SO - Dominion Energy Upholds Big Dividend Shares Pop

2023-11-08 00:25:07 ET

Summary

- Dominion Energy reported 3Q 2023 earnings, driving multiple stakes into the ground to reduce uncertainty that's been dogging the shares.

- Management is executing clear priorities to re-tool the company. The CVOW project remains on time and on budget.

- CEO Bob Blue offered a straight-line commitment to the current dividend. No walk-backing.

- Shares are heavily discounted and backstopped by the current 6 percent dividend yield.

- Long-term, buy-and-hold income investors may want to give this one a good look.

On November 3, Dominion Energy ( D ) reported 3Q 2023 earnings. For investors following the company narrative, management provided the necessary guidance to remove a great deal of the uncertainty surrounding the stock. Post-earnings, the stock popped on high volume; of particular note for a utility ticker.

In this article, the third I've written this year advocating Dominion common stock, we will do a quick history review, reiterate my investment thesis, and then re-examine the thesis' validity based on the financial report and commentary provided by CEO and Chairman Bob Blue.

Background

A 33 percent dividend cut announced mid-year 2020 soured many income investors on the stock. Essentially, the cut was in response to the company being pushed into canceling the Atlantic Coast Pipeline. Anti-pipeline opponents tied up the project in litigation and despite winning a Supreme Court case, project timing was scuttled while anticipated construction costs skyrocketed. Management elected to bail out of the endeavor.

Nonetheless, as late as September 2022, Dominion stock still traded in the low $80s range.

Shares took a plunge in conjunction with 3Q 2022 earnings when CEO Bob Blue announced a "top to bottom" business review. This spooked some investors who thought the review was cover for another dividend cut. Others interpreted the business review to mean management lacked purpose and direction.

Compounding the uncertainty, Dominion management was moving forward on a $9.8 billion offshore wind farm. Plans were in place to construct a massive, 2.6 gigawatt wind farm off the coast of Virginia. The project, named the Coastal Virginia Offshore Windfarm (CVOW), was to begin construction in 2024 and become operational in 2026. The one-of-a-kind project has drawn criticism from a variety of investor groups.

Then, through the summer of 2023, management began announcing major asset sales: including Cove Point LNG and three large gas distribution companies. These sales totaled $17.5 billion. No small potatoes.

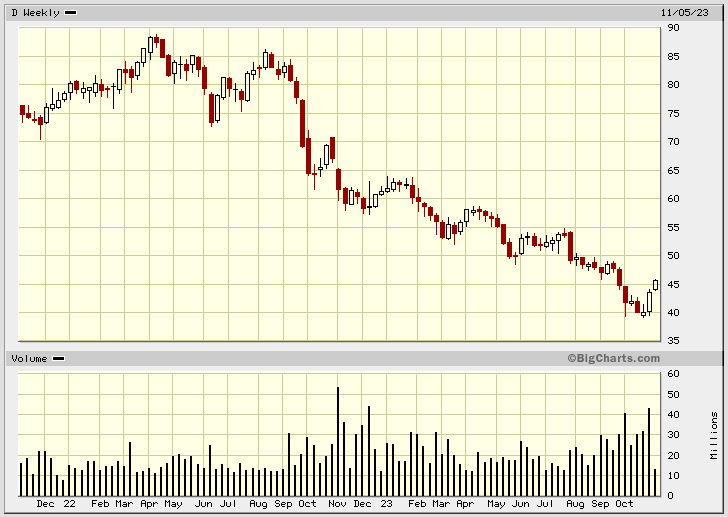

By late 2022, D stock nosedived from $80 to $60, then appeared to stabilize.

Dominion Energy -- Price and Volume (2-year)

{kind=link}

However, throughout most of 2023, shares continued to fall: in part due to questions around the forward business plan, rapidly rising interest rates, general investor disdain for Utility stocks, and negative sentiment around CVOW.

By late October, shares fell to a multi-year low, settling just below $40.

