DLMAF - Dollarama: Q1 Delivers More Growth

2023-06-08 04:38:58 ET

Summary

- Dollarama Inc. exceeded analysts' expectations with strong Q1 financial results, highlighted by a 17% increase in same-store sales growth.

- The company also reiterated its lofty guidance, while shareholders rejected a proposal to adopt stricter climate targets, citing conflicts with Dollarama's growth plan.

- I cautiously recommend a "Buy" rating for the company, with an 18-month stock price target of $88 CAD.

Introduction

Dollarama Inc. ( DOL:CA ), the largest discount dollar store chain in Canada, exceeded analysts' expectations with impressive Q1 earnings , showcasing significant same store sales growth amidst a high inflation environment. The company delivered strong financial results and reiterated positive guidance for the upcoming year. That said, the stock experienced limited movement following the earnings release, as the Bank of Canada stole the spotlight with an unexpected interest rate hike of 0.25%.

In my recent Q4 and FY2022 report on DOL:CA, I maintained a predominantly optimistic outlook on the stock, highlighting the company's operational resilience throughout the year. With same-store sales and net income surpassing expectations, there is potential for further growth that may not be fully reflected at present. Along with the earnings release came news that DOL:CA shareholders rejected a proposal to adopt stricter climate targets, as company executives expressed concerns about long-term emission goals conflicting with Dollarama's growth strategy. The proposal aimed to align Dollarama's climate change initiatives more closely with other retailers such as Loblaw ( L:CA ), Walmart ( WMT ), and Costco ( COST ). I cautiously recommend a "Buy" rating on DOL:CA stock, with an adjusted 18-month stock price target of $88, up from $86. This target is supported by a projected FY2024 EV/EBITDA ratio of 21.9 and an expected earnings per share of $3.15 for the current fiscal year.

Q1 Review

DOL:CA reported revenue of $1.29Bn , demonstrating impressive sales growth of 20.7% and a notable increase in same-store sales growth of 17.1%. Gross margins remained steady at 42.2%, showing a slight improvement of 10 basis points compared to the previous year, with consumables continuing to contribute significantly to the overall sales mix. EBITDA reached $366.3MM, accounting for 28.3% of total sales, marking a 30 basis point increase from the previous year.

SG&A expenses experienced a slight rise of 10 basis points, representing 15.1% of sales for Q4 of FY2023. The company's tight cost structure demonstrated resilience even during several quarters of high growth. Net earnings for DOL:CA amounted to $179.9MM, resulting in earnings per share of $0.63, surpassing the earnings per share of $0.49 recorded in the same quarter of the previous year.

Although inventory stood elevated at $937.7MM, it remained in line with the company's needs, given their expanding store footprint, and actually dipped $19.5MM from last year. Dollarcity, the company's 50.1% owned South American subsidiary, contributed $13.1MM in net earnings and continued its gradual growth, up from $8.7MM in net earnings last year. The Latin American discount leader opened 8 net new stores, while DOL:CA opened 21 net new stores in the quarter.

Operationally, the quarter was quite strong and provides further support for a stock rise. Costs and inventory were contained amidst more blowout revenue growth and margins have stabilized now in the low-mid 40% range. The only material negative was the rising financing costs, as the company continues on a growth trajectory towards 2,000 stores in Canada by 2031 and will likely take on new debt in the near future. However, given the consistent growth in sales and net income, I'm not too worried about these developments.

