OGN - Don't Buy Viatris And Organon Just Because Of The Dividends

Summary

- Viatris and Organon are what can currently be described as "deep value plays" in the pharmaceutical sector. They face largely similar challenges, but on closer inspection are quite different companies.

- While I have already reported on Viatris' ever-changing portfolio, in this article I will take a closer look at Organon's portfolio and highlight the differences in strategy.

- In addition to comparing R&D spending and upcoming debt maturities, I will also discuss the current valuation of Organon and Viatris using discounted cash flow sensitivity analyses.

- I will outline why I ultimately decided to sell Viatris, even though I know the stock is cheap.

- In addition, I will explain why there are currently considerably better dividend investments with similar yields in the healthcare sector and provide some examples.

Introduction

As my regular readers know, I was originally very positive about the prospects of Viatris Inc. ( VTRS ), even after the announced sale of its Biosimilars division (see my February and May 2022 articles). However, my optimism faded after learning of management's acquisition of Oyster Point Pharma and Famy Life Sciences. In my November 2022 update, I argued that there were growing signs that Viatris was returning to a management style that was responsible for Mylan's long-term underperformance. Nevertheless, I rated the stock a "Hold" due to its still very strong free cash flow and cheap valuation. In the meantime, I sold my modest VTRS position because I have lost confidence in management, largely due to the way it communicated the recent transactions. Investor optimism is not helped by a management team that likes its decisions to go unquestioned, preferring instead to present shareholders with a fait accompli. Another important reason for selling my shares was the difficulty, not to say impossibility, of establishing a reliable baseline scenario due to the constant restructuring of the portfolio.

Having been intrigued by the - at least theoretically - favorable valuation of Viatris, I looked at Organon & Co. ( OGN ), which has a similar story in that it is a spin-off of a large pharmaceutical company (Merck & Co, MRK ). Organon and Viatris are in a similar situation - they have a huge debt mountain to shoulder, generate a significant portion of their cash flow from declining legacy brands, and have elusive growth prospects.

In this article, I will compare the two companies from different angles and conclude whether Organon is indeed a good replacement for Viatris, as a "deep value" pick in the healthcare sector. In addition, I will present cash flow-based valuations of the two companies and explain why there are currently better investments in the healthcare sector from a dividend investor's perspective and provide some examples. Since Organon and Viatris are expected to release their annual results on February 16 and likely at the end of February, respectively, I will also point out what I would look for in the earnings reports.

Overview Of Organon And Comparison With Viatris

Rather than go into detail about Viatris' business (see links in the introduction and my original article about the company), in this article I will give a brief overview of Organon & Co. and compare the two companies.

The very young company, which only went public in June 2021 , has a portfolio of around 60 therapeutics from Merck focused on women's health, particularly contraception and fertility, but also biosimilars (immunology and oncology treatments) and other therapeutics (cardiovascular, dermatology, respiratory and pain). While Organon represents about 15% of Merck's Human Health division by revenue, the company has to manage about 60% of all the division's stock-keeping units ((SKUs)), which likely makes managing SpinCo quite complex (slide 8, 2021 Merck Investor Day presentation ). At the same time, the fact that Organon operates six internally-owned manufacturing facilities, where the majority of its products are produced, is quite reassuring (slide 19, Merck Investor Day 2021 presentation).

Through the Women's Health segment, Organon markets contraceptive products such as Nexplanon (etonogestrel implant), NuvaRing (hormone-containing vaginal ring) and Cerazette (desogestrel, oral contraceptive), as well as fertility products such as Follistim (ovulation-regulating hormone) and ganirelix acetate (ovulation-regulating gonadotropin-releasing hormone antagonist). Nexplanon is a leading long-acting reversible contraceptive with U.S. market exclusivity through 2027 and estimated peak sales of more than $1 billion. In 2021, the product generated $769 million, up 13% year-over-year but roughly flat on a two-year comparison (slide 27, Merck Investor Day presentation). In the first nine months of 2022, Nexplanon grew 10% year-over-year. In fertility treatments, Organon is second only to Germany's Merck KGaA ( MKGAF , MKKGY ), which is the dominant player with 40% market share (slide 41, Merck Investor Day 2021 presentation).

