DOMO - Domo: No Rescue In Sight

2023-12-04 18:02:33 ET

Summary

- Domo's stock has lost 30% of its value this year and is expected to face further decline.

- The company's poor Q3 results indicate continued deceleration in revenue growth and negative cash flow.

- Domo's move to a consumption-based business model may not be enough to compete with larger software suites offered by competitors.

Amid substantial rallies for most of the tech sector in the hopes of lower interest rates, Domo ( DOMO ) remains a rare holdout. This BI software company has long lagged its tech peers in the markets since the pandemic began, but this isn't just poor sentiment at play: the company has struggled fundamentally as larger competitors encroach on its market.

Year to date, shares of Domo have lost ~30% of their value; in my view, there's further pain to go.

I last wrote a bearish article on Domo in September, when the stock was trading closer to $9 per share. Since then, the company has released poor Q3 results that showcased continued deceleration in revenue growth, amid negative cash flow that is constraining a cash-poor balance sheet. In light of this, and considering the fact that Domo stock has edged back up somewhat over the past month, I am reiterating my bearish opinion on this name.

Domo's biggest plan to save itself revolves around moving to a consumption-based business model. This involves rolling out a freemium version of its product and charging users on a usage basis (SaaS companies that price products similarly include Snowflake ( SNOW ), Twilio ( TWLO ), and Datadog ( DDOG )).

Yet in my view, the underlying issue for Domo can't be fixed by changing how it bills customers. Domo is losing because its competitors are part of much larger software suites: Microsoft PowerBI ( MSFT ) is natively connected across the Microsoft ecosystem; ditto for Tableau, which was acquired by Salesforce. When so much of data visualization relies on connections to various data streams, what competitive advantage does Domo present?

As a reminder for investors who are newer to this name, here are all the core risk factors I see in Domo:

- Dramatically slower billings growth rates- BI is a "nice to have," but not a "must have." In this environment, where IT budgets are being cut, Domo implementations and deal closings are likely to get delayed, and in this time of weakness, larger players like Tableau/Salesforce and Microsoft Power BI, which are packaged as part of other "mission critical" software products, may prevail.

- Incredibly challenging competitive landscape- Unfortunately, business intelligence software is among the most crowded arenas of enterprise software. At one time, many companies were still new to BI and choosing among vendors in a relatively greenfield landscape, but now the major players like Tableau or Microsoft Power BI are already very commonly installed.

- Software companies that can't grow also can't become profitable. Cost cuts can only do so much; but Domo's lack of top-line growth will rob it of the economies of scale it needs to hit profitability.

- Domo has limited liquidity and more debt than cash. An unexpected downturn in new deals or a sharp decline in renewals may put Domo into a pinch if it is forced to raise additional capital. Equity capital will be dilutive for Domo in this market as its stock sits well below pandemic-era highs, and debt capital will come at a huge interest cost that Domo may not be able to handle.

From a valuation standpoint, Domo of course remains quite cheap - which would be the only reason to consider investing in the stock. At current share prices just under $10, Domo trades at a market cap of $360.3 million. After we net off the $66.5 million of cash and $108.6 million of debt off Domo's most recent balance sheet, the company's resulting enterprise value is $402.4 million.

Meanwhile, for next fiscal year FY25 (the fiscal year for Domo ending in January 2025), Wall Street analysts are expecting the company to generate $323.8 million in revenue, representing just 2% y/y growth (data from Yahoo Finance ). Even this may be aggressive, as it represents acceleration from current-quarter revenue and billings growth rates; and it essentially banks on the hope that the switch to a consumption-based model will ultimately be successful. Nevertheless, taking consensus estimates at face value, we arrive at a valuation multiple of just 1.2x EV/FY25 revenue.

Cheap - but cheap for a reason. Steer clear here as Domo continues to struggle with its growth trajectory.