An Investment Thesis

I first got on board Dominion Energy stock in January 2023. Indeed, by then the stock had tanked 25 percent from previous highs, despite maintaining reasonable fundamentals. The 2020 dividend cut, an open-ended business review, and sentiment around the CVOW project created a toxic stew.

My investment thesis involved the following underpinnings:

-

Look to buy what's out-of-favor

-

Uncertainty with sideboards creates opportunity

-

Do not mix my politics with my investments, let the data lead the way

-

Follow operational and financial fundamentals

-

Seek deep-value stocks with a good narrative

Dominion Energy ticked all the boxes.

As interest rates rose, utility stocks were clearly out of favor. Dominion Energy was especially out of favor.

Dominion Energy was caught up in considerable uncertainty; however, the scale and regulated nature of its core business provided insulation. Management recognized the current path wasn't going to generate adequate returns and decided to do something about it.

Negative sentiment about CVOW did not appear supported by the facts. CVOW is a regulated utility project; encouraged by the Virginia legislature and approved by the Virginia State Corporation Commission (a public utility commission).

Dominion Energy fundamentals remained reasonable by historical and comparison with peers. I highlighted this in an article published on January 18, 2023, entitled, " Switching Horses on Valuation: Southern Company Vs. Dominion Energy ." Southern Company ( SO ) remains one of the better-run public utility corporations.

Nevertheless, Dominion Energy's common stock continued to take a beating. Shares had dropped from $80 to $60, and after advocating the stock, shares fell by another third to ~$40. These prices just didn't compute using historical or comparative valuation methodology.

In September, Seeking Alpha editors published my second article on Dominion entitled, " Dominion Energy: Enbridge Deal Sets the Table ." Despite the bloodshed, pieces were falling into place.

All of which brings us to the most recent earnings report.

What Did We Learn from the 3Q 2023 Earning Release?

Let's break it down.

The Quarterly Numbers

There were no startling revelations in the quarterly financial package . But there were at least two notable nuances in the package.

Dominion Energy is a company in the midst of a major transition. Therefore, focusing on the short-term financials is unlikely to provide a great deal of investment insight. Nonetheless, there were two items that caught my eye.

-

The TTM FFO (Funds From Operations) to Debt ratio rose to 15 percent.

Why is this important? One of the major tenets of the financial restructuring has been to bolster the balance sheet. For utilities, FFO / Debt is an important measure of balance sheet strength. Previously, Dominion management reported a ratio below 14 percent was the rating agencies' "downgrade threshold." The 3Q report indicates the company is now out of the line of fire.

-

TTM total electric sales grew 3.1 percent. YoY DVA and DSC customer base grew 1.0 percent and 1.7 percent, respectively.

Dominion management elected to concentrate the business on regulated electric service in Virginia and South Carolina.

Dominion Virginia and Dominion South Carolina continue to grow smartly: both in terms of customers and electric usage. For regulated utilities, a growing customer base and total KW electric sales are two of the most powerful engines to fuel increased earnings and cash flow.

By comparison, peer utility Southern Company reported 3Q total electric sales improved 2.1 percent, and total electric customers grew by 1.2 percent.

Mid-Atlantic and southeastern U.S. states remain relatively strong in terms of population growth and electric consumption. This bodes well for Dominion Energy and management's decision to focus on electric service in these regions.

CEO Bob Blue Conference Call Remarks

In contrast to the raw numbers, CEO Bob Blue shot off some big guns on the earnings conference call . He addressed a number of uncertainties head-on. CFO Steven Ridge provided a solid backup.

The following slides from the earnings presentation capture many of the themes discussed on the call.

investors.dominionenergy.com investors.dominionenergy.com

{kind=link}

{kind=link}

Drilling down, I've highlighted headlines in bold and followed with supporting commentary by Dominion CEO Bob Blue.