The Biosimilars segment currently comprises Renflexis (infliximab, immunology), Ontruzant (trastuzumab, oncology), Brenzys (etanercept, immunology), Aybintio (bevacizumab, oncology) and Hadlima (adalimumab, immunology). Of particular note, Brenzys, Renflexis, Hadlima and Ontruzant are in direct competition with the highly successful immunology treatments Enbrel (Amgen, AMGN ), Remicade (Johnson & Johnson, JNJ ), Humira (AbbVie, ABBV ) and Roche's - RHHBY , RHHBF - tumor therapy Herceptin). Due to the success of these drugs, several biosimilars are now available, indicating fierce competition and thus problematic profitability. The segment is rather small (see below), but Organon - unlike Viatris - continues to develop biosimilars in-house. The company estimates that biosimilars sales can double by 2025 (slide 27, presentation at Merck Investor Day 2021), but that would mean only a 12% contribution to total revenue, assuming flat sales in Women's Health and Established Brands.

The Established Brands segment contributes the lion's share of Organon's sales, similar to Viatris' "Brands" segment, which includes drugs such as Lipitor, Lyrica, Celebrex, Viagra, and Zoloft. Organon's legacy segment includes 49 brands (slide 26, presentation at Merck Investor Day 2021), including Zetia (ezetimibe, cholesterol), Atozet (atorvastatin, cholesterol), Cozaar (losartan, hypertension), Singulair (montelukast, asthma), Nasonex (mometasone, asthma), and Arcoxia (etoricoxib, pain & various forms of arthritis)

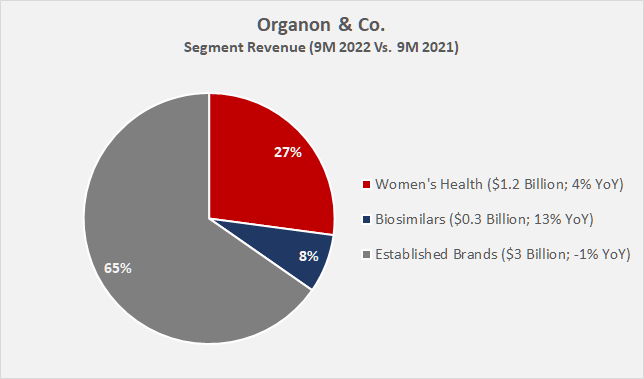

Figure 1 shows Organon's segment sales for the first nine months of 2022 and year-over-year segment growth rates. Organon was able to more than offset the decline in the Established Brands segment with growth in Biosimilars and Women's Health, resulting in overall revenue growth of 0.9% year-over-year.

Figure 1: Organon’s [OGN] segment revenues and year-over-year growth (own work, based on the data found in the company’s 2022 Q3 earnings presentation)

{kind=link}

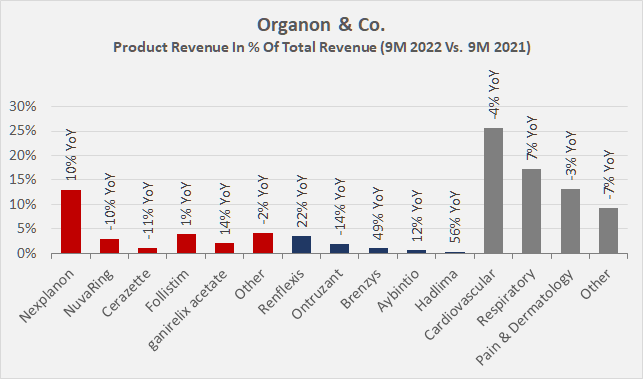

Figure 2 provides a detailed overview of the inner workings of the segments and shows the early stage of the important biosimilars Hadlima and Brenzys. In Women's Health, Nexplanon and injectable ganirelix acetate were the key growth drivers, as expected.

