DG - Dollar Tree: Don't Be Fooled By The Solid Revenue Growth

2023-11-21 05:49:07 ET

Summary

- Dollar Tree demonstrates a solid ability to drive revenue growth in the current weak macro environment as consumers are becoming more price-conscious.

- However, despite impressive revenue growth, profitability metrics are shrinking, which is a red flag for potential investors.

- My valuation analysis suggests the stock is significantly overvalued.

Investment thesis

Discount retail chains like Dollar Tree (DLTR) are the primary beneficiaries of the current high inflation environment and softening employment data. Consumers are becoming more cost-conscious in such unfavorable environments, and fixed-price offerings like DLTR's are becoming more appealing, especially for everyday non-discretionary items. Therefore, I am not surprised that the company demonstrates solid revenue growth and market share improvement in the current environment. However, the company's business model aiming at below-average earners also significantly limits its ability to pass on inflationary factors to customers. Moreover, my valuation analysis suggests the stock is significantly overvalued. All in all, I assign DLTR a "Sell" rating.

Company information

Dollar Tree is a discount variety store chain that operates over 16 thousand stores across 48 U.S. states and five Canadian provinces. The business is operated via two reportable segments: Dollar Tree and Family Dollar. According to the latest 10-K report , Dollar Tree generated 54% of the company's total revenue.

The major difference between the two nameplates is the approach to pricing. Most of Dollar Tree's offerings are merchandised at a fixed $1.25 price, and Family Dollar is more flexible in pricing. However, both segments are aimed at below-average-income customers.

Financials

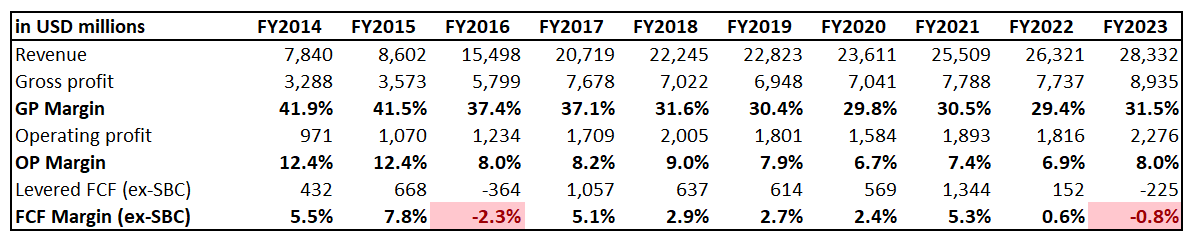

I have mixed feelings about DLTR's financial performance over the past decade. Revenue has tripled over the last ten years, indicating a massive 15% CAGR for the top line. However, DLTR's profitability metrics are in steady decline. The operating margin shrank from 12.4% to 8% over the decade, which is a warning sign. The same is true with the free cash flow [FCF] margin ex-stock-based compensation [ex-SBC], which has been below 1% in the last two full fiscal years.

{kind=link}

Having deteriorating profitability metrics despite massive revenue growth suggests that the management might be pursuing growth at all costs, which is not sustainable. The fact that DLTR struggles to improve the FCF margin results in a weak balance sheet with high leverage and a substantial net debt position. The quick ratio is razor-thin, which is crucial to underline. The current stance of the balance sheet does not position the company well to fuel further aggressive growth.

