DOMO - Domo: Founder Returns And Ready For A Rebound

2023-03-18 00:41:58 ET

Summary

- Domo is data analytics and visualization company, which is classed as a “challenger” by Gartner.

- The company has over 2,200 customers which include major brands such as; Zillow, Loreal, Cisco, Zillow, eBay, DHL, Unilever, the NBA and many more.

- In the fourth quarter of FY23, the company beat both revenue and earnings growth estimates.

- Its founder (Josh James) has returned as the CEO to help get the company back on track.

Domo ( DOMO ) is a data analytics software company that was named as a “challenger” by Gartner. Historically, organizations have struggled with siloed datasets that couldn’t be easily visualized. Domo solves this issue by offering a unified view of all data from multiple sources. Given the “big data” industry is forecast to grow at an 11% compounded annual growth rate up until 2026, the company is poised to benefit from this trend. Domo has already reported a top and bottom line beat for the fourth quarter of the fiscal year of 2023, which is a positive sign. In this post, I’m going to break down its fourth quarter results, before revealing my valuation model and forecasts for DOMO stock. Let’s dive in.

Financial Rebound?

Domo reported solid financial results for the fourth quarter of FY 2023. Its revenue was $79.62 million which beat analyst forecasts by $2.15 million and increased by ~14% year over year.

Domo was previously categorized as a “high growth” business and achieved growth rates of between 20% and 40%, between the years of 2018 and 2021. In order to help get the company back on track, its founder (Josh James) has been reappointed as the CEO.

The beautiful thing about Domo’s business is it makes the majority (88%) of its revenue from subscription services, which adds some consistency to the top line. Its subscription revenue expanded by 18% year over year to $70.3 million, which was positive. The only negative really was a 3% decline in billings to $104.5 million. These metrics look to have been slightly impacted by the macroeconomic environment which has caused longer sales cycles.

A positive is its current RPO or Remaining Performance Obligations increased by 10% year over year to $234.8 million. In addition, its total RPO increased by 12% year over year to $378.2 million. Generally, when we see faster ARR growth than RPO, that can indicate the signing of multi-year contracts, which management confirmed on the earnings call.

In fact, Domo reported a staggering 65% of its customers are in multi-year contracts, up from 62% in the prior year. The signing of multi-year contracts is an extremely positive sign given the tough economic backdrop.

Its gross retention rate did dip by 1% year over year to 89%, but its net retention rate was still over 100%, which was positive, as it means the majority of customers are sticking with the product on an equivalent spend basis.

Margins and Balance Sheet

Moving onto profitability, the company reported earnings per share [EPS] of negative $0.57, which beat analyst forecasts by $0.03. This was driven by operating income improvement from a loss of $30.1 million in Q4 FY22 to a loss of $16.2 million by Q4 FY23. The beautiful thing about a software company is it inherently has high operating leverage built into its business model. The company has a strong balance sheet with $66.5 million in cash and cash equivalents. The company has fairly high total debt of $128.8 million but the majority $108.6 million is long-term debt.

