VTIP - Don't Be Misled By The CPI Headline Number: The Details Tell A Different Story

2023-05-10 13:30:19 ET

Summary

- The headline CPI numbers are being interpreted as confirming that the Federal Reserve will pause rates and then, most likely begin to lower them.

- The details of the CPI report paint a more complex picture which we go into here.

- The month-over-month numbers point to areas where inflation may be ramping up again.

- But a review of the CPI shows us why it is of limited value in predicting the Federal Reserve's future actions.

When it comes to the metrics used to gauge inflation, far too many investors look only at brief media supplied headlines instead of taking the time to look at the actual data. That is never more true than when the monthly Bureau of Labor Statistics CPI reports come out.

Today's headlines focused on the annualized inflation rate of 4.9%, which had dropped below 5% for the first time since May of 2021. Quite a few headlines went on to assure readers that this means the Fed will have to stop raising its rate. Since this is what investors want to hear, this interpretation of the CPI figures was greeted with delight. Treasury rates dropped across all but the shortest maturities.

Treasury Rates (as of 11:45 AM) After April CPI Report Release

Seeking Alpha

But if you blindly accept this analysis, you may be very surprised at what happens next. That's because the details of the actual April CPI report paint a different picture.

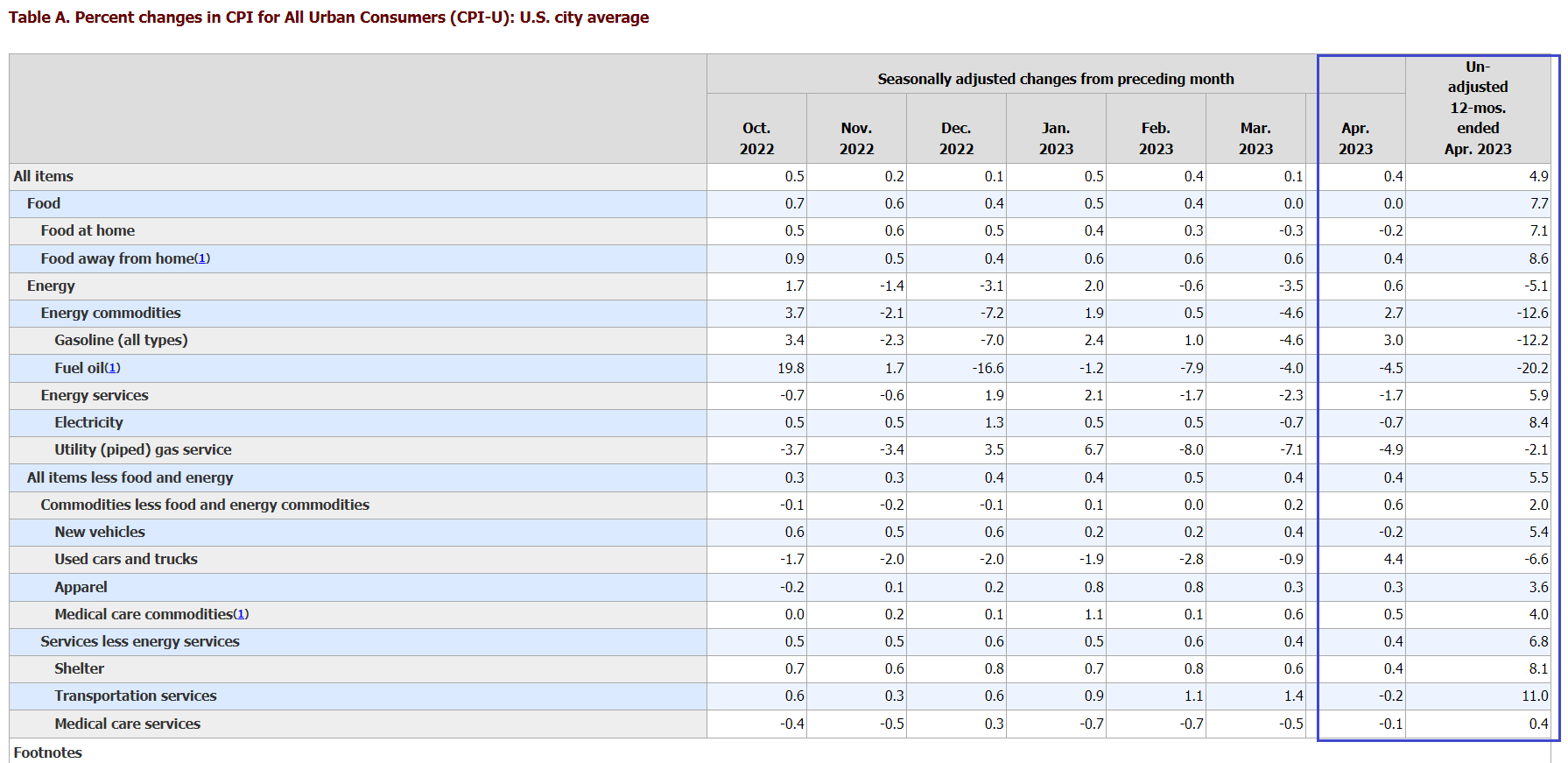

There Are Huge Differences Between Annual And Monthly Inflation Rates in CPI Report Subcategories

The actual CPI release can be read at the Bureau of Labor website . Below is the chart provided in that report that breaks out the inflation rate for the various categories used to tabulate both the CPI and the Core CPI (which excludes food and energy.) I have highlighted the most recent April data and the column showing the annualized inflation rate.