Figure 2: Organon’s [OGN] product and subsegment revenues and year-over-year growth (own work, based on the data found in the company’s 2022 Q3 earnings presentation)

{kind=link}

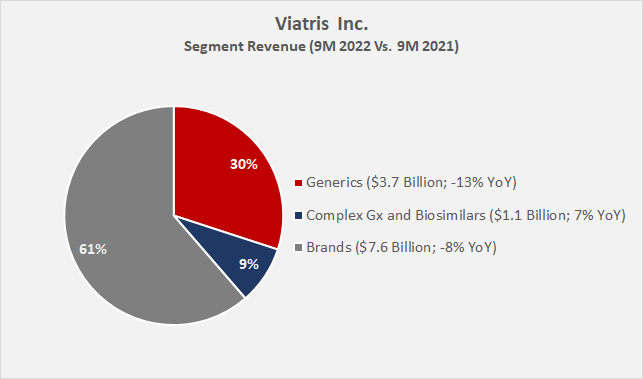

All in all, Organon's 2022 performance should be viewed as quite positive, given management's difficult position to offset declining legacy sales with growth in Women's Health and the still-not-very-significant Biosimilars segment, and the significant headwinds from foreign exchange in the first nine months of 2022 (slide 16, Q3 2022 Earnings presentation ). However, Viatris' performance was significantly worse over the same period, as the company reported an 8.4% year-over-year decline in sales. Both the Generics and Brands segments are losing sales, and the growing $1.1 billion contribution from the Complex Generics ((Gx)) and Biosimilars segment (7% year-over-year) hasn't helped much (Figure 3). Those unfamiliar with Viatris should know that the company sold its Biosimilars segment to Biocon Biologics in 2022 (while retaining a small equity stake), which will reduce segment sales by about one-third going forward, based on full-year 2021 sales figures.

Figure 3: Viatris’ [VTRS] segment revenues and year-over-year growth (own work, based on the data found in the company’s 2022 10-Q3)

{kind=link}

Both companies have global operations, but the appreciation of the U.S. dollar against other major currencies in 2022 cannot be used to explain Viatris' disproportionate revenue decline, given that both companies derive approximately 75% of their revenue from international markets (Figure 4).

Figure 4: Comparison of Organon’s [OGN] and Viatris’ [VTRS] revenue by geography, including year-over-year growth rates (own work, based on the data found in the companies’ 2022 10-Q3s)

{kind=link}

To counter declining revenues, Viatris announced that it would make acquisitions. I discussed the November 2022 acquisitions of Oyster Point Pharma and Famy Life Sciences in detail (see link in introduction). In short, growth remains elusive, not to say questionable, in my opinion. In the long term, Viatris plans to focus on ophthalmology, gastrointestinal, and dermatology in an attempt to move away from the low-margin generics business.

As shown in Figure 5, Organon is increasingly investing in R&D and has increased its guidance for R&D spending from mid to high single digits (as a percentage of revenue) to high single digits ( Q2 2022 Earnings press release ). In contrast, Viatris will likely again report declining R&D spending as a percentage of revenue. This fits the narrative that Viatris is increasingly trying to grow through acquisitions (not a particular strength of former Mylan executives, to say the least). To be fair, however, it should be added that Organon also completed acquisitions in 2021. Alydia Health , a medical device company focused on the prevention of postpartum hemorrhage and abnormal postpartum uterine bleeding, was acquired in June (total consideration $240 million). Forendo Pharma , which added an early-stage endometriosis therapeutic ( FOR-6219 ) to Organon's pipeline, was acquired in December for a total consideration of up to $954 million, including commercial milestone payments of up to $600 million. In February 2022, Organon acquired marketing rights for oral contraceptive pills in China and Vietnam from Bayer ( BAYRY , BAYZF ). A month later, Organon agreed with Daré Bioscience to license global commercialization rights for Xaciato (clindamycin phosphate, bacterial vaginosis) for a total amount of up to $182.5 million. I consider Organon's approach of growing through acquisitions but focusing on licensing rights and milestone payments to be quite prudent given its high debt (see next but one section). However, the company is clearly focused on organic growth, as evidenced by its much higher relative R&D spending compared to Viatris.