Valuation and Forecasts

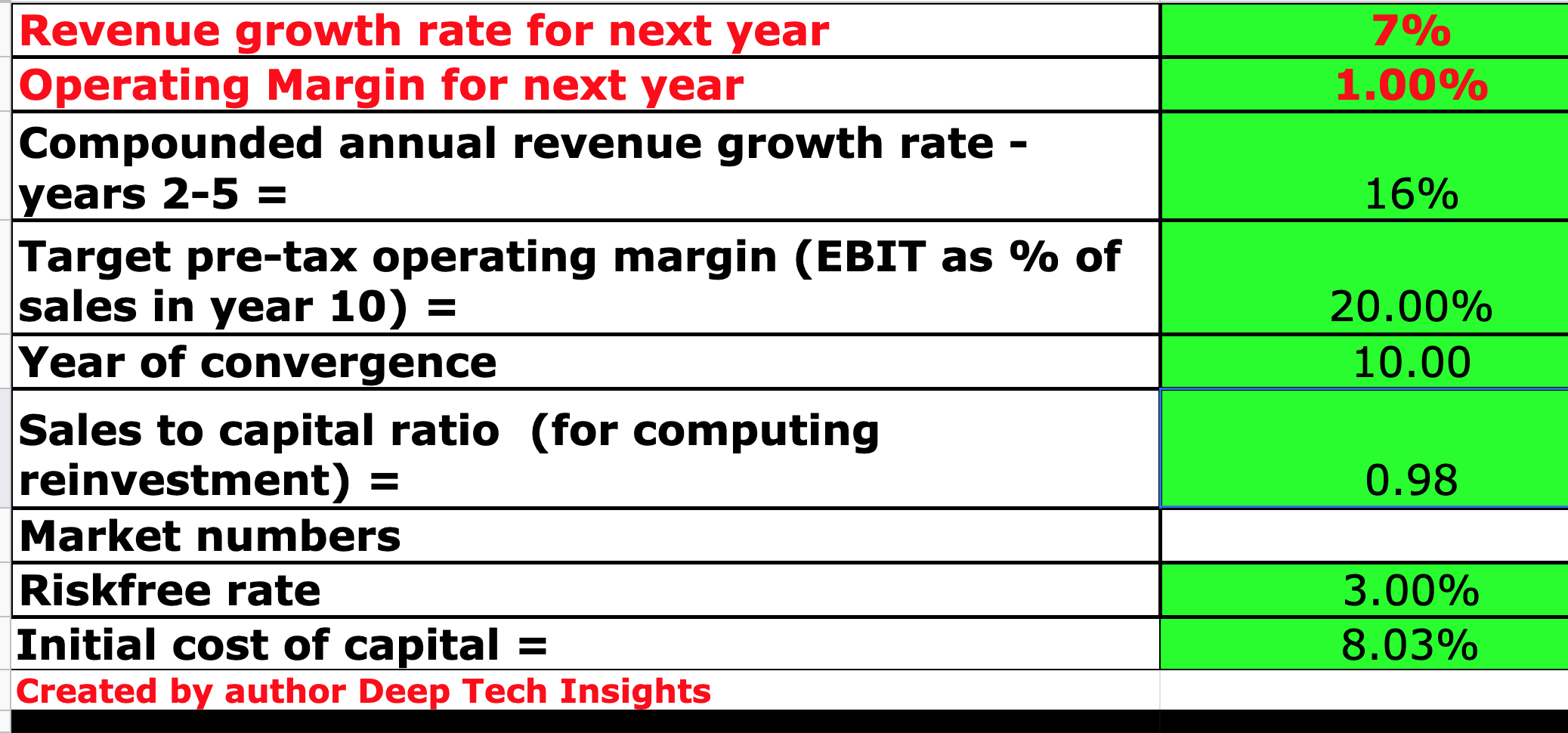

In order to value Domo, I have plugged its latest financial data into my discounted cash flow valuation model. I have forecast 6% revenue growth for “next year” or FY24 in my model. This is based upon management's conservative forecast of between 5% and 7% revenue growth or between $323 million and $330 million for the full year. Keep in mind, this is substantially lower than the 14% revenue growth achieved in Q4FY23, year over year. In years 2 to 5, I have forecast slightly higher than this growth rate with 16% per year forecast. I expect this to be driven by improved macroeconomic conditions, as well as management changes and realignment.

Domo stock valuation 1 (Created by author Deep Tech Insights)

{kind=link}

To increase the accuracy of my model, I have capitalized R&D expenses which has boosted net income. I have forecast a 1% operating margin for “next year” or FY24. This is based upon management's forecast of a “slightly positive” operating margin for the full year. Over the next 10 years, I have forecast operating expansion growth to 20%, which is below the 23% average of companies in the software industry.

