D - Dominion Energy: Still Too Much Debt For Me To Consider Buying

2023-09-06 01:47:53 ET

Summary

- Dominion Energy provides natural gas and electricity to customers in 16 states.

- Although they enjoy inelastic demand for their services, the company has been experiencing an ever-worsening debt situation.

- As of this most recent quarter, they are paying more in dividends and interest than they earn in income.

- I currently rate D stock as a Hold.

Thesis

I keep a short list of companies I would be willing to buy the dip on during the peak fear that black swan events typically bring. Because demand for their services is inelastic, most of the list is dominated by utility providers.

I continue to watch Dominion Energy, Inc. ( D ) in hopes of adding it to this list. The last time I published an article on Dominion was in March and at that time, I decided their debt situation was too unattractive. Since then, their debt situation has only worsened. After looking over their financials and valuation, I presently rate Dominion stock as a Hold.

Company Background

Dominion provides electricity and natural gas to about 7 million customers across 16 states. They are headquartered in Richmond, Virginia, and have pledged to be net-zero emissions by 2050.

D Company Background (Seeking Alpha)

{kind=link}

Long-Term Trends

The United States natural gas market is projected to have a CAGR of 5% through 2028. The United States power market is projected to have a CAGR of over 5.6% until 2027. The Inflation Reduction Act is expected to provide tailwinds for utility providers for years to come.

The Federal Reserve has placed a target for long term average inflation of 2% , which usually comes with a loose job market . With them still battling inflation they are expected to continue hiking rates and maintain them at an elevated level for an extended period of time before they can lower them. Projections for the pace of lowering will continue to change as events unfold, but current estimates place it around 5.1% by the end of 2023, 3.6% by the end of 2024, and 2.4% by the end of 2025.

Annual Financials

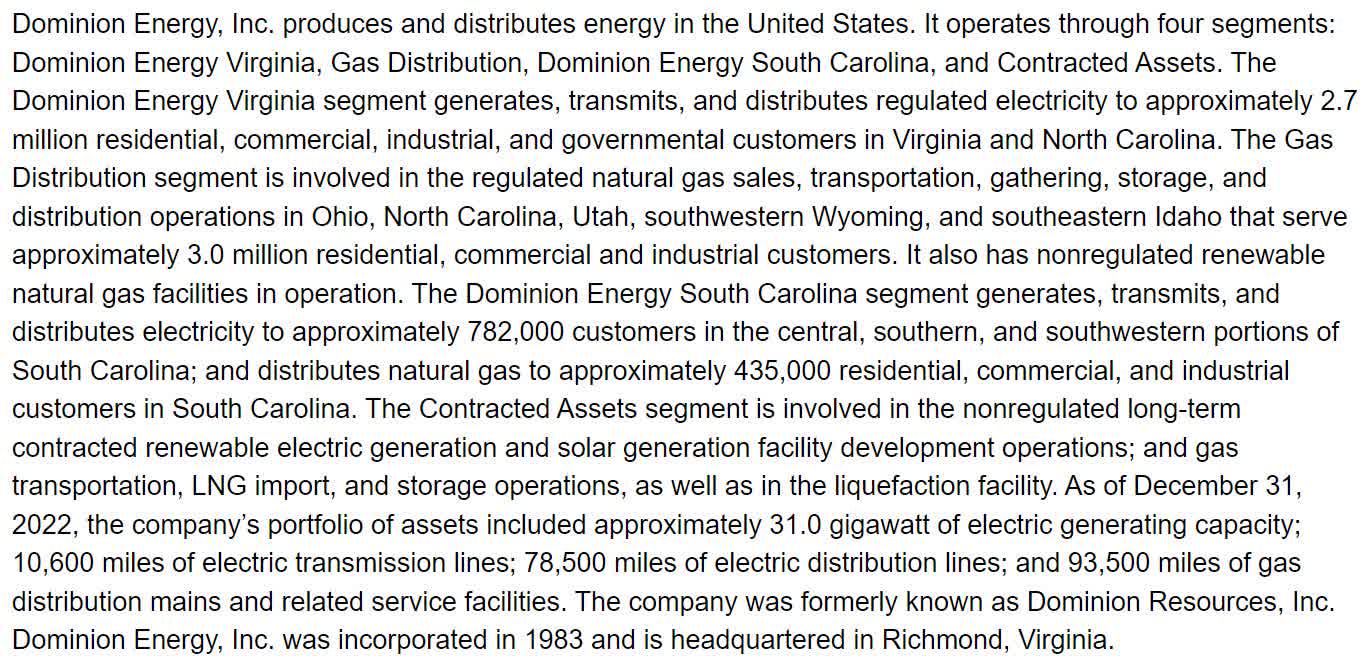

The company experienced a decline in revenue and reached a low in 2018. Annual revenue has grown significantly since then. In 2013 they had an annual revenue of $13.12B; by 2022 that had grown to $17.174B. This represents a total rise of 30.9% at an average annual rate of 3.43%.

