DOMO - Domo: Downgrade On Enterprise Slowdown

2023-04-04 13:08:09 ET

Summary

- The 4% - 7% revenue growth outlook in FY 2024 makes Domo a far cry from what it should be: a 20% - 30% growth stock.

- Enterprise sales productivity issue is a bump in the road. I adjusted the baseline scenario to project Domo to reclaim 20%+ growth in FY 2027.

- Domo's market positioning is still solid, though the growing AI-driven trend and specialization dynamics in BI value chain may present a threat.

I am downgrading Domo (DOMO) to neutral at least for the medium term. I believe that the recent sales productivity issues and leadership changes may delay Domo's progress in capturing more sizable shares of the enterprise market. Enterprise market share is a key component of my long-term growth story for the company. Accordingly, I also have adjusted my model to account for these factors.

The share price is currently hovering around the all-time low, and the 1.3x P/S may seem attractive. But it is best to wait until there are signs of improvement in Domo's enterprise sales motion and IT spend recovery momentum into the next few quarters before considering an upgrade to my position.

Background

I have been on both sides of Domo. I covered it for the first time in 2019 and most recently in 2020 . In both cases, I observed positive reactions to my calls:

- In 2019, I initiated my coverage in August with a neutral stance as I saw Domo taking in a relatively disproportionate amount of debt while burning $100m+ worth of operational cash on a yearly basis, yet I felt that Domo could be a strategic acquisition in the BI space, following Tableau's path. The following month, Domo shed nearly 30% of its value as its share price dropped to a yearly low of ~$15 per share.

- In 2020, I upgraded my previous neutral call and projected an end-year price target of $37 (~15% upside). At the time, Domo exceeded my expectations. The following year, the share price more than doubled and even reached an all-time high in August.

In 2022, things started to decelerate for Domo, and in fact, the tech sector in general. Shares of tech giant Amazon ( AMZN ), for example, plunged by ~50% while likewise, Domo saw its share price slashed by more than a third YoY. As the broader market was hit by inflationary pressure and businesses started to rationalize spending, Domo might have been unfortunate to double down on enterprise at the wrong time.

