DOMO - Domo: Irreversible Losses

2023-09-25 23:41:47 ET

Summary

- Domo, an enterprise technology company, has seen its BI product's growth grind to a halt, causing its shares to slip over 30% this year.

- The company's recent guidance cut and slower billings growth rates indicate a worsening situation, making recovery unlikely.

- Domo faces a challenging competitive landscape in the business intelligence software market and has limited resources, which may lead to trouble down the line.

It has been an exceedingly tough year for enterprise technology companies, but generally speaking, it has been better to be a large player than to be a smaller one in this climate. Domo ( DOMO ) is finding this out the hard way this year, as its BI product - already a lightning rod for competition among both large and small vendors - saw growth grind to a halt.

Year to date, shares of Domo have slipped more than 30%, even as most other tech peers remain up double-digits for the year. In my view, investors should resist the temptation to catch a falling knife: there's very little hope for recovery here.

A bad situation is only getting worse

I last wrote a bearish opinion on Domo in July, when the stock was trading closer to $16. Since then, the stock has crashed by more than 40%, on the back of a recent guidance cut. In light of all this, I remain quite bearish on the name.

{kind=link}

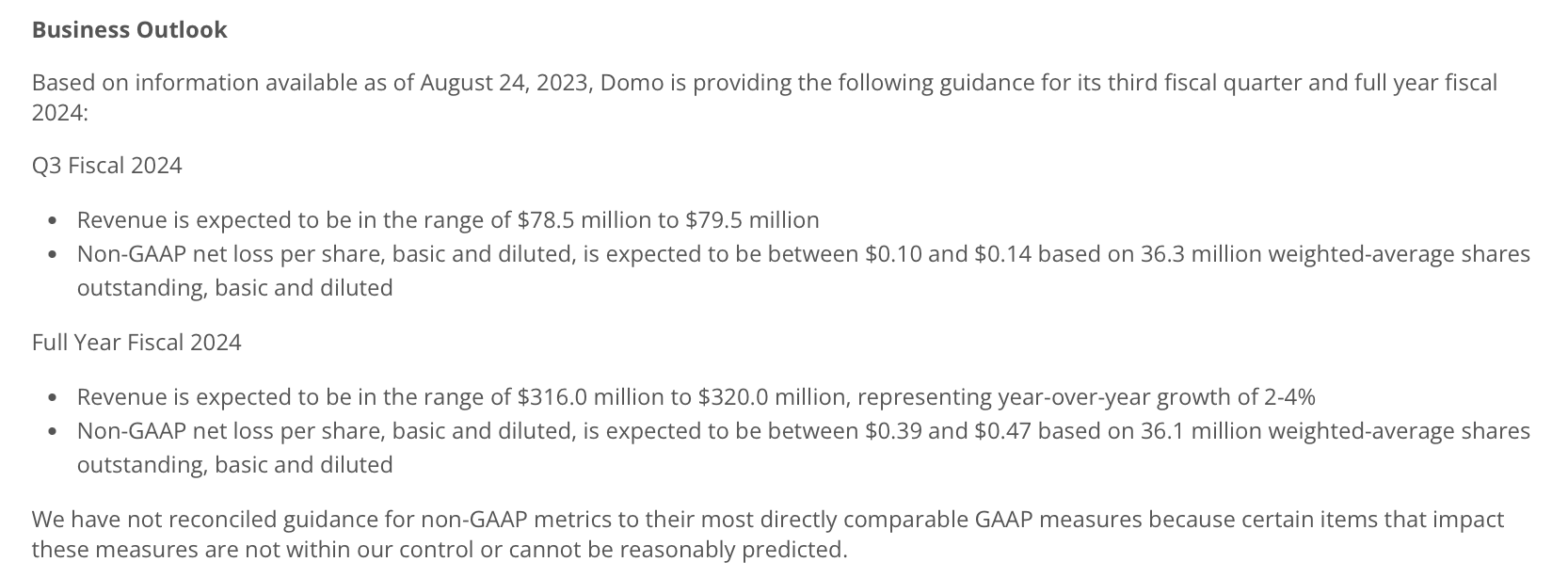

As can be seen in the snapshot above, Domo is now guiding to just $316-$320 million in revenue, or 2-4% y/y growth: or about half the growth at the midpoint versus a prior outlook that called for 4-6% y/y growth. And while many enterprise software companies have cited tougher sales cycles and deal scrutiny, many have at least managed to retain their conservative guidance outlooks and in many cases still raise them: Domo's guidance cut is an anomaly in the industry.