{kind=link}

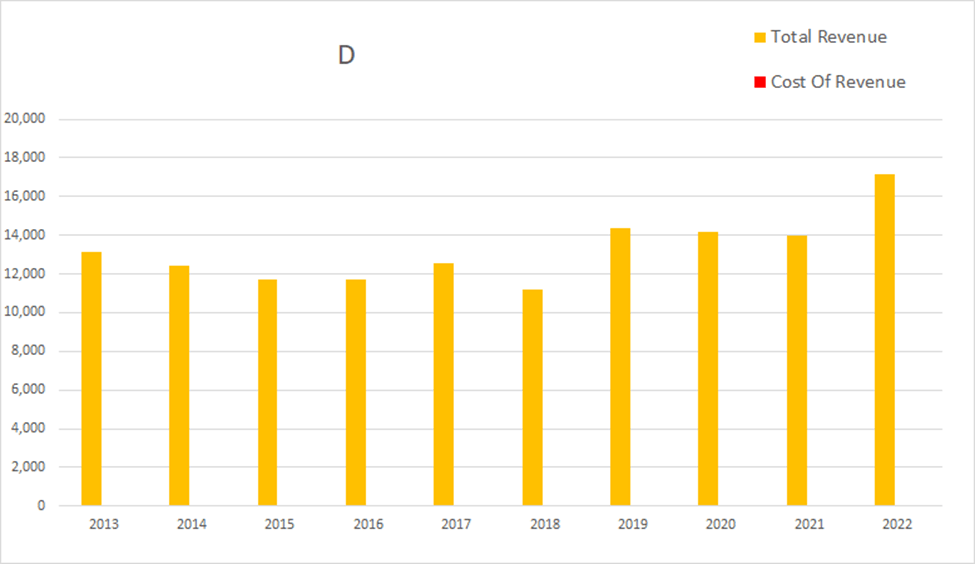

Because much of it comes from an atypically large Unusual Item, I am treating their net margin for 2021 as an outlier and ignoring it.

D Annual Unusual Items (Seeking Alpha, Dominion Financials)

As of the most recent annual report, EBITDA margins were 45.92%, operating margins were 27.79%, and net margins were 5.79%.

{kind=link}

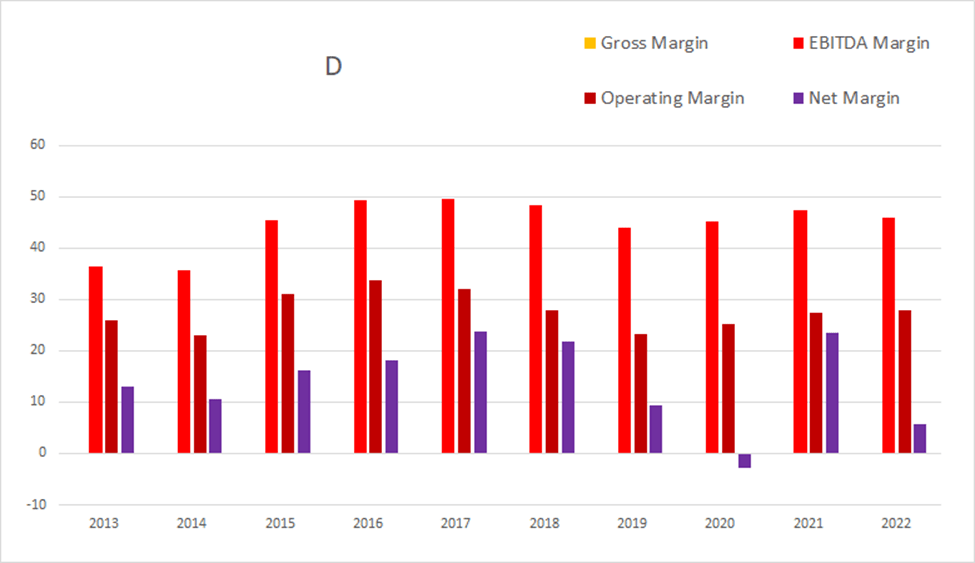

Their dilution rate over the last decade was quite unappealing. Total common shares outstanding was at 581M in 2013; by the end of 2022 that rose to 835M. This represents a 43.72% increase in share count, which comes out to an average annual rate of 4.86%. Over that same period, operating income rose from $3,387M to $4,773M, a 40.92% total rise at an average rate of 4.55%.