DOL:CA Q4 Presentation

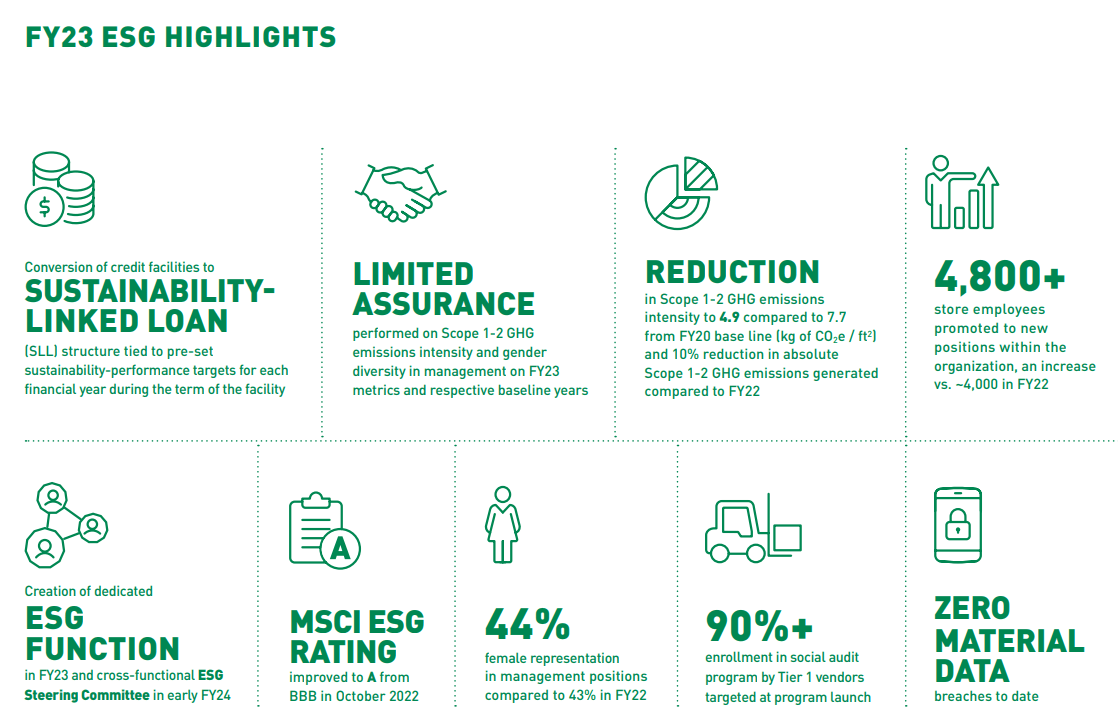

DOL:CA foresees sustained demand for affordable everyday items in the first half of FY2024, but expects demand trends to normalize in the second half. To ensure balanced capital allocation, the corporation plans to invest in organic growth while also returning capital to shareholders. Additionally, the company released their 2023 ESG report that targets emissions reductions over the next decade. However, the firm didn't fully embrace an ESG at all costs strategy.

DOL:CA shareholders voted against a proposal to adopt stricter climate targets, citing conflicts with the company's growth plan. The proposal, supported by the non-profit Shareholder Association for Research and Education (SHARE), aimed to align Dollarama's climate change efforts with other peer retailers. The vote took place during the company's annual shareholder meeting following the release of their Q1 financial results. CEO Neil Rossy urged shareholders to reject the proposal, stating that long-term greenhouse gas emission targets aligned with the Paris Agreement's 1.5-degree goal would be " incompatible with the company's significant growth plan ", as they rely on assumptions and face uncertainties. Given the company's detailed plan on ESG improvements and their A rating from MSCI, I don't think this development is a material negative.

{kind=link}

Throughout FY2024, DOL:CA aims to maintain a balanced leverage ratio (Net Debt to EBITDA) below its historical target range of 2.75-3x. In Q1, the ratio dipped to 2.52x due to a substantial increase in EBITDA. For the fiscal year, the company still anticipates net new store openings of 60 to 70, comparable store sales growth ranging from 5-6%, gross margins in the range of 43.5-44.5%, SG&A ranging from 14.7-15.2%, and CAPEX of $190MM-$200MM.

During the earnings call, analysts pressed executives for insight concerning future margins. Management highlighted a slight shift away from lower-margin consumables, but noted that no clear trend indicating lasting strength had emerged. Questions regarding the breakdown of new versus existing customers were also posed, but it became apparent that DOL:CA does not closely track customer share, leading to an inability to provide a specific response. While operationally strong, I believe there is some room to grow in terms of leveraging customer sales analytics, which could enhance future returns.

