DG - Dollar Tree: Strong Potential But Can New Management Execute On Turnaround Plans?

2023-08-02 19:11:28 ET

Summary

- Dollar Tree and Dollar General are leading discount variety retail store operators in North America.

- Dollar Tree has struggled since its acquisition of Family Dollar in 2015, but recent changes by activist investor Mantle Ridge have sparked a turnaround.

- Dollar Tree's investment in upgrading its stores, supply chain, and IT systems should position it as a strong competitor to Dollar General.

- The expansion of multi-price point product offerings over time could attract cash-strapped customers from Walgreens, CVS, convenience stores, and local mom and pop stores who extract premium prices by virtue of their locations.

Overview

Dollar General Corporation ( DG ) and Dollar Tree Inc. ( DLTR ) are two leading operators of discount variety retail stores in North America.

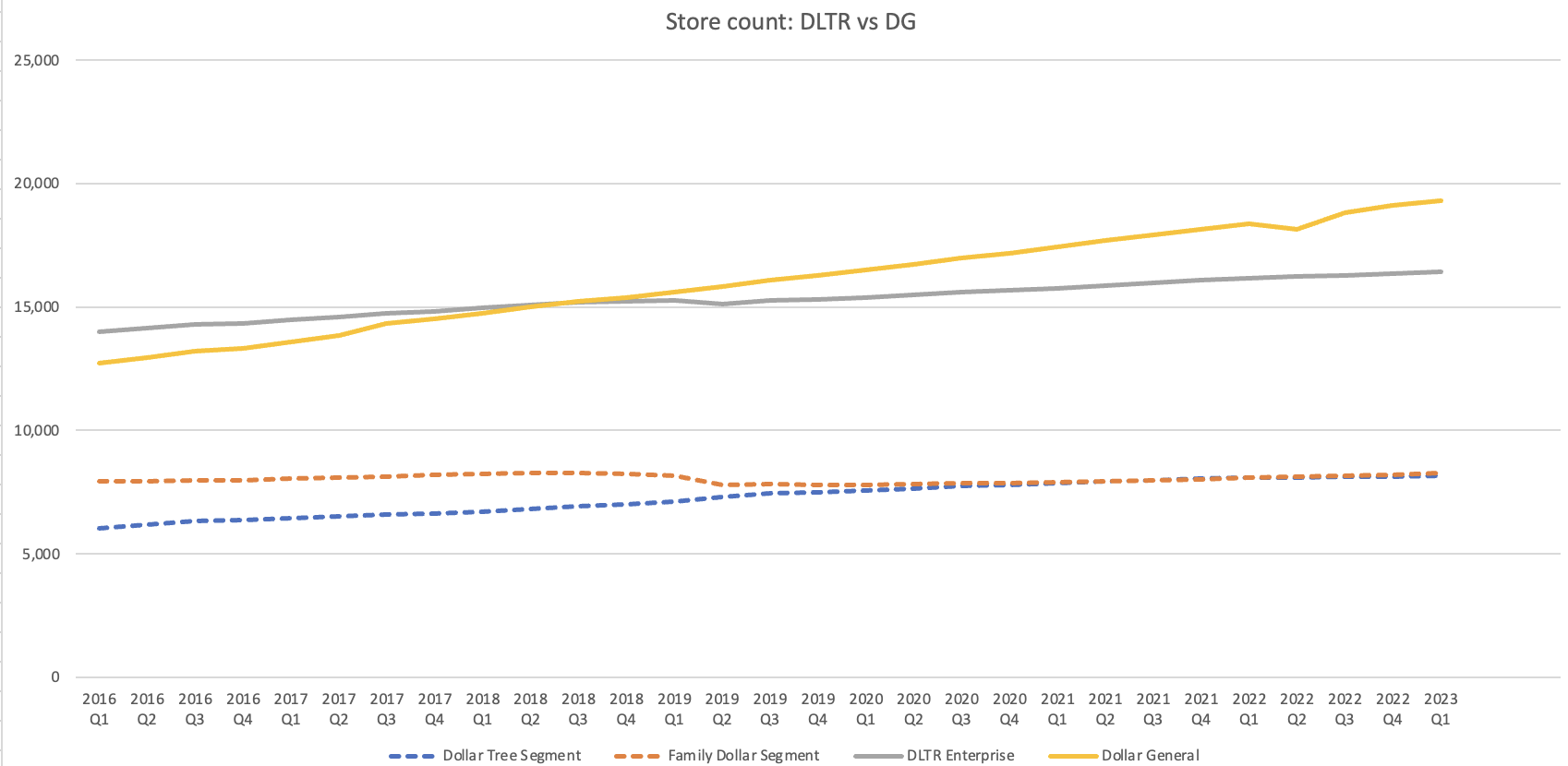

Dollar Tree Inc. operated 16,419 stores (Figure 1, grey solid line) in two segments: Dollar Tree Stores (blue dashed line) and Family Dollar Stores (orange dashed line)—a public company which it acquired in September 2015. Dollar Tree Stores offer merchandise at a fixed price of $1.25 in both the US and Canada, while Family Dollar Stores, like competitor Dollar General, offers a broader variety of general merchandise across a wider range of price points.

Dollar General has expanded more quickly than Dollar Tree since 2016, and operated 19,294 stores as of Q1 2023 (yellow solid line).

Figure 1 Store count: Dollar Tree vs Dollar General

Author based on company financial data

{kind=link}

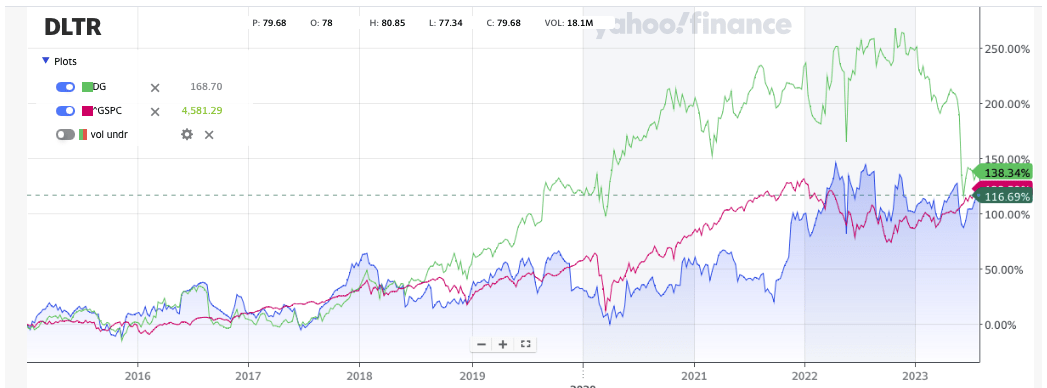

After Dollar Tree’s 2015 acquisition of Family Dollar, its stock price went sideways for six years as the company struggled to fix Family Dollar’s weak operations and integrate the supply chain of Dollar Tree Stores with Family Dollar’s (Figure 2, blue line). However, the stock jumped in the fourth quarter of 2022 after activist investor Mantle Ridge LP acquired a 5.66% equity stake plus 4.19% in cash-settled derivatives, revamped the entire management team, reconstituted the board of directors, and announced major investments for the future.

In contrast, Dollar General’s stock price has climbed steadily over the same period of time but pulled back sharply over the last three quarter after it missed earnings and warned of macroeconomic headwinds (Figure 2, green line). Over the last eight years, Dollar General has outperformed the S&P 500 index (red line) even after the recent pullback, while Dollar Tree has slightly underperformed the S&P 500.

Figure 2 Stock price comparison vs DG, S&P 500

{kind=link}

This is a detailed update to my May 14, 2023 article titled Dollar Tree: Expect Higher Risk And Potentially Higher Returns . In this analysis, I have included new information from the company's recent investor day presentations.

Investment thesis

On June 23, Dollar Tree conducted its 2023 Investor Day event for the investment community, in which it discussed the consequences of years of underinvestment by previous management, the long-term potential of the company, and the areas of investments needed to achieve its potential.

At the current price earnings ratio of 25x (discussed below in Figure 36), Dollar Tree’s valuation is attractive but will likely deteriorate in the near term as the company takes a longer-term view and invests substantially more in employee compensation, store upgrades, private label products, supply chain efficiencies, and IT systems. If the company executes well, its Family Dollar Store segment will become a credible competitor to Dollar General, while its Dollar Tree Store segment could enter and dominate the discount general merchandise category that offers cash-strapped consumers a much-needed alternative to local convenience stores and front of store pharmacy retailers.

An investment in Dollar Tree has some elements of the take-private plays in which experienced private equity managers acquire control of sub-optimally managed companies, revamp the management team and implement turn-around strategies which position the companies to compete more effectively in the future (a good example is KKR Inc’s ( KKR ) 2008 buyout of Dollar General). Even though Mantle Ridge did not acquire control of Dollar Tree, it was able to gain sufficient influence to effect significant changes, creating an opportunity for small investors to jump on the bandwagon and benefit from their hard work.

The current stock price of ~$150 is approximately 40% above Mantle Ridge’s $106.77 average entry price as reported by CNBC. This premium reflects the substantial progress in the turnaround orchestrated by Mantle Ridge—it has rebuilt the management team with experienced and proven members, reconstituted the board, put in a well-developed strategy, and begun implementing turnaround plans.

An investment in Dollar Tree will be largely a bet on the ability of the new management team installed by Mantle Ridge to execute on its turnaround strategy. There is risk, and the variability in outcomes is hard to quantify. As such, the decision on whether to invest comes down to a qualitative judgement call over financial numbers.

Considering the new CEO Richard Dreiling’s record at Dollar General, upgraded management team’s skillset and experience, credibility of the turnaround strategy, and potential long-term upside from repositioning Dollar Tree Stores, I believe the risk-return is favorable. However, this is an investment that requires close monitoring as investors need to ensure that the turnaround is on track and the Mantle Ridge team remains fully committed to the investment.

Dollar Tree’s reason for existence

Discount stores like Dollar Tree serve customers who need or love good deals. This includes segments of the population with very limited budgets, and reasonably affluent consumers “treasure hunting” for a good deal.

1. Customers with limited budgets who need affordable daily necessities:

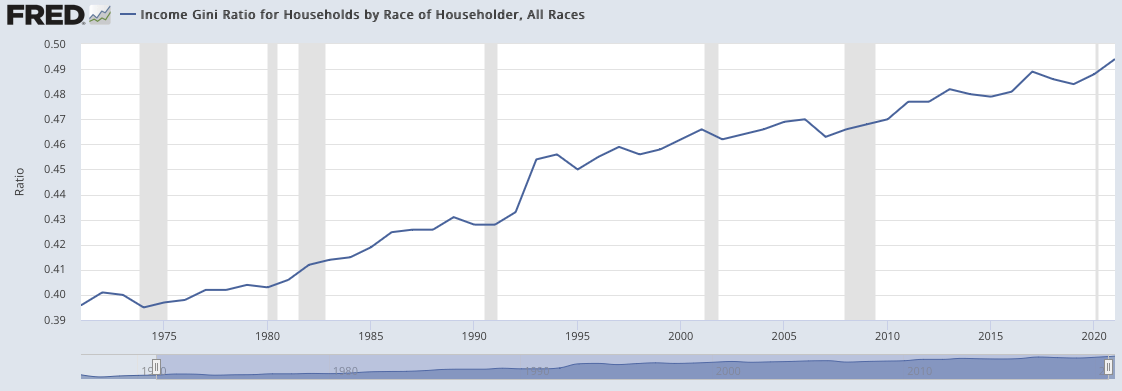

As documented extensively in the business and financial media, there has been a thinning out of the middle class and polarization of the US demographics—wealth in North America is increasingly concentrated amongst the rich and the base of lower income earners is expanding (Figure 3). The inevitable trends of robotics, artificial intelligence, and off-shoring continue and will cause more and more jobs to be replaced by cheaper and more efficient machines, computers, and overseas labor.

