DOMO - Domo Loses Large Customers Amid Industry Competitive Pressures

2023-09-22 14:30:14 ET

Summary

- Domo, Inc. provides business intelligence and data visualization software.

- The global market for business intelligence software and services is expected to grow, driven by increasing demand for data processing and analysis.

- Domo's financial trends show plateauing revenue, decreasing expenses, and negative earnings per share.

- With large customer losses, lengthening sales cycles, and increasing competitive pressure, my outlook on Domo, Inc. is to Sell.

A Quick Take On Domo

Domo ( DOMO ) provides business intelligence and data visualization software that digitally connects different parts of the enterprise.

The firm is experiencing large customer churn and longer sales cycles.

Given increasing client hesitancy, recent customer losses and the ability of larger competitors to bundle similar types of services, I’m not optimistic about Domo, Inc.

My outlook on DOMO is to Sell.

Domo Overview And Market

American Fork, Utah-based business intelligence firm Domo was founded in 2010 to help businesses optimize their operations by combining data, people and expertise to improve business results.

The firm is led by Founder and CEO Josh James, who was previously the Founder and CEO of Omniture, a company he also took public.

Domo has developed a suite of software products to fix fundamental problems that plague traditional business intelligence markets.

The company's offerings include:

- Data integration - connect to over 1,000 pre-built data sources

- Data visualization - drag-and-drop visualization tools

- Data collaboration - share data and insights with others in the organization

- AI-powered insights - artificial intelligence to help identify business patterns and trends

According to a 2023 market research report by Mordor Intelligence, the global market for business intelligence software and services was estimated at $26.8 billion in 2023 and is forecasted to reach $42.5 billion in 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of 9.65% from 2023 to 2028.

The main drivers for this expected growth are an increasing demand from businesses to process increasing amounts of data in shorter time periods to make better decisions faster.

Also, the BFSI (Banking, Financial Services and Insurance) industry is expected to drive the highest demand for business intelligence software and services through 2028.