Model Shows Limited Upside

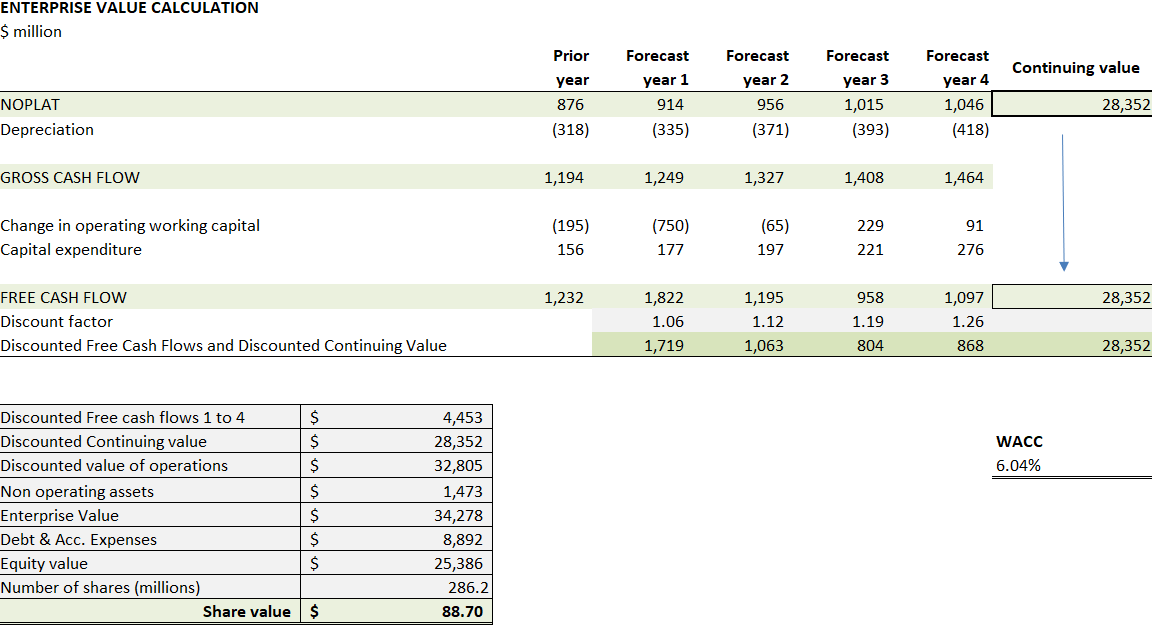

DOL:CA continues to perform steadily, and fundamentals could support another move up after busted revenue growth. However, when compared to other discount retail companies, DOL:CA is nearly fully valued. The company has enough cash reserves and available credit to finance its current expansion strategies, but further stock price acceleration as rates increase will be difficult. The model predicts that the WACC will be ~6%. As interest rates rise, it is expected that the projected cost of debt will exceed the previous issuance coupon of ~5.1%. Fortunately, the interest rates for their previous fixed-rate debt are in the range of 1.5% to 3.6%.

Author WACC Forecast

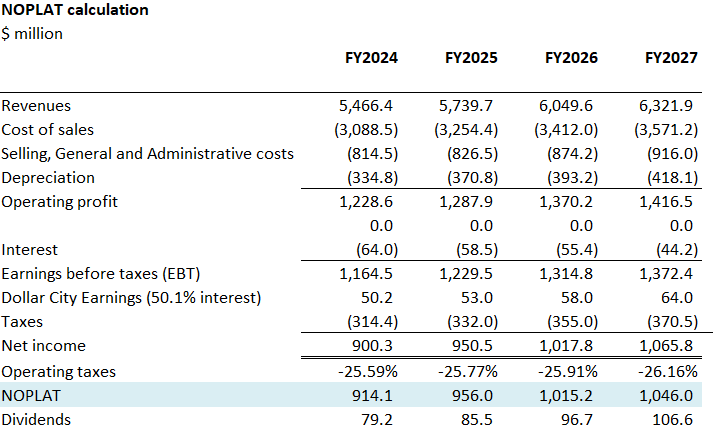

I forecast the continuing value of over $28Bn, given a ~8% revenue increase this year and blended revenue growth of ~5% for three years, as same store sales growth and Dollarcity continue to impress in the near future. I see the margins ending near the low end of guidance, at 43.5%, for the year. I hold other cost ratios mostly equal to guidance, as they were already conservative given the strong Q4 numbers. An $88 share price (see below) can be supported with fundamentals. The share price is supported by a 21.9 FY2024 EV/EBITDA ratio and a 28.2 P/E multiple, a slight premium compared to industry peers in the mid-high teens, but warranted, given that DOL:CA is unmatched in Canada and Latin America.

{kind=link}

{kind=link}

Conclusion

DOL:CA reported impressive Q1 results, solidifying its position as the leading discount retailer in Canada. With high inflation prompting consumers to trade down, the company remains poised to benefit. Although the stock is almost fairly valued, I believe it warrants a cautious buy due to the company's track record of surpassing expectations and its focus on organic growth, cost management, and ESG initiatives. My forecast suggests a target share price of $88 CAD over an 18-month period.

For further details see:

Dollarama: Q1 Delivers More Growth