Figure 5: Comparison of Organon’s [OGN] and Viatris’ [VTRS] R&D expenses in terms of revenue (own work, based on the data found in the companies’ 2021 10-Ks and the 2022 10-Q3s)

{kind=link}

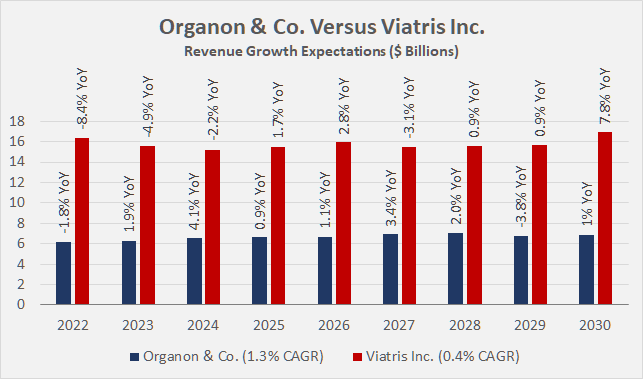

Analysts' expectations for future revenue growth at Organon and Viatris are quite muted (Figure 6), which is hardly surprising given the decline in the "bread and butter" segments of both companies. Nevertheless, I personally find Organon's story more compelling. The current portfolio of Established Brands seems more robust to me, and the Women's Health and Biosimilars segments show solid growth. Of course, given the complexity of developing and bringing biosimilars to market and the fierce competition, I would not overstate the profitability potential of the segment. In the case of Viatris, the expected sales and especially the expected earnings boost from the acquisition of Oyster Point Pharma seem very optimistic, not to say aggressive (see my previous article). In addition, Viatris will face further near-term sales declines due to upcoming asset sales, which will need to be replaced with therapeutics that can more than offset this decline and that of the base business. With R&D spending subdued, internal pipeline successes are unlikely to tip the scales, and Viatris' financial ability to grow through acquisitions is very limited. Finally, as I detailed in my previous article, it looks more and more like Robert Coury is still at the helm, whose acquisition-related performance is not the best, to say the least.

Figure 6: Comparison of Organon’s [OGN] and Viatris’ [VTRS] revenue growth expectations (own work, based on analyst estimates as published on www.seekingalpha.com)

{kind=link}

Viatris’ $20 Billion Debt Pile – How To Beat The Elephant In The Room?

In its Q3 2022 earnings presentation , Viatris management reiterated free cash flow ((FCF)) guidance of approximately $2.7 billion, representing a current FCF margin of 17%, which is undoubtedly a solid number. However, it is important to understand that FCF will decline going forward given asset sales and continued erosion of the base business unless management is able to reignite growth through R&D and/or acquisitions.

Management has promised to repay $6.5 billion by 2023. By the end of the third quarter of 2022, the company had already repaid $4.2 billion since 2021 and is definitely moving in the right direction. Viatris will not only use a significant portion of its FCF to repay debt, but will also use proceeds from asset sales for this purpose. As mentioned earlier, the company has sold its Biosimilars business for gross proceeds of up to $3.3 billion, but expects to raise an additional $6 billion through the sale of "non-core" assets. Recently, Advent was mentioned as a potential bidder for Viatris' consumer health assets.

One can rightly wonder what the core of Viatris is - I bought the company as a generics powerhouse that could expand its customer relationships through Pfizer/Upjohn's well-known therapeutics and geographic reach. However, it increasingly appears that management wants to focus on higher margin businesses in ophthalmology, gastrointestinal and dermatology, and possibly move away from generics in the future. That sounds good in theory, but management's M&A track record to date leaves much to be desired.

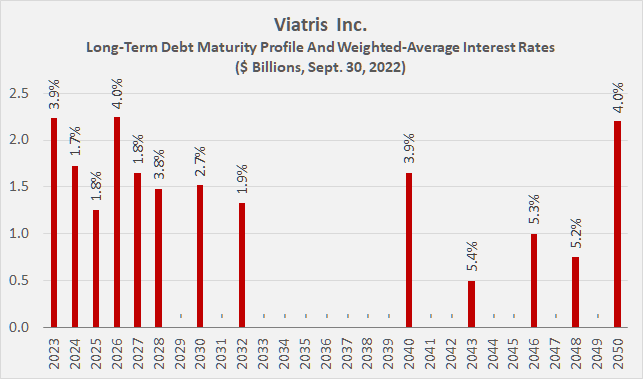

Viatris has a long-term issuer rating of Baa3 (BBB- S&P equivalent) with a stable outlook, which was affirmed in November 2022. However, in a later report in November 2022 , Moody's highlighted the execution risk associated with Viatris' change in strategy, but did not modify the rating or outlook. A renewed focus on acquisitions could delay the time to achieve Viatris' gross debt target of three times EBITDA, in part because the announced divestments will lower EBTIDA, and could lead rating agencies to potentially downgrade debt to junk levels. The maturity profile in Figure 7, based on data in Viatris' 2022 10-Q3 (p. 32), shows a total of $4.6 billion maturing in 2024, 2025, and 2027, with a very low interest rate. A refinancing of these notes in the current environment and possible negative actions by the rating agencies would understandably worsen the company's interest coverage.