Seeking Alpha

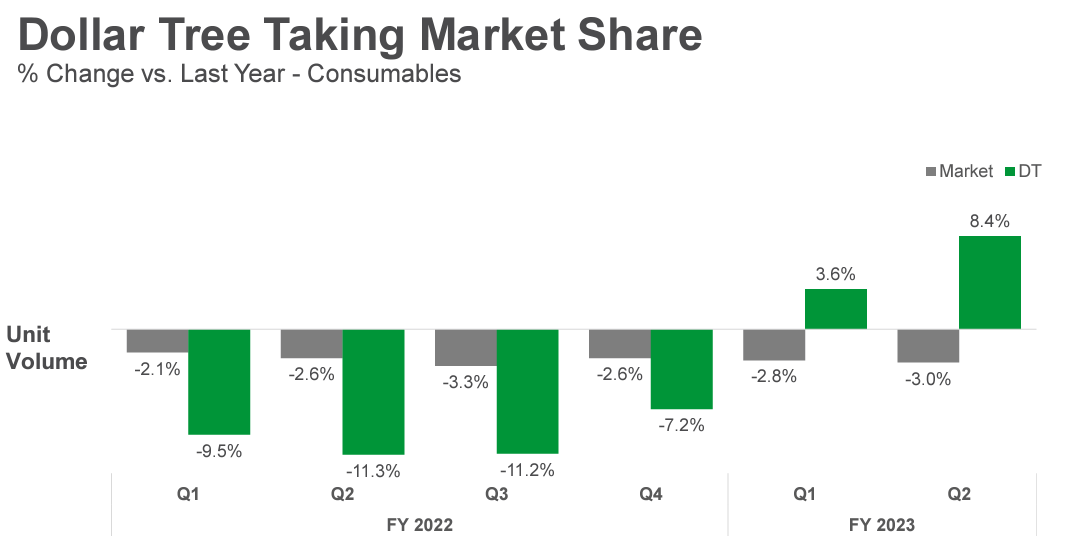

The latest quarterly earnings were released on August 24, when the company topped consensus estimates. Revenue grew by 8% YoY. Solid revenue growth was driven by increased traffic and higher sales per square foot. According to the earnings call, DLTR gained market share in consumables for the second consecutive quarter, and the company's unit volume growth outpaced the market.

Seeking Alpha

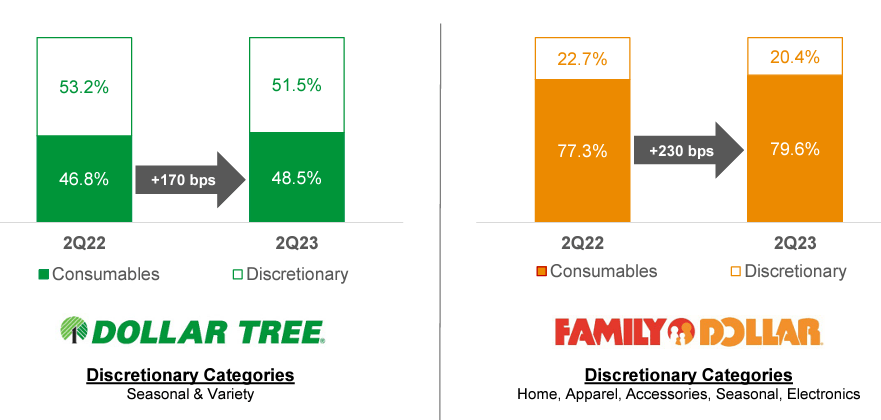

Despite revenue growth, a notable decrease in profitability metrics occurred. The operating margin declined YoY from 7.5% to 3.9%. The weakness in operating leverage happened due to various factors. The less favorable revenue mix was a significant reason, as the portion of more profitable discretionary categories declined both in Dollar Tree and Family Dollar. Apart from the unfavorable sales mix, the lower merchandise margin also occurred due to inflationary pressures.

DLTR's latest earnings presentation

{kind=link}

The upcoming quarter's earnings release is scheduled for November 29. Quarterly revenue is expected by consensus at $7.43 billion, which indicates a 7% YoY growth. Despite revenue growth, the adjusted EPS is expected to decline YoY from $1.20 to $1.01, meaning that the management expects challenges for the bottom line to be sustained in the foreseeable future.

Seeking Alpha

The ability of management to drive revenue growth is strong and was proved by many successful previous years. The harsh environment of high-interest rates and inflation is a tailwind for discounters like DLTR-the declining savings rate in the U.S. suggests that customers' pockets are draining, and people are likely to seek cheaper options for their everyday shopping. Increased traffic in DLTR's stores and increased market share is a clear indication that the demand for cheaper staples is growing.

DLTR's latest earnings presentation

{kind=link}

But the company's deteriorating profitability is a big elephant in the room. From the bottom line perspective, DLTR's business model is playing against it. We have seen an unfavorable secular trend for the company's profitability, and I do not expect significant profitability improvement in the near future either. Inflationary pressure is still high, especially given the fact that oil prices are still elevated despite very tight monetary policies across the developed economies. At the same time, positioning the major part of the business as fixed-price, DLTR has no room to pass on the inflationary factor to its customers.

To add context regarding DLTR's weakening profitability, I would also like to compare the company's operating margin trend to that of its closest rival, Dollar General ( DG ). While DG's operating margin has also deteriorated over the last decade, it demonstrated much stronger resilience than DLTR. The narrowing operating profitability of the industry's two prominent players suggests that this unfavorable trend is inherent to the industry as a whole. However, it looks like DLTR's management is less flexible in dealing with the headwind, which is also a warning sign for potential investors.

The profitability metrics of a good business shall expand as the business scales up, but we see the opposite for DLTR. Revenue more than tripled over the last decade, but profitability metrics were in a secular decline. The company's balance sheet is insufficient to expect sudden dividend payouts or generous stock buybacks.