As a reminder, here are what I view as the longer-term risks for Domo:

- Dramatically slower billings growth rates. BI is a "nice to have," but not a "must have." In this environment, where IT budgets are being cut, Domo implementations and deal closings are likely to get delayed, and in this time of weakness, larger players like Tableau/Salesforce ( CRM ) and Microsoft Power BI ( MSFT ), which are packaged as part of other "mission critical" software products, may prevail.

- Incredibly challenging competitive landscape. And unfortunately, business intelligence software is among the most crowded arenas of enterprise software. At one time, many companies were still new to BI and choosing among vendors in a relatively greenfield landscape, but now the major players like Tableau or Microsoft Power BI are already very commonly installed.

- Though free cash flow positive, Domo has limited resources with less than $100 million of balance sheet cash. An unexpected downturn in new deals or a sharp decline in renewals may put Domo into a pinch if it is forced to raise additional capital. Equity capital will be dilutive for Domo in this market as its stock sits well below pandemic-era highs, and debt capital will come at a huge interest cost that Domo may not be able to handle.

Valuation check

Of course, with Domo's recent crash, the company has become tremendously cheap. At current share prices just under $10, Domo's market cap sits at $345.5 million. After we net off the $66.5 million of cash and $108.6 million of debt on Domo's most recent balance sheet, its resulting enterprise value is $387.6 million.

For next year FY25 (the fiscal year for Domo ending in January 2025), Wall Street analysts are expecting Domo to generate $322.7 million in revenue, or just 2% y/y growth - consensus is effectively not calling for a near-term rebound either.

This puts Domo's valuation at 1.2x EV/FY25 revenue - among the cheapest multiples in the enterprise software sector.

The main reason I bring up valuation is that the only upside risk I see for Domo is an acquisition scenario in which a large enterprise player scoops up Domo for a premium to nab its customer base. This being said, Domo has been a cheap and attainable target for quite a while - so it's difficult to bank on a potential takeover exit when Domo has been on the proverbial chopping block for so long.

Q2 download: growth ailments have no remedy

Let's now discuss the core issues that surfaced with Domo's most recent quarterly results. The Q2 earnings summary is shown below:

{kind=link}

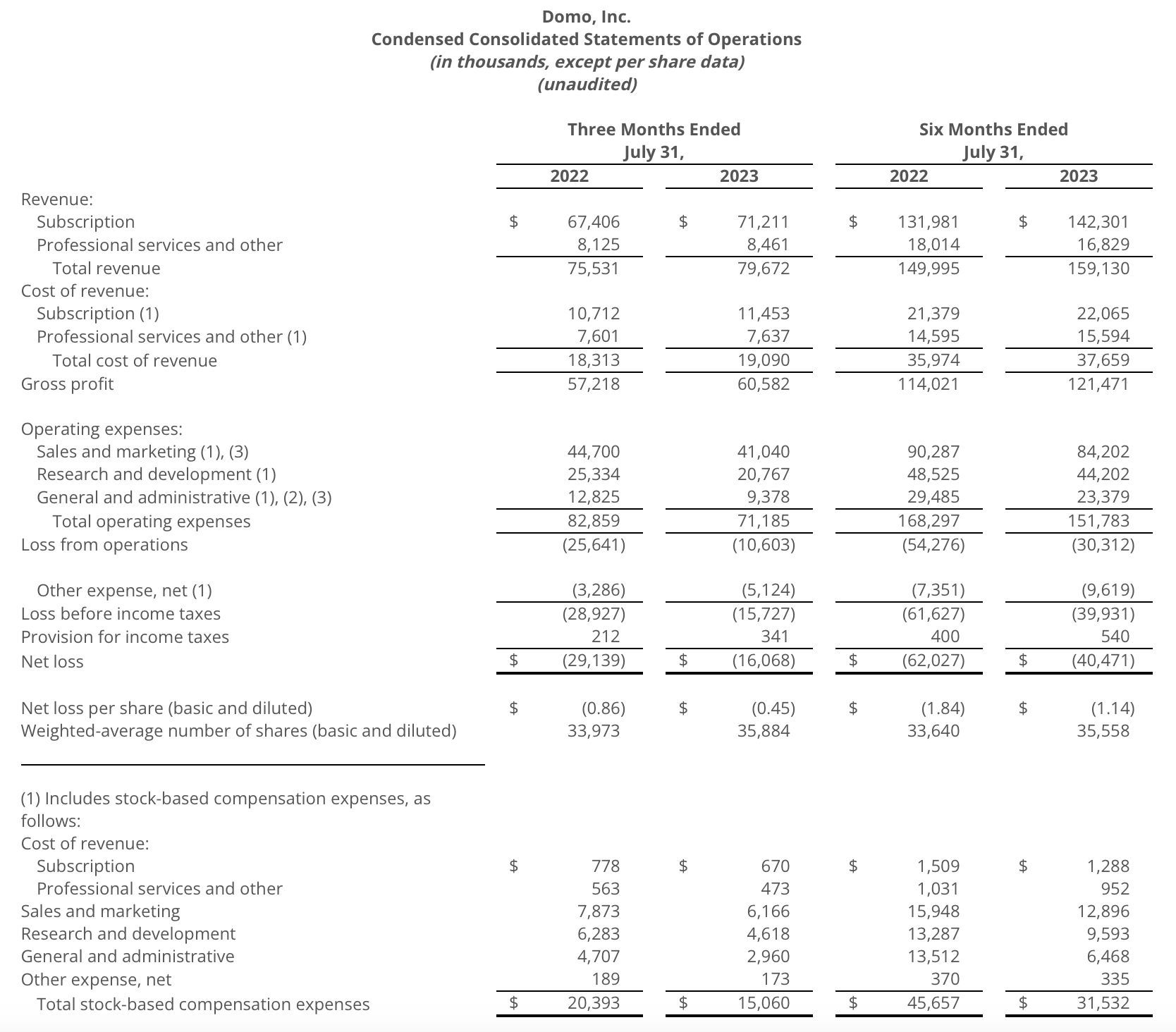

Revenue grew just 5% y/y to $75.5 million, essentially in line with Street expectations of $74.8 million but decelerating two points versus Q1's already slim 7% y/y growth rate.

Of course, we knew that growth was on the wane because billings started to slip negatively last quarter; and in Q2 again, billings declined by -2% y/y to $70.6 million. We should also note that it's not just the y/y declines in billings that are concerning, but the fact that nominal billings dollars are lower than revenue means that Domo is recognizing revenue faster than it's signing new deals , drawing down its deferred revenue balances - one of the key leading indicators for a flailing software company.

The core issue here is a macro concern - but one that may have long-lasting impacts. Domo faces competition from many software vendors that have much more sprawling product portfolios: such as Microsoft, Salesforce, Oracle (ORCL), and SAP (SAP). Customers of these companies have other products that are more difficult to shed than BI, so it's easier to consolidate a company's software stack into one of these portfolio vendors than to pay a separate fee for Domo if the aim is expense consolidation and reduction.

One of Domo's main answers to this issue is to pivot toward usage-based pricing. It's banking on the hope that if some customers churn, the customers that stay behind might be incentivized to use Domo more and pay for the privilege, helping Domo to make up for lost ground. Per CEO Josh James' remarks on the Q2 earnings call :

Second, I believe our increased focus on consumption-based pricing can be a growth driver and create stronger relationships with our customers as we've removed the limitation on number of seats in an account by granting access to all employees of a customer and only charging for data usage similar to Snowflake, AWS and others.

Because we can charge for usage while offering seat licenses and visualization for free, consumption pricing solves many of our historic barriers to adoption and more directly aligns our pricing to the value realized by our customers. Thanks to this, consumption pricing is opening more doors for upsell opportunities."

The company notes that 50% of its new logo wins in Q2 were consumption-based deals, up from 30% in Q1 (and it's targeting 75% in Q3 and beyond). We have not yet seen, however, this change in pricing strategy translate to growth upside yet.

The one saving grace is that Domo is focused on cost savings during its time of growth challenges. The company generated a $4.5 million pro forma operating income (a 7% margin) in Q2, versus a loss of roughly equivalent magnitude in the year-ago Q2. We should be careful, however, as low growth provides for very limited opportunities for Domo to continue expanding its bottom line.

Key takeaways

In my view, Domo's challenges will be very difficult to surmount, and from an investor's perspective, the only exit path would be a low-probability acquisition. Fundamentally, I believe the company will continue to face heightened churn and increasing competitive pressure - it's better to stay on the sidelines and invest elsewhere.

For further details see:

Domo: Irreversible Losses