D Annual Share Count vs. Cash vs. Income (By Author)

{kind=link}

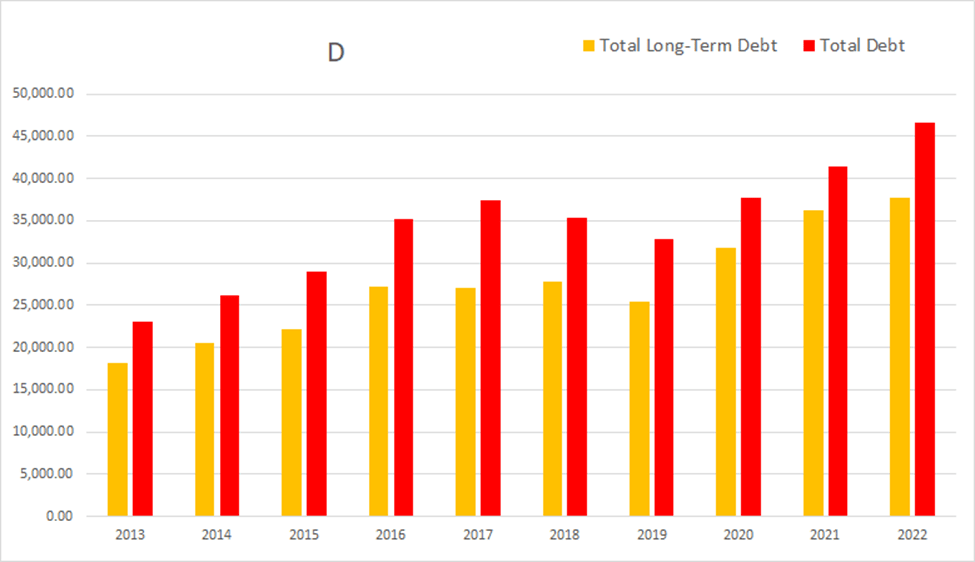

Their debt has grown significantly over the last decade. As of the 2022 annual report, they had -$1.001B in net interest expense, total debt was $46.608B, and long-term debt was $37.730B.

{kind=link}

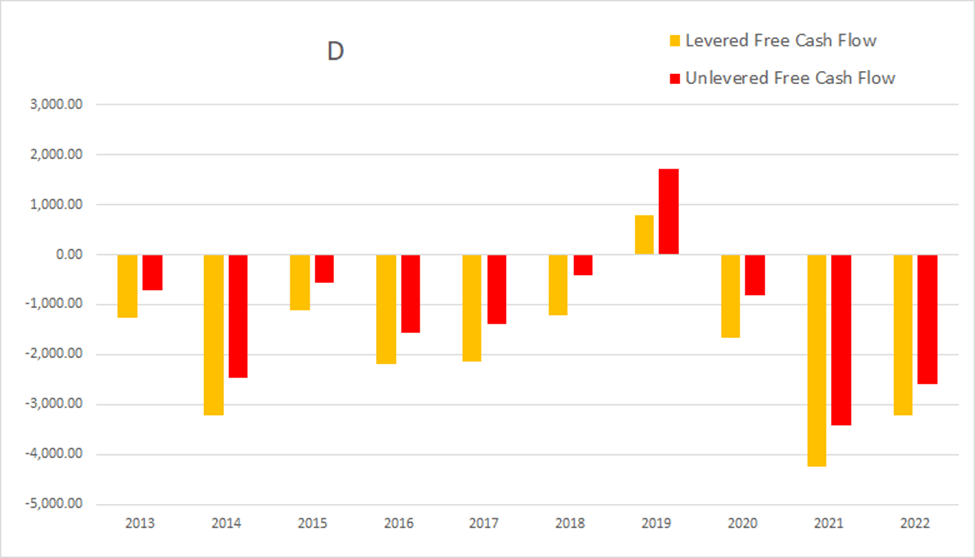

Their cash flow situation has been unappealing for most of the last decade. As of this most recent annual report, cash and equivalents was $153M, operating income was $4.773B, EBITDA was $7.886B, net income was $994M, unlevered free cash flow was -$2.592B, and levered free cash flow was -$3.2175B.

D Annual Cash Flow (By Author)

