DLTR - Dollar Tree Q3 Earnings Preview: Eyeing Potential Reversal In Sales Mix As One Forward Catalyst

2023-11-27 08:00:00 ET

Summary

- Dollar Tree is set to report Q3 results on Wednesday prior to market open.

- Leading up to the release, shares have lagged the broader markets, with double-digit percentage losses.

- While traffic trends have been positive, the company has been stung by margin pressure due to rising costs, unfavorable product mix, and elevated shrink.

- Against a difficult macroeconomic backdrop, a heightened desire for value from consumers could have benefited DLTR’s discretionary offerings in the most recent quarter.

- Heading into the release, I remain bullish on DLTR’s long-term prospects despite the bearish sentiment on the stock.

Dollar Tree ( DLTR ) is heading into its Q3 reporting period with double-digit percentage YTD share price losses since my last update shortly after its Q1 release. At the time, I expressed optimism on DLTR’s turnaround progress under the helm of CEO Rick Dreiling. I was also bullish on the positive trends being reported on store traffic levels.

I’ve maintained a bullish stance despite the continued share price weakness. Though shares are up about 9% over the past month, the stock still has further to run, in my view. For investors seeking positioning, I believe DLTR presents upside potential of over 20% from current trading levels. In advance of earnings, here’s what investors should know about DLTR.

DLTR Key Stock Metrics

Shares in DLTR were nursing YTD losses of over 16% through the U.S. Thanksgiving Day holiday. The broader S&P ( SPY ), in contrast, was up about the same in the other direction over the same period.

Despite the losses, the stock still trades at a forward multiple of just under 20x, in line with the larger market index.

Seeking Alpha - YTD Returns Of DLTR

{kind=link}

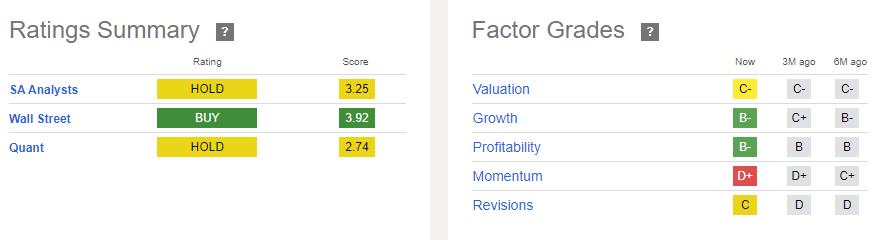

The premium valuation, as well as DLTR’s negative momentum in recent months, are two reasons why Seeking Alpha’s quant ratings grade shares as a “hold” at current trading levels. EPS targets have also been negatively revised by consensus analyst estimates, another headwind on DLTR’s quant grading.

Seeking Alpha - Quant Ratings Summary Of DLTR

{kind=link}

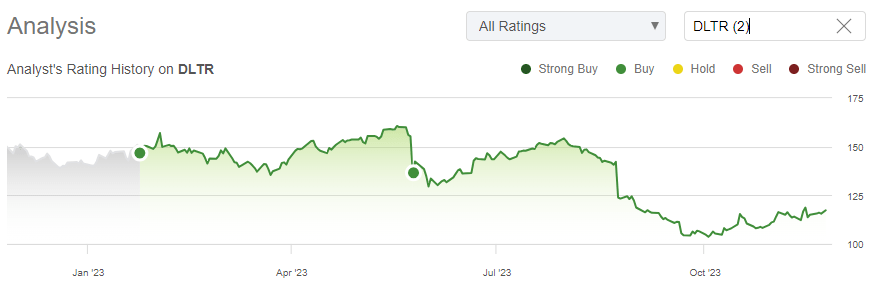

The SA Analyst community also views the stock neutrally, with just two “buy” ratings since June. This contrasts with my past two bullish ratings, both prior to the Q2 release, which disappointed investors and analysts, alike.

Seeking Alpha - Author Ratings Summary Of DLTR

{kind=link}

It also differs from consensus Wall Street targets , which see upside of over 20% in the stock. In October, Goldman Sachs ( GS ) turned bullish and affixed a price target of $137/share, citing strong earnings growth potential and improving store traffic trends, among other factors.

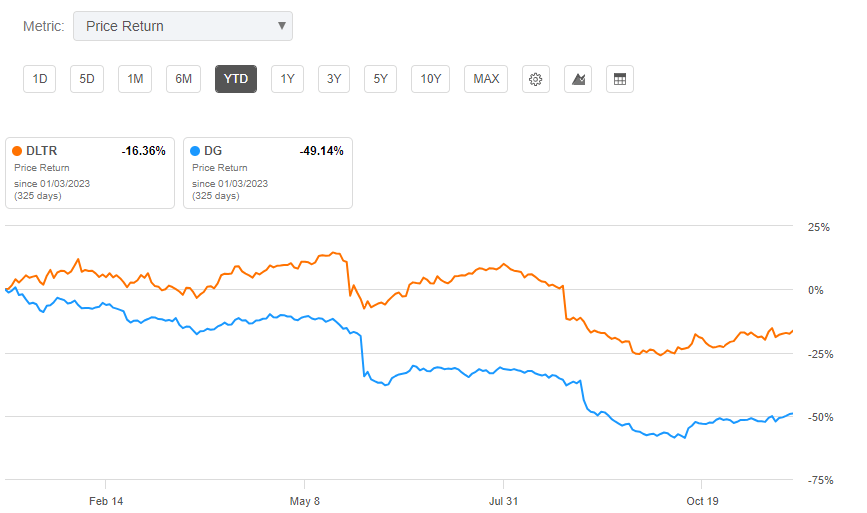

DLTR has also fared better in the eyes of investors than its closest peer, Dollar General ( DG ), who is down 50% YTD and is currently going through its own transitional period following the return of its former CEO, Todd Vasos.