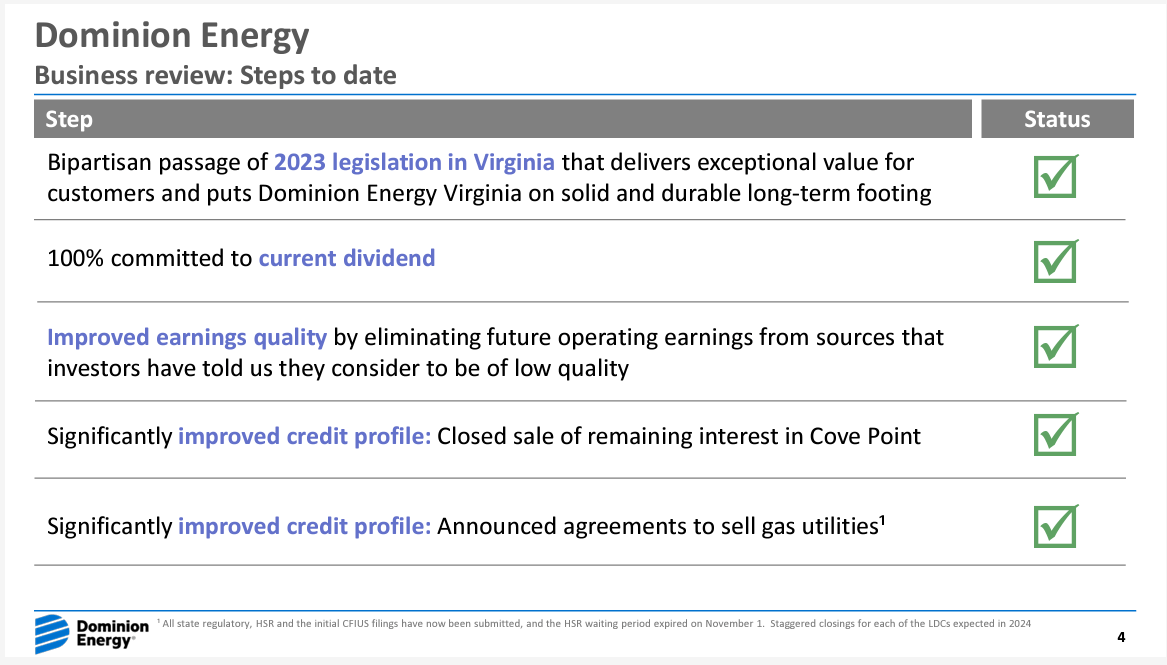

The current dividend is secure.

CEO Bob Blue

We've been and continue to be 100% committed to our current dividend. Earnings growth combined with a period of low to no dividend growth will restore our payout ratio to a peer appropriate range over time.

During the Q&A session, Mr. Blue reiterated himself. He didn't stutter:

Jeremy Tonet - Analyst

Appreciate the commentary just laid out there with regards to how you're talking about the review, but just wanted to go to the dividend, if I could, and just wanted to see if the dividend policy remains intact, even if for some reason you keep all of wind [CVOW]. Is there any scenario where, keeping the dividend at these levels [$2.67 annualized] just wouldn't make sense?

CEO Bob Blue

We're committed to the dividend, Jeremy. As we said, we're 100% committed to the dividend. Trying to talk about scenarios that people could imagine, I don't think is terribly productive. We've been committed to the dividend since the beginning. We haven't wavered in that. We're not wavering on it today.

The balance sheet is materially stronger, with further improvement to come. Management followed through on their commitment to use asset sale proceeds to pay down debt.

CEO Bob Blue on the Cove Point sale

On a strategic front, we announced and closed on the sale of our remaining interest in Cove Point.

We applied the $3.3 billion of after-tax proceeds to reducing debt. This was a significantly credit accretive transaction done with a high-quality counterparty after a robust competitive process.

CEO Bob Blue on the gas distribution asset sales

We announced the sale of our gas utilities to Enbridge, one of North America's largest energy infrastructure companies. We ran broad and competitive processes for each of the individual utilities and we are delighted to have found a partner that not only shares our ideals around safety, reliability, customer service, employee treatment and community investment, but that was also the most competitive option on value across each of the three utilities.