Domo’s Recent Financial Trends

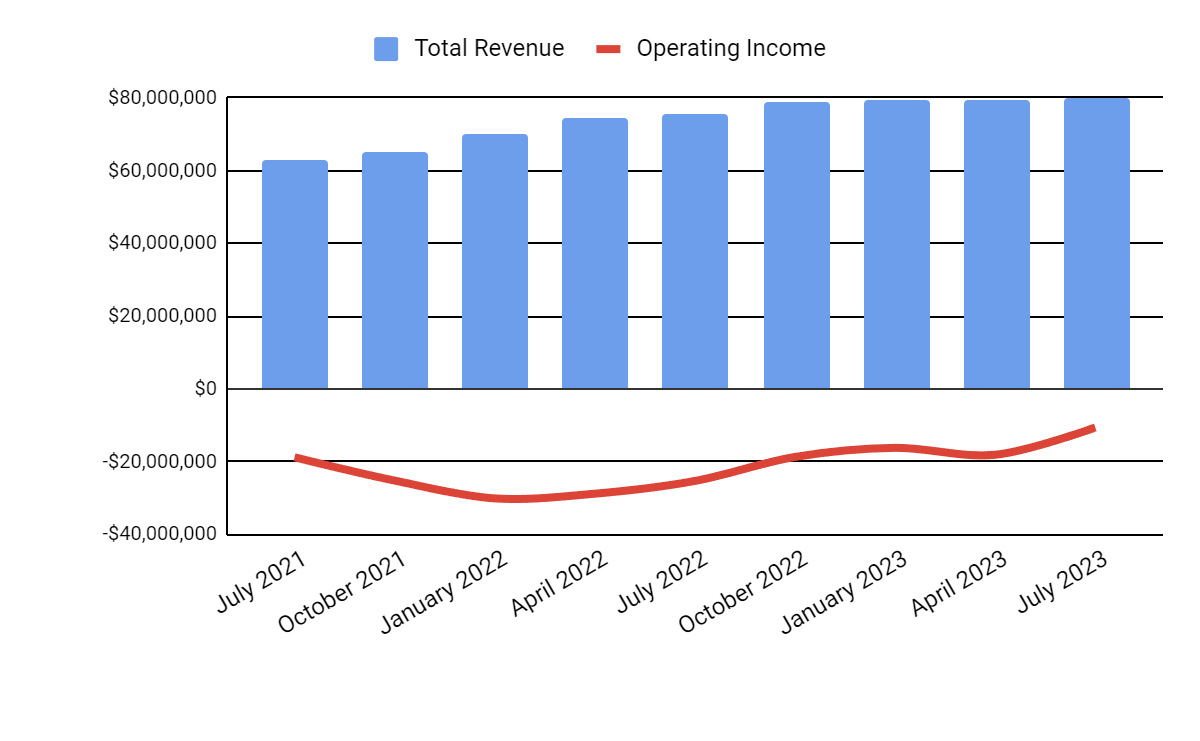

- Total revenue by quarter has begun to plateau; Operating losses by quarter have lessened in recent quarters:

Total Revenue and Operating Income (Seeking Alpha)

{kind=link}

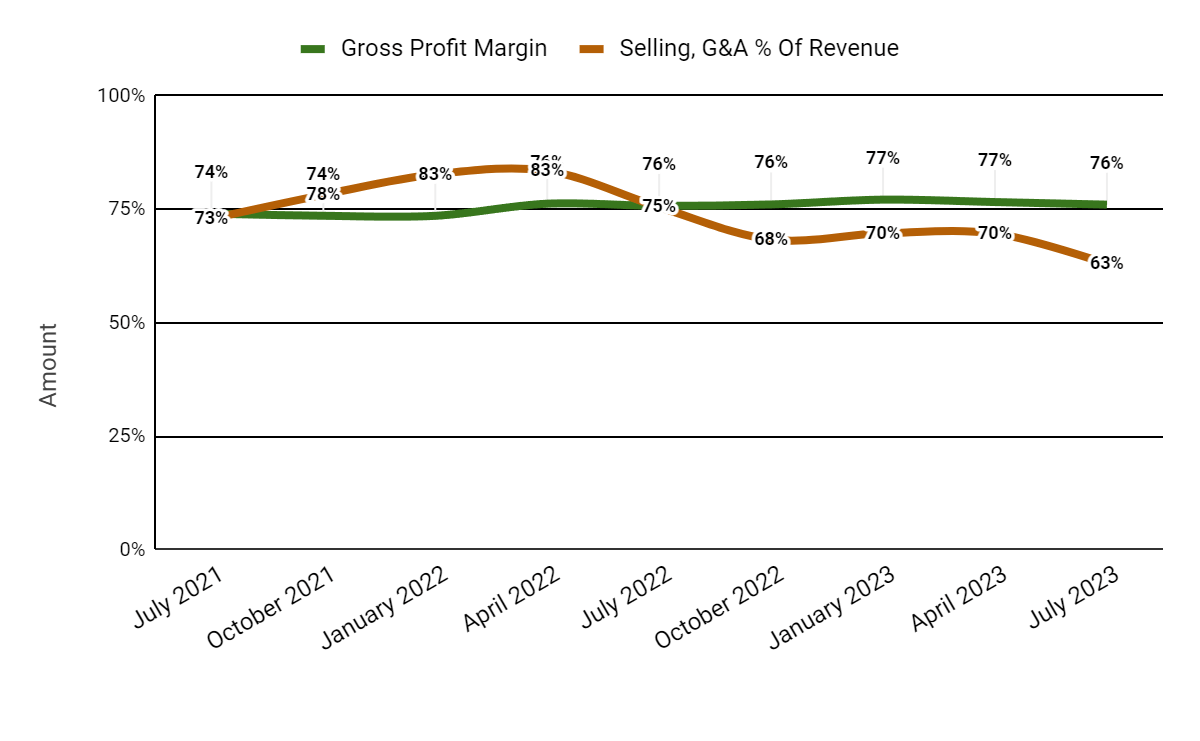

- Gross profit margin by quarter has trended slightly higher in recent quarter; Selling and G&A expenses as a percentage of total revenue by quarter have dropped sharply more recently:

Gross Profit Margin and SG&A % Of Revenue (Seeking Alpha)