Q4 2023 review

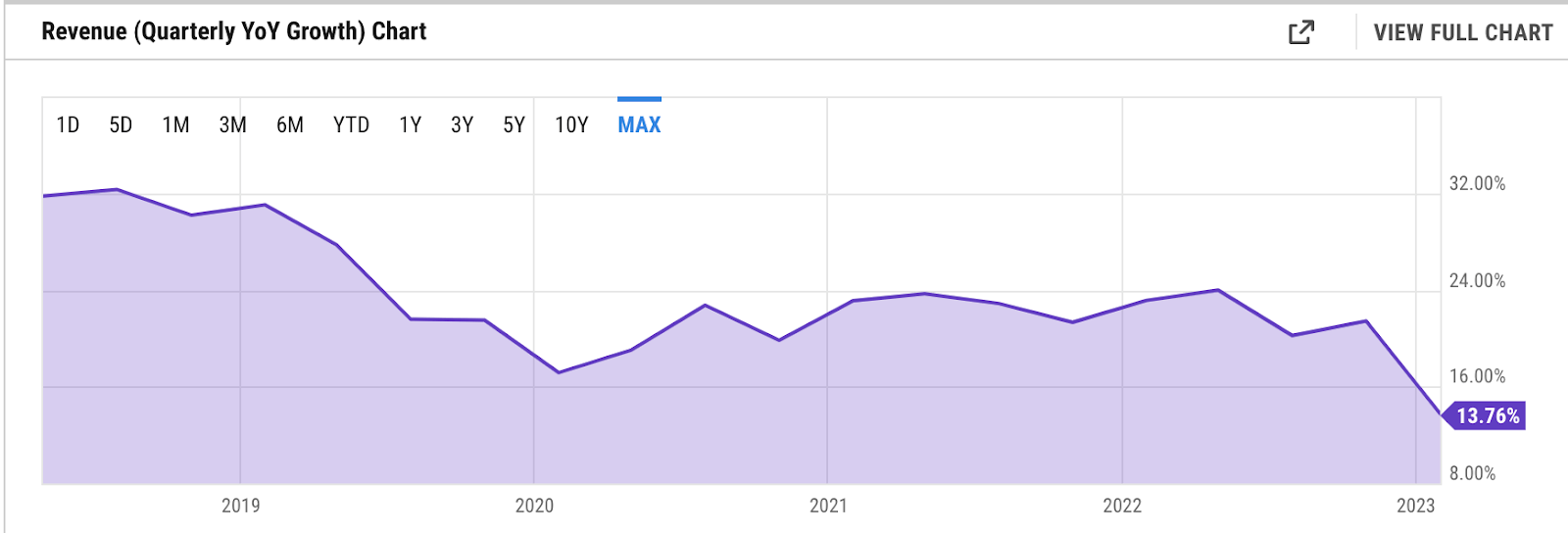

In Q4 2023, Domo beat its guidance by ~2.8% with a revenue of $79.6 million, which was a ~14% YoY growth. This has been Domo's weakest quarterly YoY growth since it went public almost 5 years ago.

{kind=link}

The combination of a tough macro environment and sales productivity issue seems to have taken a toll on the stock. I expect this to continue in Q1 2024 as the company guides a 5% decline in billings, and 4% - 9% growth for the full year.

An area where Domo did well was in profitability. Blended Q4 gross margin was ~76%, the highest seen since IPO. In fact, gross margin has improved consistently every quarter. This was primarily driven by the higher margin from subscription revenue, which was ~85% in Q4. There is a potential margin expansion further when professional service revenue declines as % of revenue with higher upsell and renewal activities.

{kind=link}

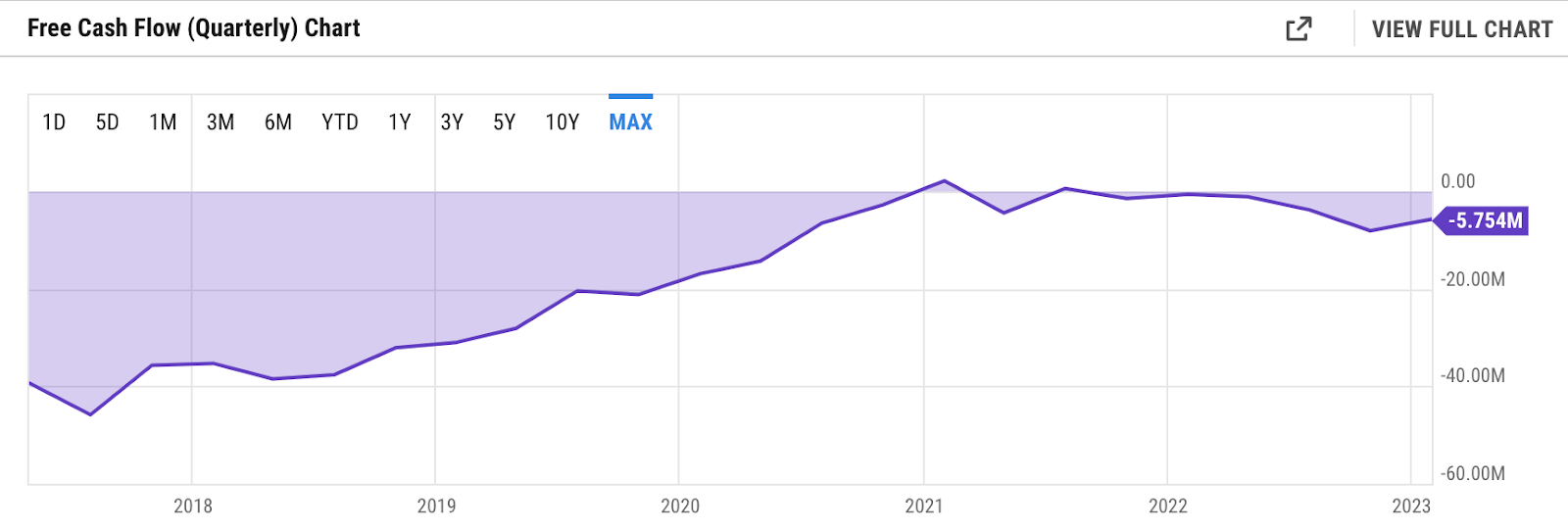

FCF (Free Cash Flow) also improved slightly to -$5.7 million from the previous quarter, despite still being in the red. Domo has been a cash-burning company for most of its lifetime, but the trend has been improving. The last time Domo had a positive-FCF quarter was in July 2021.