Q3 download

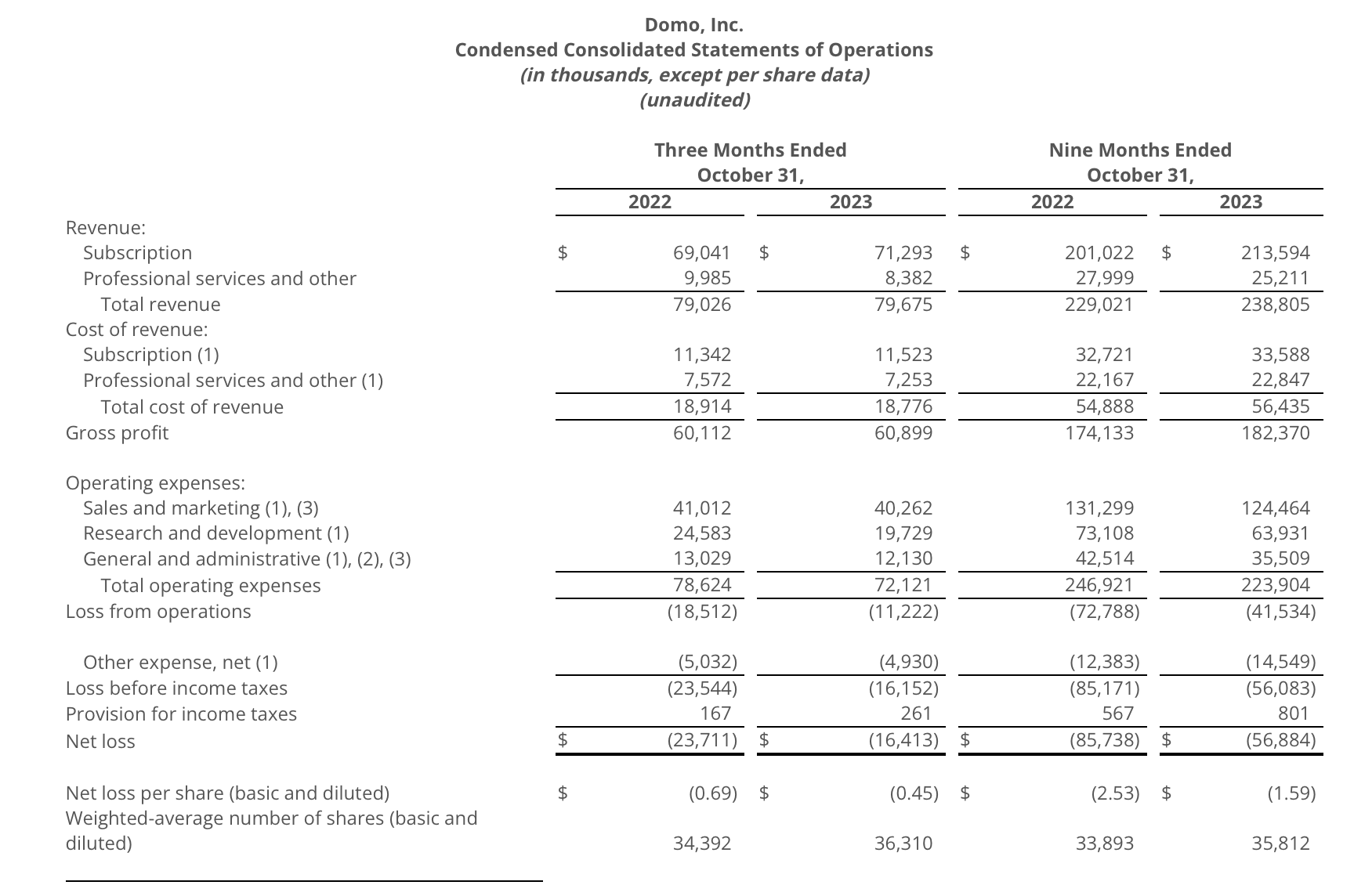

Let's now cover Domo's latest quarterly results in greater detail. The Q3 earnings summary is shown below:

{kind=link}

Domo's revenue grew just 1% y/y to $79.7 million, coming in slightly ahead of Wall Street's expectations of $79.0 million (flat y/y). Growth did, however, decelerate sharply from 5% y/y growth in Q2.

Billings in the quarter were $74.8 million, representing 1% y/y growth as well. As a reminder, billings represents the better picture of a software company's long-term growth trajectory, as it captures deals signed in the quarter that will be recognized as revenue in future quarters. In Domo's case, the fact that nominal billings dollars came in less than revenue, and growth on par, is a leading indicator that Domo's growth trajectory will continue to be challenged.

Again, the company is pinning its hopes on the transition to a consumption model and the potential wider net it's casting by opening up a freemium version of its product. So far, the company notes 20% of its ARR has shifted into consumption.

Per CEO Josh James' remarks on the Q3 earnings call :

Specifically, several years ago, we decided to test an idea: "What would customers do if they had unlimited access to features for an unlimited number of users and all visualization for free?" It was a simple value prop to customers. Pay for the value you are realizing. Well, after positive feedback we decided to run an even broader pilot last year, and the pilot proved to be a smash hit.