{kind=link}

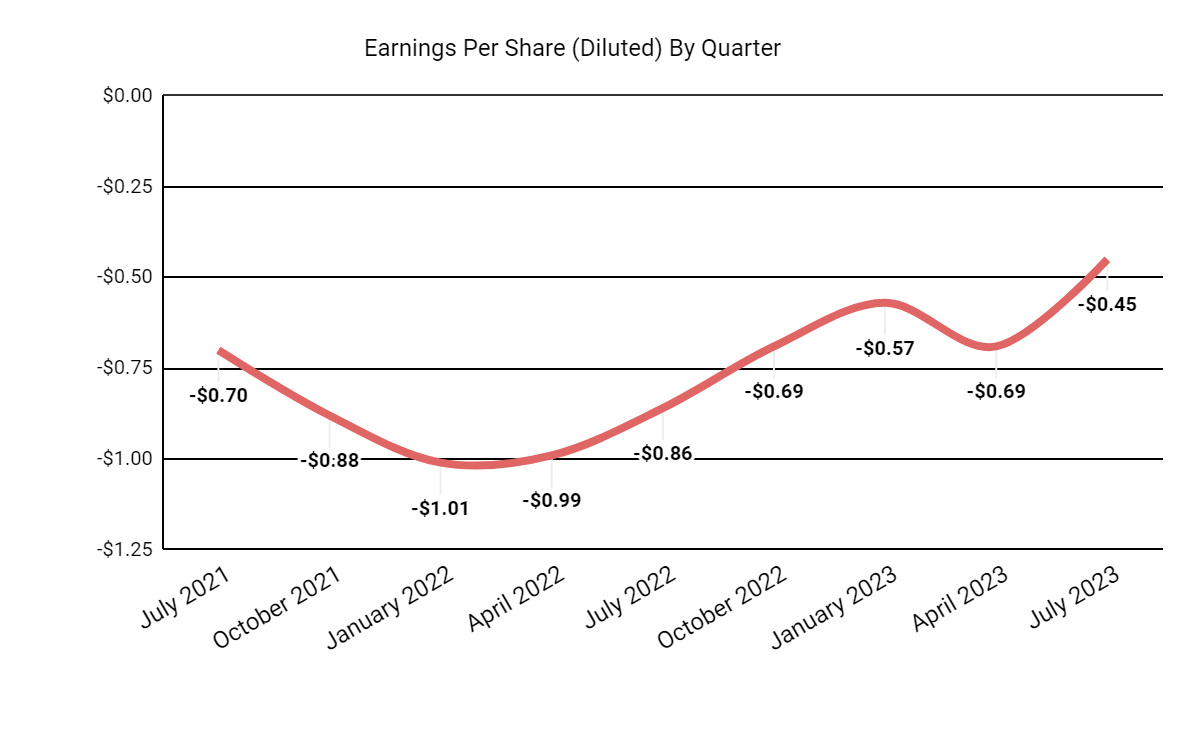

- Earnings per share (Diluted) have remained heavily negative but have made a significant move toward breakeven as SG&A expenses have decreased, although still far away from it.

Earnings Per Share (Seeking Alpha)

{kind=link}

(All data in the above charts is GAAP.)