BI market landscape review

Product-wise, a typical modern BI technology allows data extraction from various data sources and enables casual business users (non-technical / data users) across the organization to visualize and analyze these data in dynamic dashboards with the purpose of deriving business insights. The tool also has reporting and mobile capabilities.

Within the BI landscape, Domo competes with the likes of Looker/Google ( GOOGL ), Tableau/Salesforce ( CRM ), and Microsoft Power BI ( MSFT ). They all offer relatively similar BI technologies, though are generally differentiated by their perceived value proposition. Domo, for instance, appeals to mid-market customers due to the speed of deployment. Looker, on the other hand, requires the use of its own query language, LookML, to build a semantic layer for data modeling. LookML is simpler than the traditional query language SQL, and makes reusability of the model easier. This makes Looker a unique platform that is attractive for developers, who can end up driving product recommendations.

Gartner

In its annual Magic Quadrant for BI and Analytics software, Gartner considers Microsoft, Salesforce, and Qlik to be market leaders. Their BI products also have dominant presences in the enterprise segment and are generally well-reviewed. Over time, they are taking market shares from legacy BI players such as IBM ( IBM ) or Oracle ( ORCL ), but are also facing challenges from players like Domo, which found more success penetrating the mid-market than the enterprise segment.

From a strategic point of view, players like Domo would aspire to eventually break into the enterprise segment and maintain a sizable share as a co-leader in the quadrant. I think that it would be a desired move, and a reason why I have a long-term bullish view on the stock. However it is also important to consider the time it takes Domo to get there. The recent sales productivity hiccups, for instance, are slowing them down.

Domo already committed a reasonable effort to drive enterprise growth. Enterprise customers make up over 50% of the revenue today , up from ~45% around the time of its IPO . However, over the past few quarters, Domo reported difficulties in closing those deals in a cost-efficient way, especially during the tough macro environment. This soon resulted in sales rep attrition affecting the sales capacity and motivated Domo to instead refocus on its core mid-market (corporate) base for the time being.

Nonetheless, I feel that there is a good chance that Domo will reallocate more investment into revamping its enterprise business in the future. As reiterated by the CEO in the Q4 earnings call , enterprise remains a key growth driver for the company in the long term:

But if you look at a couple of the metrics inside the quarter and inside the year, there's a few things that actually point to enterprise being a real strength.

I think I've seen my customers in terms of the ones that are on multiyear contracts that actually increased this year in a meaningful amount. So, that shows real strength of relationship with your customers. And another thing that -- another metric that really stood out to me as I've been just really pouring through the numbers over the last couple of days is I had almost a 30% increase in the number of companies that have over -- an ARR over $500,000 last year. And I also had almost a 30% increase in the number of companies that are paying us over $1 million a year in ARR.

Product innovation and strategic positioning reviews

Another part where I feel Domo is under a considerable long-term risk is product strategy and innovation. BI landscape has changed over the last 10 - 20 years, and will continue to evolve in the next decade or so. The demand for traditional BI tools that favors vendors like MicroStrategy ( MSTR ), IBM, or Oracle, has shifted towards self-service BI tools that empower non-technical business users to develop visual representation of analytics. The concept puts forward an idea to cut turnaround time for data analysis required to derive valuable business insights by championing technologies that provide a comprehensive set of functionalities that reduce the dependencies on data team, such as cloud-hosted solutions, ETL, data integration, drag-and-drop UI, interactive dashboard, low-code app development environment, and embedded analytics. It has increased the breadth, and most importantly, depth of the BI value chain, especially from a technology and product innovation perspective. Vendors like Domo, Microsoft Power BI, Salesforce Tableau, or Qlik are largely the beneficiaries of this trend.

Since the last few years, the rapid advancement of technologies such as AI has further influenced the evolution of the breadth and depth of BI value chain. One area of AI application in BI, for instance, is in the use of machine learning and natural language processing to help with or even drive automation of insight productions. I have seen a few players specializing or starting to offer the functionalities in that area, such as Thoughtspot or Sisense.

