DLMAF - Dollarama: The ($5) Dollar Store

2023-03-10 11:27:45 ET

Summary

- Dollarama has thrived in the current inflationary environment as it has been able to pass on higher costs to consumers at new price-points of up to $5.00.

- The value retailer is growing on all fronts, including a Latin American expansion and the addition of 60-70 new stores annually by 2031 in Canada.

- The company expects same-store sales growth of 9.5%-10.5% for FY2023.

- Dollarama has an impressive record of returning cash to shareholders, having bought back 29% of its outstanding shares since 2014.

- While the yield is modest, Dollarama has increased its dividend for 12 consecutive years, with a 10-year CAGR of 11.9%.

Author's note: All figures listed in Canadian currency unless otherwise noted.

Investment Thesis

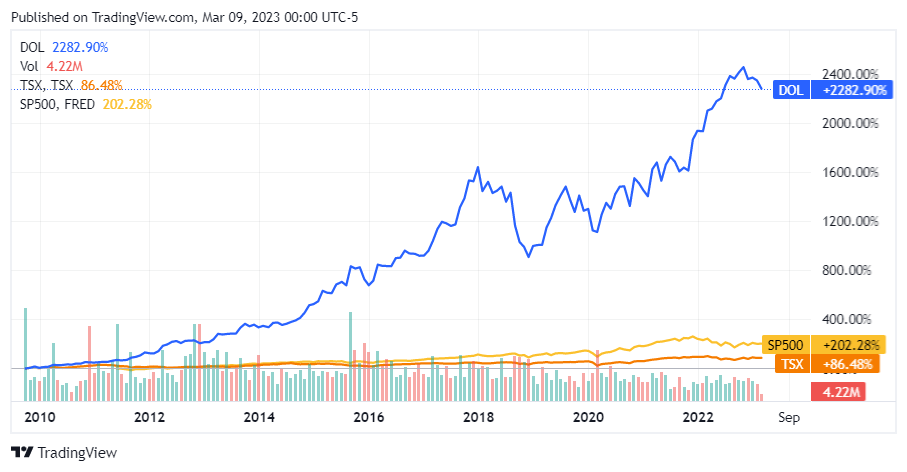

One only needs to glance at a 10-year chart to see that Dollarama Inc. ( DOL:CA ) ( DLMAF ) has been an impressive growth story, with shares up 2,393% since going public in 2009. While share price growth will likely moderate as the company grows, Dollarama continues to offer a significant growth opportunity.

Dollarama has demonstrated its resilience as a retailer by migrating to higher price points through the current inflationary period. Positive catalysts include the addition of new stores at a pace of 60-70 stores annually to 2031, coupled with mid-single-digit same-store sales growth. In addition to its domestic expansion and organic growth profile, Dollarama owns a 50.1% interest in Dollarcity, which operates a growing network of 395 stores across Colombia, El Salvador, Guatemala, and Peru.

This growth is accompanied by a strong balance sheet, a capital-light business model, and commitment from management to return capital to shareholders through dividends and share buybacks.

Dollarama Stock Chart (Seeking Alpha)