There is also a large base of undersaved retirees—seniors living on very small (as low as $500) monthly social security checks (of which $100 goes to Medicare) who are forced to do seasonal labor work (e.g., at Amazon warehouses) while living out of their cars or campers—a phenomenon depicted in Nomadland, the winner of the best movie in the 2020 Academy Awards.

Figure 3 Income GINI Ratio for US households

FRED: St. Louis Federal Reserve

{kind=link}

In addition, there is a base of woefully undersaved baby boomers that is approaching retirement. According to a September 2018 report from the Transamerica Center for Retirement Research titled “ A precarious existence : how today’s retirees are financially faring in retirement”, the life savings of the average baby boomer is USD152,000. Assuming those savings are spent over 20 years, the annual cash available is USD8,000, which, when added to annual social security payments of USD17,000, yields a total of USD25,000, which doesn’t go particularly far in today’s inflationary environment. Unfortunately, it is not easy for impending retirees to play catchup because of the subtle but very real job discrimination faced by older workers and the fact that time has run out for them to compound capital. Boomers nearing retirement are not in a position to take on meaningful equity risk as it is a time they should be shifting into safer fixed income-type instruments.

This base of low earners and undersaved retirees will only continue to expand, which creates an increasingly greater need for stores that are able to offer daily necessities and general merchandise at low price points to meet living necessities. To expand product offerings beyond bread and dried cereal, Dollar Tree has been renovating its stores to include refrigerated sections that sell frozen meals, steaks, and vegetables, making fulfilling and nutritious meals available for just a few dollars.

2. The mass affluent who want a good deal

Judging from the number and popularity of Dollar Tree stores in reasonably affluent suburban markets (just visit a nearby store on weekends), middle- and upper-income consumers love treasure hunting for great bargains in these clean and well-organized stores. Consumers who used to cringe at having to pay Radio Shack $6 for the cable to connect their iPhone to the AUX jack in their car can now buy the same cable at their local Dollar Tree Store for $1.25.

From North Asia through Southeast Asia (e.g., Japan, China, Malaysia, Singapore, and Indonesia), “mass-chic” value stores like Daiso, Mini-So and others have been sprouting up. In Singapore, there is a Daiso store in the ultra-high end Ion Mall in the heart of the fashionable Orchard Road shopping district, located near luxury stores selling Ferragamo leather goods, Louis Vuitton handbags, Van Cleef & Arpels Jewelry, and Vacheron Constantin timepieces, and the store is packed throughout the week.

I believe this is empirical proof that the highly affluent like bargains as much as the rest of us and represents an under-penetrated opportunity that Dollar Tree is well positioned to address.

3. Businesses that face cost pressures

Dollar Tree has revamped its website which previously appeared to be an afterthought into a well thought-through offering that targets businesses and organizations who need to buy supplies by the case but have to keep costs down (e.g., restaurants, care facilities, cleaning services, religious & non-profits).

While management has not discussed web sales in detail, this channel leverages the Company’s unique buying sourcing capabilities and efficient distribution, which could open up a sizeable untapped opportunity.

Looking forward:

Unfortunately, the number of lower income and undersaved retirees will inevitably grow over the next decade, and they will need a source of affordable living necessities. Everybody, rich or poor, love a bargain, and businesses need to keep their costs down more than ever. These trends will persist and Dollar Tree is well-positioned and equipped to serve these needs.

I believe Dollar Tree and similar discount stores have hardly penetrated the US retail landscape—there is plenty of white space to open more new stores, and the company will likely expand and dot the North American retail landscape like Starbucks cafes, Dunkin outlets, and McDonalds restaurants. Dollar Tree’s multi-price strategy (discussed below) will accelerate the company’s penetration into this segment.

Family Dollar and Dollar Tree Stores—a tale of two cities

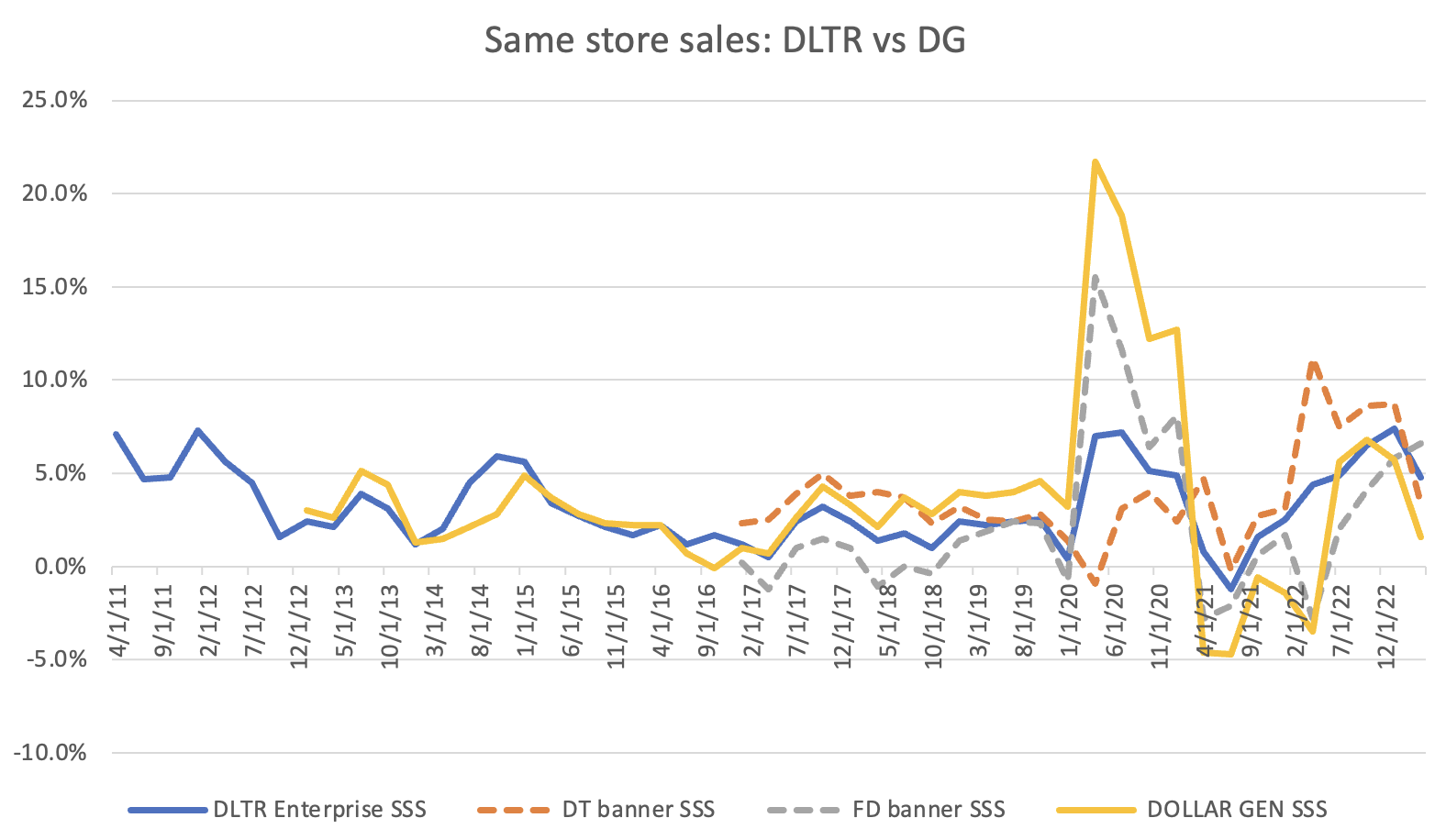

The company’s Dollar Tree Store segment has performed reasonably well on a same-store sale basis (Figure 4, orange dashed line). In contrast, the Family Dollar Store segment has, apart from the three quarters following the imposition of the COVID-19 lockdowns when it was allowed to stay open, underperformed due to its suboptimal operations (grey dashed line). Management found that the Family Dollar Store segment was losing share to competitors as it is unable to price its products competitively due to its sub-par operations.

Figure 4 Dollar Tree Inc segment same store sales growth

Author based on company financial data

{kind=link}

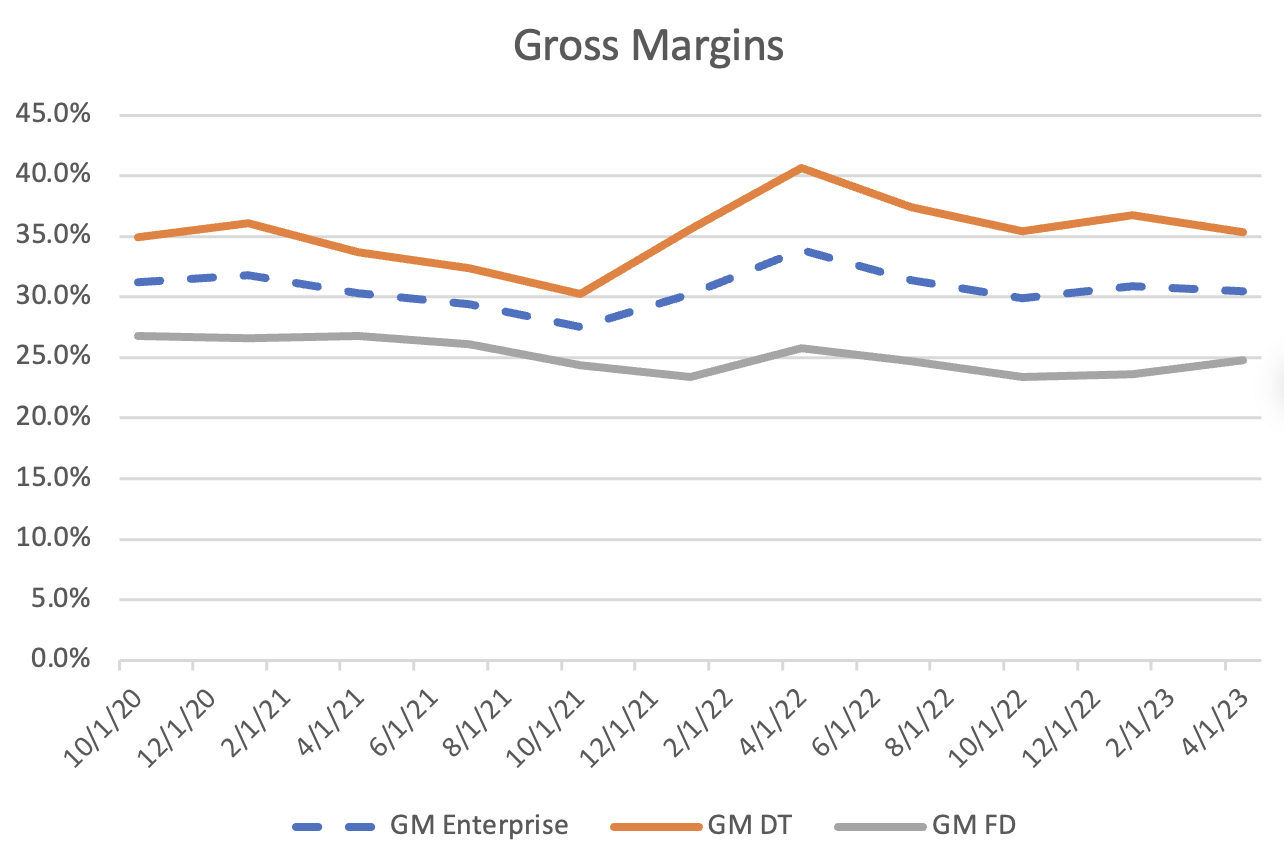

The Dollar Tree Store segment gross margins have been as much almost 1,000 basis points higher than the Family Dollar Segment (Figure 5, orange vs grey solid lines).