Figure 7: Viatris’ [VTRS] long-term debt maturity profile; $976 million “maturing” in 2023 represent a JPY term loan facility and a USD revolving facility, estimated with a current weighted average yield of 4.4% (own work, based on the company’s 2022 10-Q3)

{kind=link}

While this all sounds quite negative, it is worth pointing out that Viatris recorded interest expense of $636 million in 2021 and should be expected to be less than $600 million in 2022. This translates to an interest coverage ratio of 5.5 times FCF before interest. If the FCF declines, the ratio will become worse, and refinancing of the 2024, 2025 and 2027 notes will also contribute to this. Of course, asset sales in principle work in the opposite direction, but I think it is prudent to question the process as a whole. After all, Viatris is consuming its own substance in order to be able to reduce debt, forcing itself to make risky acquisitions.

My biggest fear is that the company will slow down debt repayment after 2023 and focus on acquisitions, which could jeopardize its investment-grade rating. As for the dividend, I may have read too much into Coury's remarks during the Q3 2022 earnings call , but I still took notice when he again mentioned a "continuation of [the] dividend" and the launch of a $1 billion buyback program in 2023. Also, last year a dividend increase was announced in early January, while no such press release was issued this year. Perhaps the dividend will indeed be frozen at the expense of share buybacks, which would of course benefit the company's per-share metrics and thus potentially the relative market performance metric which is a part of management’s long-term incentive plan (e.g., p. 52 f., 2022 proxy statement ).

Organon – Half The Debt, Half The Problems?

At first glance, Organon's long-term debt of $9 billion appears far more manageable than Viatris' debt of nearly $20 billion, given that the company's FCF in 2021 was approximately $1.8 billion (i.e., an FCF margin of 29%). This results in a manageable but still significant notional debt repayment period of 4.7 years when using current rates, or 5.3 years when using management's 2022 interest expense guidance of $420 million. However, Organon's baseline FCF is likely much lower, as discussed below.

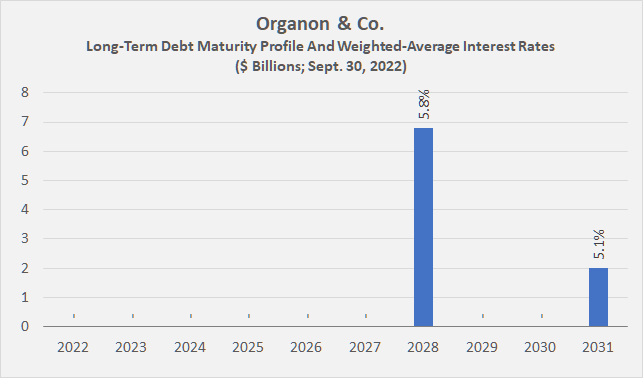

The key point is that Organon's long-term debt is rated non-investment grade ( Ba2, with a stable outlook ), unlike that of Viatris. From this point of view, it is hardly surprising that the interest burden is higher, as can be seen from the maturity profile in Figure 8, which also shows the weighted average interest rates. Problematically for Organon, 40% of its debt is floating at LIBOR plus 300 basis points, which puts it in a rather unfavorable position in the current environment. After all, the three-month USD LIBOR is currently 4.87%.