This trend could also be both a threat and an opportunity for Domo, and that depends on how well the company can prevent more firefighting going forward to focus on its strategic positioning to react to this emerging trend. While large cap enterprise-focused players such as Microsoft or Tableau can potentially get away by making strategic acquisitions to bolster AI capabilities, I believe that Domo does not have that luxury.

To establish new capabilities, Domo has mostly been relying on in-house R&Ds. On one hand, it has demonstrated the company's strong commitment for organic growth. But as the value chain gets more complex, it increasingly takes some specialization strategy to outperform competitions in certain BI functions. BI leader Qlik, for instance, has recently announced an intention to acquire Talend , a solution focusing on data integration and management - an integral part of BI value chain - all despite the fact that Qlik has had its own data integration solutions. What is interesting is that Qlik and Talend are both portfolio companies of Thoma Bravo, a PE firm with a strong focus and experience in enterprise software.

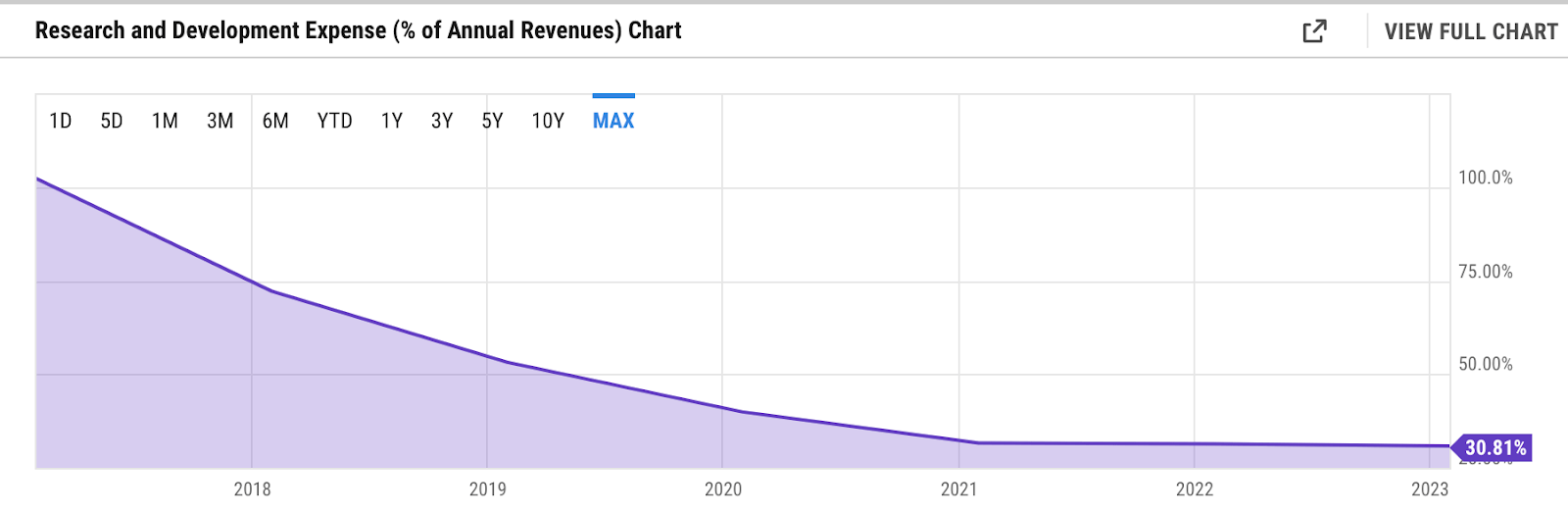

Though Domo's product is generally well-reviewed, I have seen Domo as more of a sales-led software company in recent years. GAAP R&D spend as % of revenue has declined to around 30%-level from over 50% post-IPO.