Figure 5 Dollar Tree Inc segment gross margins

Author based on company financial data

{kind=link}

While the Dollar Tree Store segment operating margins have averaged around 15% over the last three years (Figure 6, orange line), the Family Dollar Store segment operating margins have steadily declined to around breakeven (grey line), indicating the failure to improve the efficiency in the latter’s operations or derive integration synergies between the two segments.

Figure 6 Dollar Tree Inc segment operating margins

Author based on company financial data

{kind=link}

In Q4 2022, the company responded by implementing “price investments” at the Family Dollar Store segment--cutting prices to ensure its products were priced in-line with its competitors’. This resulted in a tick-up in the segment’s market share and same store sales growth (Figure 4, grey line) However, operating margins have continued to fall to break-even levels (Figure 6, grey line), and are likely to remain weak until Dollar Tree management upgrades its supply chain—which is one of issues that will be described below.

(Interestingly, at Dollar General’s Q1 2003 earnings call, UBS analyst Michael Lasser asked management if Family Dollar’s “price investments” would cause a “race to the bottom”. Dollar General management did not deny it but responded that they needed to “get even sharper on certain items that matter”).

A new management team and reconstituted board

Over the last 15 months, 12 of the 14 officers listed on the leadership page of Dollar Tree’s website have been replaced. Four key positions (Chairman/CEO, Family Dollar Chief Merchandising Officer, Chief Supply Chain Officer, and Chief Information Officer) were filled by officers who had previously worked at Dollar General. The only two members who have not been replaced were Neil Curran, who heads Dollar Tree Canada, and Rick McNeely, the Chief Merchandising Officer for the Dollar Tree Store segment. However, Rick McNeely's Family Dollar Merchandising responsibilities were shifted to Larry Gatta, a new hire from Dollar General.

Chairman and CEO : In March 2022, Richard Dreiling was elected to the board as Chairman under the Mantle Ridge Stewardship Framework Agreement, replacing then-Chairman Bob Sasser, who was also previously CEO of Dollar Tree. In January 2023, he took over the role of CEO from Mike Witynski.

Richard Dreiling previously served as Chairman and CEO of Dollar General from 2008 after it was taken private by Kohlberg Kravis & Roberts & Co. ( KKR ) till 2016, and delivered a strong return for both KKR and investors after the company went public.

Under Mantle Ridge’s leadership, the company has hired several former senior Dollar General executives to head key areas that are in need of fixing.

Chief Supply Chain Officer : Mike Kindy, who joined Dollar Tree in May 2023, was previously Executive Vice President at Dollar General, accountable for supply chain strategy, including transportation, distribution, demand chain, allocations, procurement, and master data management. While at Dollar General, Kindy oversaw the addition of nine traditional distribution centers, the inception of the DG Fresh supply chain, and the creation of the DG private fleet, which gave Dollar General more operational control of its supply chain.

Kindy is well-credentialed to revamp the Family Dollar segment’s under-developed supply chain, one of the critical areas in dire need of fixing. As Richard Dreiling noted on the Q2 2022 earnings call:

“In terms of the supply chain side, we’re looking at everything in the supply chain. We are assembling, I think Mike would agree, probably one of the best supply chain teams in the country. We have a lot of distribution centers that need to be updated and modernized .

I believe that a successful update and modernization of Dollar Tree’s enterprise supply chain is essential to drive efficiency and profitability for both the Family Dollar and Dollar Tree segments.”

Mike Kindy replaced John Flanigan, who joined Dollar Tree as Chief Supply Chain Officer in May 2022 after retiring from a similar role at Dollar General in 2016. I was not able to find any information on this change.

Chief Merchandising Officer, Family Dollar : Larry Gatta, previously served as Senior Vice President and General Merchandise for consumables at Dollar General. (As I noted above, Gatta takes over the Dollar General role from Rick McNeely, had previously served as Enterprise Chief Merchandising Officer responsible for both the Dollar Tree Store and Family Dollar Store segments). Richard Dreiling noted:

“Larry will be focused on improving Family Dollar’s operating performance and productivity through sales driving initiatives that provide great value for our shoppers. [He has been tasked to] improve store productivity, customer satisfaction, and to better support store associates through efficiencies. Changes include adding linear footage; developing seasonal assortments as a focal point; utilizing deeper shelving on key consumable categories to enhance store efficiencies and improve in-stocks; expanding the direct-to-store delivery offering; enhancing space dedicated to snacks and increasing the beverage offering; and optimizing the frozen food assortments.”

Chief Information Officer : Bobby Aflatooni joined Dollar Tree from Howard Hughes, but he worked at Dollar General from 2011 through 2018. He too has his work cut out for him. According to Richard Dreiling, the underinvestment in IT is “amazing”:

“ The IT side — information technology, I might classify as a little bit bigger surprise, in that there are a lot of basic things that the operators and the merchants need and the supply chain needs.

We are simply not where we need to be from a systems perspective to reach our potential . We have recently begun a comprehensive review of all of our systems and infrastructure to make the right decisions and investments to take Dollar Tree and Family Dollar to the next level.”

Other key senior positions were similarly replaced with well-qualified managers bringing very relevant experiences, including:

Chief Financial Officer : Jeff Davis, previously Treasurer for Walmart Stores, CFO for Walmart US, CFO at JC Penney, and CFO at Darden Restaurants

Chief Operating Officer: Mike Creedon, previously COO at Advanced Auto Parts

Chief People Officer: Jenn Hulett, previously Chief Human Resources Officer of Core-Mark.

The company is still searching for a general counsel after Janet Dhillon resigned in February 2023. This position is currently handled by John Mitchell, who is the senior deputy general counsel at the company.

Every officer has work cut out for them. In a high-stakes turnaround situation, time is of the essence and there is little room for underperformance.

The company has reconstituted the board of eleven directors, replacing six of the existing directors with Paul Hilal as vice-Chair and five independent directors. Interestingly, I observed that one of the original directors, Thomas Dickson, was a signatory on the company’s 2022 SEC Form 10-K but does not appear on the company’s board of directors web page .

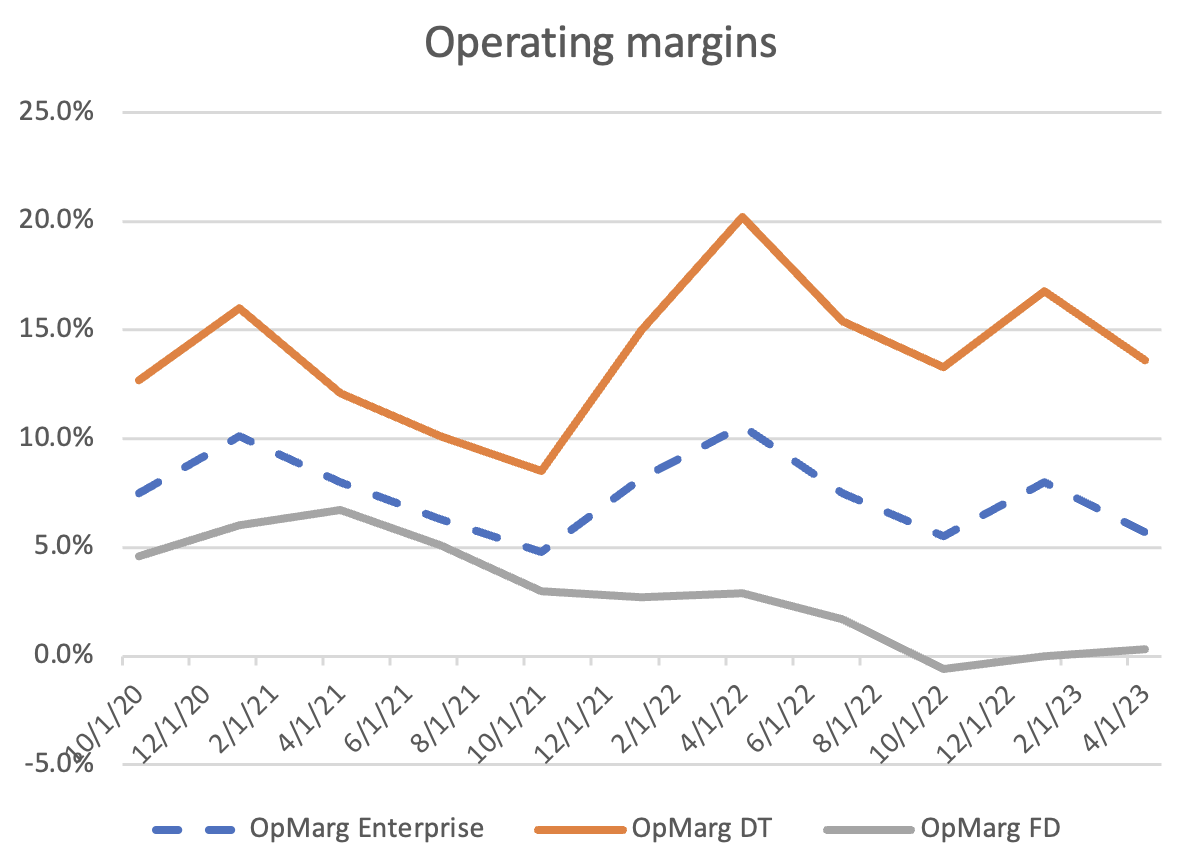

Key areas identified for improvement:

In its June 2023 investor day event, management noted that the previous team had underinvested in the company and highlighted several key areas where it plans to ramp investments to accelerate sales, reduce costs, and expand shareholder returns (Figure 7):

Figure 7 Underinvested areas requiring additional investment

Company 2023 investor day presentation

{kind=link}

Upgrade compensation structure:

Chief Operating Officer Mike Creedon described the need to provide workers with more competitive wages and benefits; job-specific and personal development training; and a career path that helps in the retention of talent.