{kind=link}

The first thing that will strike you if you spend any time looking at this table is how big a gap there is between the unadjusted 12-month inflation rate and the month-over-month rate of inflation in each category for April 2023. Quite a few categories have dramatically lowered their annual inflation rates but have seen their month-over-month inflation rate rise in April. The reverse is true, too. As we will see, some of this is due to seasonal factors which are not adjusted in this data. But some of it may reflect forces that are still at work propelling inflation in a way that could lead to many more months of inflation tracking far above the Federal Reserve's 2% target.

Let's look now at the most significant disparities we see between annualized and month-over-month inflation.

Energy Costs Rose So Much in 2022 That Their Annualized Decline Can Be Misleading

The greatest decreases in annualized inflation have occurred in Energy-related categories: Energy itself and Transportation services. (Note that Transportation services, which rise in concert with gasoline prices, is a part of the Core CPI that is supposed to exclude food and energy prices.)

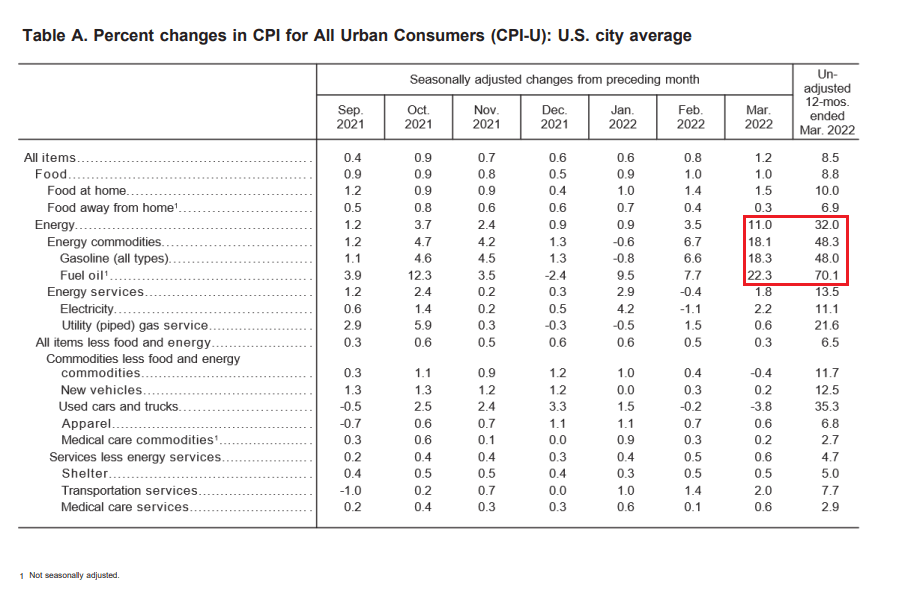

But investors need to remember that the decline in energy costs occurred after an extreme surge in those costs was caused last year after measures taken in response to the Russian invasion of Ukraine. Below you see the same CPI data we saw above as reported in the CPI report for March 2022 . This gives you an idea of just how dramatically energy prices inflated 13 months ago. Overall Energy costs continued to rise 3.9% in May of 2022 , and a whopping 10.4% in June.

