DLTR - Dollar Tree: Positive Traffic Growth Being Overlooked

2023-05-25 09:58:24 ET

Summary

- Shares of Dollar Tree have been outperforming in 2023 due in part to high expectations for new CEO Rick Dreiling's turnaround plan.

- This plan includes major upfront investments in areas such as labor and wages, store upgrades, and other corporate initiatives.

- Despite the near-term headwinds on earnings that were expected, investors appeared largely optimistic, at least based on the share price.

- The bid-up in the shares, however, exposed the stock to a pullback on any disappointment in their earnings release.

- Though investors didn't like the lowered revisions on earnings, I view positive trends as a key offset. And I believe these trends are being overlooked.

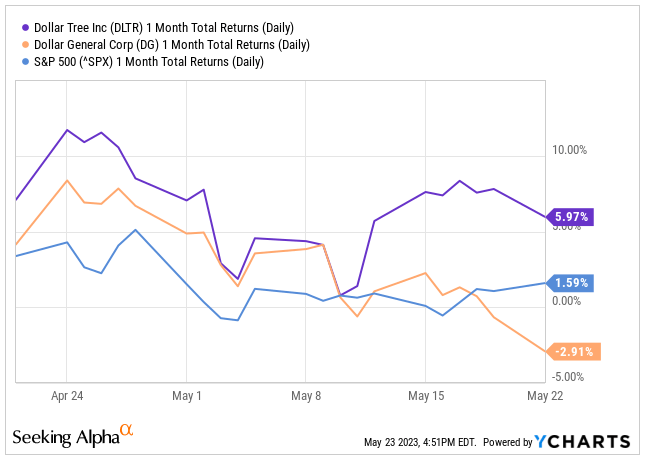

The recent share price performance of Dollar Tree ( DLTR ) in relation to peer, Dollar General ( DG ), and the broader market in general would suggest expectations were high for the company heading into the Q1 release.

Over the past month, for example, shares were up about 6% in the days prior to their report. This compares favorably to a decline in DG and a less than 2% increase in the broader S&P 500 ( SPY ).

{kind=link}

YCharts - 1-MTH Returns Of DLTR Compared To DG And The Broader S&P

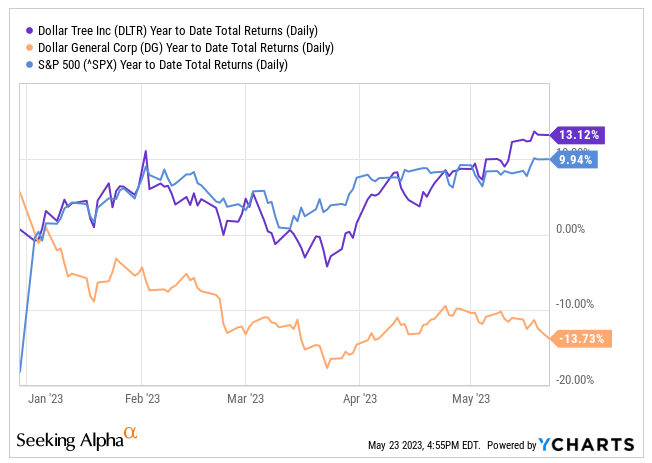

The stock is also riding high on a YTD basis, up about 13%.

{kind=link}

YCharts - YTD Returns Of DLTR Compared To DG And The Broader S&P

The outperformance is despite a planned reset that called for weaker operational performance through 2023. The run-up in the shares, then, could largely be attributed to enthusiasm for new CEO Richard (“Rick”) Dreiling ’s turnaround vision for the company. At the beginning of the year, he noted that DLTR would accomplish in three to five years what would normally take most others much longer to complete.

But to get there, he was expecting large upfront investments in the current year, which was initially expected to weigh on results. Nevertheless, investors were still optimistic enough to bid up the stock in advance of earnings.

I don't find it surprising, then, to se e it pull back foll owing their earnings release that guided for lower full-year earnings on expectations for elevated shrink. While the instant reaction was to sell, I believe positive traffic growth in both units is being overlooked. As such, I would find any weakness in the stock as an attractive entry point for long-term investors.

What Did DLTR Expect Heading Into Their Earnings Release?

Through an accelerated turnaround plan under the new CEO, DLTR expected significant upfront investments in areas such as labor and wages, store upgrades, and other corporate initiatives. They also were transparent in noting that they were expecting a minimal return on these investments, at least in the near term.

All considered, they were expecting a +$430M increase in SG&A costs for 2023 or $1.45 on a per share basis. In addition, they were expecting a +$2.0B CAPEX pipeline, slightly above the +$1.8B to +$1.9B range provided by DG .