Family Dollar Store merchandising:

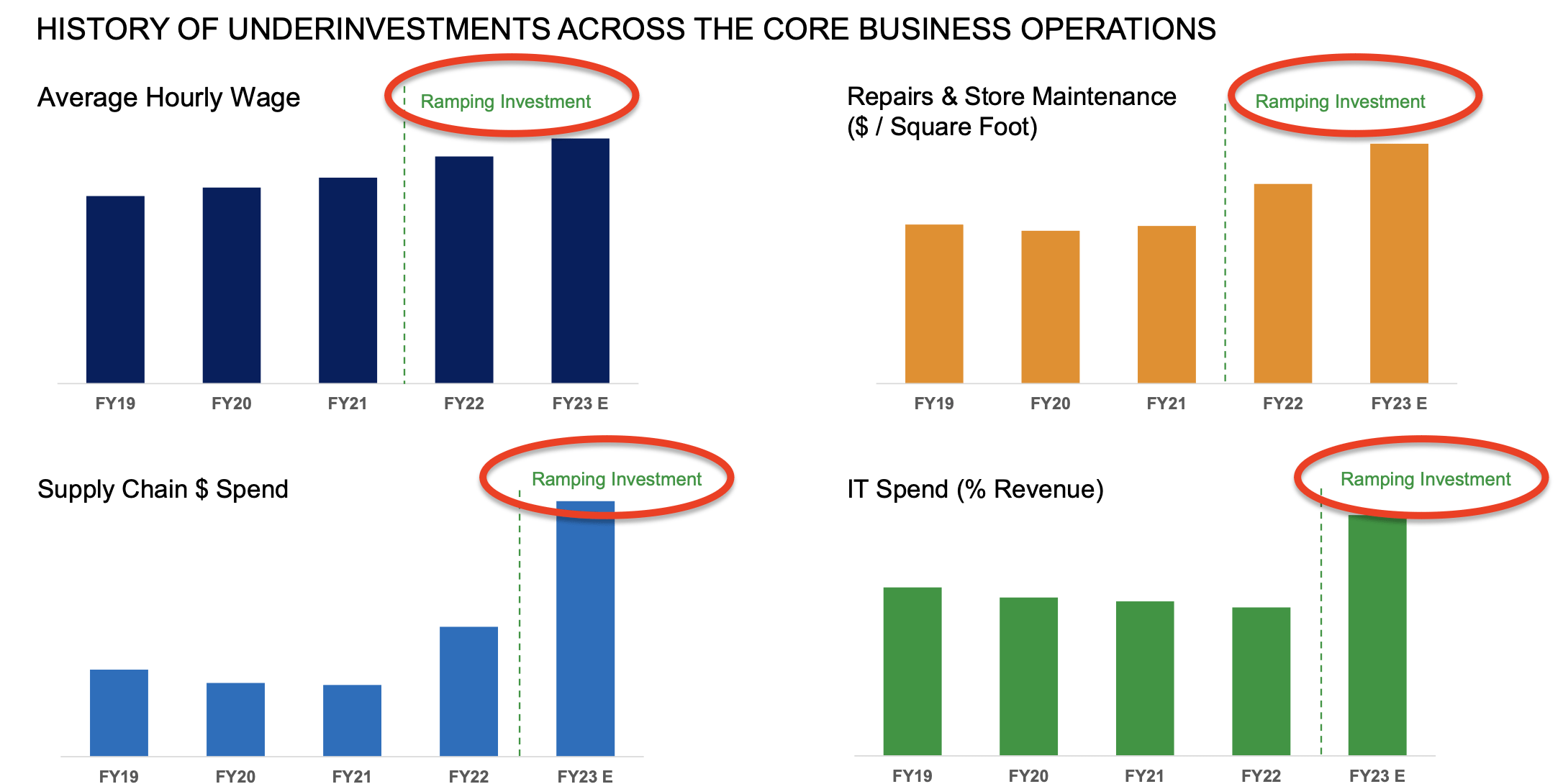

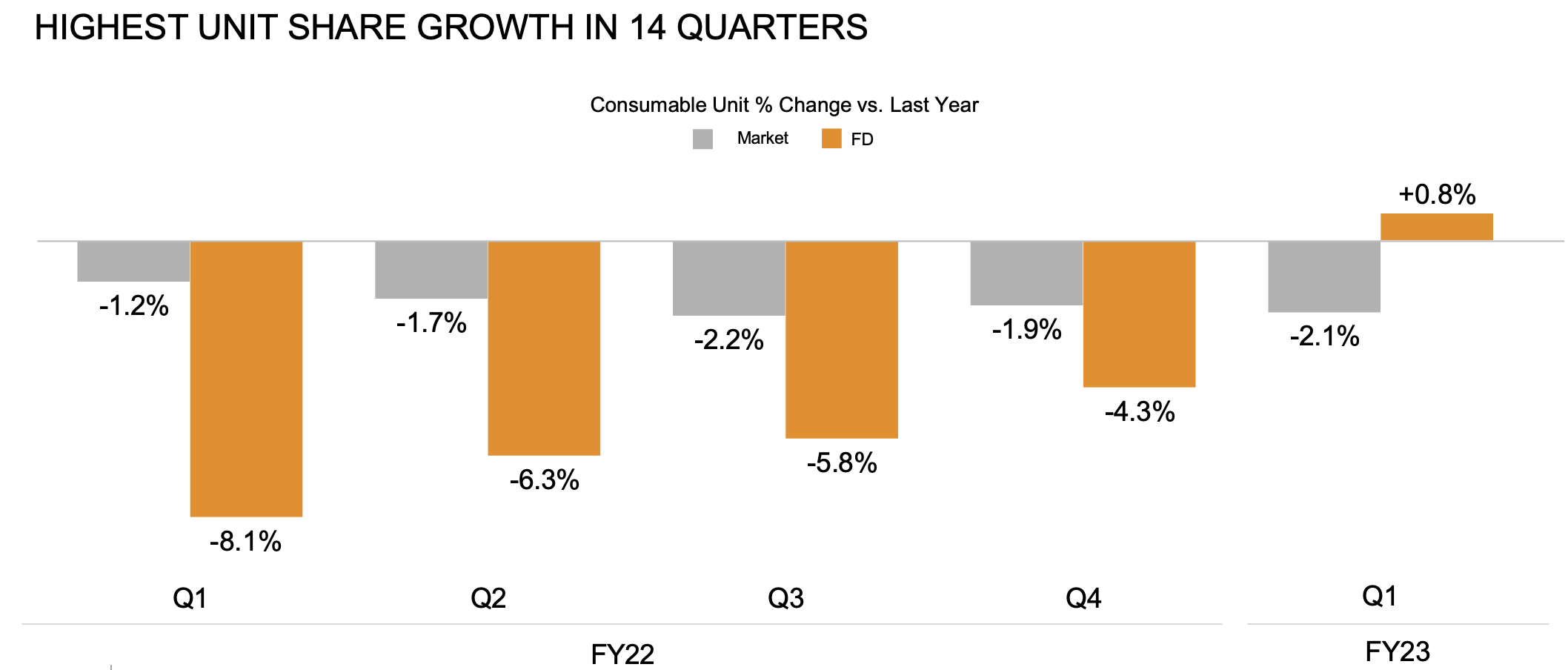

Family Dollar Chief Merchandising Officer Larry Gatta noted in his presentation that price is the main motivating factor for Family Dollar Store customers, who have incomes of ~$70,000 and below. He pointed out that the June 2022 “price investment” to lower prices to competitive levels (Figure 8) reversed the loss of market share, which resulted in the highest unit market gains for consumables in 14 quarters (Figure 9).

Figure 8 Dollar Tree pricing index (2020-present)

Company 2023 investor day presentation

{kind=link}

Figure 9 Family Dollar market share growth

Company 2023 investor day presentation

{kind=link}

He also went through a discussion of enhanced store formats, better shelf configuration to increase SKUs, introduction of private labels, and improved marketing/promotion—all of which are designed to attract and retain customers by improving customer value, convenience, and experience.Early trials of new store upgrades have been encouraging—the $69,000 per store investments have resulted in sales lifts of 10%.

Even though the share gains and revenue growth at the Family Dollar Stores are positive signs, the price cuts have caused driven operating margins down to barely breakeven levels (Figure 6 above, grey line). It is imperative that the company improves its supply chain logistics and upgrades its IT systems to reduce costs and return the segment to reasonable profitability.

Dollar Tree Store merchandising:

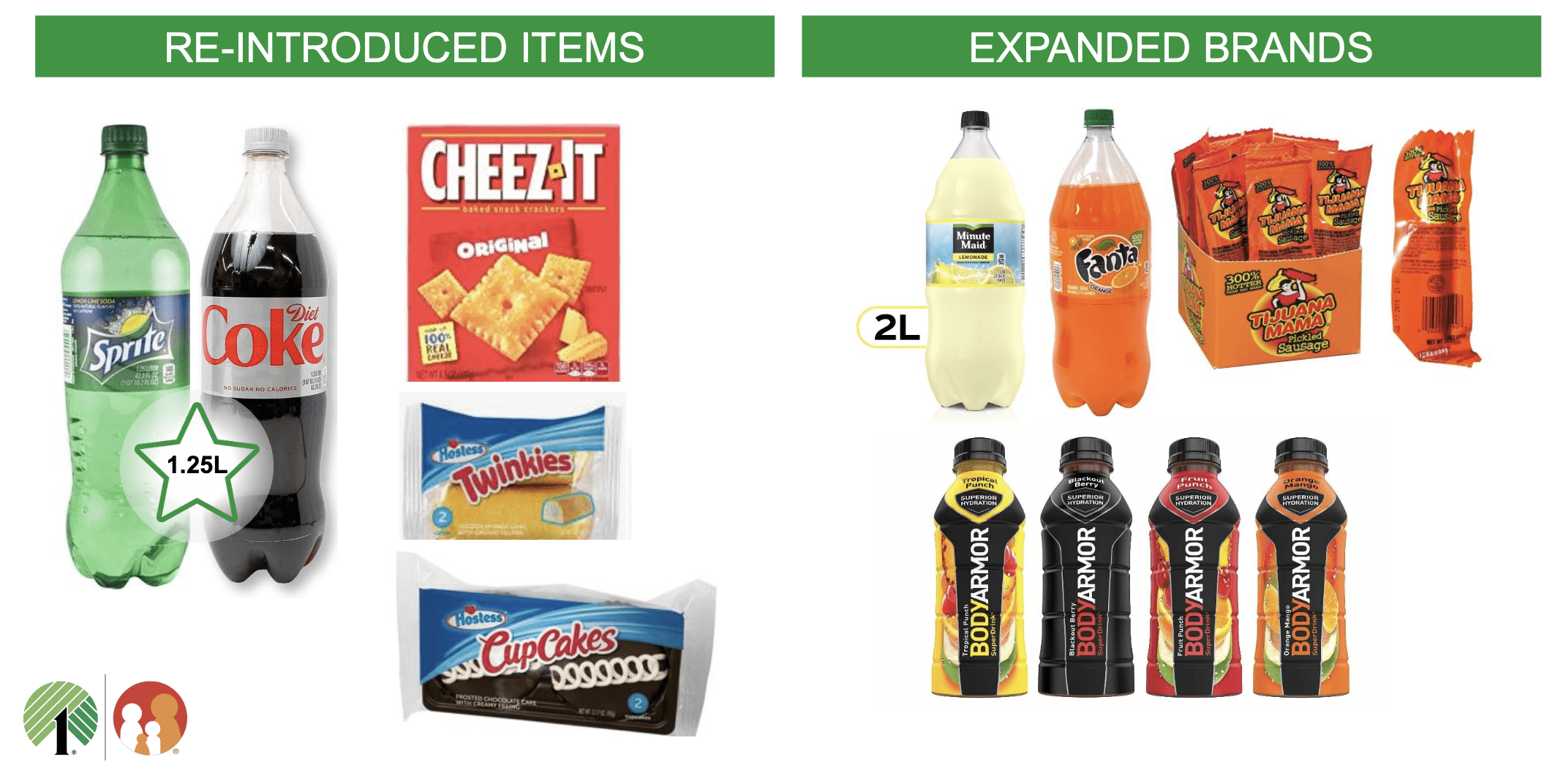

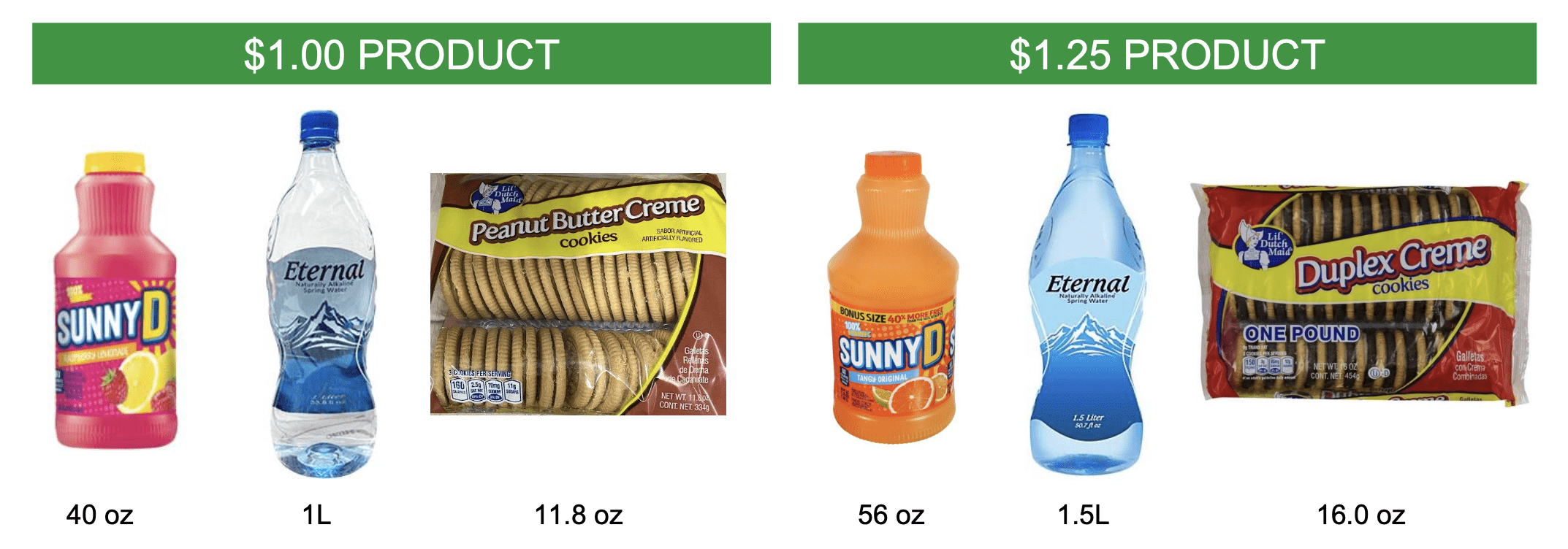

In his 2023 investor day presentation, Dollar Tree Stores Chief Merchandising Officer Rick McNeely announced the segment has successful transitioned from the historical $1 price point to a $1.25 price point. This has enabled Dollar Tree Stores to re-introduce products that were discontinued because the company was no longer able to offer at a $1 price point due to inflation (Figure 10), and to offer better value to customers at lower unit prices (Figure 11).

Figure 10 re-introduced and expanded items at $1.25 price point

Company 2023 investor day presentation

{kind=link}

Figure 11 Additional value to Dollar Tree Store customers

Company 2023 investor day presentation

{kind=link}

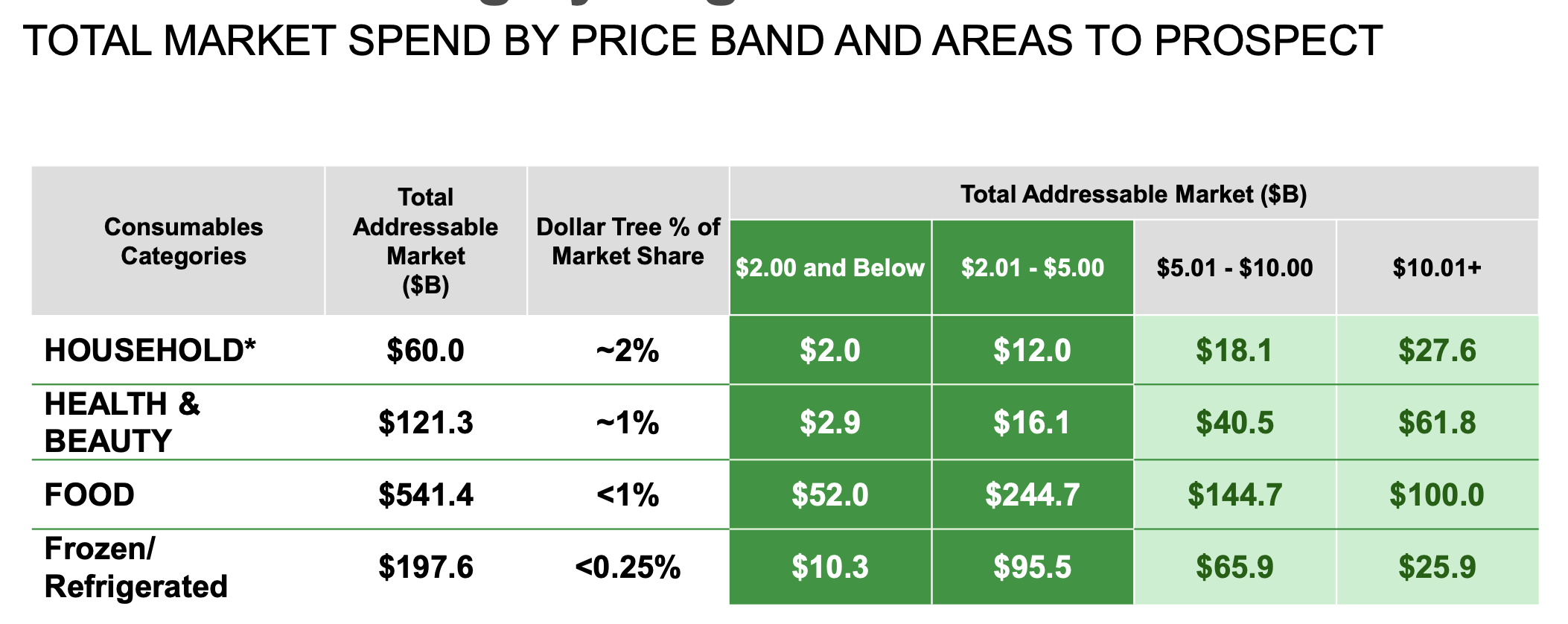

At the same time, Dollar Tree Stores has created a “multi-price” section for products priced at $3, $4, and $5. This opens multiple opportunities to expand the total addressable market (Figure 12) and extend the range of its product offerings into additional new categories and products priced above $1, such as sport equipment (e.g., basketballs), home products (e.g., 6-foot Christmas trees), and personal care products.

Figure 12 Additional addressable market with $3, $4, and $5 price points

Company 2023 investor day presentation

{kind=link}

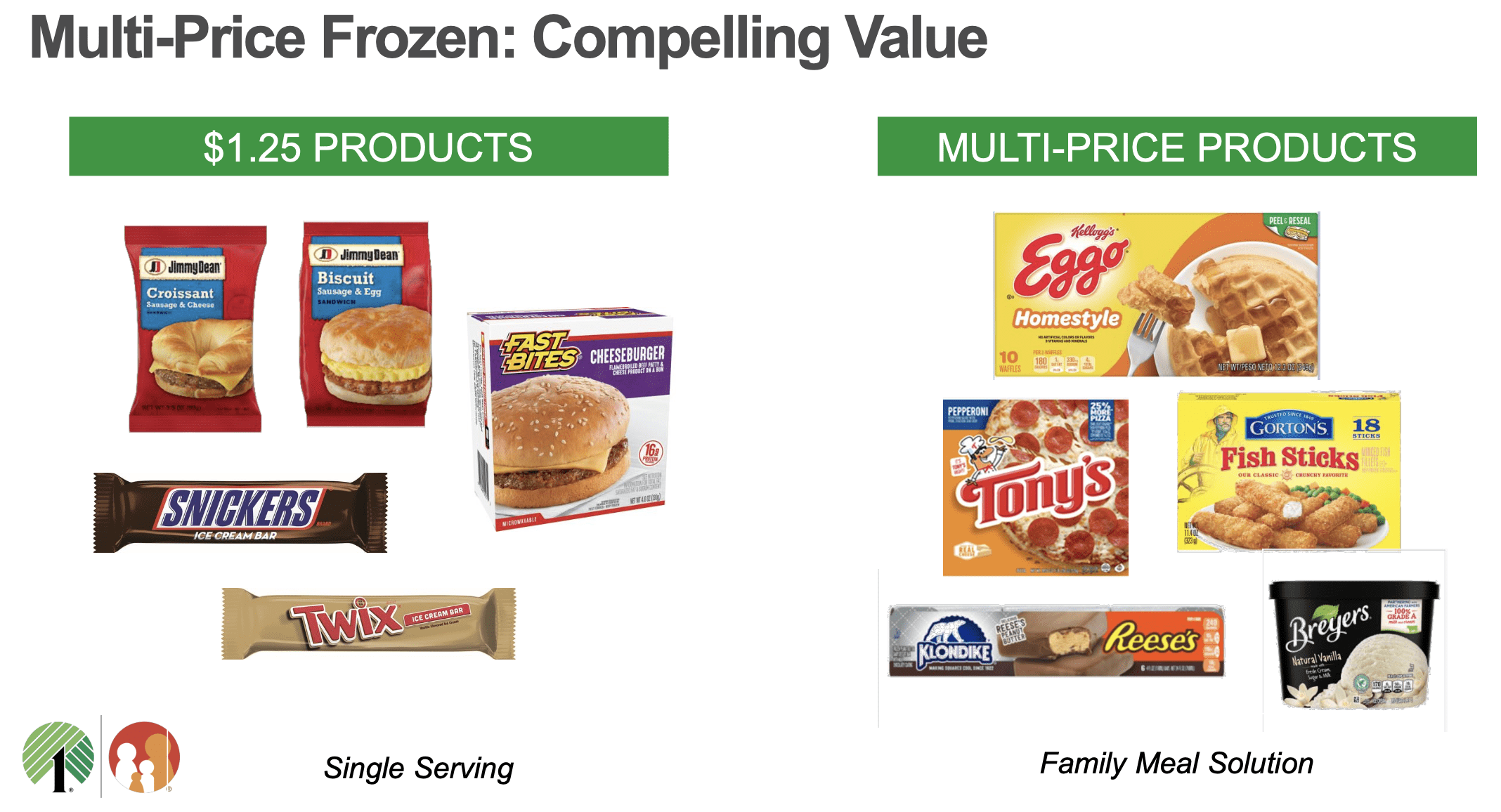

With these higher price points, Dollar Tree Stores is now able to move beyond single serve portions to provide family meal solutions (Figure 13).

Figure 13 Moving beyond single serve portions to family meals

Company 2023 investor day presentation

{kind=link}

McNeely shared plans to expand shelf space for higher price items from 30% today to as much as 80% in the future. I believe this puts the company in a good position to take share from higher priced retailers and convenience stores and potentially create a discount consumable and general merchandise retailer targeted at cash-strapped consumers. However, as with the Family Dollar Store segment, the ability to provide value consistently at low prices is predicated on well-run supply chain and IT systems.