{kind=link}

So, though energy prices have declined year-over-year when compared to a period during which they rose as much as 22.3% in a single month, their decline, though significant, has not been enough to bring energy prices down to a level anywhere near where they were before the Russian invasion. Furthermore, as the data above suggests, oil prices fluctuate dramatically from month to month. There is no reason to believe they won't continue to do this. And, when they rise, they raise the cost of transporting most of what moves on our highways, which translates into higher manufacturer costs and eventually higher prices.

If we break out Energy into the two categories reported in the CPI report, we see some interesting differences between them.

Fuel Oil Prices Are Misleading As They Are Highly Seasonal

Fuel oil heats most homes located outside of towns and cities in cold-winter regions like the Northeast. As you can see, fuel oil prices rose 22.3% last March but have been declining since December of 2022. They are still much higher than they were in January 2021. In addition, remember that people working from homes that are heated with oil are keeping their thermostats in the comfort zone all day rather than letting them drop while they are at work.

Heating oil is purchased in bulk, with most consumers only filling their 275 gallon tanks a few times a year. That is why the price usually drops dramatically in the summer when people aren't heating their homes but still have enough oil in their tanks that they can't yet order another fill.

As you can see from the data from both October 2021 and October 2023, when it starts getting cold, the price of heating oil surges again. It rose by 12.3% in October 2021, before anyone was thinking about Russia, and it surged a lot more in October 2022, when it rose 19.8%. It is very likely to surge this fall, again.

Gasoline Costs Are Rising Again

The data from this past month shows that after declining last month the rate at which the price of gasoline rose picked up again in April. This is also a seasonal effect. Gas prices like fuel oil prices are still far above where they were 3 years ago and will likely remain high unless we have the kind of recession that keeps people at home. Given the pressure on workers to return to the office and the extremely strong numbers we're seeing for employment, this isn't going to happen any time soon in the United States.

Annualized Housing Costs Have Risen Far Higher than that Headline 4.9%

Housing costs in the U. S. have continued to rise at an annualized rate of 8.1%. The month-over-month numbers do show that the rate of inflation is declining, but that the cost of housing continues to rise at a rate near 5%.

The slight drop in month-over-month inflation, in April 2023, from .6% per month to .4%, may also be a seasonal phenomenon. How many leases are written April to April? How many families buy homes in April? Relatively few compared to the summer months , since so many families move only when the school year is over. It won't be until the summer is well underway that we will have a better idea of how housing prices are changing.

There is, however, reason to believe housing costs will continue to soar--for reasons that don't show up in the CPI report.

Anecdotally I am hearing that the cost of appliances and of paying service people for repairs have forced landlords to raise rents just to stay solvent. Perusing the ads in my local paper, I note that even the cheapest household appliance prices are hundreds of dollars more than what they were three years ago. There is also a growing shortage of skilled tradespeople able to do the routine repair work needed to maintain older properties. Electricians and plumbers are in particularly short supply. This is pushing up the cost of those services, which in turn forces landlords to raise rents to cover their costs.

When we turn to home sales, the big news in housing is the lack of inventory . Fewer homes are being built than are needed for the population. Meanwhile, people who already own homes are not selling them to buy move-up properties and are only putting their homes on the market when forced to do so by death, divorce, the need for institutional care, or foreclosure. This is because they are locked into 2-3% mortgages and can't afford to finance homes of the same value as the ones they currently own, to say nothing of move-up homes. As a result of this home inventory shortage, in every market I'm familiar with the handful of homes coming onto the market are each getting from 3 to 10 or more competitive offers, which is continuing to push up the sales prices of these homes.