We now feel like we've reached critical mass with over 20% of our ARR on the consumption model. As we continue to look at the results from this very large sample size, we feel very confident in making the decision and saying we're going all in on consumption. By the end of next year, we expect to have the vast majority of our revenue on the consumption model.

Again, we now have over 400 customers on consumption contracts, representing over 15% of our customer base and over 20% of our ARR. When customers move to consumption, we are seeing user counts growing at almost 3 times the speed of seat-based customers. And we are seeing 3 times the adoption rate on premium features like data science."

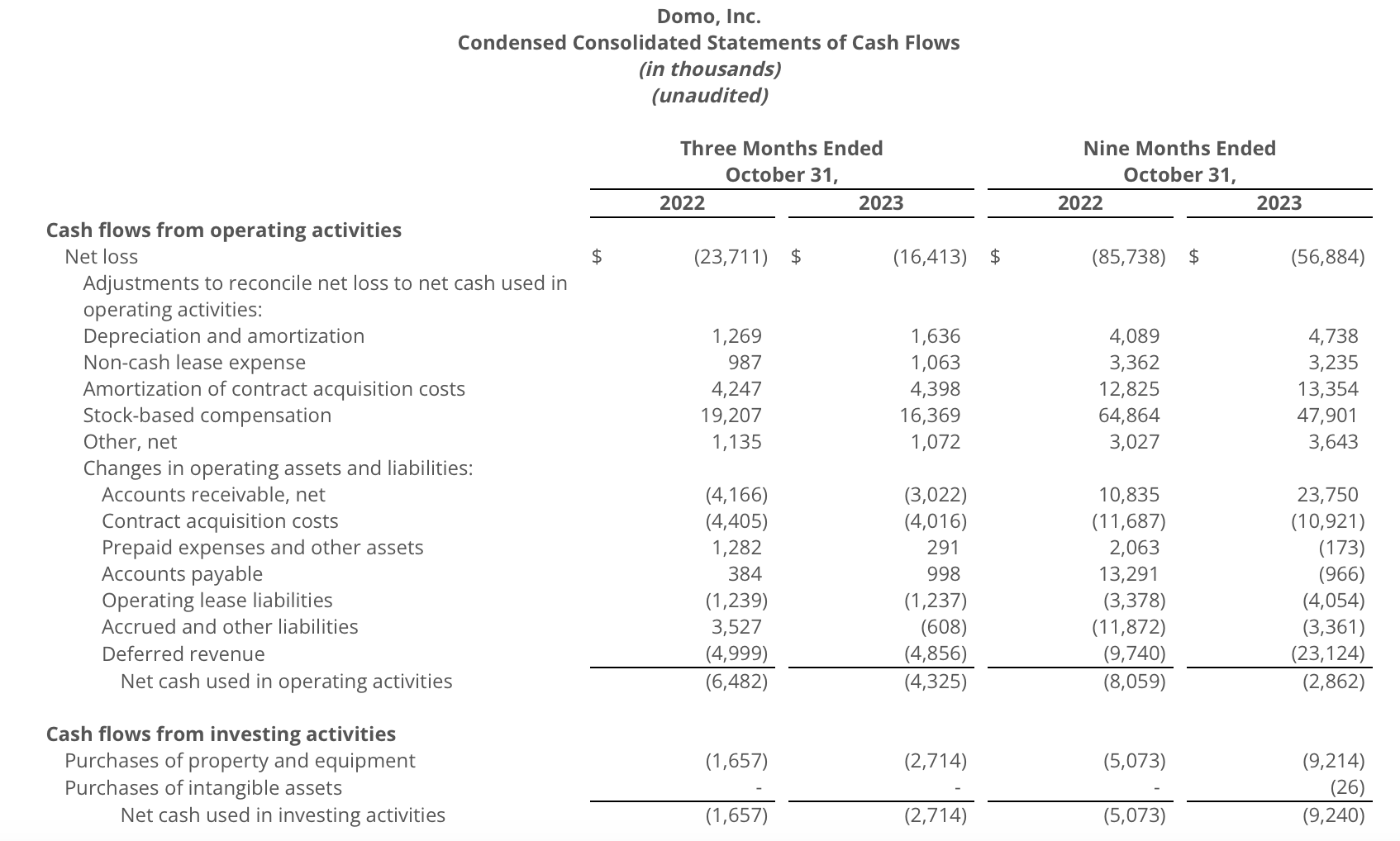

We should carefully watch Domo's resources, however. The company's headcount reductions have helped to stem losses (pro forma operating margins rose 6 points y/y to 3%, up from -3% in the year-ago Q3), but cash flow is still negative. Year to date, the company has burned through -$2.9 million in operating cash flow and -$12.1 million in free cash flow, including capex - compared to -$13.1 million in FCF in the year-ago period.