We intend to apply 100% of the estimated after-tax proceeds of nearly $9 billion to reducing parent-level debt , which, based on current rates, will result in the reduction of around $500 million of pre-tax interest expense annually.

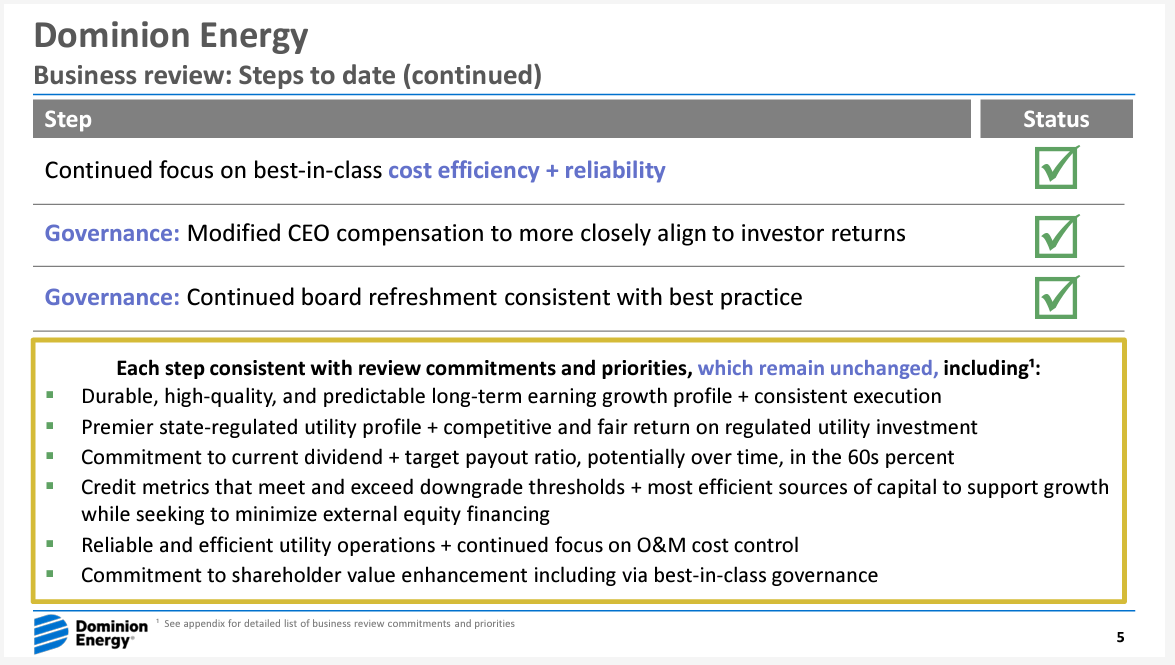

There's fresh blood in the boardroom. Governance and executive compensation are in focus.

CEO Bob Blue on board transition

As part of our ongoing Board refreshment process , we've now added six new directors since 2019, bringing the average tenure of our 11 directors to six years.

CEO Bob Blue on his pay package

Finally, on governance, the Board, in direct response to investor feedback, modified my compensation structure for 2023 to align my economic incentives more closely with the financial interests of our shareholders. As a result, 100% of my 2023 long-term incentive compensation is now performance-based, 70% is premised solely on three-year relative total shareholder return, with a 65-percentile relative performance required to achieve a 100%, which is well above the medium threshold of industry peers.