Figure 8: Organon's [OGN] long-term debt maturity profile (own work, based on the company’s 2022 10-Q3)

{kind=link}

Unlike Viatris, Organon has no maturities in the next few years, but due to the current high weighted average interest rate, interest coverage is only about 4.6 times 2021 free cash flow before interest. Worse, in the first nine months of 2022, Organon generated only $458 million in non-normalized FCF, compared to $1.98 billion in the same period in 2021. The company reported a $944 million increase in accounts payable in 9M-2021 (which increased operating cash flow) and a $323 million decrease so far in 2022. Normalizing working capital movements and adjusting for stock-based compensation, I estimate Organon's base free cash flow to be around $1 billion. That puts the company's FCF margin at 16%, which suggests room for improvement. As a result, and using management's projected interest expense for 2022, I estimate Organon's baseline interest coverage ratio to be 3.4 times FCF before interest.

Overall, I consider Organon's debt pile riskier than Viatris' due to its high floating rate component and lower credit rating, but I am more comfortable with the company's setup and growth prospects. The portfolio is more rounded and not subject to constant change, which makes it difficult to impossible to establish a baseline scenario for Viatris. So the better cash flow visibility would let me sleep more soundly as an Organon shareholder, even if its interest coverage is quite weak. Nevertheless, and even though I acknowledge that we cannot predict the future, the current weighted average interest rate already represents a very negative case given the aggressive rate hikes by the Federal Reserve in 2022.

Valuation And Verdict

Viatris began as a highly leveraged generics and biosimilars company with a number of solid legacy therapeutics. The company so far maintains its investment-grade rating, but needs to sell assets to get its debt under control. The divestiture of its Biosimilars segment was not a negative per se, but the fact that management is increasingly trying to steer the company away from generics to become a leader in ophthalmology, gastrointestinal, and dermatology seems to me to be a very risky proposition given the high debt and management's poor track record in mergers and acquisitions. Aggressive marketing of the acquisition of Oyster Point Pharma and its key product Tyrvaya during the Q3 2022 conference call hinted that Robert Coury is still at the helm, and the revenue and earnings estimates (why guide for "adjusted EBITDA" in 2028?) seemed overly optimistic to me. The future of Viatris raises many questions and provides few answers, and investor optimism is not exactly bolstered by a management team that likes its decisions to go unquestioned, preferring instead to present shareholders with a fait accompli.

At first glance, Organon looks like a much worse and riskier investment due to its non-investment grade rating and high proportion of floating rate debt. However, Organon's underlying business looks more stable than Viatris', is significantly less opaque, and management continues to follow its line since the spinoff from Merck in June 2021. Organon's business development initiatives are less risky and seem very appropriate to me overall. The company is not skimping on R&D investments, unlike Viatris, which is likely looking for the perceived "easy way out" by growing through acquisitions. Moreover, Organon's base business - the livelihood it was given by Merck to have a chance to shoulder its heavy debt load - is eroding more slowly than Viatris'. It will take a long time for the Women's Health division to become Organon's cash cow, but early indications are that the erosion of the base business can be held in check by growth in the other two divisions. At the same time, I remain cautious because sales growth is only part of the game. In terms of profitability, it will be a while before the Women's Health and Biosimilars divisions make a significant contribution, considering that Merck KGaA is a significant competitor in Women's Health and that biosimilars are difficult to develop and bring to market, and are largely commoditized these days.

For these reasons, it is hardly surprising that Viatris is cheaper than Organon - the market simply hates uncertainty, and Viatris has plenty of it. Given that both companies are highly leveraged, I think a valuation based on enterprise value ((EV)) rather than pure market capitalization is prudent. Figure 9 shows a comparison between the value of Viatris and Organon and that of Teva Pharmaceutical Ltd. ( TEVA ) and the much more robust and larger Novartis AG ( NVS , NVSEF ) in terms of EV/EBITDA and EV/sales. It is important to understand that these multiples-based valuations assume that the denominators (EBITDA and sales) do not decline significantly. Viatris is valued similarly to Teva, which is understandable given its ongoing challenges, while investors value Organon at a relative premium - likely for the reasons discussed above. Unsurprisingly, investors are paying a significant premium for diversification, size and reliability - after all, Novartis is nearly nine times the size of Organon in terms of sales. Moreover, Novartis' net debt of less than CHF 9 billion is almost negligible compared to a market capitalization of over CHF 170 billion.