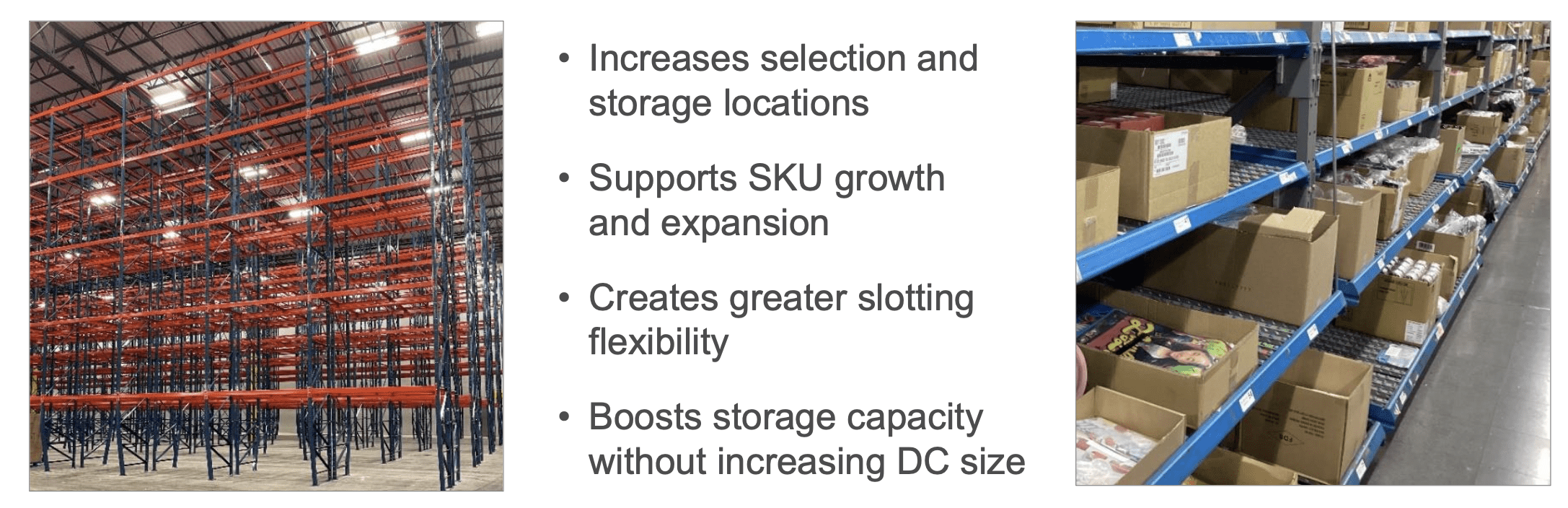

Supply chain and logistics investments:

In his 2023 investor day presentation, Chief Supply Chain Officer Mike Kindy discussed initiatives to streamline the store delivery process and improve the distribution capabilities for better on-time store delivery at lower costs.

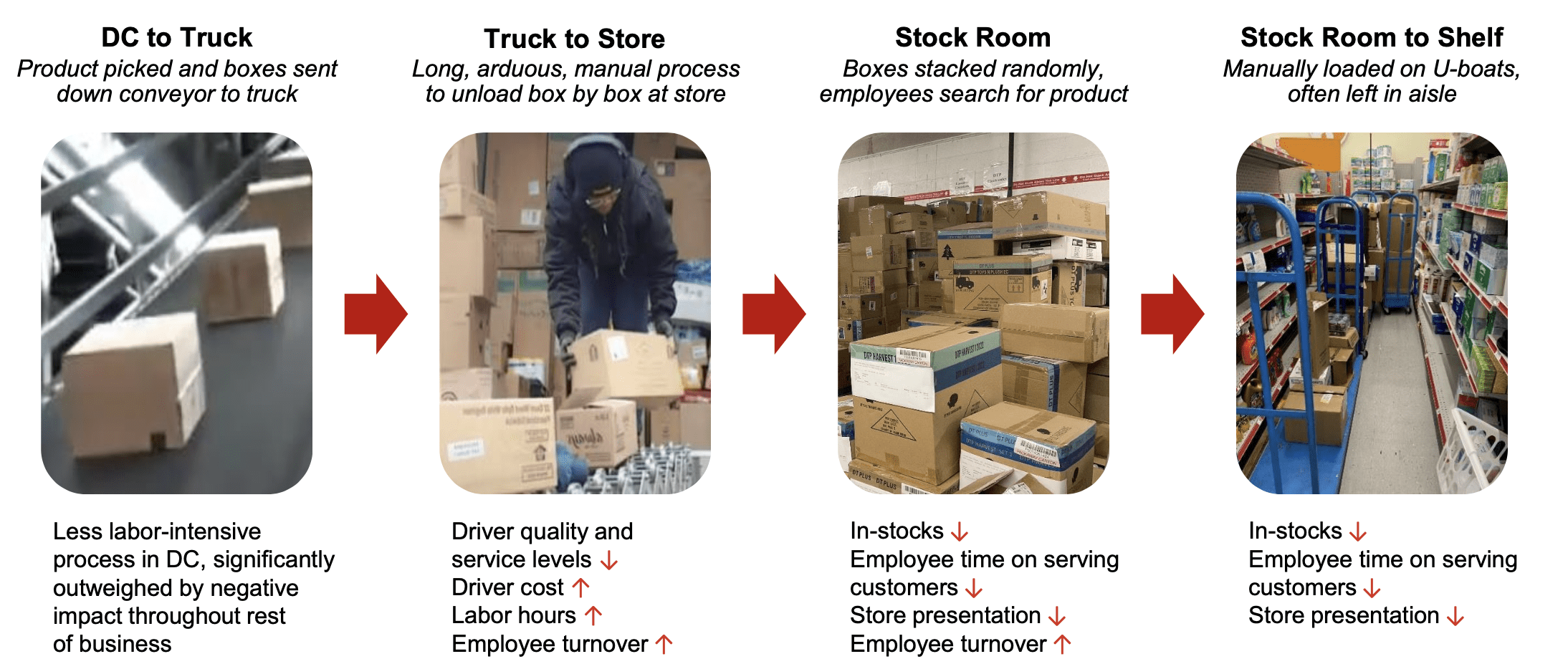

Streamlining the store delivery process:

By transitioning from shipping store deliveries in individual carton boxes (Figure 14) to the use of caged carts (Figure 15), the company is able to increase the efficiency of the truck loading and unloading process, stock room organization, and shelf stocking. I believe this is “low hanging fruit” that can be implemented with relative ease.

Figure 14 Current store delivery process

Company 2023 investor day presentation

{kind=link}

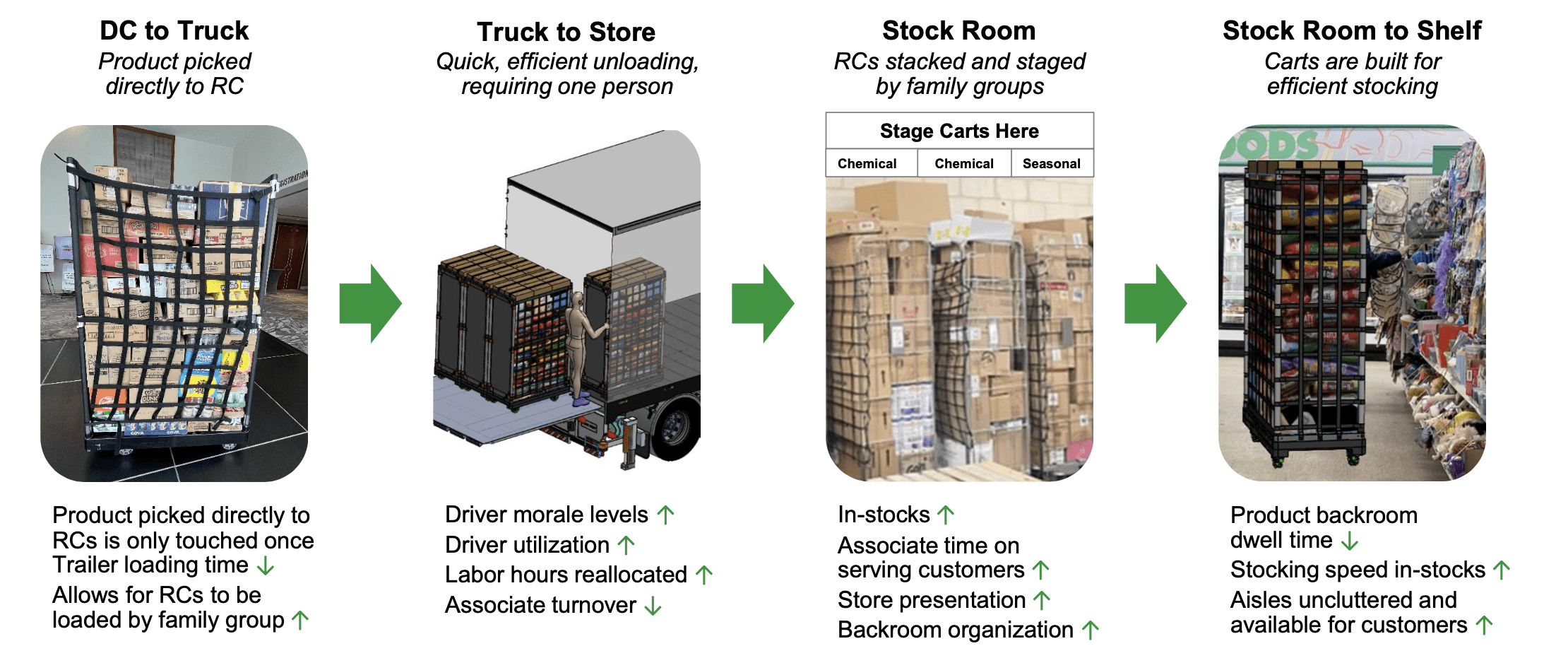

The future Truck loading and store delivery process Mike Kindy described requires better organization at the distribution center but saves significant time and labor at the store (Figure 15).

Figure 15 Revamped store delivery process

Company 2023 investor day presentation

{kind=link}

Improve the distribution center and transportation system capabilities:

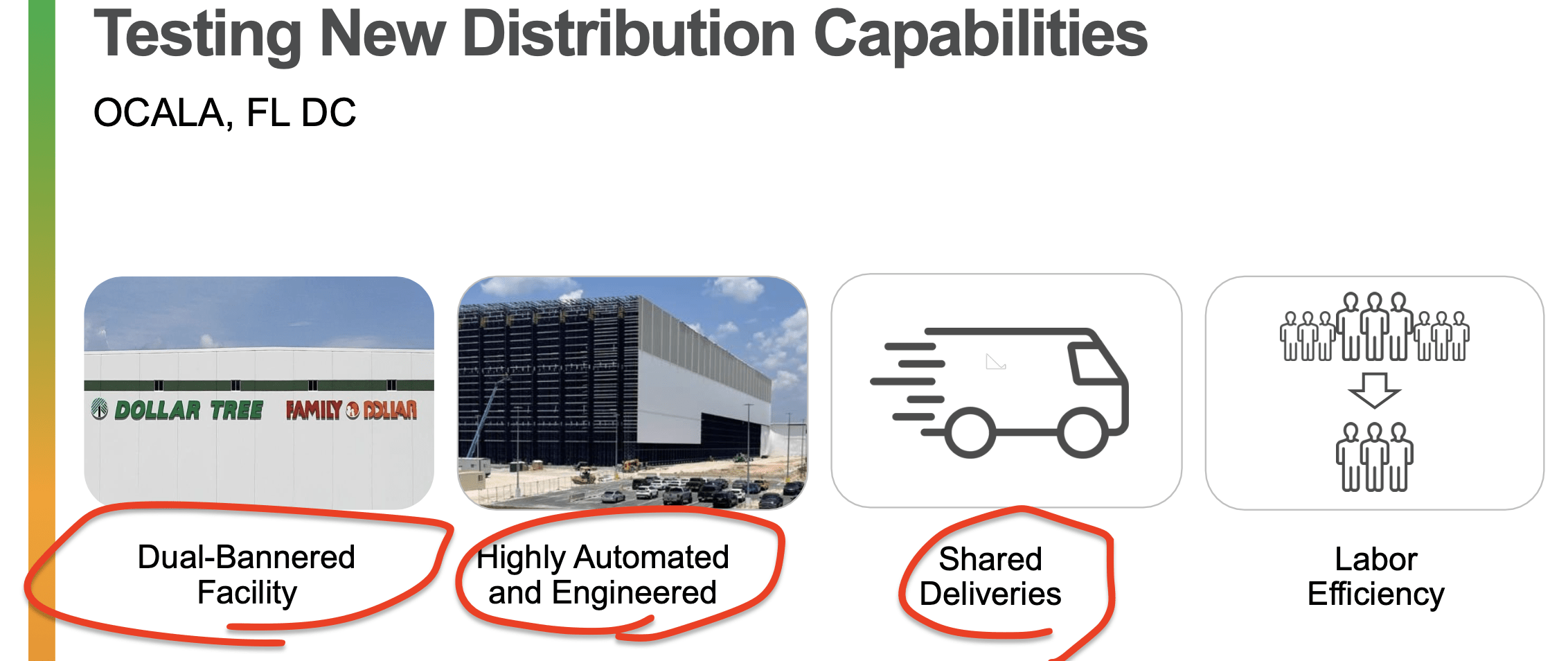

In his presentation, Mike Kindy also discussed investments to increase distribution center ((DC)) capacity and build highly automated warehouses to optimize labor efficiency. He also noted that the company was testing dual bannered warehouses that can serve both Dollar Tree and Family Dollar stores (Figure 16)—this is something that previous management had discussed but not delivered. For example, on the Q2 2018 earnings call , the then-management did not address the pointed question from Credit Suisse analyst Judah Frommer on whether the new Warrensburg, Missouri warehouse will have dual-banner DC capabilities by stating that “as we rebannered stores, converted [Family Dollar] stores to Dollar Tree, we needed the firepower on the Dollar Tree side. So, that's the other reason that Warrensburg will service Dollar Tree initially”.