{kind=link}

Company Profile

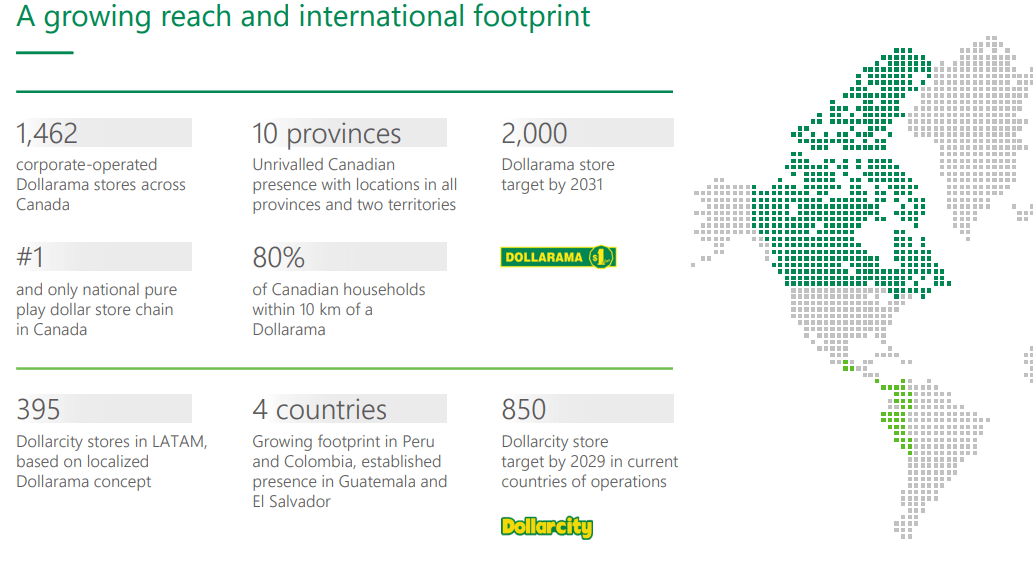

With 1,462 corporately owned stores, Dollarama Inc. is the market leader for fixed-price point retail in Canada. Dollarama was founded as a single store in Montreal, Canada in 1992. Today, it is 6X larger than the next largest "dollar-store" label in Canada. The brand quickly expanded across Canada where it caught the attention of Bain Capital, which was an early investor in the company, prior to the public offering in 2009.

After six years of a successful strategic partnership that saw Dollarama expand into Latin America, Dollarama acquired a 50.1% stake in the Panama-based Dollarcity, in 2019, adding another growth platform for the retailer. Insiders, including the founding Rossy family, owned 4.2% of the outstanding common shares as of the end of March 2022. With a market cap of approximately $22B, Dollarama trades on the Toronto Stock Exchange under the symbol "DOL" with daily average volume of 650K shares.

Dollarama Company Profile (Dollarama)

{kind=link}

A Growing Network

Dollarama has an aggressive goal of expanding to 2,000 stores by 2031. This works out to 1.25 stores opening per week for the next 8 years. This expansion offers a quick return on investment, with the average store costing $650K (of which $250K is inventory) and delivering $2.6M in sales by the end of year two. New stores will be built across Canada, with an emphasis on western provinces. This expansion of the company's domestic footprint will be supported by significant investments in new distribution capacity.

Myriad Tailwinds

Dollarama is the beneficiary of evolving consumer behavior, driven by inflation and rising prices. The average transaction size is now double what it was a decade ago, with the average basket size growing to $13.61 in the most recent quarter. As the retailer at the value end of the consumer discretionary and consumable spectrum, Dollarama has been able to gradually introduce new price points of up to $5.00 for a variety of SKUs.