{kind=link}

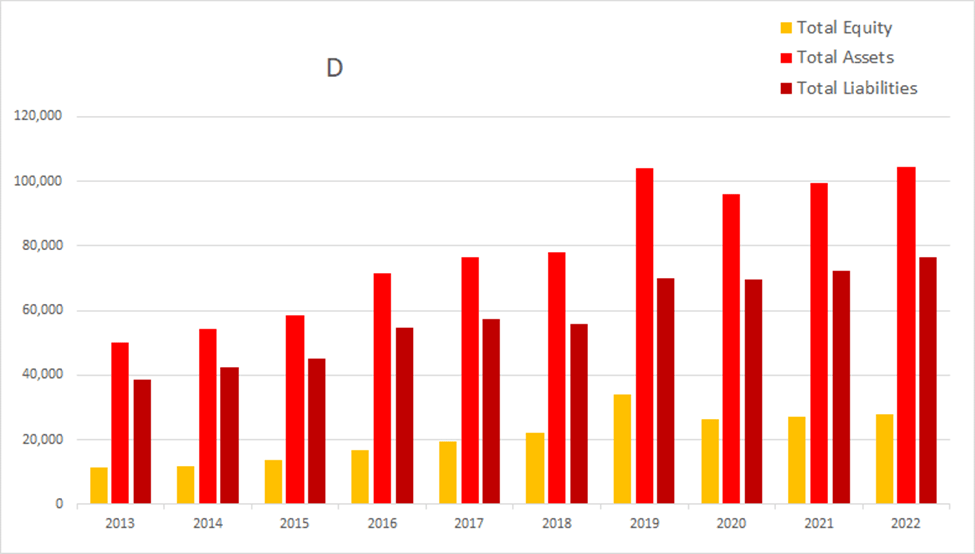

Other than the temporary spike in 2019, their total equity has been slowly rising.

D Annual Total Equity (By Author)

{kind=link}

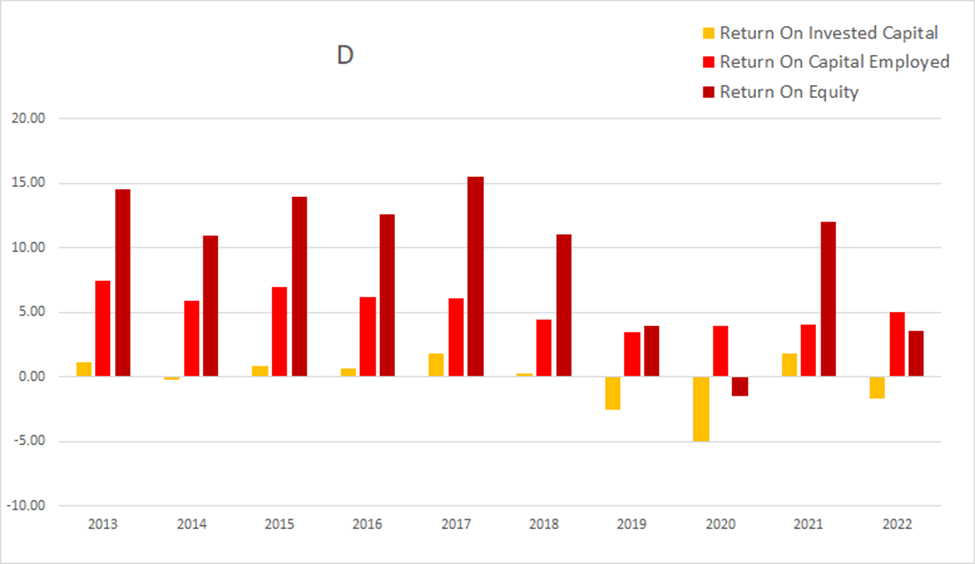

They have been unable to consistently produce attractive values for return on invested capital. As of the most recent annual report ROIC was -1.66%, ROCE was 5.00%, and ROE was at 3.57%.

{kind=link}

Quarterly Financials

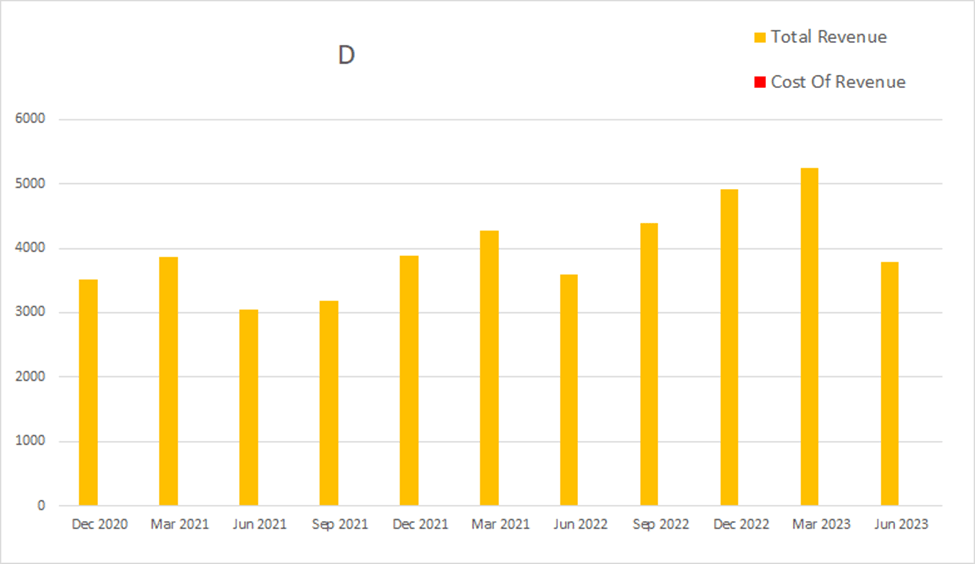

Their quarterly financials show clear seasonality. Dominion typically experiences lower revenue during warmer months and higher revenue during colder months. Eight quarters ago Dominion had a quarterly revenue of $3,038M. Four quarters ago that had grown to $3,596M; by this most recent quarter that had further grown to $3,794M. This represents a total two-year increase of 24.88% at an average quarterly rate of 3.11%.