Figure 16 New distribution strategies

Company 2023 investor day presentation

{kind=link}

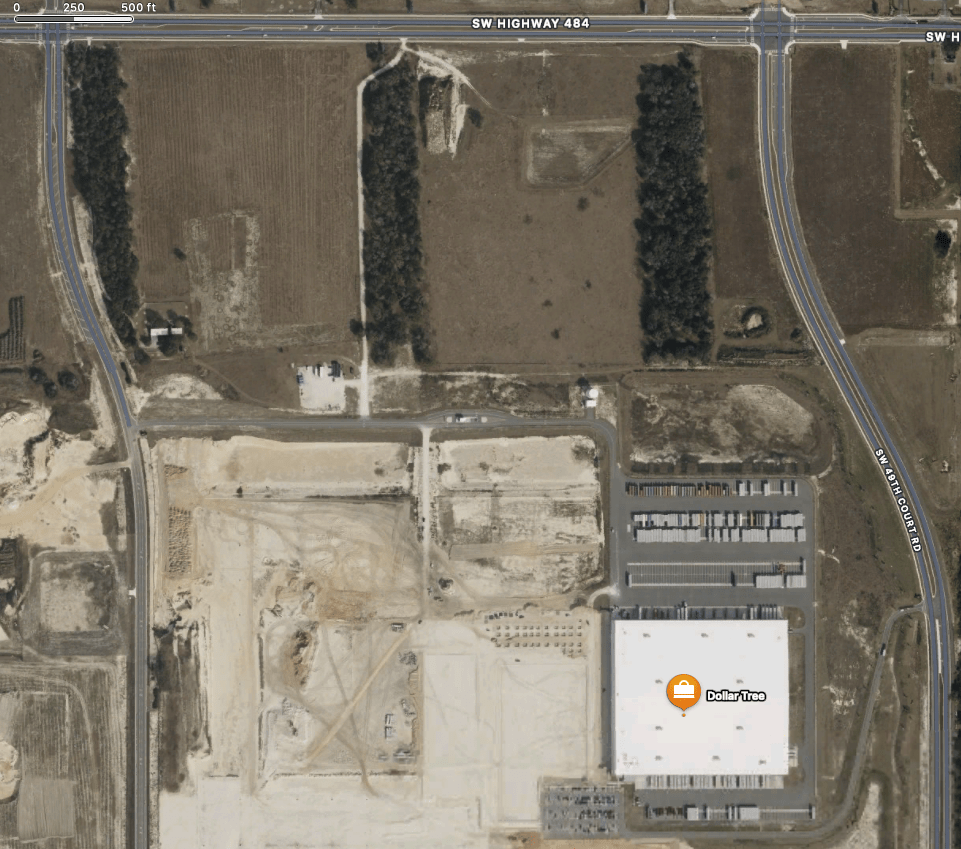

Management is testing these capabilities at their Ocala, Florida distribution center. At the 2023 investor day, Supply chain chief Mike Kindy described this DC as their “first foray” into highly automated and engineered distribution centers (Figure 16 above).

The pictures provided in the Investor Day deck (Figure 17) indicate that the existing DC is not of the same sophistication as the futuristic, heavily robotic warehouses operated by Amazon ( AMZN ) or McLane’s (previously a subsidiary of Walmart (WMT), now owned by Berkshire Hathaway (BRK.A) (BRK.B). Further, the company’s (Figure 18) and ziprecruiter’s job listings for the facility still seek workers with skills required of a fairly traditional fashioned DC.

Figure 17 Inside of company distribution center

Company 2023 investor day presentation

{kind=link}

Figure 18 Help wanted ad for the DC at Ocala FL

Dollar Tree help wanted ad

However, the Ocala Gazette reported on May 21, 2021 that Dollar Tree has applied for a 145-foot distribution tower to accommodate an automated storage rack at the facility, suggesting that the $200 million expansion in the plot adjacent to the existing DC (Figure 19), which includes integrated automation in its construction bid specifications, is designed with robotics in mind. The dual-banner system is expected to be up and running by 2024 and could be the prototype DC that helps the company to stay ahead of the competition. (Dollar Tree is likely keeping its plans under wraps so we may have to wait till the company is ready to share the information with the investment community and public).

Figure 19 Satellite view of Ocala FL Distribution Center

{kind=link}

The company is also making long overdue investments to modernize its including its warehouse, labor, yard management, and transportation systems (Figure 20); and lower costs by building its own equipment fleet.

Figure 20 Objectives of transportation management system

Company 2023 investor day presentation

{kind=link}

Investments to upgrade IT systems:

At the company's June 2023 investor day, Chief Information Officer Bobby Alfatooni’s acknowledged that the company’s systems are antiquated, and discussed plans to build a cloud-first infrastructure platform that will enable the company to run big data analytics and artificial intelligence algorithms, as well as to upgrade and integrate its core applications with proven technologies. This will allow the company to create a better customer experience and scale up more easily while reducing its product and distribution costs (Figure 21).

Figure 21 Company IT strategy and deliverables

Company 2023 investor day presentation

{kind=link}

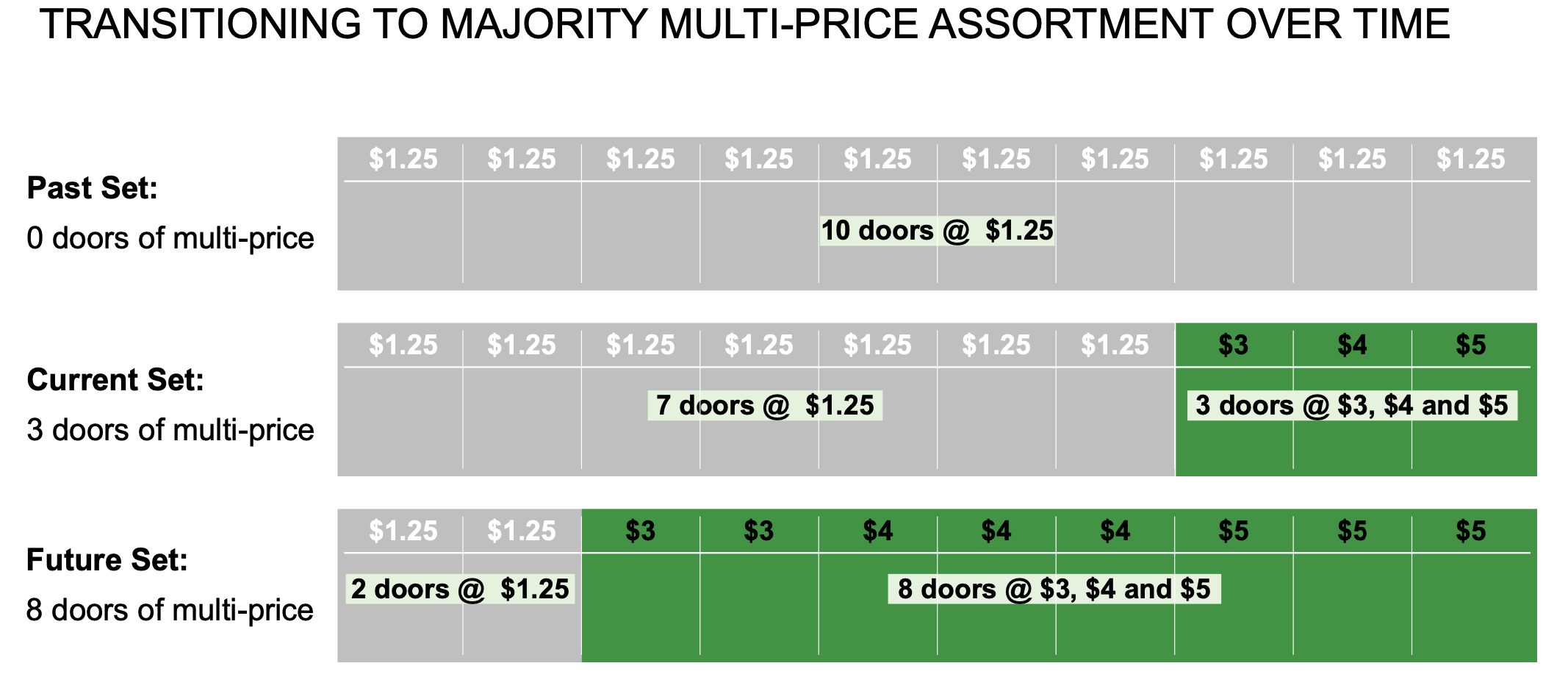

Potential to reposition Dollar Tree Stores over the longer term

The multi-price point products at Dollar Tree stores will initially take up just 30% of overall store space, but the company envisions expanding the space for multi-price products to 80% of its shelves over time (Figure 22).

Figure 22 Transitioning Dollar Tree Stores to multi-price assortment over time

Company 2023 investor day presentation

{kind=link}

I believe this strategy is prudent as it gives the Dollar Tree Store segment room to introduce or raise prices on more products going forward. It could also enable the company to offer price-sensitive customers an increasingly broader range of lower priced everyday necessities and general merchandise, potentially creating filling an important niche serving less affluent, cash-strapped customers and taking share from the front end stores of retail pharmacies (such as Walgreens ( WBA ) and CVS (CVS)), neighborhood convenience stores (such as Seven-Eleven, Casey’s (CASY), and the mom-and-pops) which have been able to extract premium pricing due to their convenient locations.

Summary of improvements

Many of the areas of investment seem reasonably straightforward—for example, store upgrades have generated an uplift in sales for the last several years, the new store delivery process sounds perfectly logical, and a new transportation management system should improve delivery timeliness and costs. However, some of the supply chain and IT system upgrades are less straightforward but necessary to raise the company’s efficiency.

Until the company succeeds, the Family Dollar Store segment, which currently has an operating margin that is barely breakeven, is of little shareholder value in my view.

As previously discussed, it is very possible that the company may be cautious about revealing too much about its supply chain and IT system upgrade plans. As such, we will have to wait for additional details in the coming quarters before making a judgement on the strategies.

Will the turnaround succeed under Mantle Ridge’s leadership?

Mantle Ridge’s investment style is substantially more labor-intensive than the typical activist hedge fund and closer to private equity buyouts, which limits the number of investments it can make. Mantle Ridge founder Paul Hilal’s past investments have as a whole delivered above-market returns despite the underperformance of Aramark, which was hit hard by the COVID-19 outbreak. In addition, I believe he has sufficient skin in this game.

I covered Mantle Ridge and its track record in a previous article . However, given the importance of Mantle Ridge's role to the success of the turnaround, I have updated and replicated the analysis for readers' convenience (in indents).

Who is Mantle Ridge?