Valuation

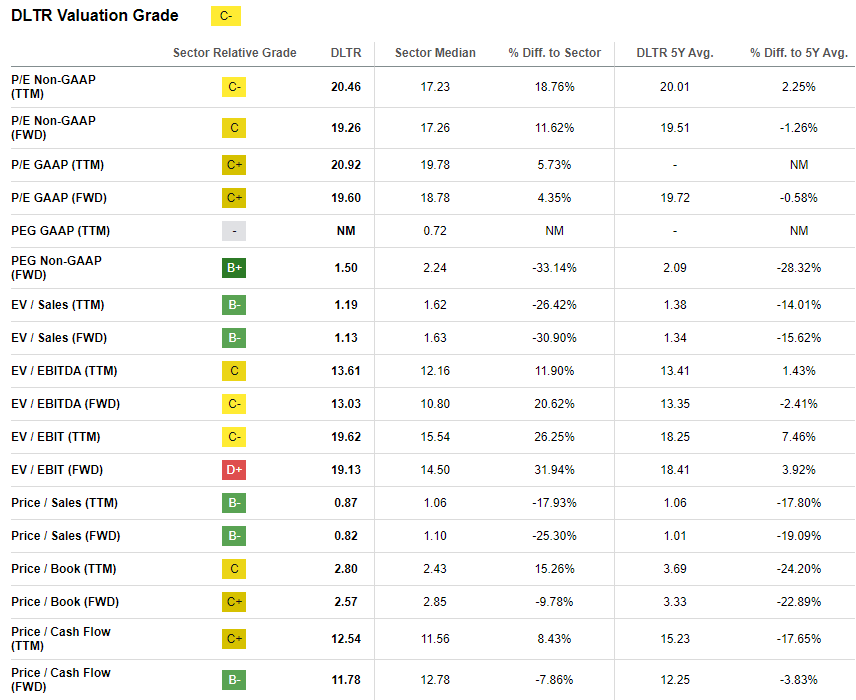

The stock price declined by 18% year-to-date, significantly underperforming the broader U.S. market. Seeking Alpha Quant assigns the stock an average "C-" valuation grade, meaning the stock is approximately fairly valued from the perspective of valuation ratios. Indeed, the current multiples are mostly in line with historical averages.

{kind=link}

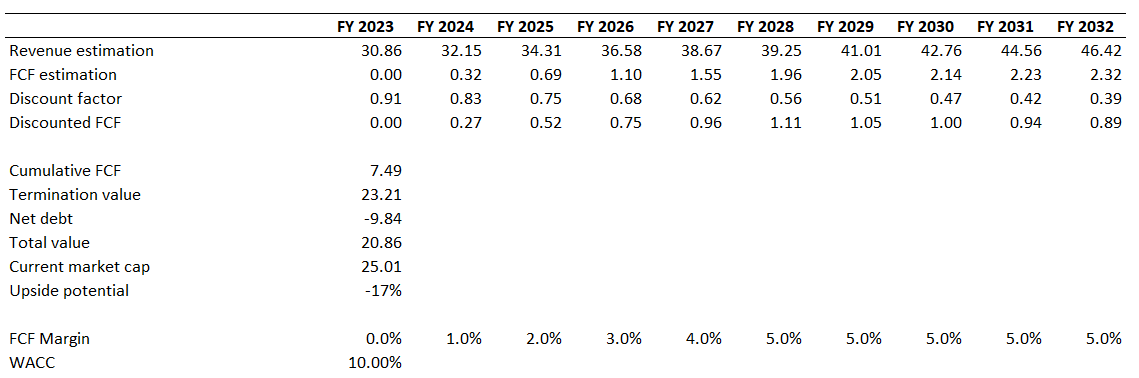

I want to proceed with the discounted cash flow [DCF] simulation. I use a 10% WACC for discounting. Consensus revenue estimates project a 5% CAGR for the next decade, which I consider fair enough to use for my DCF. I use a zero TTM FCF margin for the base year and expect a one-percentage point yearly expansion, with the metric peaking at 5%.

{kind=link}

According to my DCF simulation, the business's fair value is $21 billion. This means that the stock is about 17% overvalued. My fair price for DLTR is $95 per share.

Risks to consider

Timely breaking headlines can substantially influence stock prices, often leading to significant fluctuations in either direction. In case the management unveils a robust cost-efficiency plan with the prospect of yielding hundreds of millions in structural savings, such a development is likely to serve as a substantial positive catalyst for the stock price.

Elevated energy commodity prices are a vital factor pushing inflation higher. At the same time, we all know that a significant volume of global oil supply is under sanctions due to geopolitical tensions with oil-rich countries like Russia and Iran. A sudden improvement in geopolitical trends might be a strong catalyst for oil prices to go down. This will likely significantly ease inflationary pressures, which might help to improve DLTR's profitability.

Bottom line

To conclude, DLTR is a "Sell". Despite the expected revenue growth, profitability, and FCF prevail over the long term in building shareholder value. And from the point of view of profitability, the picture does not look well. While profitability deterioration is a problem for the whole industry, it looks like the company's primary rival is dealing with the secular headwind in a much more efficient manner. Moreover, my valuation analysis suggests the stock is significantly overvalued even after a year-to-day price decline.

For further details see:

Dollar Tree: Don't Be Fooled By The Solid Revenue Growth