D Quarterly Revenue (By Author)

{kind=link}

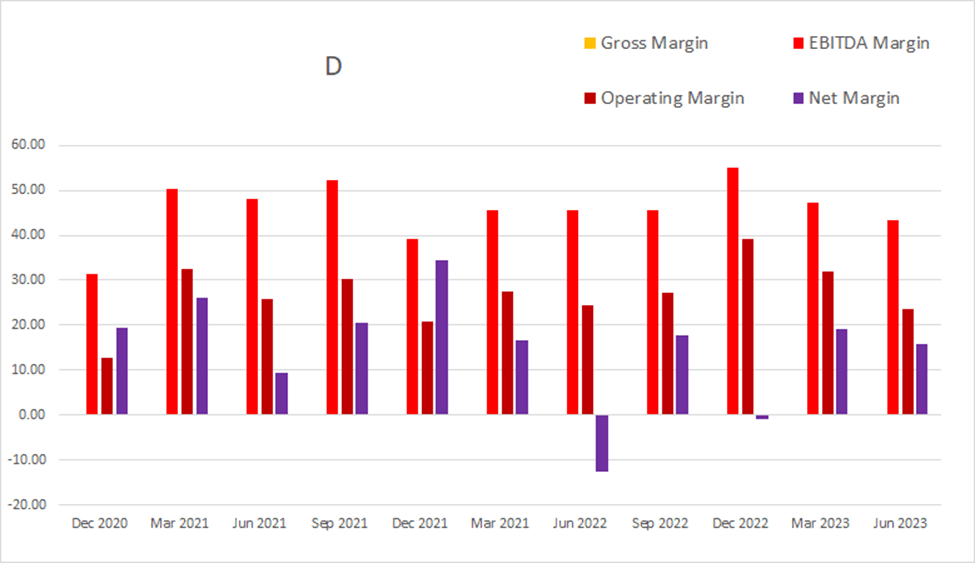

This seasonality also strongly affects margins. As of the most recent quarter, EBITDA margins were 43.44%, operating margins were 23.51%, and net margins were at 15.79%.

D Quarterly Margins (By Author)

{kind=link}

The sum of their last eight quarters of dilution comes to 3.68%. This falls below their ten-year average of 4.86%. Over the last four quarters this dilution rate dropped to 0.60%. The pace of dilution appears to be slowing.

D Quarterly Share Count vs. Cash vs. Dilution (By Author)

{kind=link}

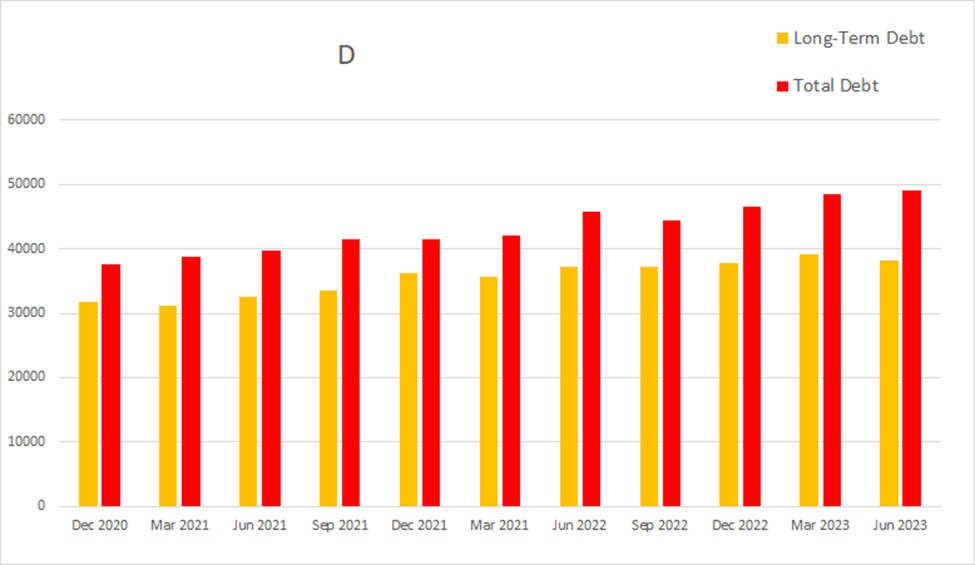

The most recent quarter, Dominion had -$430M in net interest expense, total debt was at $48.978B, and long-term debt was at $38.134B.

