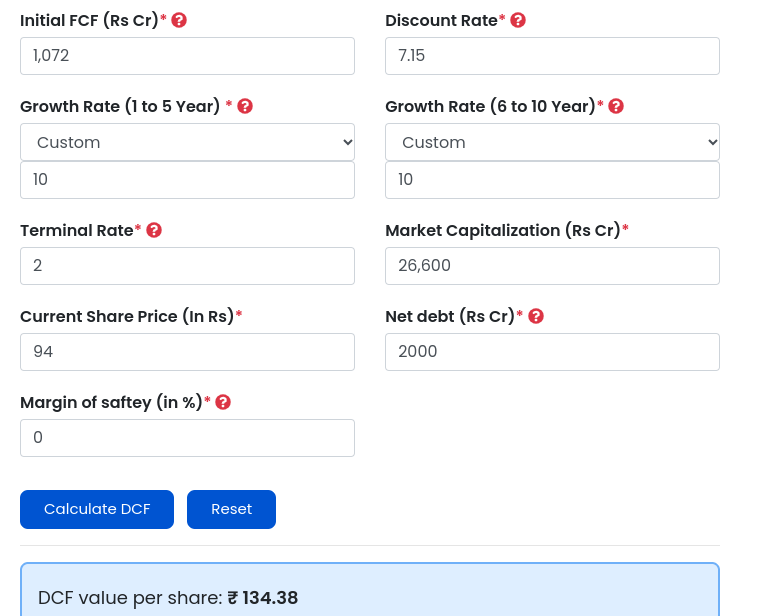

Now, let's consider a discounted cash flow valuation for Dollarama. Given my perspective of lower risks, I can afford to be less conservative. I'm assuming a 7.15% discount rate based on the WACC , a 10% growth in free cash flow based on anticipated revenue growth as per analysts' projections, and annual buybacks of about 2.5%. The terminal growth rate is set at 2%.

The result suggests an undervalued company by 42%, with an intrinsic value of $134. this calculation doesn't rely on overly conservative assumptions. In my view, a quality company like Dollarama, even considering its non-American status, is quite intriguing at this level of discount.

{kind=link}

Turning to multiples, a PEG ratio of 1.3 is reasonably attractive, and a forward FCF yield of 4.4% is excellent for this type of company. it's not currently trading below its historical averages, which might be less favorable to some, I personally prefer to invest when there is the potential for multiple expansion back to the mean. This adds an extra layer of safety to my investment approach.

Risks

The risks I see for DG include a challenging economic environment, which could adversely impact its customer base, as we are witnessing now. The issue of debt is particularly worrisome, and I wouldn't be surprised if, in the coming years, DG has to curtail its buyback program or reduce dividends due to the burden on the company's balance sheet. Additionally, growing competition and market maturation are also concerns for me. It's worth noting that DG's valuation, while not as attractive as when it was at $99 in early October, is still relatively cheap in certain models.

For Dollarama, I'm concerned about margin maturation. I believe that, as a retailer, there's a limit to how much you can expand your margins. A slowdown in this regard could lead to a deceleration in EPS growth, potentially resulting in multiple contraction. Furthermore, the competition in Canada could intensify with the expansion of Dollar Tree and other local players. While the valuation appears favorable in the DCF model, I'm cautious about buying above the multiple averages, as I don't see an upper target for this.

Conclusions

In the end, it all boils down to the risk-reward balance. I see Dollarama as a high-quality company with a track record of consistent performance and no recent setbacks. Moreover, it appears to be reasonably priced. On the other hand, Dollar General, while trading at a more favorable price, is less appealing based on the parameters I examine (ROIC, growth, margins), and it has faced significant challenges recently.

As an investor who leans more towards Growth at a Reasonable Price and quality companies, my obvious choice is Dollarama. I rate it as a BUY because I believe the risk-reward ratio is in favor of investors. However, if the price were a bit lower, say in the $80s, it would undoubtedly be a strong buy for me.

Dollar General, on the other hand, doesn't align with my investment preferences. I prefer businesses with rock-solid balance sheets and high ROIC, and DG doesn't meet those criteria. In my view, the price isn't low enough to compensate for the associated risks, so I rate it as a HOLD.

I look forward to reading your thoughts in the comments.

For further details see:

Dollar General Vs. Dollarama: Value Vs. Quality