DOMO - Domo: Stepping To The Sidelines After Recent Rebound

2023-04-25 09:15:12 ET

Summary

- Shares of Domo have rebounded ~15% year to date, even in the face of sharpening macro headwinds.

- In its most recent quarter, Domo's billings continued to decelerate to a y/y decline.

- The company is forecasting only single-digit revenue growth in FY24, as weaker enterprise IT budgets put pressure on Domo's ability to close deals.

- Domo is still cheap at ~2x forward revenue, but there are no near-term catalysts that can spark a further rally.

In a time of extreme market volatility, I continue to hold to the opinion that the best way investors can beat the market is to stock-pick very carefully, and part of that process involves cycling out names that have run out of rope to rally further.

Domo ( DOMO ), for me, falls into this category. The business intelligence software company has seen a generous ~15% year to date lift in its stock despite a visible slowdown in fundamental performance:

I was bullish on Domo earlier this year and doubled down on my position when the stock slid to the low-teens, but after seeing the company's latest fourth-quarter results which featured a sharp deceleration in billings, I'm changing my rating on the stock to neutral.

Now, I see Domo as a relatively balanced mix of positives and negatives. On the bright side for Domo:

- Business intelligence is a truly horizontal, wide-open market- Though many companies may be putting off their digital transformation projects in the face of current economic headwinds, the trends toward data mining and data visualization are incredibly clear and applicable to companies in all industries. Domo enjoys secular tailwinds in this regard that, in my view, are still in the early innings.

- High pro forma gross margins- Domo's subscription pro forma gross margins are north of 80%, which gives the company plenty of room to scale its operations profitably as it grows.

- Domo is focusing on profitability- In the wake of slowing growth rates, Domo has lasered in on reducing cost. The company recently broke even on a pro forma operating margin basis.

This all being said, we now have to be wary of:

- Dramatically slower billings growth rates- BI is a "nice to have," but not a "must have." In this environment where IT budgets are being cut, Domo implementations and deal closings are likely to get delayed, and in this time of weakness larger players like Tableau/Salesforce ( CRM ) and Microsoft PowerBI ( MSFT ) which are packaged as part of other "mission critical" software products may prevail.

- Though free cash flow positive, Domo has limited resources with less than $100 million of balance sheet cash. An unexpected downturn in new deals or a sharp decline in renewals may put Domo into a pinch if it is forced to raise additional capital.

From a valuation standpoint, Domo remains relatively cheap. At current share prices near $16, Domo trades at a market cap of $556.4 million. After we net off the $66.5 million of cash and $108.6 million of debt on Domo's most recent balance sheet, the company's resulting enterprise value is $598.5 million.