{kind=link}

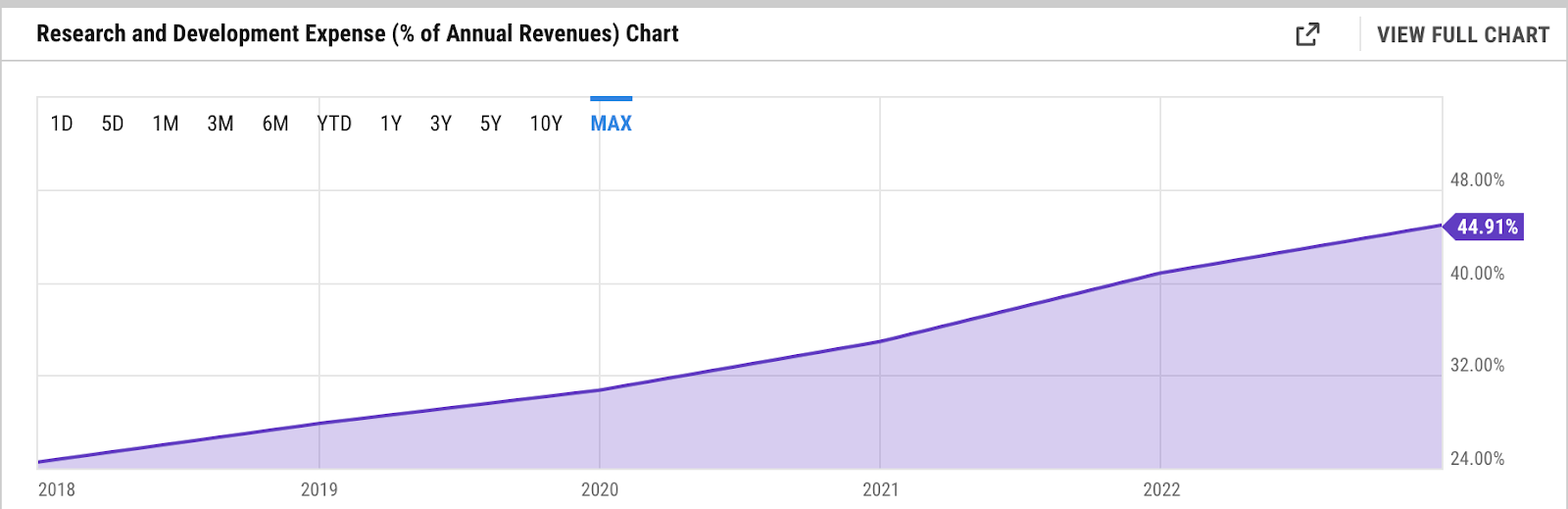

In contrast, the GAAP R&D spend of a product-led cloud software company like Datadog has trended upwards on a % of revenue basis since its IPO. Datadog today spends ~45% of its revenue towards R&D.

{kind=link}

At this point, it seems challenging for Domo to invest more in R&D as the company guides to near-term improvement in profitability. Domo will also have to balance the R&D need with its long-term target expectation. Domo expects non-GAAP R&D spend as % of revenue to drop to 15% in the long-term target. The FY 2022 figure was ~25%.