{kind=link}

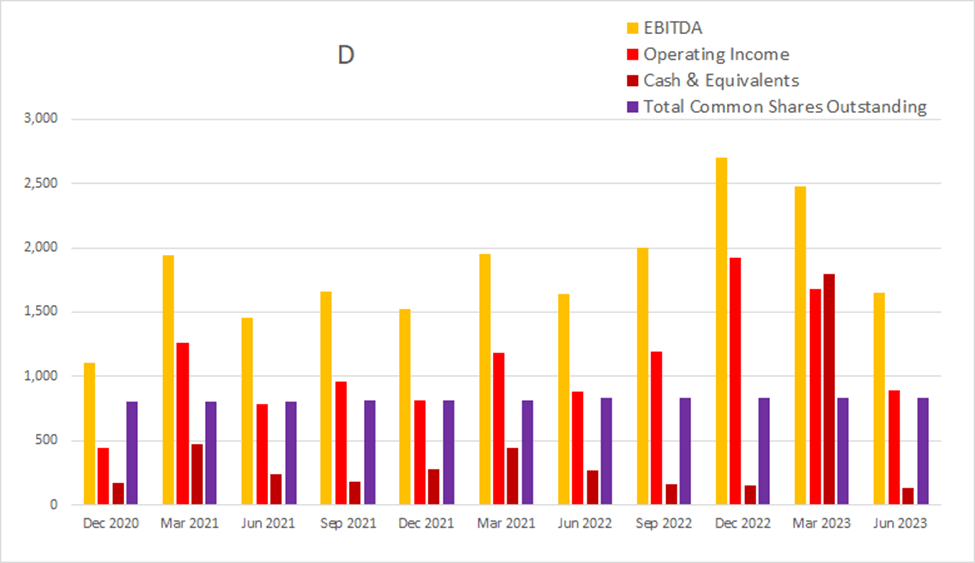

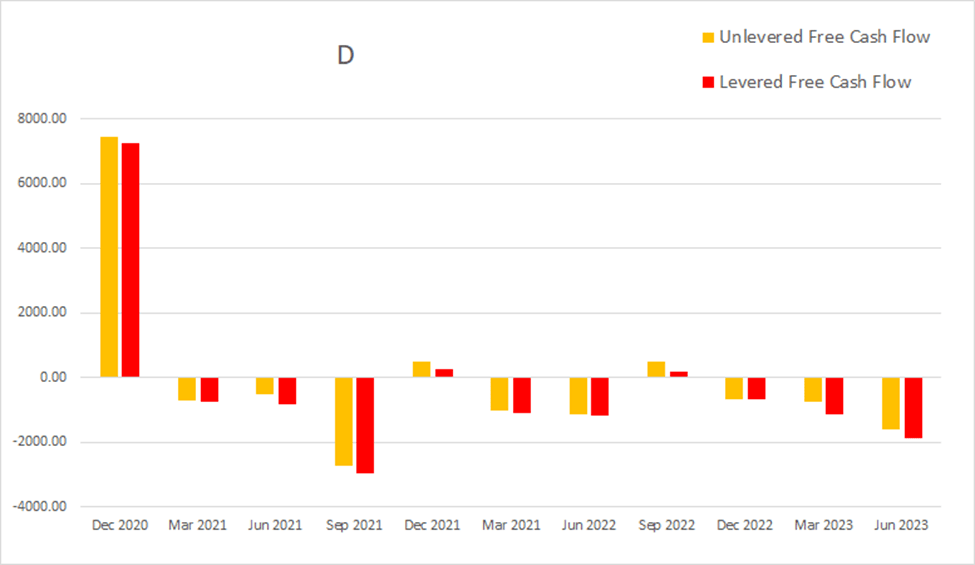

Even when looked at on a quarterly basis, their cash flow situation continues to be unappealing. As of the most recent earnings report, cash and equivalents were $137M, quarterly operating income was $892M, EBITDA was $1648M, net income was $599M, unlevered free cash flow was at -$1599.5M, and levered free cash flow was at -$1868.3M.