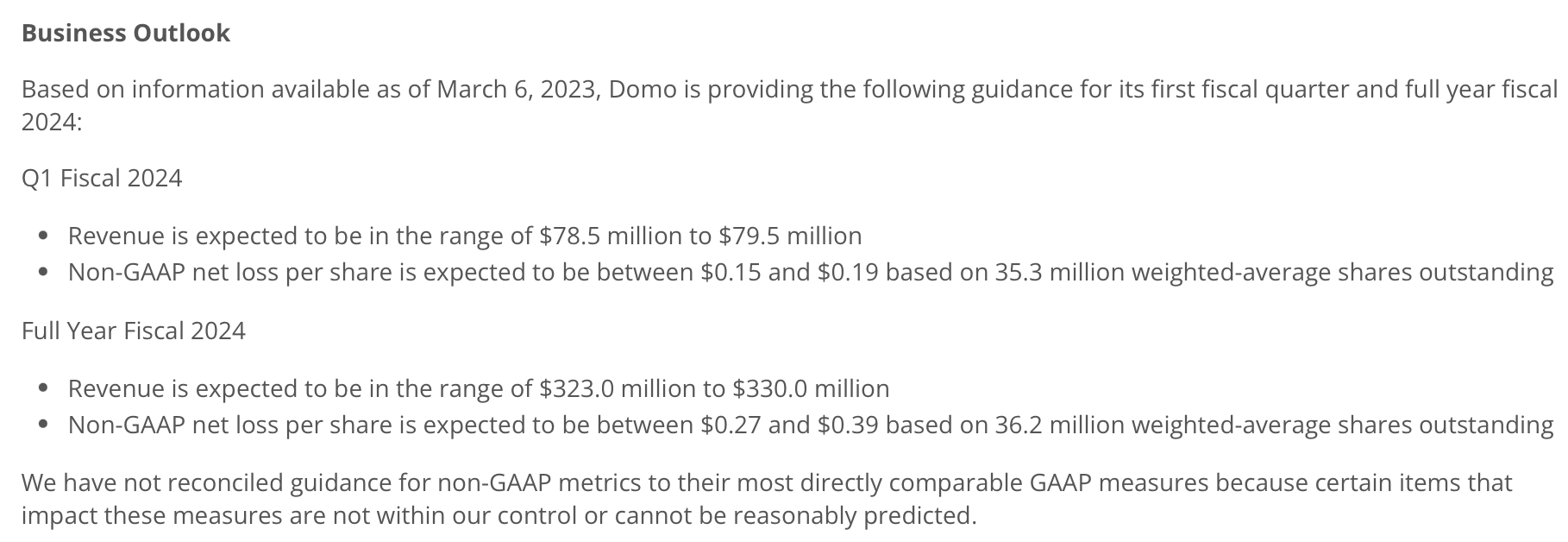

For the current fiscal year FY24 (the fiscal year for Domo ending in January 2024), Domo has guided to $323-$330 million in revenue, representing a growth range of 5-7% y/y:

{kind=link}

Note that while software companies usually tend to guide conservatively, I think this outlook is relatively fair considering Domo exited Q4 and FY23 at a billings growth rate of -3% y/y and +9% y/y, respectively.

The midpoint of this outlook puts Domo's valuation at 1.8x EV/FY24 revenue - which is cheap to be sure, but when Domo is looking at declining billings growth rates and no near-term catalysts to solve its demand issues, I think there won't be much room for an upward multiples re-rating.

The bottom line here: I'm moving to the sidelines on Domo. I'm interested in re-buying this stock if it touches back down to the $12 level, but until then I'm more comfortable de-risking this out of my portfolio.