Valuation

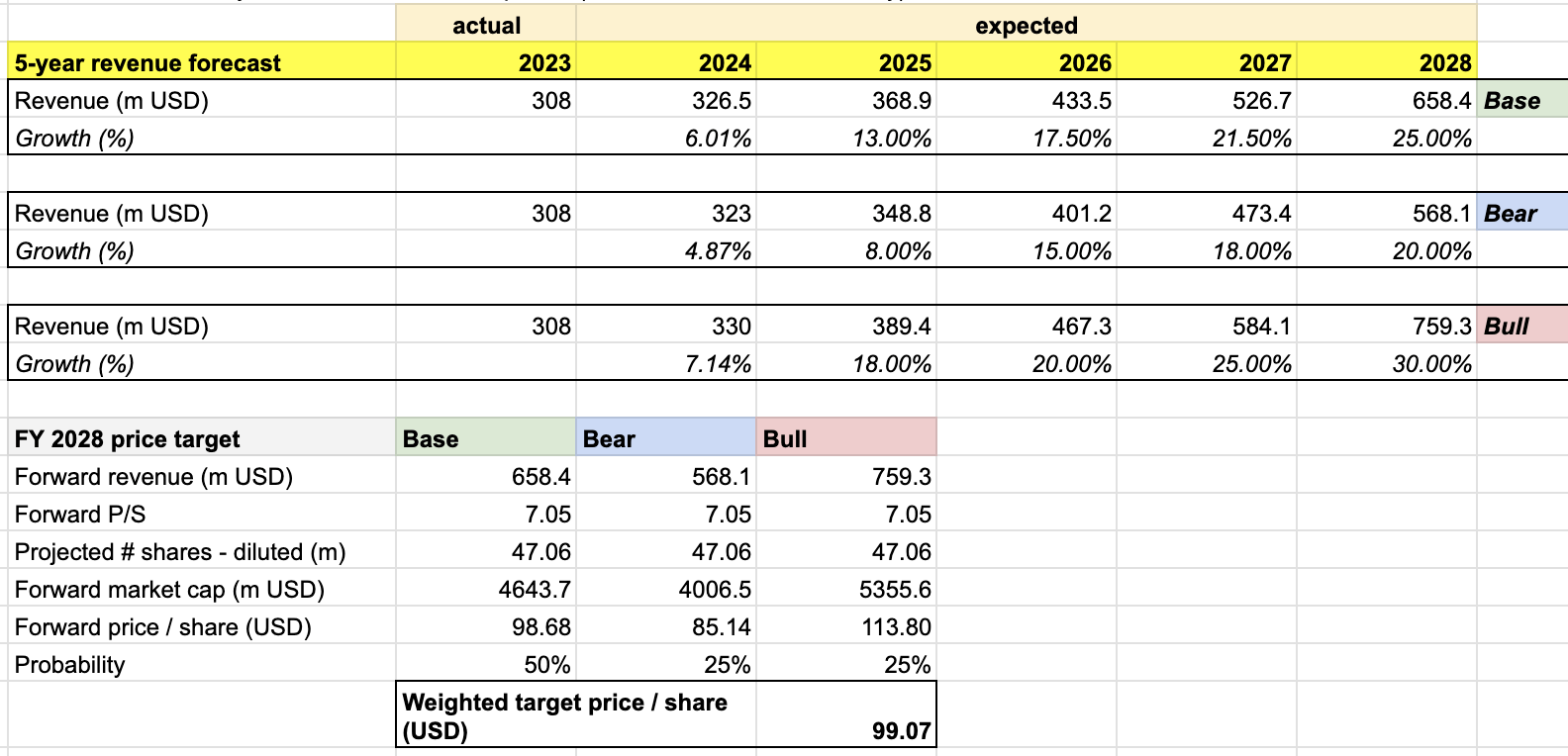

In my model, I ran an exercise to link my growth story to Domo's top-line numbers under 3 different possible scenarios over the next 5 years:

-

Base scenario (decent enterprise successes with minor sales productivity issues): Domo to finish FY 2024 with $326 million of revenue (middle of the guidance), and then reenter double-digit growth in the low to mid-teens the following fiscal year before breaking into 20% in FY 2027, and then 25% growth in FY 2028.

-

Bearish scenario (little success in penetrating enterprise market with occasional sales productivity issues): Domo to finish FY 2024 at the lower end of its guidance with $323 million of revenue, and are only able to finish with a single-digit growth the next year. Domo then finishes the next two fiscal years with mid- to high-teens revenue growth rates, and finally achieves 20% growth at the end FY 2028, lower range of its target model.

-

Bullish scenario (strong enterprise success, no sales productivity issues, and solid strategic/product positioning to capture new trends): Domo to finish FY 2024 at the higher end of its guidance with $330 million of revenue, and straight away reenter 20% range in FY 2026, and accelerate further to 30% at the end of FY 2028, finishing at the upper range of its target model.

Under all scenarios, I expect Domo to finish FY 2028 within the revenue growth range of 20% - 30%, which is consistent with Domo's aspiration in its long-term target model . I also assume that Domo will continue to achieve success with its core customer base (corporate/mid-market).