D Quarterly Cash Flow (By Author)

{kind=link}

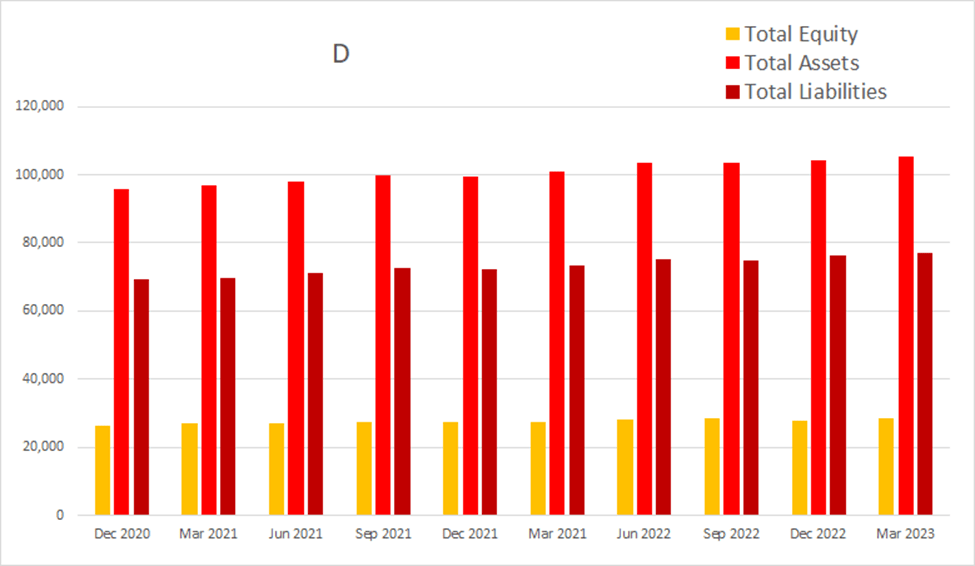

Total equity continues to steadily rise.

D Quarterly Total Equity (By Author)

{kind=link}

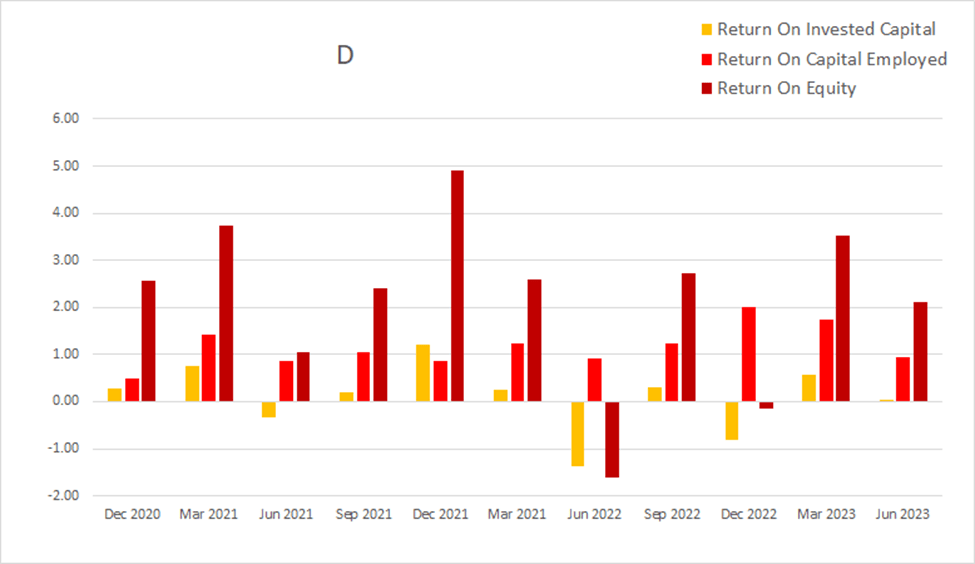

I was hoping to see some attractive returns during the quarters where seasonality is handing Dominion higher revenue. However, even while looking at them on a quarterly basis, their returns are still unappealing. As of the most recent earnings report, ROIC was 0.05%, ROCE was 0.94%, and ROE was at 2.11%.

D Quarterly Returns (By Author)

{kind=link}

Valuation

As of September 1st, 2023, Dominion had a market capitalization of $40.06B and traded for $47.88 per share. They currently have a forward P/E of 13.88x, an EPS Long-Term CAGR of -2.85%, and a forward Yield of 5.58%. Using these values I calculated a PEGY of 5.084x and an Inverted PEGY of 0.1967x. Multiplying the inverted PEGY by today's share price produces a fair value estimate of $9.42 per share.