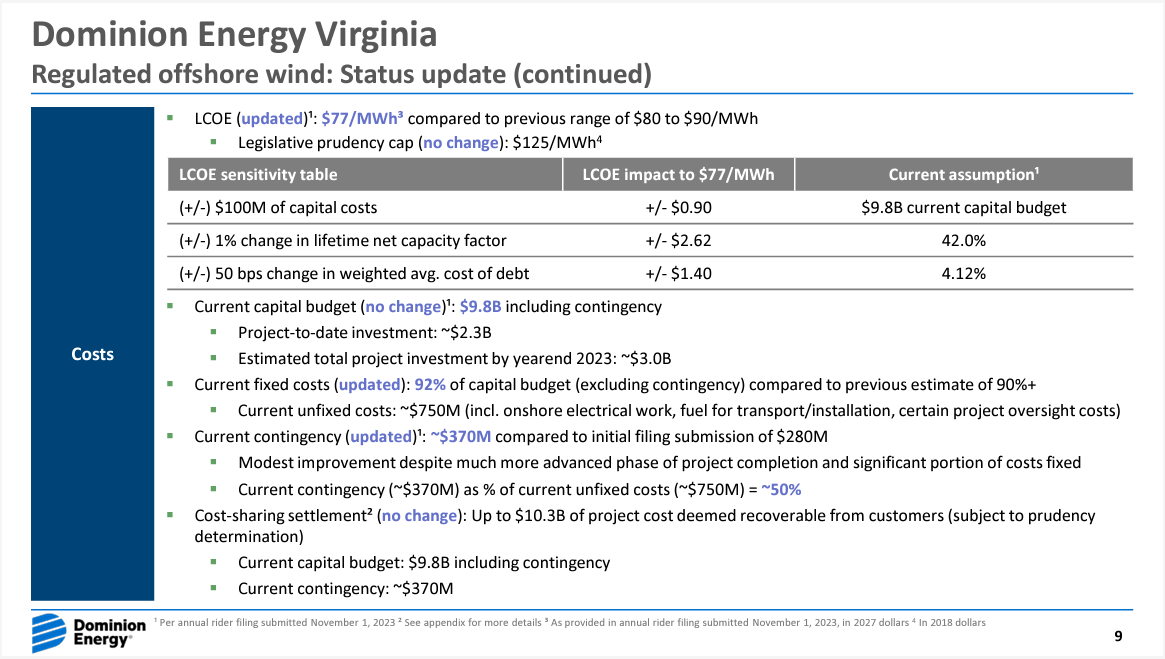

The CVOW project remains on time and on budget. The LCOE (Levelized Cost of Energy) for the project was lowered. Dominion management now seeks an outside equity partner on the project.

CEO Bob Blue on project LCOE and costs

Turning to cost on Slide 9 [see below], I draw your attention to the key metrics we have included in the slide, much of which is by way of reminder. First, we updated the project's expected LCOE in our filing earlier this week to approximately $77 per megawatt hour, as compared to our previous range of $80 to $90.

Next, the project's total cost remains $9.8 billion. Project to date, we have invested approximately $2.3 billion, which we expect to grow to around $3 billion by year end. I am pleased to update that our current project costs, excluding contingency, have improved to 92% fixed.

{kind=link}

CEO Bob Blue on obtaining CVOW equity partners

As part of the business review, we're in advanced stages of a process to transact with a partner with a focus on pro-rata sharing of project costs. The process has driven considerable interest from attractive and high-quality potential counterparties.

We've got multiple parties who are engaged with us, and our objective is a true equity partner with pro rata sharing of project costs. That's what we're after.

Looking Forward

Looking ahead, management clarified several additional items.