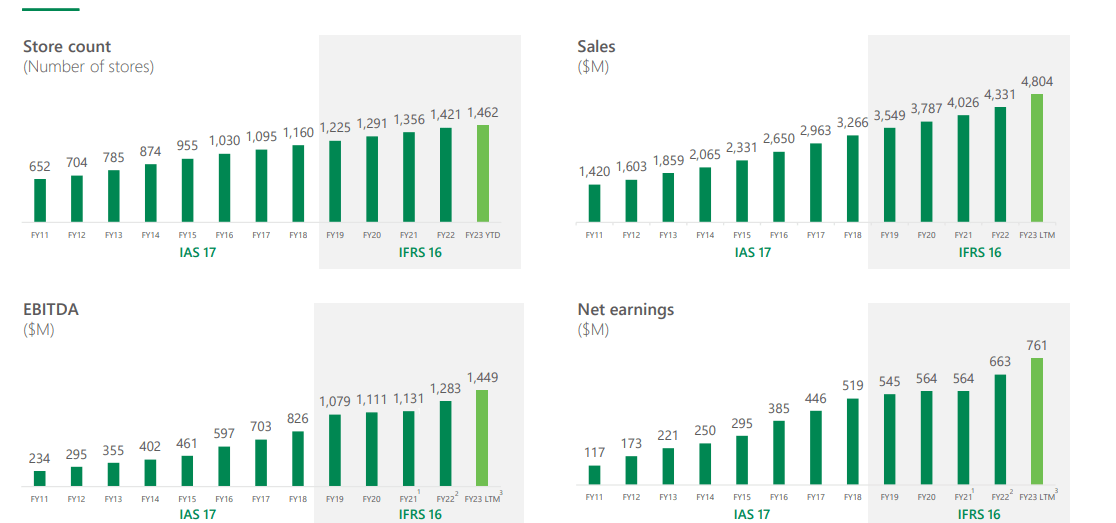

Foot traffic in Dollarama's stores has recovered approximately 97% of pre-pandemic levels, while same-store sales have continued to grow. Despite periodic store closures, Dollarama achieved an EPS CAGR of 13.7% from 2019 through 2022. On the company's recent earnings call , Chief Financial Officer, J.P. Towner updated the company's expectations for same-store sales for 2023:

With stronger than historical demand for lower margin consumable products and our very strong SSS performance, we have increased our SSS assumption for fiscal 2023 from a range of 6.5% to 7.5% to a range of 9.5% to 10.5%

Dollarama Growth Profile (Dollarama)

{kind=link}

Along with steady sales growth which should surpass $5B in FY24, Dollarama has continued to improve its EBITDA margin. Since 2011, the EBITDA margin has almost doubled from 16.5% to 30.2% in 2023 TTM.

On the supply side, container costs for shipping have normalized to pre-pandemic levels, allowing the company to rebuild its inventory position. While there are still major headwinds and price pressure from domestic vendors and domestic manufacturers, overseas suppliers have restored production levels and normalized shipping. This is an important trend to watch as Dollarama's low product prices depend on effective supply chain management.

Latin American Expansion

With 395 stores across Peru and Columbia, Guatemala, and El Salvador, Dollarcity is a rapidly growing brand in Latin America. The Latin American market is currently underpenetrated relative to a mature market like Canada. As an indication of the company's growth ambitions in this region, it recently announced an increase to its Dollarcity store target from 600 by 2029 to 850 stores. By the end of the decade, Dollarcity stores will make up approximately one-third of Dollarama's total network. While Dollarcity's gross margin lags the ~46% average of Dollarama, the subsidiary is making progress to narrow the gap. The 50.1% stake in the company in the subsidiary is worth approximately $8-9/share.

Returning Cash to Shareholders

Dollarama has been prolific in its use of NCIB to boost EPS. Have shrunk share count from 430M to 303M since 2014. This is a reduction of approximately 29% of the public float over the past 8 years. This NCIB program has been achieved through a mixture of approximately 75% free cash flow and 25% debt. This has been a sustainable model as earnings growth has exceeded the after-tax cost of debt. This intentional use of leverage has led to the company's capital structure evolving over time. Adjusted net Debt to LTM EBITDA has moved up over the past decade from under 2X in 2012 to 2.84X in 2022. A recent DBRS Morningstar ratings report indicates a comfort level with this practice and current credit rating <3.5X Debt to EBITDA.

Shrinking the share count so dramatically, while also pursuing organic growth and adding stores has resulted in healthy EPS growth. Under the current NCIB running from July 2022 to July 2023, Dollarama is approved to repurchase up to 18,713,765 of its common shares, representing 7.5% of the public float. RBC Capital Markets anticipates an annualized buyback yield of approximately 5.5% going forward. Should the cost of borrowing increase significantly, Dollarama may choose to forgo or use the debt-funded portion of its NCIB opportunistically. Morningstar anticipates FCF of $800M and $900M in F2023 and F2024, respectively, which could be supplemented with debt to repurchase shares.