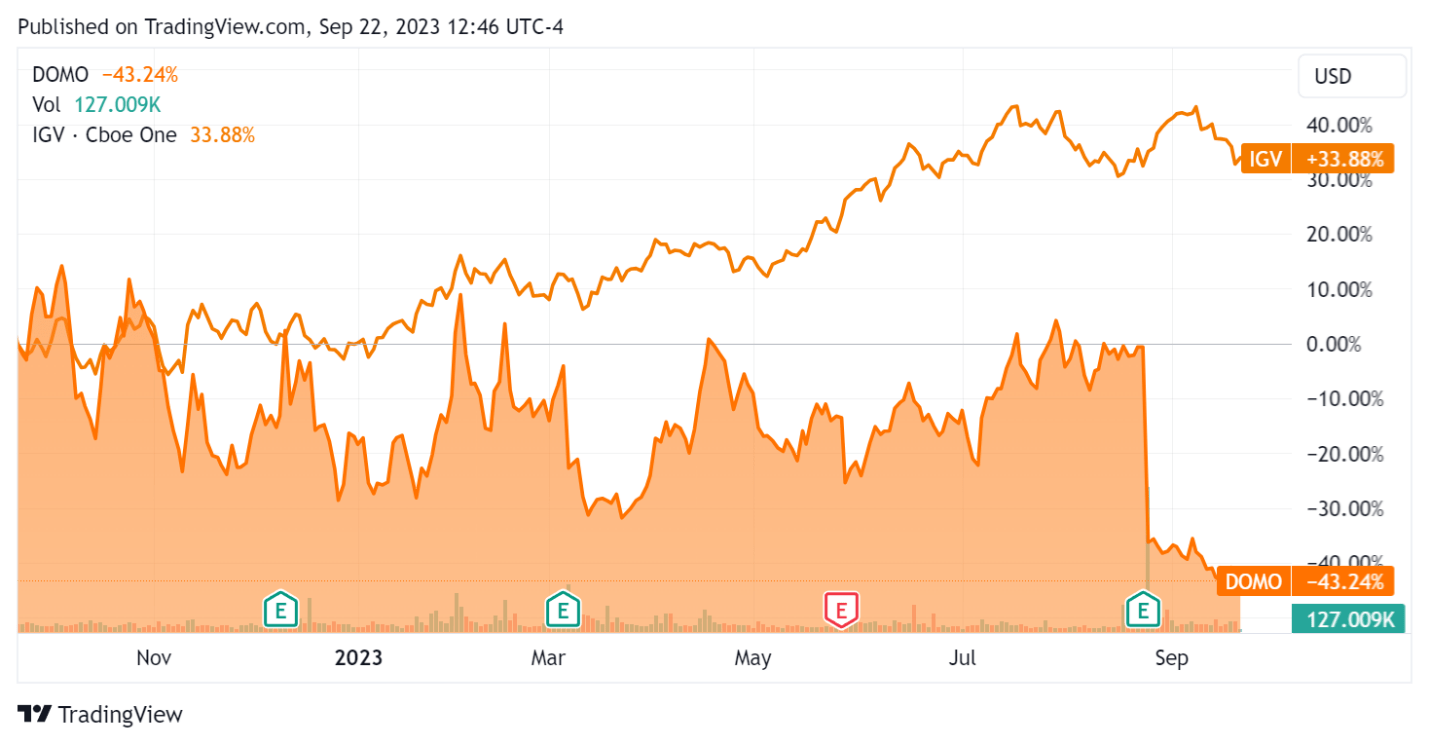

In the past 12 months, DOMO’s stock price has fallen 43.24% vs. that of the iShares Expanded Technology-Software ETF’s (IGV) rise of 33.88%:

52-Week Stock Price Comparison (Seeking Alpha)

{kind=link}

For balance sheet results, the firm ended the quarter with $60.2 million in cash and equivalents and $111.0 million in total debt, all of which was long-term.

Over the trailing twelve months, free cash used was ($19.0 million), during which capital expenditures were $11.1 million. The company paid a hefty $69.7 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Domo

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 1.4 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 1.1 |

| Revenue Growth Rate |

| 11.5% |

| Net Income Margin |

| -26.4% |

| EBITDA % |

| -20.0% |

| Market Capitalization |

| $366,240,000 |

| Enterprise Value |

| $435,310,000 |

| Operating Cash Flow |

| -$7,850,000 |

| Earnings Per Share (Fully Diluted) |

| -$2.40 |

(Source - Seeking Alpha.)

DOMO’s most recent unadjusted Rule of 40 calculation was negative (8.5%) as of FQ2 2024’s results, so the firm has performed poorly in this regard, per the table below:

| Rule of 40 Performance (Unadjusted) |

| FQ2 2024 |

| Revenue Growth % |

| 11.5% |

| EBITDA % |

| -20.0% |

| Total |

| -8.5% |

(Source - Seeking Alpha.)