Figure 9: Multiples-based valuation of Organon & Co. [OGN] and Viatris Inc. [VTRS], compared to peers Teva Pharmaceutical Ltd [TEVA] and Novartis AG [NVS, NVSEF] (own work, based on Novartis 2022 annual report, Teva’s, Organon’s, and Viatris’ 2022 guidance and third-quarter reports)

{kind=link}

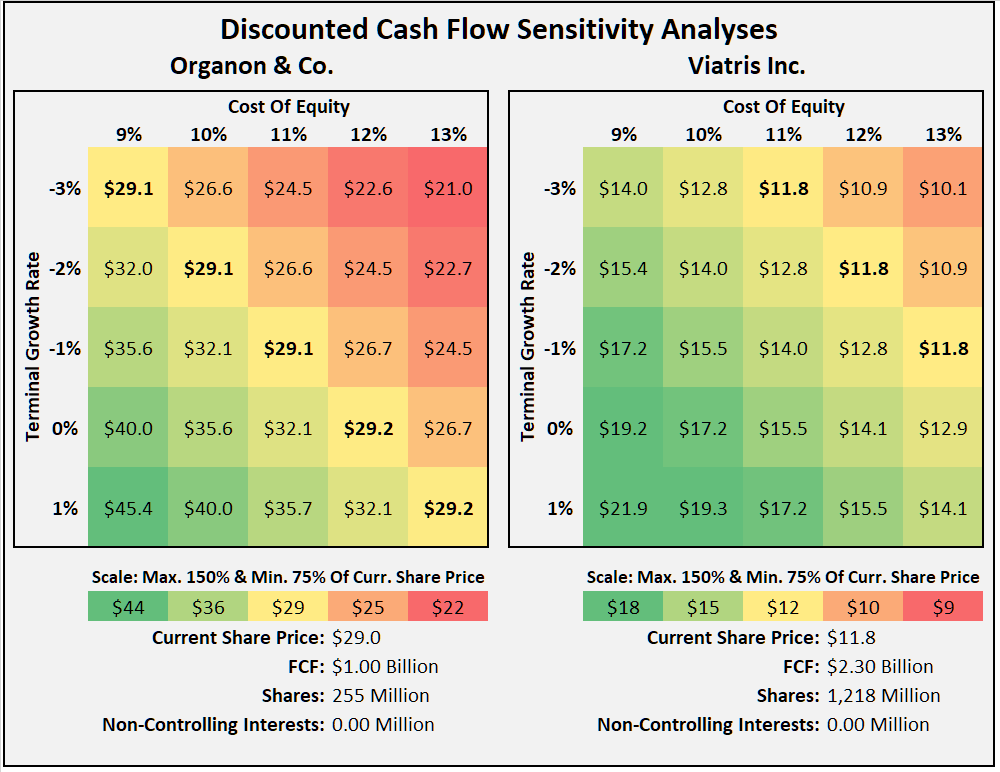

For the discounted cash flow ((DCF)) valuations, I used annual free cash flow of $1 billion for Organon, which is equal to or slightly less than CFO Matt Walsh's guidance at the Q3 2022 earnings call . For Viatris, I used $2.3 billion, which is less than free cash flow for 2021 and 2022, but in line with what CEO Michael Goettler projected for the period starting in 2024 on the Q3 2022 earnings call . As I've detailed before, this number is subject to significant uncertainty. In addition to the notorious susceptibility of DCF models to input parameters, this is another reason for performing a DCF sensitivity analysis instead of reporting a simple fair value estimate. Figure 10 shows the two analyses and confirms that Organon stock is more expensive than Viatris, but still quite cheap. Assuming an investor is comfortable with an 11% cost of equity, Organon's free cash flow can decline by -1% per year to justify the current $29 share price. At the same cost of equity, Viatris' stock price currently implies a decline of 3% per year, or an erosion of $550 million over ten years. Clearly, shareholders do not trust Viatris' projections of "at least $2.3 billion" for the future, assuming they are satisfied with a cost of equity of 11%.