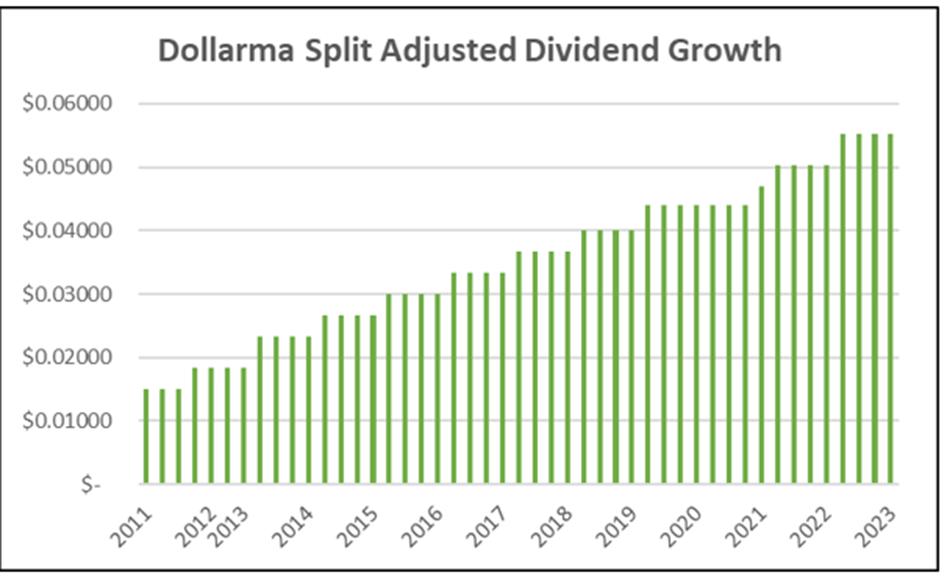

Dividend Growth

In addition to returning cash through share buybacks, Dollarama has remained committed to growing its dividend. Dollarama pays a quarterly dividend of $0.0553 for an annual payout of $0.22. The company initiated its dividend program in 2011 and has consistently announced annual increases for the past 12 years.

Dollarama Dividend Growth (Author)

{kind=link}

While the company's dividend yield is inconsequential at 0.29% this is as much a reflection of the company's rapid share price growth. With a 10-year dividend growth rate of almost 12% and a payout ratio of 9%, Dollarama is a candidate for continued dividend growth as the company matures. Yield will improve over time as EPS growth moderates and the company pivots to returning more cash to investors through dividend increases rather than share repurchases. For investors who don't require current income, Dollarama is a good option for building a high yield-on-cost investment over a longer time horizon.

Dollarama Dividend CAGR (Author)

Risk Analysis

In June 2022, DBRS Morningstar confirmed Dollarama's credit rating of BBB with stable trends. The rating agency expects that Dollarama is well-equipped to continue modest margin expansion despite the current inflationary environment:

DBRS Morningstar believes that the Company has ample room to absorb these inflationary pressures within the context of the current rating category. Furthermore, the rating actions continue to incorporate Dollarama's disciplined expansion plans, which are steadily increasing its scale and geographic diversification, as well as DBRS Morningstar's expectation that the Company will maintain its consistent financial management practices.

While I expect Dollarama to be a net beneficiary of persistent inflationary pressures, wage pressures could have an impact on margins if unemployment stays low for longer. Similarly, cost pressure from domestic vendors and suppliers could negatively impact margins. As an importer of goods, Dollarama would see margins under pressure if the Canadian dollar weakened for a sustained period.

Operating in Latin America could expose the company to some political risks. Peru and El Salvador in particular have had some recent political turbulence. As the Dollarcity business grows in revenue, the impact of FX fluctuations could create currency risk. In my view, however, the opportunity in the underpenetrated region with fast-growing consumer spending levels more than outweighs these concerns.

Dollarama has a forward P/E of 27X, implying a sustained growth trajectory. While I think this valuation is warranted, the stock is priced for growth at the high end of the 4-5% same-store sales growth range and continued margin expansion.

Investor Takeaways

Dollarama is an impressive growth story that still has gas in the tank. The ability to pass on inflationary pressure to customers in the form of higher price points, up to $5.00, allows the company to continue to grow EBITDA margins despite higher product costs. Dollarama's ambitious domestic and Latin American expansion plans, along with improving foot traffic and average transaction values, will all contribute to continued sales growth. An effective financial management program that has boosted EPS through share repurchases and a growing dividend signal a strong total return opportunity.

For further details see:

Dollarama: The ($5) Dollar Store