{kind=link}

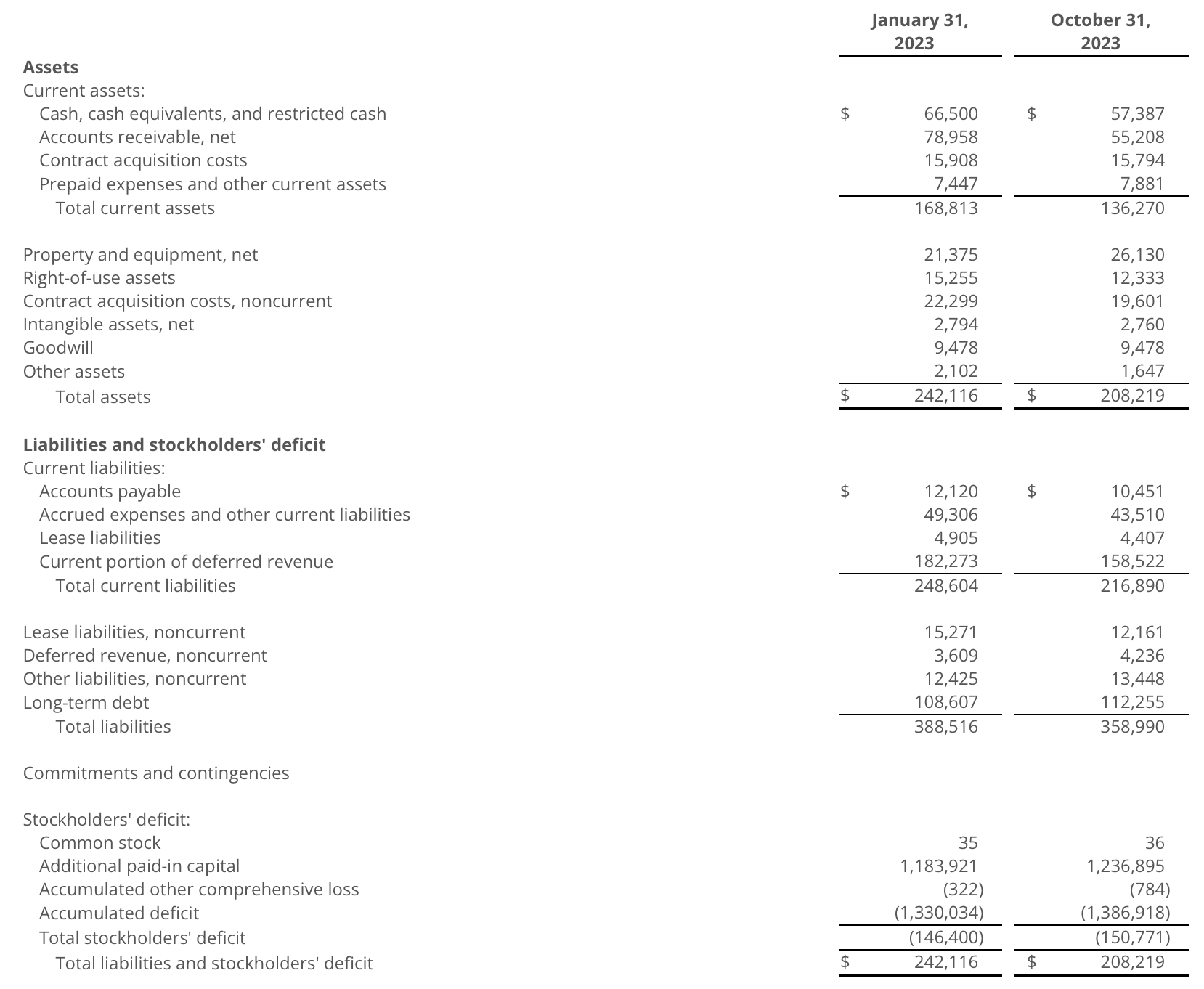

As of the end of Q3, Domo had just $57.4 million of cash left on its balance sheet - and that's more than offset by $112.3 million of debt:

{kind=link}

Key takeaways

In my view, a consumption-based billings model will do little to resuscitate Domo's growth profile. The company will run into a cash crunch soon if cash burn continues to be negative, and there just aren't enough reasons to stay invested in this name, even at a ~1x revenue multiple. Steer clear here and invest elsewhere.

For further details see:

Domo: No Rescue In Sight