Seeking Alpha - YTD Returns Of DLTR Compared To DG

{kind=link}

DLTR Q3 Guidance And Expectations

In conjunction with DLTR’s Q2 release , CFO Jeff Davis reaffirmed the midpoint of DLTR’s full-year earnings guidance. But he narrowed the range, with an uptick at the lower end and a downward revision at the upper.

At $5.93/share, the midpoint is also well below consensus estimates of $6.02/share. It was this underwhelming guidance that was primarily to blame for the post-release share price weakness.

Driving the full-year guidance are factors such as sales mix and unfavorable shrink trends. In addition, the guidance also accounts for the higher costs associated with DLTR’s continued turnaround efforts, including higher R&M and labor costs.

More specifically to Q3, DLTR is expecting a mid-single-digit percentage increase in comparable store sales, with total consolidated sales landing in the range of +$7.3B to +$7.5B. And from an earnings perspective, DLTR sees diluted EPS at a midpoint just shy of $1.00/share at $0.99/share.

What To Watch When DLTR Reports Q3 Results

Sales Mix: Much like other retailers, DLTR has cited unfavorable product mix as one headwind on overall margin strength. This stems from the shift in consumer spending from the discretionary categories to the lower-margin consumable items.

DLTR Q2 FY23 Earnings Presentation - Quarterly Sales Metrics By Quarter

The mix has tempered otherwise strong data on sales. In Q2, for example, comparable sales were up 6.9%, ahead of consensus estimates for a 5.7% increase. But the greater weighting to the consumable categories held back gross margins in both of DLTR’s operating units.

While the management team did guide for a continued headwind in mix through the remainder of the fiscal year, this is one metric I can see coming in better than expected. Last year in Q3, DLTR saw an overall improvement in mix in the back half of the year, particularly in its Family Dollar unit. This coincided with back-to-school and the holiday seasons. With value-based shopping even more important this fiscal year, DLTR is one retailer that could have been a beneficiary of selective consumer spending.

Shrink: Another headwind for DLTR that has been common elsewhere is theft. In Q2, CEO Rick Dreiling noted that DLTR would be taking additional steps to safeguard inventory levels. Aside from moving and locking selective units of merchandise, Dreiling also left open the possibility of discounting the more heavily targeted items. The costs associated with these preventative measures subtracted from DLTR’s full-year guidance, adding to investor disappointment.

While shrink is still a concern among retailers, it hasn’t been as significant of a theme for those retailers that have reported thus far. This provides some degree of confidence that DLTR could have positive news to share on this front when results are released on Wednesday.

Margins: In Q2, operating income in DLTR’s namesake and Family Dollar segments declined 27.8% and 78.8%, respectively. Driving the declines in each respective unit were a combination of gross margin pressure and rising SG&A costs associated with the company’s turnaround efforts, primarily in the form of rising wages and R&M-related expenses on their storefronts.

Any improvements in mix or a positive turn in shrink could lead to better-than-expected margins in both units. While I do see SG&A costs continuing to rise from additional store openings, I can see some of this pressure being relieved by improvements in both mix and shrink.

Is DLTR Stock A Buy, Sell, Or Hold?

Following a strong run to new 52-week highs earlier in the year, a confluence of factors have sent shares of DLTR lower through the second half of the fiscal year. While positive foot traffic and market share gains have been positive notes, a more pronounced consumer weighting to consumables has strained margins. And this has occurred simultaneously as DLTR is incurring rising SG&A costs related to ongoing transformation efforts.

Walmart ( WMT ) has also likely taken share from both Dollar Tree and Dollar General in both the discretionary and consumables categories.

Despite rising costs and increasing competition, DLTR still sees full-year EPS at $10/share or more by 2026. If achieved, that would mark a significant milestone from the mid-single-digit earnings estimate of the current year. One can debate whether this is likely to come to fruition. But in my view, the milestone is attainable under the current leadership of current CEO Rick Dreiling, one who has already shown adeptness at navigating through a challenging operating environment, whether it be increasing enterprise traffic levels or leading positive unit growth in the consumables category.

In my view, bearish sentiment on the stock in recent months via negative earnings revisions and the lack of forward momentum provide shares a healthy buffer for a bounce in the event of any notable beat. I can see this occurring either through a better-than-expected sales mix and/or profit outlook. I’ve maintained a bullish stance on DLTR in prior coverage, and I maintain the bullish view heading into the Q3 print due to an improving discretionary spending outlook and a more favorable environment for margin strength.

For further details see:

Dollar Tree Q3 Earnings Preview: Eyeing Potential Reversal In Sales Mix As One Forward Catalyst