Figure 10: Discounted cash flow sensitivity analyses for Organon & Co. [OGN] and Viatris Inc. [VTRS] (own work, based on management’s remarks during the Q3 2022 earnings calls, data from the 2022 10-Q3s, and own estimates)

{kind=link}

In a direct comparison, I would feel more comfortable as a shareholder of Organon, as the investment case is clearer, the baseline performance is more plausible, and even though the company’s debt poses a greater risk than Viatris’, which is still rated investment grade and largely consists of fixed rate notes. Organon's management seems more trustworthy to me, given the surprises that Viatris' management keeps coming up with. The lack of a dividend increase announcement in January is another disappointment, but who knows, maybe management will announce an increase along with the annual results, but I would definitely consider a frozen dividend as another broken promise by management. In contrast, Organon's dividend, currently representing a 3.9% yield, was always communicated as being paid out with FCF in mind. CFO Walsh noted back in August 2021 that the dividend payout was targeted at "low 20% of free cash flow", but did not rule out subsequent increases if Organon increases its free cash flow. However, there were no firm commitments on that front - unlike Viatris' CEO Goettler said in his remarks during the Q4 2021 earnings call :

Our financial commitments for Phase I, so that's the year '21, '22 and '23, remain unchanged: pay down $6.5 billion in debt, achieved $1 billion in synergies and grow our quarterly dividend to return value to shareholders.

As a result, I do not consider either Organon or Viatris to be a good investment from a dividend growth perspective, although I believe Organon could surprise investors positively if management is able to reignite growth. However, as a dividend growth oriented investor, I believe there are better investments in the pharmaceutical sector with similar or slightly lower dividend yields and better balance sheets. For example, I recently covered Pfizer ( PFE ), which currently yields 3.70% and has a promising pipeline and robust base business (excluding Comirnaty and Paxlovid). Amgen also appears to have returned to at least fair value territory, currently yielding 3.55%. I was not quite as bullish as the broader market after the stock reached nearly $300 following the earnings release (see my update ), but am still quite positive about the company's prospects, as I pointed out in a previous analysis . In particular, I appreciate the shareholder-friendly attitude of Amgen's management. AbbVie is arguably riskier due to its high debt, as is indicated by its dividend yield of 3.94%, but its bold acquisition of Allergan is bearing fruit, and its pipeline and already-approved drugs (e.g., Skyrizi and Rinvoq) appear increasingly capable of offsetting Humira's decline.

What To Look For In The Upcoming Earnings Reports

Finally, with full-year results due on Thursday (Organon) and likely closer to the end of February (Viatris), I would like to point out what I would look for as a shareholder or as an individual interested in investing in either company:

- Have the Women's Health and Biosimilars segments continued to show growth, and are sales expectations for Established Brands relatively flat? Is it reasonable to expect a significant cash flow contribution from Biosimilars in the near term - is there any guidance from management in this regard?

- Has Viatris' guidance been changed yet again? What about Oyster Point's contribution - were there signs of management sandbagging revenue and earnings guidance? After all, Tyrvaya was praised with great emotion during the Q3 2022 earnings call.

- Have any other acquisitions been announced at Viatris? If so, do they fit, and are cash flow contribution expectations realistic?

- Does Viatris' management remain committed to the guidance of $9 billion in proceeds from asset sales? I would watch for any adjustments or non-cash proceeds, as in the case of the Biosimilars transaction.

- Free cash flow guidance should be closely scrutinized at both companies, with a focus on potential adjustments. For Organon, I would expect a "mean-reversion" in free cash flow due to a decline in working capital, and I would review Viatris' guidance in the context of CEO Goettler's earlier long-term guidance of $2.3 billion annually.

- I do not expect Organon to increase its dividend, but there is still a possibility that Viatris management will announce an increase. After all, management originally committed to an increasing dividend. Consequently, I would view the lack of an announcement quite negatively and as confirmation of my distrust.

- At the end of the third quarter of 2022, Viatris reported $750 million of 3.125% notes and $500 million of 4.200% notes due 2023. Does management intend to repay the notes as announced? Has there been any news regarding the announced share repurchases?

- At the end of Q3 2022, Viatris reported $750 million of 3.125% notes and $500 million of 4.200% notes which mature in 2023. Does management intend to retire the notes as previously announced? Was there news regarding the previously announced share buybacks? Does management remain committed to further deleveraging?

Thank you very much for taking the time to read my article. How did you like it, my style of presentation, the level of detail? If there is anything you'd like me to improve or expand upon in future articles, do let me know in the comments section below.

For further details see:

Don't Buy Viatris And Organon Just Because Of The Dividends