On the bottom line, they guided for earnings of $6.55/share at the midpoint, which would have represented a 9% decline from their 2022 actuals. It’s worth noting that before their Q4 update, consensus estimates were for about a 6% increase.

Following their Q4 release, the stock was subject to a downgrade from JPMorgan to a “neutral” rating from “overweight” previously. Driving the revision were expectations of a deterioration following a near-term peak.

In addition, Raymond James assessed DG higher on their pair trade idea between the two companies, citing DLTR’s multi-year turnaround plan as one headwind that would put them even further behind DG. This, however, was counteracted by positive commentary from analysts at Gordon Haskett on optimism surrounding Rick’s new stewardship and vision for the company.

Did DLTR Meet Expectations?

In the first fiscal quarter of 2023, DLTR reported total consolidated net sales of +$7.3B and adjusted diluted EPS of $1.47/share. While total revenues were in-line, earnings fell short of estimates .

In their namesake unit, DLTR delivered comparable sales growth of 3.4%. While this is a lower rate of growth than in prior quarters, it's worth noting the significant tick higher in traffic growth, up 5.5%.

This represents a 660 basis point ("bps") improvement sequentially and would be a build on top of the 410bps improvement in Q4. Also noteworthy is that the higher traffic levels came on negative average tickets.

Q1FY23 Earnings Release - Summary Of Operational Performance In Namesake Unit

Even more promising is results in their Family Dollar unit. Here, comparable sales were up 6.6% on both traffic and average tickets. The significant bump in traffic levels comes after several quarters of either negative or meager growth. The improvements here provide confidence that the current turnaround efforts are working.

Q1FY23 Earnings Release - Summary Of Operational Performance In Family Dollar Unit

On an overall enterprise basis, same-store sales were up 4.8%. Unfavorable product mix that was weighted more heavily to the lower margin consumables did drive margins lower to 30.5%.

But this isn't significantly off from the 30.9% that they reported in the prior quarter, especially when considering the headwinds from elevated inventory shrinkage.

Higher costs resulting from their turnaround efforts did result in much lower operating margins in the period. Adjusted operating margins in Q1, for example, was 6.1%. This compares to 8% last quarter. Higher SG&A was largely to blame, as it jumped from 22.9% of revenues last quarter to 24.8% in Q1 or 24.4% on an adjusted basis.

What Does DLTR Expect Moving Forward?

Though the full-year sales outlook was maintained, the adjusted EPS range was paired to a range of $5.73/share to $6.13/share or $5.93/share at the midpoint. This would be a significant pullback from the prior midpoint of $6.55/share.

The major culprit for the revisions include elevated shrink and a continued shift toward lower margin consumables. Lower freight charges, however, are expected to provide a partial offset, though the earnings benefit is expected to be more back-end loaded.

Looking ahead to Q2, management sees consolidated net sales in a tight range of +$7.0B to +$7.2B, with earnings expected at $0.84/share at the midpoint.

What To Do with DLTR Following Earnings?

A key aspect of my bull thesis for DLTR stock is store traffic. In my prior coverage of the stock, the company was off their Q3FY22 results. At that time, positive topline results were reported. But traffic figures underwhelmed, and the stock turned lower, accordingly.

In Q4FY22, the traffic figures began to show more signs of improvement. Their Family Dollar unit, for example, turned in their second straight quarter of positive traffic growth. And there was also a 410 basis point improvement in their namesake as well.

The improved traffic levels in combination with increased optimism surrounding Rick Dreiling’s turnaround efforts resulted in recent outperformance, in my view.

Given the recent run-up, shares were at risk of a pullback on any disappointment in their most recent earnings release. And this disappointment did come in the form of a paired outlook on earnings due to elevated shrinkage.

While the news on shrink is important, what I view as more important is the positive improvement in traffic levels. In fact, the improvements are significant, especially in their namesake, which saw the effects of traffic growth more than offset weaker tickets. The bump up in traffic growth in their Family Dollar unit to the mid 4% range is even more notable.

Given the positive developments in their traffic levels, which appears to be validating their current investments in their turnaround, I'm maintaining my bullish view on the stock.

At present, shares trade at a sizable premium to DG, at 24x forward earnings versus about 19x for DG. In addition, consensus price targets for DLTR currently stand at about $158/share, which doesn’t represent material upside from current trading levels.

I, however, foresee above-average earnings growth in future periods resulting from current initiatives. At a 20x multiple of future EPS, I can see shares trading fairly in the $180/share range. Any weakness in the interim, therefore, would be viewed as an attractive buying opportunity.

For further details see:

Dollar Tree: Positive Traffic Growth Being Overlooked