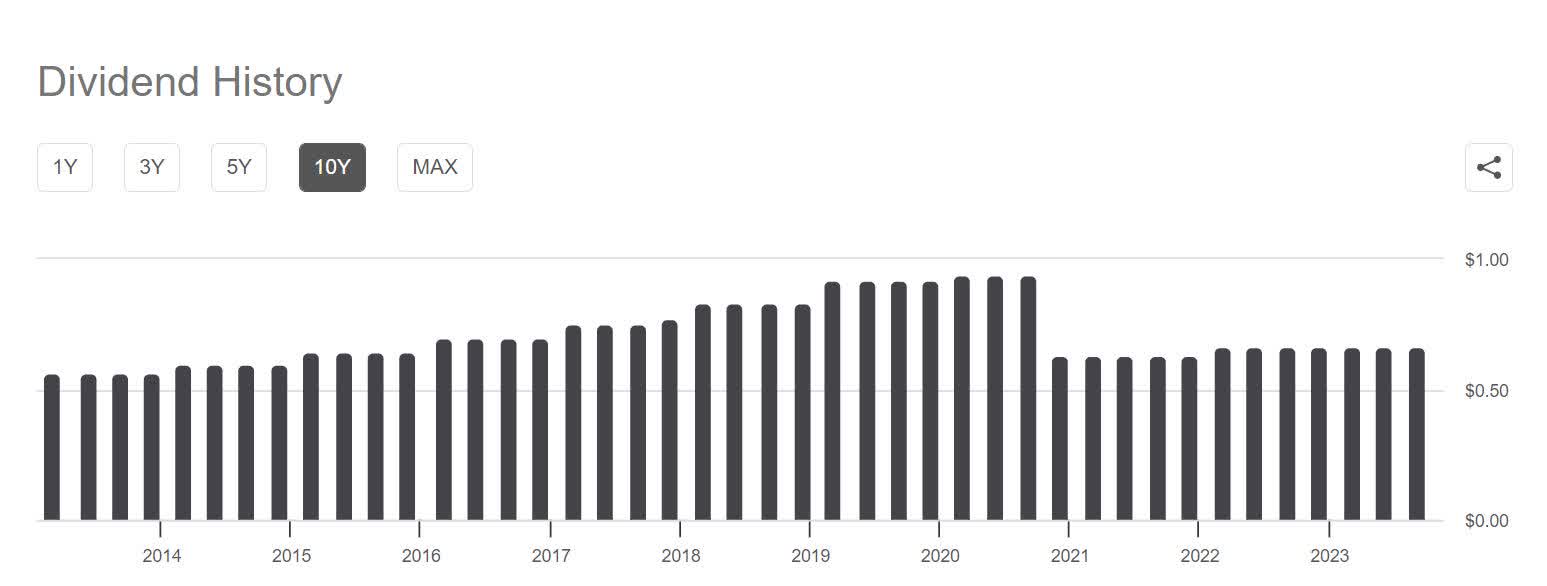

If I instead chose to take a look at value from a discounted cash flow perspective, I get a noticeably different result. Using a discount rate of 9%, their present annual payout of $2.67 , their projected dividend 10Y CAGR of 1.89% , and assuming they can maintain this growth rate for the full 20 years, I calculated a fair value estimate of $38.26 per share.

D Dividend History (Seeking Alpha)

{kind=link}

Risks

Dominion has a significant debt load. The Fed is already in a position where it is holding rates at an elevated level in order to lower inflation and loosen the job market. If inflation were to begin rising again, the Fed would be forced to raise rates further. Their already significant debt load could become even more of a burden.

Catalysts

The company would directly benefit from a lowering of interest rates. With consumers already used to an inflationary environment, they also stand to benefit from any price hikes they can pass on to their customers.

Conclusions

The last time I examined Dominion, their most recent financials were for the quarter ending in December 2022. At the time long-term debt was $37,730M while quarterly unlevered cash flow was -$678.1M. Currently, they have $38,134M in long-term debt, and quarterly unlevered cash flow is -$1,599.5M. The situation has only gotten worse.

Overall, Dominion appears to be saddled with negative cash flow due to a combination of their debt and their dividend obligations. Instead of buybacks being used to power up dividend increases and producing attractive yield on cost for long-term holders, they have been plagued with dilution and were forced to cut their dividend in 2020.

This most recent quarter, Dominion only had an operating income of $892M, yet paid $558M in dividends and $430M in net interest expense. I know most of the long-term holders are not going to want to hear this, but I believe they have painted themselves into a corner and are very quickly running out of options. Even if they somehow work out a deal where they stop paying interest on their debt and are able to devote 100% of their operating income to paying down their principal, their $37,730M in long-term debt would take 42.3 quarters to pay all the way down.

For me to consider adding them to my black swan list, I would first require that Dominion slash its dividend to zero and focus on paying its debt down for at least the next 5-7 years. This may sound heretical to some of you, but I consider it incredibly irresponsible to continue paying out unsustainable yield in the face of crippling debt. When faced with a conflict of interest, I believe companies should always prioritize the long-term health of the company over short-term shareholder returns.

Because of their significant debt risk, if I were to open a position in Dominion Energy, I would not reinvest the dividends. Instead of turning on the DRIP, I would instead attempt to take risk off the table by lowering my cost basis as quickly as possible. I would look to sell covered calls on the position while moving all of the dividends and premium collected to other investments.

For further details see:

Dominion Energy: Still Too Much Debt For Me To Consider Buying