Q4 download

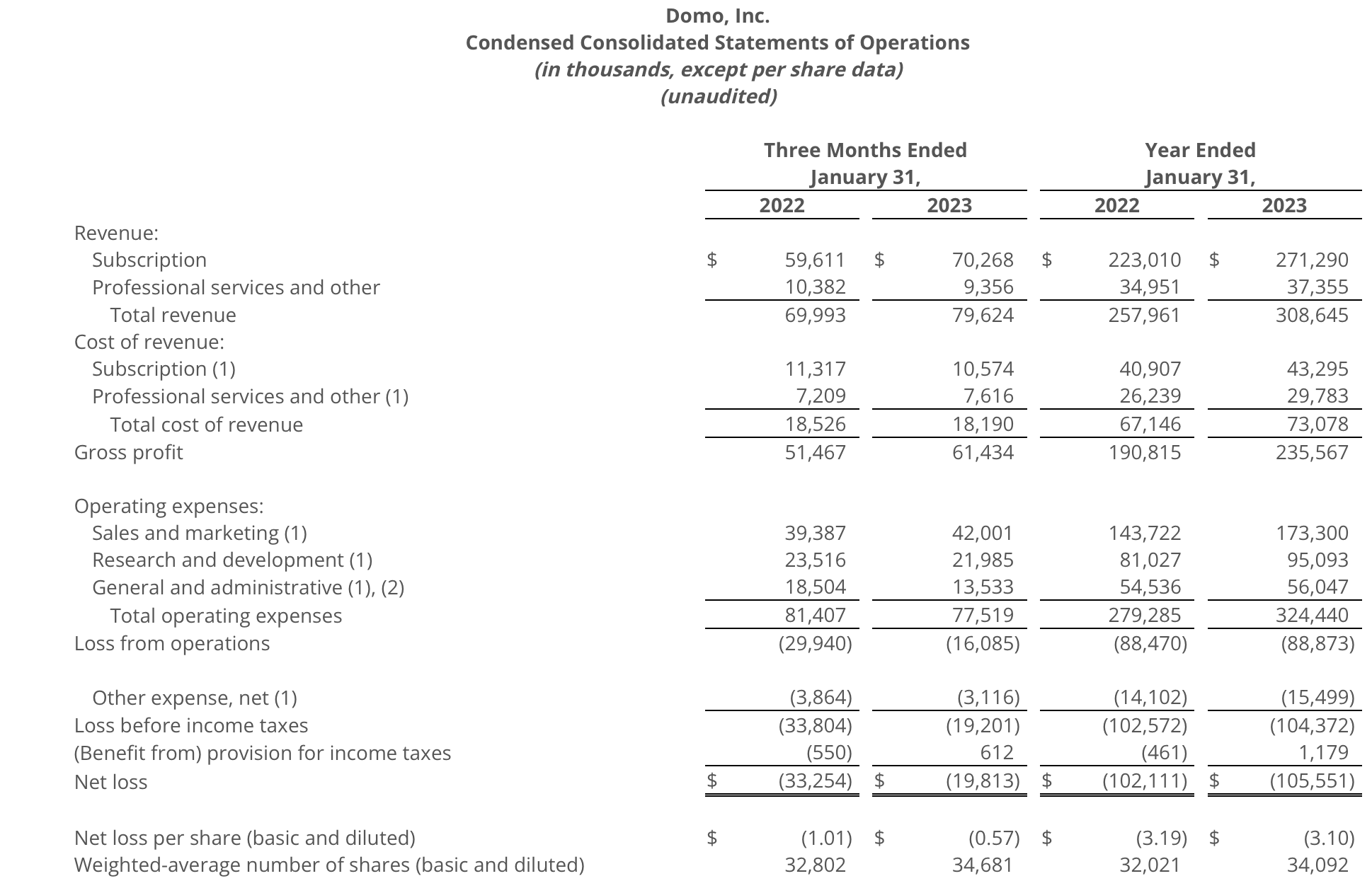

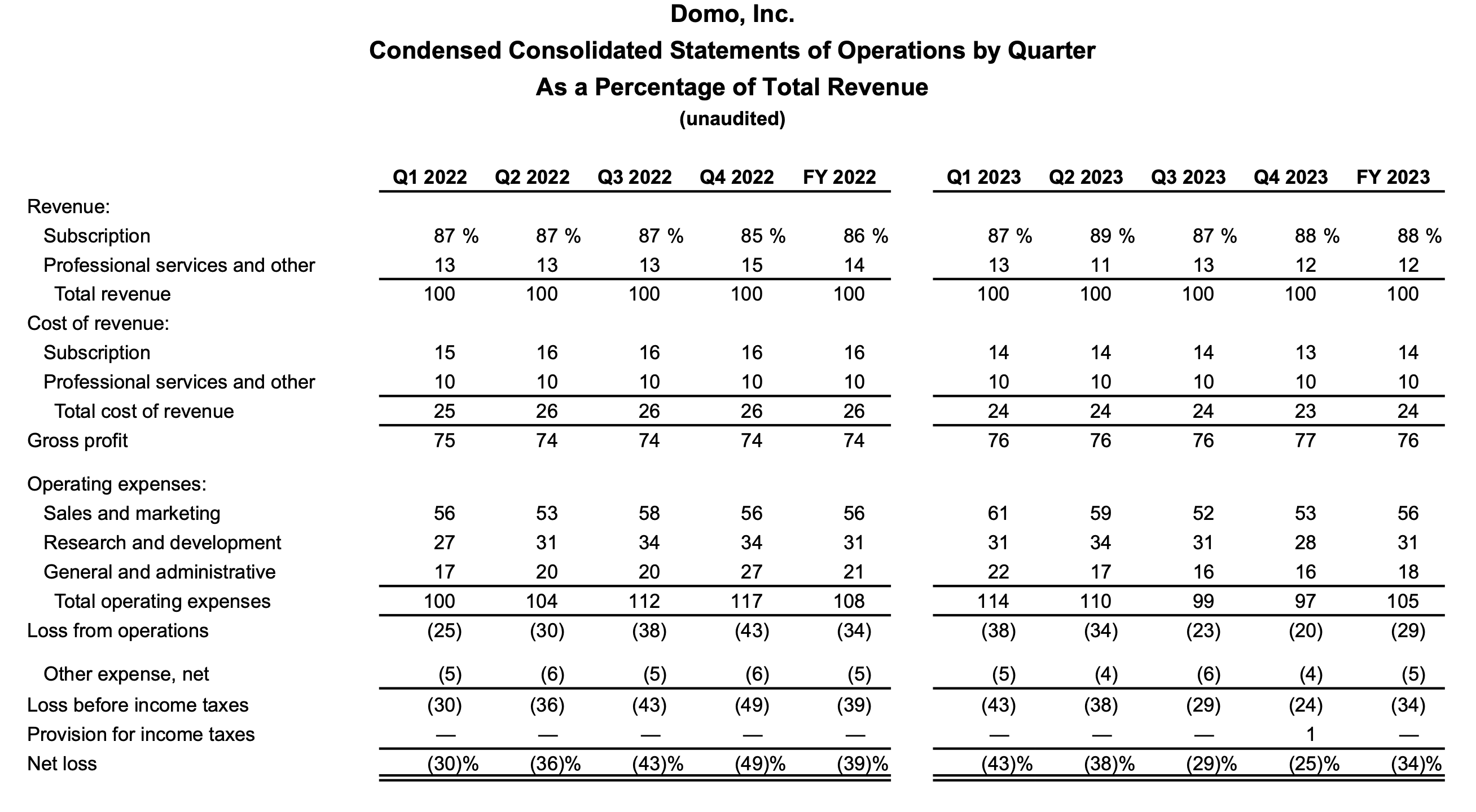

Let's now run through Domo's latest Q4 results in greater detail. The Q4 earnings summary is shown below:

{kind=link}

Domo's Q4 revenue grew 14% y/y to $79.6 million, beating Wall Street's expectations of $77.4 million (+11% y/y) by a three-point margin, as well as the high end of Domo's 11% guidance range. This being said, revenue growth sharply decelerated from 21% y/y in Q3, which was already evident in Domo's billings trends (which had decelerated to just 5% y/y growth in Q3).

Unfortunately, billings continued to slip in Q4. As shown in the chart below, Q4 billings landed at $104.5 million, down -3% y/y during a critical Q4 period (which usually represents a seasonal high mark as IT departments look to spend their budgets before the end of the year).

{kind=link}

As seasoned software investors are aware, Domo's billings slowdown is likely a leading indicator of revenue deceleration in the quarters to come - hence why Domo is implying revenue growth slowing to the mid single-digits in FY24.

There's one nugget of positive news here: Domo noted that its pipeline entering Q1 is higher than last year. This is good as it indicates potential in the quarter, but if enterprise demand continues to weaken and it can't convert this pipeline into sales, a strong pipeline is meaningless. Note that billings in Q1 are expected to continue softening to a -5% y/y trend, before rebounding to full-year growth in the back segment of the year.

Per CFO David Jollee's remarks on the Q4 earnings call:

We delivered Q4 billings of $104.5 million, a year-over-year decrease of 3%. This decrease was driven by a tough compare on the one hand, but also by a challenging macro environment that affected our new business growth in our renewal rates [...]

That said, we entered Q1 with more pipeline than we had a year ago. For Q1, we are guiding to billings of about $69 million, which is down 5% year-over-year. For full year billings, we are providing a range of approximately $335 million to $353 million, representing a range of 4% to 9% growth."

Cost management, however, is one of Domo's strengths as it manages through this slowdown. On a GAAP basis, net loss ratios in Q4 slimmed to -25%, twenty-four points better than the year-ago Q4, driven by improvements in gross margin as well as reductions in all categories of operating spend.

{kind=link}

Pro forma operating margins in Q4 also hit 3%, a fourteen-point bump to -11% in the year-ago Q4.

Key takeaways

Given Domo's recent rally in the face of tightening macro headwinds, and with the billings picture to stay dim at least through Q1, I'm inclined to step to the sidelines here. Watch for Domo to dip to the ~$12 levels before buying back in.

For further details see:

Domo: Stepping To The Sidelines After Recent Rebound