{kind=link}

I then plugged the FY 2028 number into my target price calculation along with my estimates for the P/S and number of outstanding shares on a diluted basis to arrive at an estimated target price of $99 per share in FY 2028. This figure is ~7% higher than Domo's all-time high of $92 per share in August 2021. Aside from the projected revenue, there are 3 other inputs derived from my assumptions that drove my estimated target price:

-

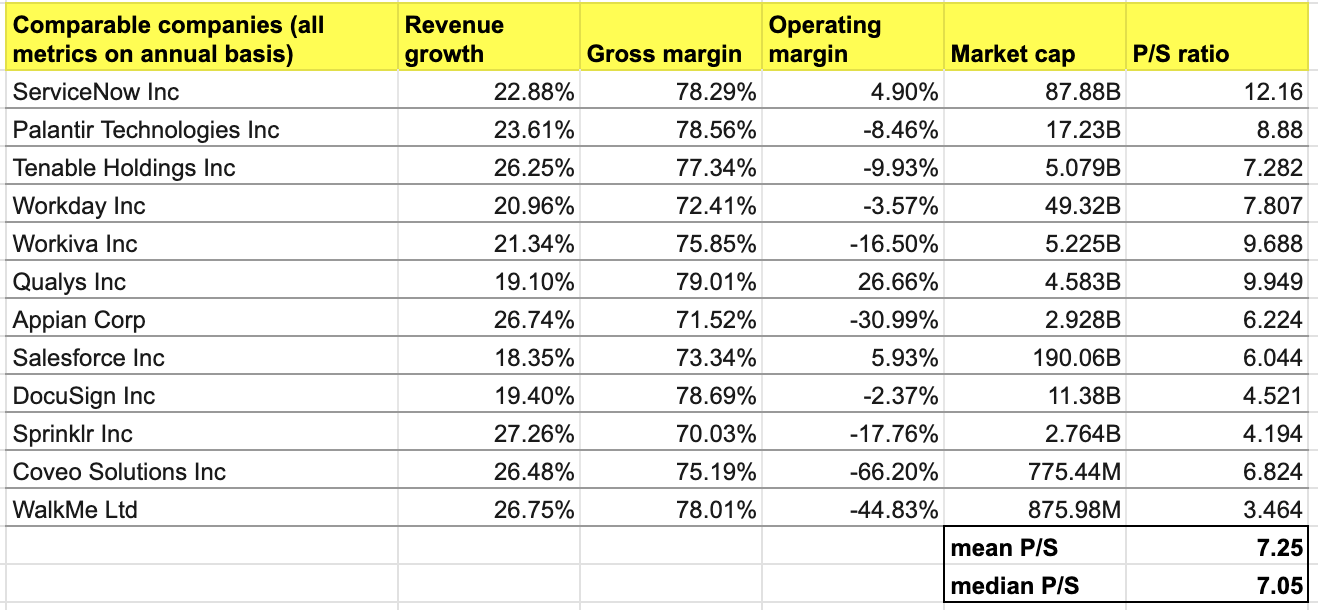

Forward P/S: I used the median P/S of the universe of cloud software stocks of different sizes but with similar revenue growth (20% - 30%) and gross margin (70% - 80%) profiles to Domo's target model.

{kind=link}

-

Projected number of outstanding shares on a diluted basis: I use Domo's guidance of 36.2 million shares in FY 2024 as a baseline, and projected a 30% dilution until FY 2028. The figure is more or less in line with Domo's historical share dilution of ~36% over the past 5 years.

-

Probability: In the end, I assigned a probability value for each base/bull/bear scenario, which I then multiplied by the target price under each case to get the scenario-weighted FY 2028 target price of $99 per share. I assigned the same probability values for both bull and bear scenarios, given my neutral stance on the stock.

Conclusion

Domo is facing a bump in the road. Top-line growth is set to decline to 4% - 7% in FY 2024, highlighting the pressure for the management to steer Domo back to its growth path to align with my thesis. I accordingly adjusted my model and downgraded my bullish call to neutral for the medium term.

Long-term, I maintain my belief that Domo can still be a 20%+ growth stock, supported by the relatively solid mid-market positioning in the BI landscape. Further, my target price of $99 per share in FY 2028 also represents a 7x to 8x upside in 5 years.

Domo may seem undervalued today, but I feel that the stock can also test the all-time-low ($8.3 per share) further on a weak earnings release. my neutral call simply suggests existing shareholders neither add nor cut positions just yet and instead prudently monitor Domo's performances and fundamentals in the next few quarters before making a decision.

For further details see:

Domo: Downgrade On Enterprise Slowdown