Used Car Prices are Surging Again

Though the annualized inflation rate for used car prices is down 6.6%, that rate reversed dramatically in April of 2023, surging 4.4% in a single month. This probably also reflects a seasonal effect: people who live in the regions of the country that experience winter weather with its salty, sandy roads, and follow up March Mud Season avoid buying cars until the weather gets nicer. It may also reflect the fact that the elevated cost of new cars and the higher financing costs are keeping people from selling their older cars. Even if interest rates were to come down, the prices of the new cars are not likely to follow them. Cars are likely to remain far less affordable for the foreseeable future.

The CPI's Categories Are Very Limited

Looking at the list categories reported in the CPI report, it should strike you how much is left out of this analysis. Most notably, the Services category only reports Energy, Transportation, and Medical Services. Think of how many other services we pay for: hairstyling, lawn care, appliance repairs, heating and cooling maintenance, day care, babysitting, dentistry... I could go on, but you get the idea. We see Food covered as a category, but what about all the other things you buy at department stores, hardware stores, and pharmacies both brick and mortar or online? Shampoo, toothpaste, hardware, over the counter pharmaceuticals, vitamins, dog treats, towels, sheets, children's toys?

This is one reason that the PCE report is preferred by the Federal Reserve's committee as it covers a wider selection of consumer items. The April PCI report won't come out until the end of May. The March report showed a significant drop in inflation, until we see that drop repeated in April, we have to be cautious. That's because the CPI for March reported a rise of only .1% but it has surged back to 4% in April.

Bottom Line: Inflation Is Far More Complex than the Monthly And YOY CPI Figures Suggest

After you have observed the CPI data and the very choppy way that its measure of inflation rises and falls from month to month and from category to category, you should be able to understand better why the Federal Reserve Governors are not going to conclude inflation is well under control any time soon.

The Fed Will Pause Far Longer Than the Financial Media Suggest

They may pause their rate hikes. But as Powell has repeatedly told us, if inflation looks like it is coming down when observed over a few brief months, they will still have held their rate constant "for some time." This is the only way they can be sure that inflation is really under control. "Some time," I believe, will extend into 2024, and possibly longer. And that's if inflation continues to decline, rather than stabilizing at its current 5% annual rate. Five percent is far, far higher than the 2% target the Federal Reserve is determined to achieve. And if inflation picks up again over the summer months, prepare yourself for further rate hikes.

Beyond that, don't invest on the assumption that we are soon going to see large rate cuts. No matter what the bond market might signal. The Federal Reserve board now knows how badly they erred in keeping rates too low, and spurring an epidemic of poor investing decisions by bankers and other executives. They also know now that were they to cut rates significantly that stimulus might kick off another inflationary surge.

Most importantly, the Fed must do what it was established to do. And as Jerome Powell points out in his press conferences, that mandate, which was put into law by Congress, orders the Fed to do two things: 1) do what it can to maintain a healthy rate of employment; and 2) control inflation.

Employment is healthier than it has been most of my life, with job shortages still very much a factor. Using the most optimistic numbers - like the CPI figures we have just looked at - inflation is still running around 5% a year. This rate of inflation, if it were to persist would double prices in just 14 years.

From this, I take it that we might get a pause in the Fed's rate raising campaign, but unless we see a good six or seven months of strongly declining inflationary pressures across a wide range of goods and services, it is very unlikely we will see rates decline.

There are Still Attractive Options Available to Retail Fixed Income Investors

Treasury rates continue to respond to investors' belief that the Fed will begin cutting rates very shortly. That means they no longer are appealing beyond the shortest maturities. But retail fixed income investors can still find excellent 3-5-year CDs rates in investments that don't attract large institutional investors.

The very best longer fixed income rates are available from Credit Unions. But brokered CDs offered by brokerages continue to offer far better yields than Treasuries even for people investing in taxable accounts.

I would suggest that fixed income investors still avoid investing in bond funds or exchange-traded funds ("ETFs"). Their current distribution yields are generally much lower than their stated SEC yields and those yields don't make up for the risk you take investing in a bond fund. If rates were to rise again, or stay at their current levels, your invested principal's value will decline for at least the length of the fund or ETF's stated duration. Since most popular bond funds have durations of 6 years or more, it makes no sense to invest in them when you can still get rates in the middle 4% range in well-chosen CDs.

For further details see:

Don't Be Misled By The CPI Headline Number: The Details Tell A Different Story