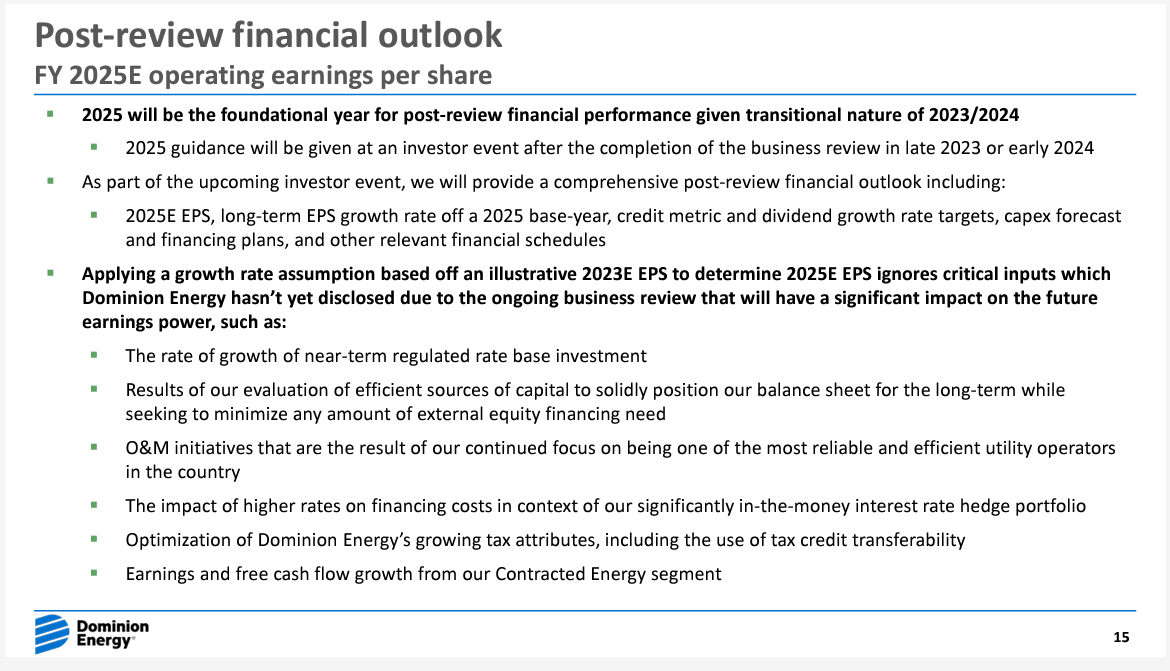

2024 will be a transitional year. The company's new baseline year is 2025. CFO Steven Ridge cautioned Street analysts against trying to use 2023 adjusted EPS results (expected to be $2.90) to run rate future earnings potential. He stated details will be provided at an investor day conference to be held in late 2023 or early 2024.

Upcoming years will mark a multi-year period of increased growth capex projects . These projects will highlight both conventional and alternative energy sources. Regulated utilities enjoy good, fixed returns on such projects, yet low competitive pressure and financial risk.

Management emphasized the stronger balance sheet is to be durable . Dominion Energy should realize over $500 million a year in reduced interest expense and be out of the rating agencies' crosshairs.

{kind=link}

What It Means for Investors

In 2023, I've been constructive on D shares. I believe the stock has and continues to be a unique opportunity to participate in equity that Mr. Market has significantly miss-priced and collect a 6 percent yield to boot.

The 3Q2023 earnings report provided answers to a number of question marks. Management laid out themes and has been executing on the priorities:

-

focus the business on regulated electric service

-

sell non-core assets

-

generate a strong/durable balance sheet

-

defend the current dividend

-

complete the CVOW project on time and on budget

-

re-tool the company to create sustainable, long-term shareholder value

Nevertheless, challenges remain; primarily construction and operational execution risk.

Currently, I do not believe there is enough management input to fully assess the stock's fair value. However, a reasonable starting point is to look at the current dividend yield versus peers. As I write this article, the yield is 5.9 percent. This is about 200 bps higher than peers. If Dominion stock provides a 5.0 percent yield, shares should rise to $54.

Prior to 3Q earnings, D shares were bid down to about $40. In the past three trading sessions, the stock has risen over 13 percent on high volume. At least one brokerage house rerated the stock. Post-earnings, I expect more to follow.

As with any stock, always buy in increments, never chase, seek to defend basis, and keep close tabs on the current newsfeed, specifically the upcoming Dominion Energy investor day.

For further details see:

Dominion Energy Upholds Big Dividend, Shares Pop