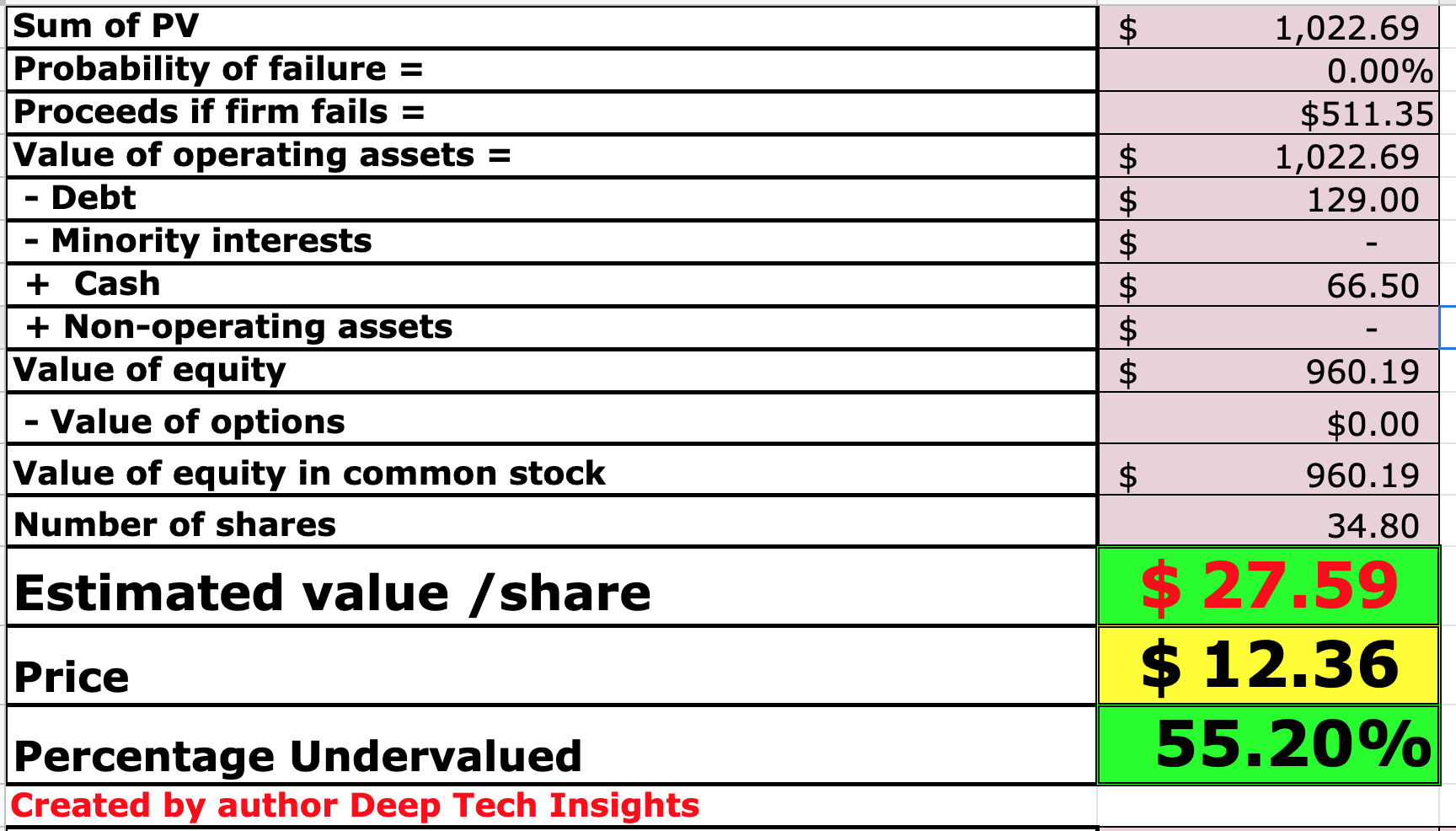

Domo stock valuation 2 (created by author Ben at Motivation 2 Invest)

{kind=link}

Given these factors, I get a fair value of ~$28 per share, the stock is trading at ~$12 per share at the time of writing, thus it is over 55% undervalued.

As an extra data point, Domo trades at a price-to-sales [P/S] ratio = 1.237, which is over 71% cheaper than its 5-year average.

Risks

Cash Burn/Share Solution

If we theoretically forecast that the business continues to make the same loss of $16.2 million in Q4 '22 moving forward, we can estimate when its cash on the balance sheet would run out. In this case, if we do $66.5 million divided by $16.2 million, the company has just over 4 quarters or one year's worth of cash left at its current burn rate. After which the company may have to issue more shares, which would dilute shareholders or take on more debt. This is a risk with the business; however, a positive is management has forecast a slightly positive operating margin for the full year of FY24.

Final Thoughts

Domo is a leading data analytics company that is poised to benefit from the growth in “big data” and the cloud. The business has faced a number of challenges from the macroeconomic environment which has caused slowing growth in the business. A positive is Domo reported a strong quarter, beating top and bottom-line growth estimates. In addition, the return of its founder as CEO should help to set a new trajectory for the company. Given my valuation model and forecasts indicate the stock is undervalued intrinsically at the time of writing, it could be a great long-term investment.

For further details see:

Domo: Founder Returns And Ready For A Rebound