Mantle Ridge is headed by Paul Hilal , a veteran activist investor and former senior partner at Pershing Square. While relatively little is known about Hilal among public market investors, it is illuminating when he remarked in an April 2021 interview with the Harvard Crimson that to “help the system work more efficiency and productively through innovation, provide some service to people reliability is massively value creating and honorable”, which may shed some light on his underlying motivations (in addition to making money, of course).

In the same interview, he also demonstrated an innate ability to get his message through in a simple, memorable, and powerful manner (look out for his “dental floss” comment and William Ackman’s response to his comment).

According to CNBC, Paul Hilal is an “incredibly experienced activist investor with a unique mix of analytical abilities, communication skills and likability that you rarely see in the activist world”. Hilal’s approach appears to be to constructively engage with the company, amicably get the required level of board representation for the given situation, bring in the right senior management team and then decide how to best optimize the portfolio of assets.

Paul Hilal’s track record

According to CNBC, Mantle Ridge is very selective with its investments. While many activists look for three to four good ideas a year, Mantle Ridge executes on one idea every few years. Hilal was credited for his roles for investments in Ceridian, Air Products & Chemicals, Canadian Pacific, CSX, and Aramark, each of which I will examine.

(1) Ceridan (2006 – 2007)

Ceridian HCM is a provider of human resources software and services. Pershing Square took a 14.8% stake and activist role in the company in 2006. Even though the financials did not markedly improve, the Ceridian was acquired by Thomas H. Lee Partners and Fidelity National Financial in 2007. It was relisted on the NYSE in 2018.

Figure 23 Ceridian revenue and net earnings

2001

2002

2003

2004

2005

2006

2007

2008

Revenue

1,167

1,160

1,214

1,320

1,459

1,565

1,645

1,565

Net earnings

59.7

111.5

98.8

36.9

127.9

173.6

83.1

-92.4

Source: company 10-K filings on SEC.gov

(2) Air Products & Chemicals (2014-end 2017)

Pershing Square took a large stake in the Air Products and Chemicals from 2014-2017. During that period, revenue was down (figure 14) but margins expanded (figure 15), enabling Pershing Square to significantly outperform the S&P 500 in this investment (figure 16).

Figure 24 Air Products & Chemicals revenue

Seeking Alpha charts

Figure 25 Air Products & Chemicals EBITDA margin

Seeking Alpha charts

Figure 26 Air Products & Chemicals stock price compared to the S&P 500 index

Yahoo Finance

(3) Canadian Pacific (2012-2017)

In 2011, Pershing Square approached Ewing Hunter Harrison , the recently retired CEO of Canadian National Railway with the role of President and CEO of Canadian Pacific should Pershing Square’s proxy battle for Canadian Pacific turn out to be successful. Following the successful proxy battle, Harrison rolled out precision scheduled railroading at Canadian National, which resulted in significant margin expansion (Figure 27) despite flat revenues (Figure 28), which resulted in a strong stock outperformance over the S&P 500 through today (Figure 29).

Figure 27 Canadian Pacific EBITDA margin

Seeking Alpha charts

Figure 28 Canadian Pacific revenue

Seeking Alpha charts

Figure 29 Canadian Pacific stock price vs. S&P 500

Yahoo Finance

(4) CSX (2017-2019)

In January 2017, Hunter Harrison resigned as CEO of Canadian Pacific and joined Paul Hilal in the management of CSX, but unexpected passed away in end-2017. Despite the loss of Mr. Harrison’s leadership, CSX’s EBITDA margin expanded (Figure 30) in spite of volatile revenues (Figure 31), and the stock appreciated by over 50% over the next 3 years, narrowly beating the S&P 500 index (Figure 32), which industry analysts attribute to the changes put in place by Mr. Harrison before he passed away.

Figure 30 CSX EBITDA Margin

Seeking Alpha charts

Figure 31 CSX revenue

Seeking Alpha charts

Figure 32 CSX stock price vs. S&P 500

Yahoo Finance

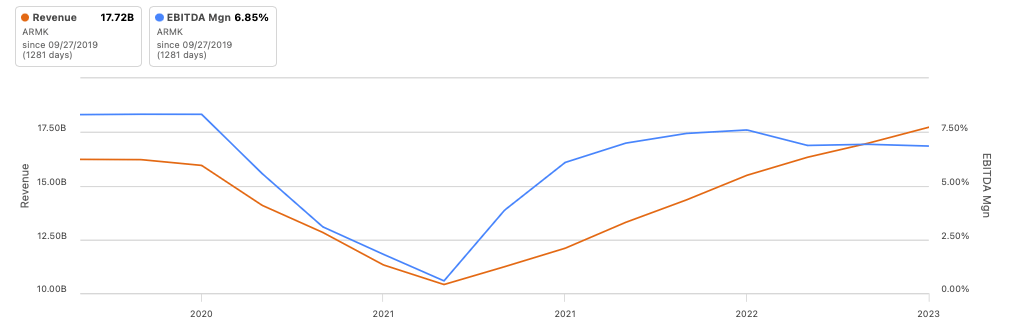

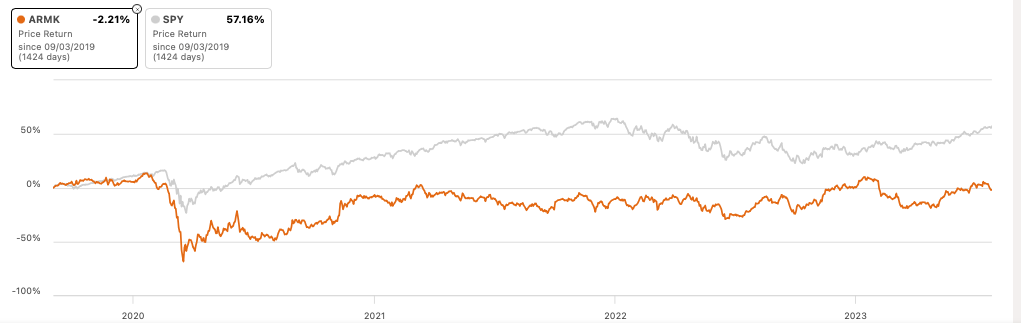

(5) Aramark (end 2019-present)

Aramark Holdings is a leading food-services provider and concessions manager which serves a wide range of customers, including corporations, healthcare facilities, prisons, sports stadiums, and national parks in the US (56% of sales) and internationally (24%). In addition, it also supplies work uniforms and related services through its Uniform and Career Apparel segment (20% of sales). The COVID outbreak struck shortly after Mantle Ridge’s investment in 2019, causing the company’s sales to take a 25% hit as food services and other events were scaled back or shut down (Figure 33, orange line). Even though Aramark was able to manage costs down (blue line), the stock price has not surprisingly underperformed the S&P500 (Figure 34). I believe the company would have been done far better had the pandemic not struck and would put this is the “truly bad luck” category.

Figure 33 Aramark revenue, EBITDA margin

{kind=link}

Figure 34 Aramark stock price vs S&P 500 index

{kind=link}

Mantle Ridge’s skin in the game

Mantle Ridge has accumulated total economic exposure representing 9.85% of the company , consisting of 12.7 million (or 5.66%) in equity with a current value of over $1.5 billion plus 4.19% in cash-settled derivatives with expiration dates between 2023 and 2026. The Limited Partnership Agreement filed with the SEC does not state Mantle Ridge’s capital commitment to the transaction, and it is likely that a substantial portion of the invested capital comes from third party investors. Nonetheless, there is pressure on Mantle Ridge to perform as it would be very difficult for the firm to raise funds in the future if it does not deliver satisfactory returns to investors.

Mantle Ridge’s position was acquired in the fourth quarter of 2021 , during which the prices fluctuated between just below $100 and $145 per share (Figure 35). According to CNBC, Mantle Ridge acquired the shares at an average price of $106.77, implying that the firm is sitting on unrealized gains of ~40%. This is a sizeable dollar gain but given the large amount of resources Mantle Ridge it has poured into the project and its history of long, management-intensive holds, it seems quite unlikely that Mantle Ridge will exit its position without a more substantial gain.

(A quick note: I have not been able to find disclosures in SEC filings stating that the company pays Paul Hilal or Mantle Ridge consulting fees. Even though Mantle Ridge receives an undisclosed management fee from its investors, it does not receive carried interest until its investors have received an undisclosed preferred return, indicating that the firm’s economic return is dependent on the upside from its equity and derivatives in Dollar Tree)

Figure 35 Dollar Tree stock price Q4 2021 – Q2 2022

{kind=link}

Valuation

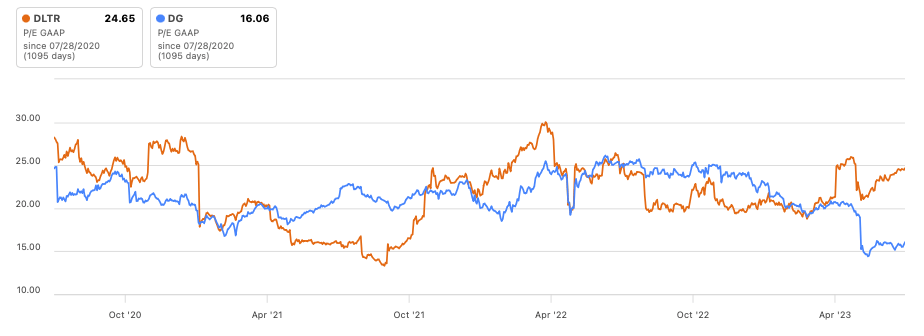

Dollar Tree’s price earnings ratio of ca. 25x is within its three-year trading range (Figure 36). However, I expect the PE ratio to expand for the near term as the company steps up its investment spending to improve the company’s competitive positioning as described in Figure 7 above.

Figure 36 Valuation on price earnings basis

{kind=link}

Risk and concerns

Execution risk: I have little doubt that the team installed by Mantle Ridge can implement the store redesigns and store delivery processes. My main concern is whether the team’s supply chain and IT system initiatives will enable it to successfully leapfrog and maintain a sustainable lead over the competition.

A race to the bottom with Dollar General: Dollar General has responded to Family Dollar Store’s price-cutting strategy (euphemistically name “price investment”) by lowering its prices on select items. As a result, the Family Dollar Store segment’s operating margins are down to near-zero, indicating that the segment is essentially worth nothing unless its merchandising strategy and the company’s supply chain and IT system initiatives are successful.

Mantle Ridge taking profits and exiting the investment abruptly: Based on its previous history and long holds and management intensive turnarounds, I would be surprised if Mantle Ridge exits its investment in Dollar Tree before the turnaround is substantially complete.

In summary

Dollar Tree has underperformed since its acquisition of Family Dollar in 2015 due to previous management’s inability to fix the operational issues and derive integration synergies between its Dollar Tree Store and Family Dollar Store segments.

Mantle Ridge, a management-intensive activist hedge fund, has acquired an economic interest representing approximately 10% of the company’s shares, revamped the management team, reconstituted the board of directors, and implemented a well-developed turnaround plan that will position the company well for the long term.

Earnings and free cash flow are likely to dip in the near term as the company invests to upgrade its employee compensation, stores, supply chain, and IT systems. These investments should lead to greater revenues and profitability over the longer term and drive shareholder value.

As the Dollar Tree Stores expand shelf space for higher price point ($3, $4, and $5) products, it could break out of its dollar store niche to become a lower cost alternative to local retailers, such as Walgreens, CVS, and the mom & pop stores that have long taken advantage of their proximity to consumers to extract premium pricing. If successful, I believe Dollar Tree’s store count potential will expand significantly.

While there are execution risks, I believe the longer-term upside could be substantial for patient, long-term oriented investors.

For further details see:

Dollar Tree: Strong Potential But Can New Management Execute On Turnaround Plans?