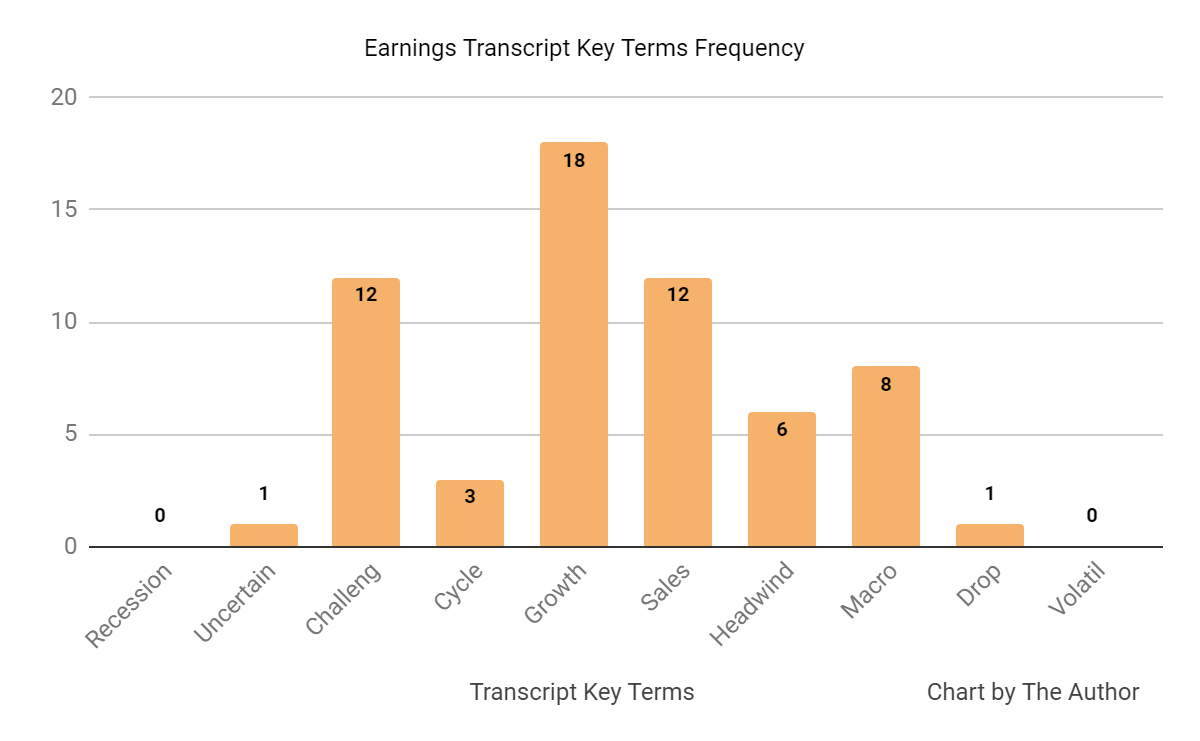

Sentiment Analysis

I prepared a chart showing the frequency of various words in the firm’s recent earnings conference call:

Earnings Transcript Key Terms Frequency (Seeking Alph)

{kind=link}

The chart indicates significant stress the company is facing in a very "challenging" "macro" environment, with lengthening sale cycles reducing its revenue growth potential.

Analysts questioned management about its lowered forecast from large customer non-renewals.

Leadership said some were worried about vendor consolidation, but that only 5 - 6 customers out of 50 large firms were at risk in the near term.

Commentary On Domo

In its last earnings call (Source - Seeking Alpha ), covering FQ2 2024’s results, management’s prepared remarks included a reference to a return to growth taking longer than anticipated due to commonly cited macroeconomic conditions.

The firm is also increasingly focused on a consumption-based revenue model. As a result, management believes this model is "opening more doors for upsell opportunities."

Also, in the past twelve months, there has been a 30% increase in contract size for new customers using a consumption-based pricing model versus the previous seat-based model.

The net retention rate was just below 100%, a reduction from Q1 and a result of difficulty in upselling additional revenue-generating software and services.

Total revenue for Q2 2023 rose by 5.6% year-over-year, and gross profit margin increased by 0.3%.

Selling and G&A expenses as a percentage of revenue dropped an impressive 12.5%, and operating losses were reduced by 58.1%, $10.6 million for the quarter.

The company's financial position is moderate, with some liquidity and a trailing twelve-month use of cash of $19 million.

DOMO’s Rule of 40 performance has been poor, with operating losses dragging down its performance here.

Looking ahead, consensus revenue estimates for 2023 suggest a potential growth rate of 2.9% versus 2022’s growth rate of 19.6% over 2021.

So, growth will likely be sharply lower than the previous year.

In the past twelve months, the firm's EV/Sales valuation multiple has dropped by 40%, as the chart from Seeking Alpha shows below:

EV/Sales Multiple History (Seeking Alpha)

{kind=link}

A potential upside catalyst to the stock could include improved revenue growth from lower sales team attrition.

However, given longer sales cycles from client hesitancy, recent customer losses and the ability for larger competitors to bundle similar types of services with their other offerings, producing continued competitive pressures, I’m not optimistic on DOMO.

My outlook on DOMO is to Sell.

For further details see:

Domo Loses Large Customers Amid Industry Competitive Pressures